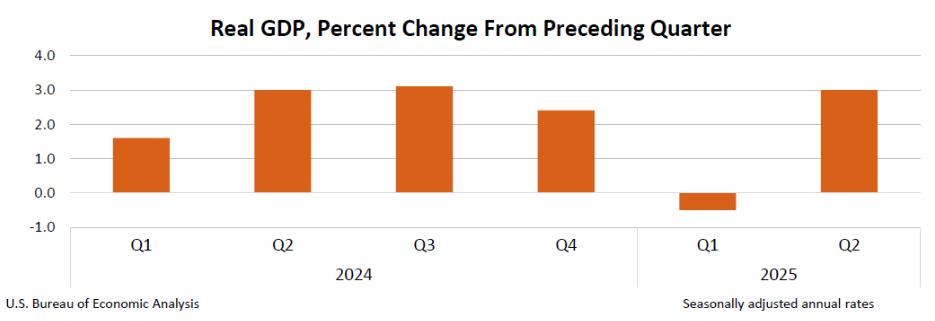

There was some impact from accounting related to foreign imports, which had the reverse effect that was seen in the prior quarter’s slightly negative GDP growth rate, which we explained on April 30 (Markets Sell Off on Negative GDP Report).

The way economists calculate GDP, a decrease in imports tends to register as an addition to GDP growth. Imports fell in the second quarter following a higher level of imports in the first quarter, in anticipation of tariffs.

Nonetheless, the economy is performing well, with unemployment rates low and inflation approaching the Fed’s stated 2% target. The PCE Price Index grew at 2.1% in the quarter. Excluding food and energy, the index grew at 2.5%.

There are pockets of weakness in the economy, however, as today’s jobs report underscores.

High interest rates are doing the very job they were intended to do—apply pressure to households by raising borrowing costs.

Consumer spending growth was 1.4%. We are still in positive territory, but consumers continue to feel the pinch of high interest rates on auto loans, credit card balances and mortgages.

This leaves room for a new Fed chair, whether he or she arrives in May of next year or earlier, to push for lower rates, which will be helpful for stocks.

Bond markets are already signaling a lower rate future ahead. Yields on 10-year Treasuries have slid down to the 4.25% range. They were close to 4.6% in May and peaked just under 4.8% in January.

An economy that is intact and growing but has room for rate cuts represents a nice set-up for investors in stocks. Today’s job report signals some economic weakness but serves as a strong talking point for Fed governors advocating for rate cuts at future meetings.

(2) Major trade deals are done.

The U.S. has already secured trade deals with its most important trading partners, including China, Japan, and most recently the EU.

Key elements of the deal with the EU involves commitments by European nations to purchase American energy as well as cooperation on technology and AI standard setting, which will benefit American tech companies.

There are still a number of unresolved trade agreements, and perhaps a few of these frozen negotiations will lead, at least temporarily, to high tariff rates getting applied to these countries.

But none of these unresolved trade relationships have the potential to cause material damage to the U.S. economy to the extent an acceptable middle ground cannot be found.

(3) AI is happening.

Without diminishing the importance of broad economic indicators and trade deals, what long-term stock market investors should perhaps be most focused on is the trajectory of the AI growth story.

If we rewind a year ago or so, most market observers were thinking about AI as having great future potential as initial investments in AI computing capacity were underway.

Earlier this year, enthusiasm for the AI theme waned after investors misinterpreted the significance of DeepSeek, a Chinese AI start-up.

But as investors have listened in recent months to what the companies most directly involved in AI have been telling them, confidence in the theme has been restored. This week, we got yet more evidence that the outlook for AI is as robust as ever.

Companies are continuing to invest heavily in AI, which has ramifications for stocks across multiple sectors as well as the economy as a whole. But perhaps more importantly, they are truly profiting from AI and developing an ever-growing list of use cases.

Shares of Microsoft (MSFT) and Meta (META) advanced sharply yesterday after earnings reports. MSFT closed up 4% on the day, while META advanced 11%.

MSFT’s cloud-computing Azure segment exceeded expectations, fueled by enterprise demand for AI-driven productivity tools. META described how AI-enhanced ad targeting and content curation is driving revenue and making the business more efficient.

An encouraging outlook on multiple fronts

Eventually, and potentially within the next few months, trade deals will be settled with all the major counterparties. Once this happens, it will remove a key source of uncertainty from the stock market and provide decision-making clarity for businesses that are heavily connected to foreign trade.

The economy has momentum but appears nowhere close to “overheating.” A strong case is emerging to start giving pressured consumers more relief in terms of lower interest rates, which still remain at levels designed to constrict economic activity.

Within the economy, AI is the industrial trend that matters most.

This point is not lost on the current administration, which appears to be doing everything it can to create a helpful regulatory infrastructure for continued AI development and deployment.

As AI reshapes the economic landscape, when evaluating any stock for potential investment, it has at this point become essential to think carefully about how the growth and proliferation of AI will impact the company’s long-term business prospects.

Not all of our Model Portfolio holdings are direct AI beneficiaries, but we apply the AI lens to every idea. The goal is to have stocks that will benefit, directly or indirectly, from AI trends, or at the very least not have their business models disrupted by innovations in AI.

Our American Resilience Model Portfolio, which focuses on quality growth opportunities, has the most direct exposure to the AI theme, with positions diversified across multiple industry sectors.