Tech stocks have been under pressure as the market responds to a developing threat: will innovation in AI actually hurt the profitability of the technology sector itself?

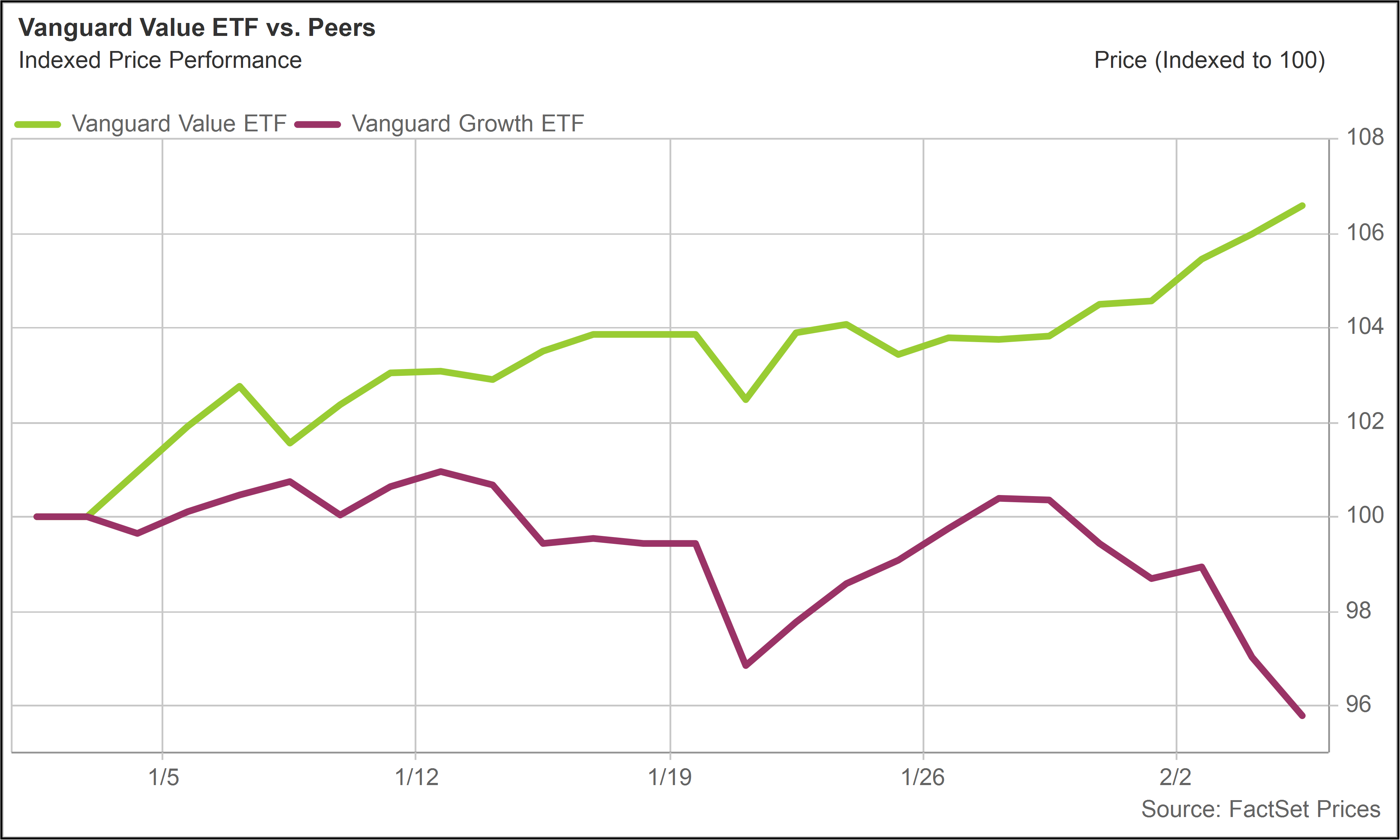

The tech-heavy NASDAQ Composite was down 1.5% today, following a 1.4% decline yesterday. The NASDAQ is now flat for the year, as investors rotate into other areas. The S&P 500 Value Index is up more than 3% so far this year.

A major factor behind the pressure on tech stocks this week was Anthropic, the AI start-up founded in 2021 by former OpenAI researchers.

Anthropic is known for its Claude large language model, which competes with OpenAI’s ChatGPT and other AI models. Backed by Amazon (AMZN) and Alphabet (GOOGL), as well as leading venture capital firms, the company is said to be targeting an Initial Public Offering later this year.

Anthropic has begun rolling out what it calls Claude Cowork plugins. These are productivity tools that automate real work tasks in legal, sales, and other business workflows.

These are not just fun demos; they are real tools designed to handle document review, legal compliance, contract triage, customer service workflows and other use cases. Most of these functions are currently addressed by other companies that offer them as high-value software services.

In other words, Claude is now offering potentially valuable services to its premium subscribers—at no incremental cost to them—that are currently being provided by other companies.

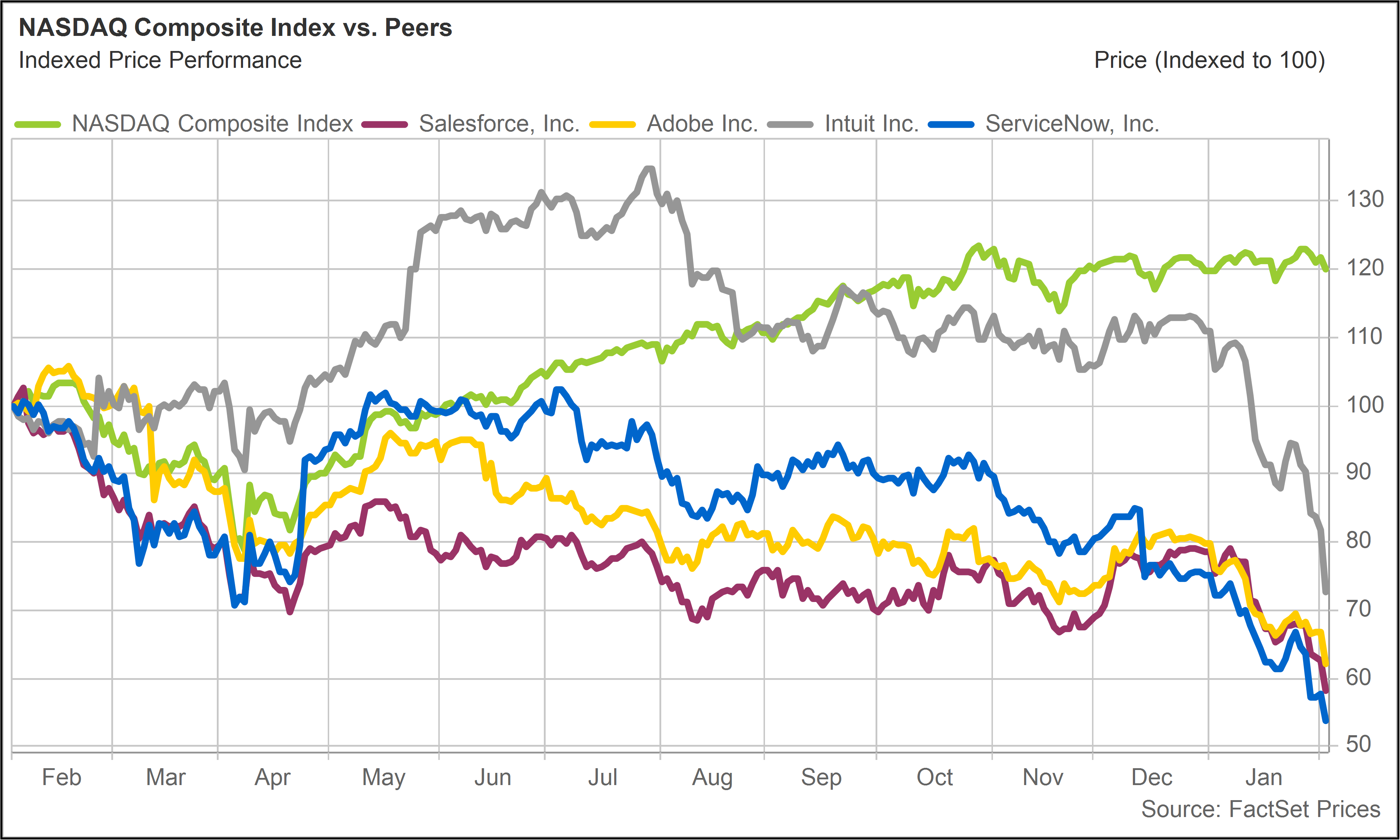

A number of high-profile technology and information services stocks have declined sharply, based on this specific development and the broader threat of AI disruption.

After all, it is not as if Anthropic—or, for that matter, the other major AI model providers—are done innovating and introducing new features.

Consumers could soon be getting for free what they used to have to pay through the nose for.

The end of SaaS?

Software-as-a-Service (SaaS) refers to the evolution of the software industry from a licensing model (much more common ten or twenty years ago) to a subscription model. Instead of buying software once and installing it on their computers, customers pay a recurring subscription charge to access the software over the internet.

SaaS was made possible by the development of cloud computing and created enormous value for both customers and businesses. Customers benefited from ease of use, continuous updates, and centralized hosting. Vendors locked in predictable, high-margin recurring revenue streams that were rewarded by the stock market.

But what happens if many of the core functions provided by these various software service providers come free with an AI subscription plan?

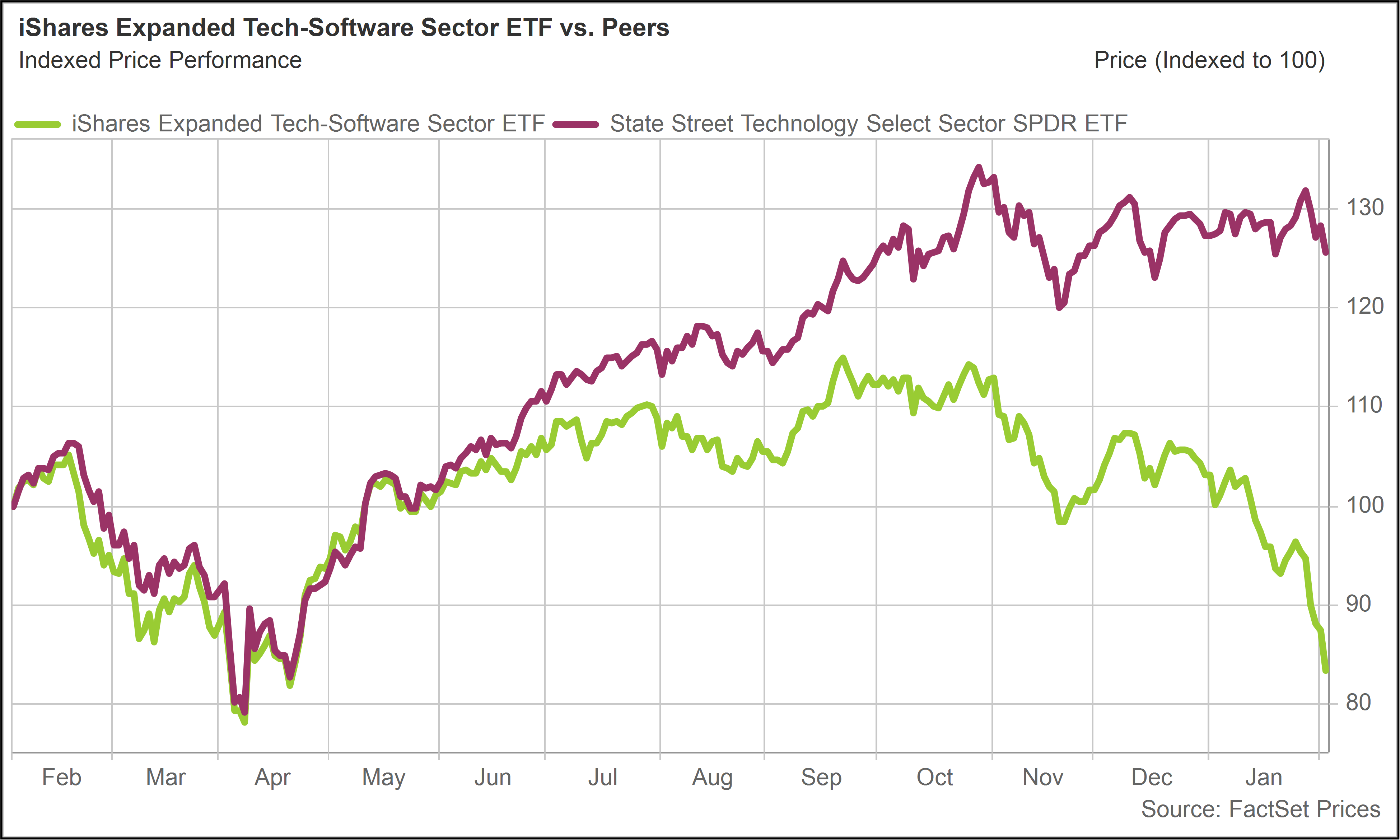

While the announcement by Anthropic has hit a number of stocks particularly hard this week, the weakness in software has actually been something of a slow motion trainwreck since last summer.

Staring in June 2025, the performance of software stocks has departed visibly from the broader technology sector. This is quite noticeable when we compare the returns of the iShares Expanded Tech-Software ETF (IGV) versus a less narrowly focused technology fund like the State Street Technology Select ETF (XLK).