The reality of tariffs and inflation

Tariffs are a form of taxation on businesses, not too different from corporate income taxes.

When the government taxes certain goods, in this case foreign goods, there is always the potential for one-time price increases to be passed through to consumers.

Similarly, when the federal government raises corporate income tax rates, businesses may compensate by raising prices to maintain after-tax profitability. This effect has been demonstrated by economists but is rarely discussed in the financial media.

If we have learned anything over the past few months, tariffs are also flexible. To the extent certain tariffs do create an inflationary bottleneck, they can be adjusted.

It is clearly not the goal of the administration, with Trump’s repeated calls for lower interest rates, to create inflationary pressures.

It is also not the goal of the Trump administration to damage the stock market, which underpinned our bullish stance on stocks during the tariff tantrum (Will Trump Pivot?).

The nice thing about “self-inflicted wounds,” as Summers phrased it, is that they can be quickly reversed.

A healthy backdrop

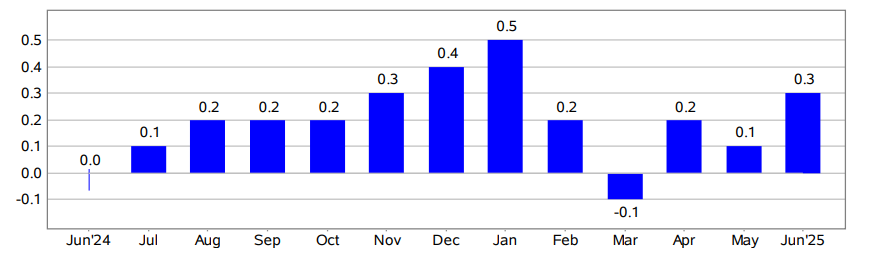

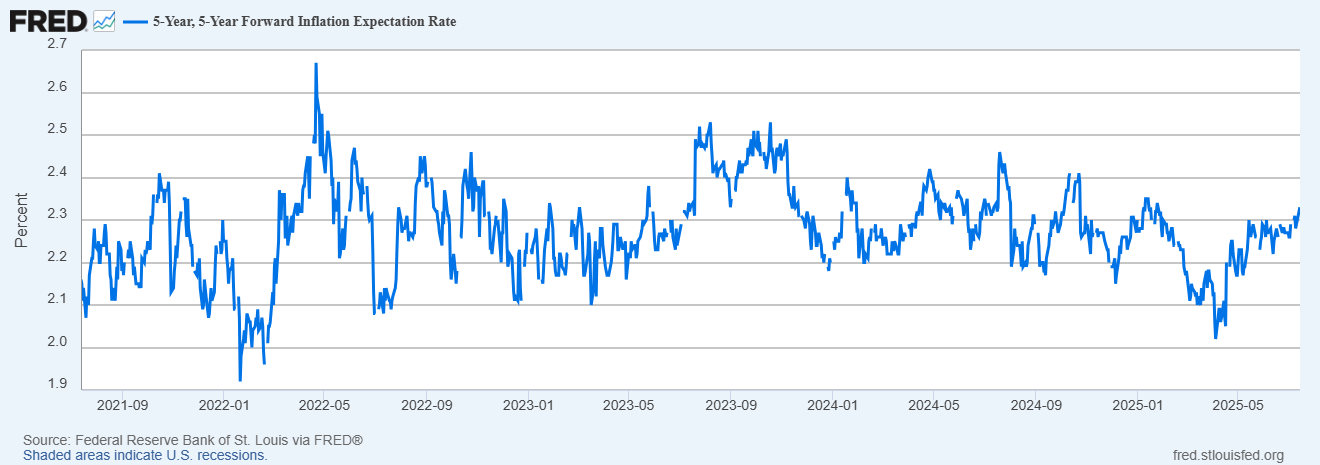

The market’s growing comfort level with the inflation outlook makes sense to us. Investors are more focused now on the growth trajectory of individual companies and positive news flow around the AI theme.

Today, shares of NVIDIA (NVDA), which made news last week when its market cap broke $4 trillion, advanced even further.

NVDA is up today more than 4% and on track to close at another all-time high above $170 per share. This comes in reaction to a policy shift that permits the sale of less advanced semiconductors within China.

We see a generally encouraging macro picture: moderate inflation, strong employment, high levels of tech-driven investment.

With a pro-growth administration pressing its economic agenda forward, it makes sense for investors to focus their energies on the many interesting opportunities that are out there across industry sectors.