Over the past several weeks, Bitcoin and other digital assets have faced renewed volatility and downside pressure. Today is no exception: Bitcoin has slipped below $100,000 as tech stocks trade sharply lower, unwinding a portion of their strong gains from recent months.

As always, we encourage subscribers to respond to market turbulence cautiously—but also opportunistically. With crypto as an asset class under pressure, we are seeing various pockets of opportunity emerge.

In traditional markets, declining prices tend to attract value-oriented buyers. That demand often prevents prices from falling too far. But in crypto, buyers with that mentality are largely absent.

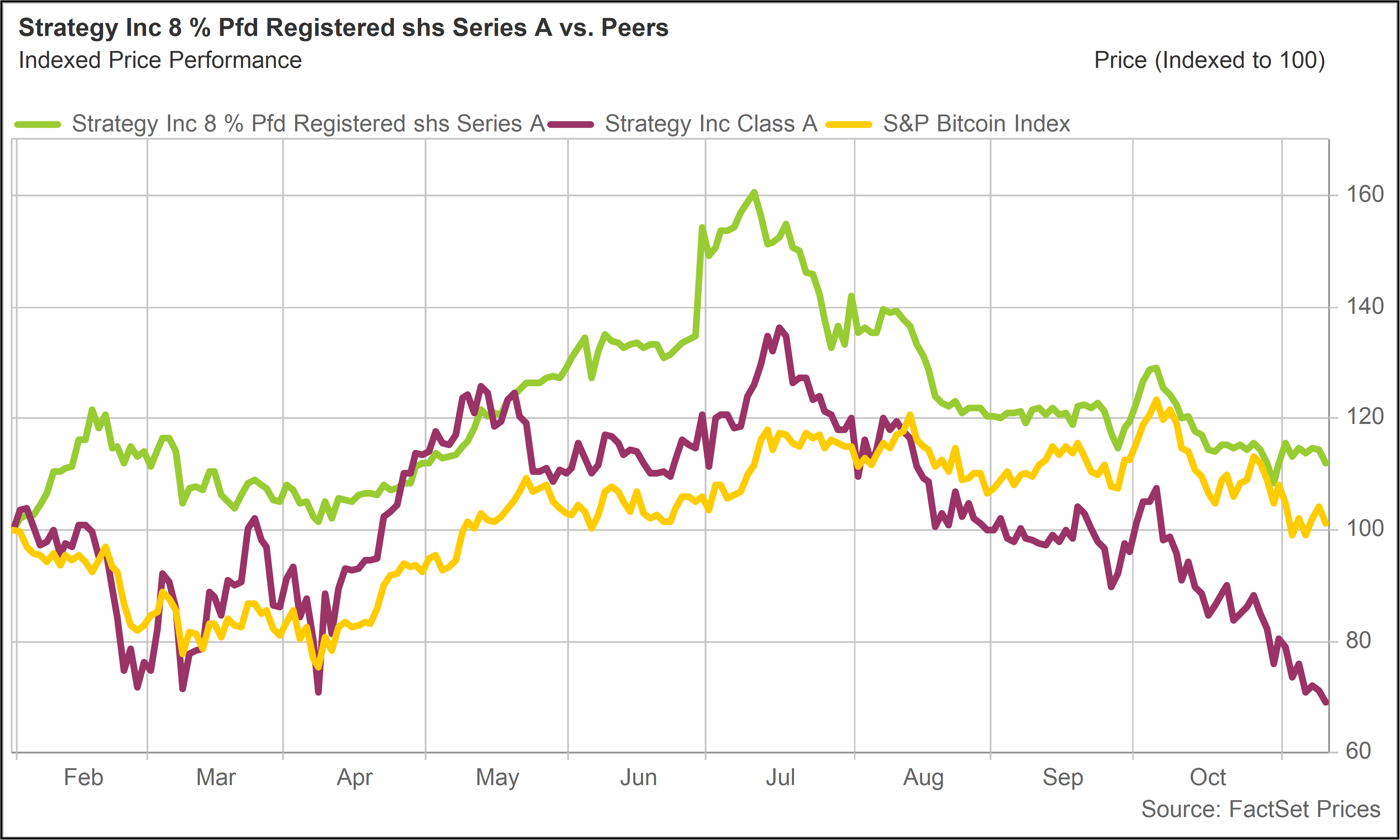

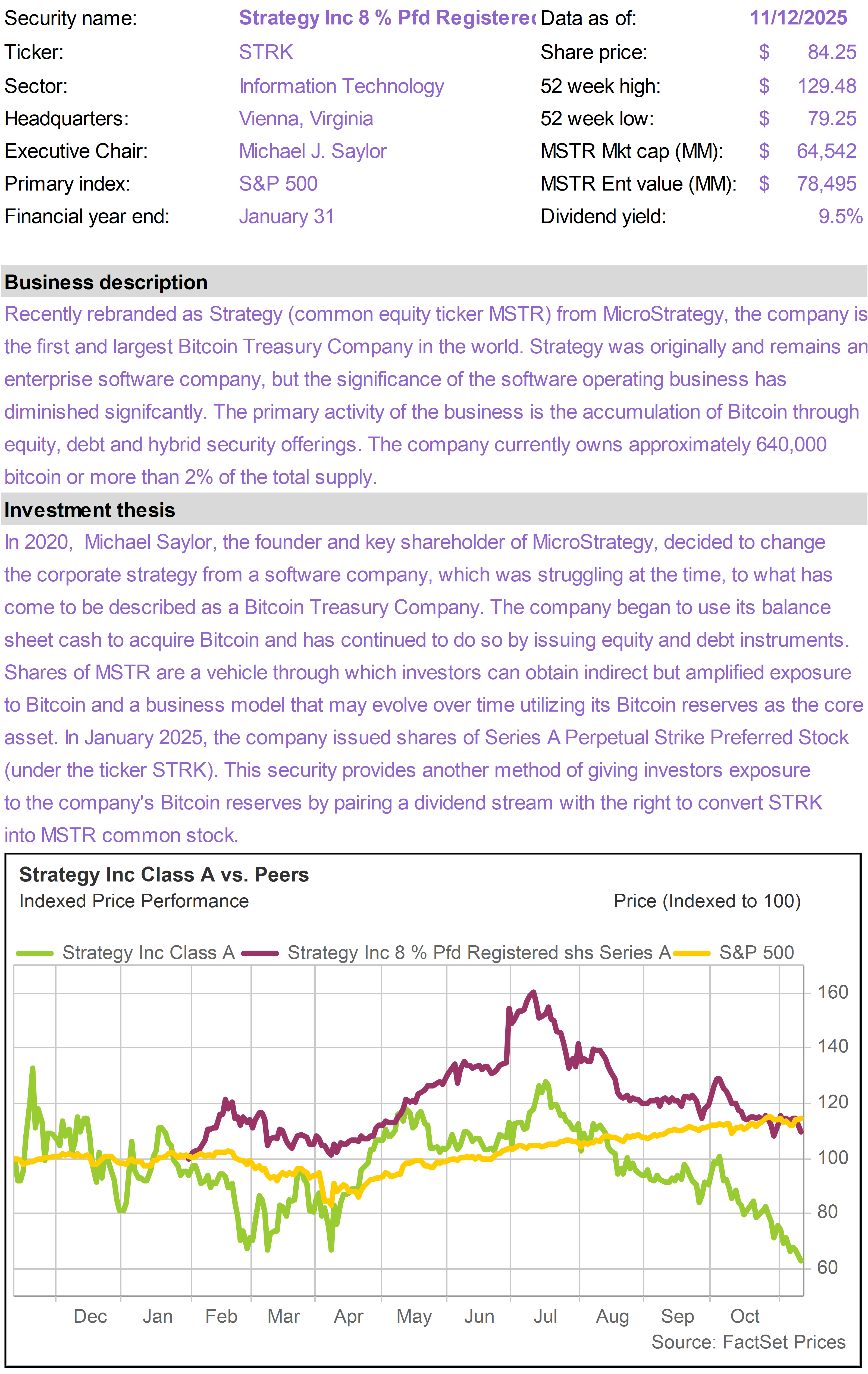

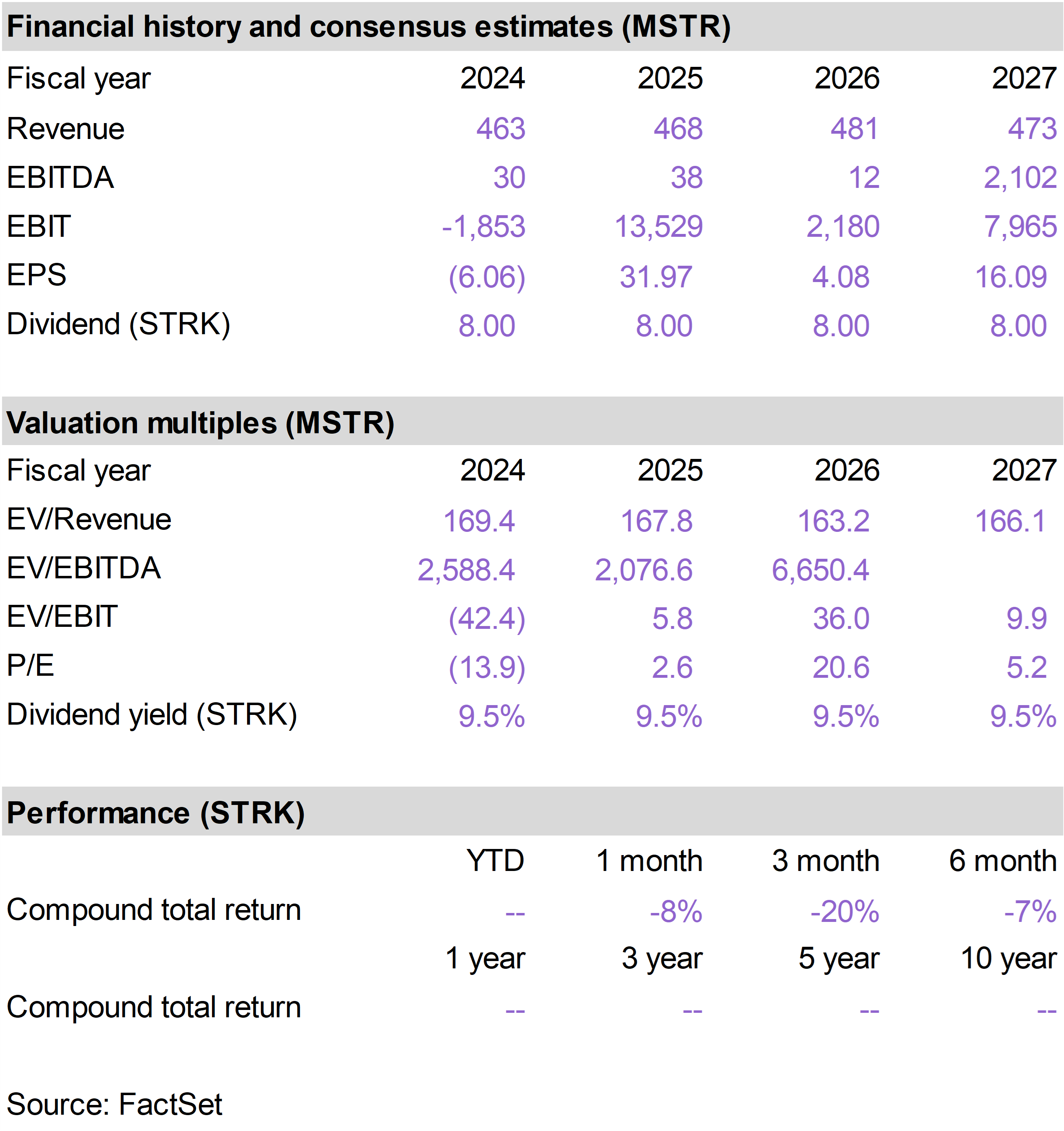

Despite steadily rising yields as prices have fallen, value-oriented investors have not gravitated toward the preferred stock securities issued earlier this year by Strategy (common stock ticker: MSTR), the Bitcoin Treasury Company founded by Michael Saylor.

For investors seeking high income and long-term Bitcoin upside potential, we view this as an opportune moment to revisit Strategy’s preferred stock offerings.

In this report, we lay out our updated thinking—especially in light of Strategy’s recent guidance on the tax treatment of its preferred dividends.

Strategy has informed investors that preferred dividends will be treated as Return of Capital (ROC) rather than ordinary dividends. ROC distributions are not taxable when received; instead, they reduce an investor’s cost basis, with taxes deferred until the shares are sold.

In March 2025, we profiled Strategy’s first preferred stock security—the 8% Perpetual “Strike” Preferred (STRK)—shortly after it was brought to market (High Yield with Bitcoin Upside).

STRK remains the only preferred instrument that can be converted into MSTR common stock.

With MSTR shares trading poorly, the conversion option is currently far “out of the money,” meaning the vast majority of the value of the shares resides in the expectation of future dividends. But the right to convert one STRK share into 0.1 MSTR shares is perpetual, meaning it never expires.

Bitcoin may be under some pressure right now, but to the extent it continues to appreciate at high rates in future years, the conversion option that comes with STRK could conceivably become “in the money” within a reasonable investment time horizon.

Setting aside the convertibility, the dividend yield on STRK now sits just under 10%. Meanwhile, the ROC treatment materially enhances the after-tax attractiveness of the shares—particularly for investors in taxable accounts.

Conflicting mindsets

Value investors are the bargain hunters of the capital markets. They are always on the prowl for irresistibly low-priced investments, like a thrifty shopper roaming the aisles of a supermarket and grabbing whatever happens to be marked down.

Crypto investors are a different breed entirely. A typical value investor might call a crypto investor a “speculator”—and mean it as an insult. The crypto investor, in turn, might wear the label as a badge of honor.

Someday, the worlds of value and crypto investing may converge. Today, they remain far apart—and that distance has real consequences for how markets behave.

As Warren Buffett, the world’s most famous and successful value investor, put it: “Price is what you pay. Value is what you get.”

Many if not most investors get excited about what they are buying. Value investors get excited about the low price they think they are paying.

From that perspective, value investing and crypto investing seem almost incompatible.

Buffett comes from an investing tradition that puts great emphasis on being able to make reliable estimates as to what a business or asset is really worth.

The main goal of most value investors is to buy securities at a large discount to their “intrinsic value.” To do this, you need to feel confident that you can generate a reasonable estimate of intrinsic value.

Value investors like Buffett therefore strongly prefer businesses that produce predictable cash flows. They are skeptical of narratives about distant future growth—and deeply skeptical of paying for outcomes that only might materialize.

The typical crypto investor is quite different.

Many crypto investors are just playing momentum—buying tokens or crypto stocks mainly because they think others will follow. They don’t necessarily have any real faith in the investment itself.

Traders in meme coins especially fit this description, since meme coins typically do not even pretend to offer any kind of fundamental value or utility. Meme coins represent speculation in its purest form.

Visualizing the future

There are many other crypto investors, however, who do have fundamental conviction. And they are willing to speculate about a future state of the world that is quite different from the current one.

Bitcoin investors, for example, often envision a future in which the monetary system changes radically. They foresee Bitcoin continuing to appreciate at high rates as the debt-burdened global economy transitions away from the U.S. dollar and other forms of fiat toward a new system based on digital hard money.

Investors in other crypto assets, like Ethereum, likewise have a vision. Their outlook is often one that is compatible with the typical Bitcoiner’s worldview but leaves room for other digital assets to succeed as well.

Ethereum investors, for example, are generally very enthusiastic about tokenization, which refers to the process of turning real-world assets (stocks, bonds, real estate) into digital assets that are traded on the blockchain.

BitMine Immersion Technologies (BMNR) has emerged as the leading Ethereum Treasury Company—and, in terms of market capitalization, is now second only to MSTR among all Digital Asset Treasury (DAT) companies.

As we described in Is BitMine the Next Crypto Superstar?, BMNR’s strategy is to accumulate as much as 5% of all Ethereum (or more) based on management’s conviction that Ethereum will be the token that benefits most from Wall Street’s shift onto blockchain infrastructure.

Value investors may in the future become more comfortable with crypto assets like Bitcoin and Ethereum and the companies that accumulate them. But at present, many seem to be keeping their distance.

This complicates Strategy’s efforts to attract investor interest—despite improved financial metrics that would normally catch the attention of value-oriented buyers.

But like many business problems, this presents a potential opportunity for patient investors who are willing to be flexible in their thinking.

A rough patch for crypto

Investor sentiment toward crypto has been fairly weak in recent weeks, though Bitcoin had bounced modestly with the reopening of the federal government.

The shutdown created a liquidity drain: federal salaries and payments were delayed, inadvertently reducing liquidity across the economy. Crypto, as one of the market’s most liquidity-sensitive asset classes, was likely disproportionately affected.

Other headwinds emerged as well. Tech sentiment broadly weakened, with investors questioning the sustainability of the AI growth theme. Reports also surfaced of large Bitcoin holders selling.

Looking over a somewhat longer time frame, early enthusiasm for newly listed DATs has faded sharply. Many of these stocks were awarded large premiums to their crypto balance sheet holdings over the summer, but now trade at or near their Net Asset Value (NAV).

As the market leader, MSTR still trades at a premium—but its mNAV (market cap relative to underlying Bitcoin holdings) has compressed materially. From a multiple of approximately 4 times in late 2024 to 2 times in mid-2025, it now sits near 1.2 times.

The re-pricing has also affected Strategy’s preferred shares, such as STRK, which have declined after peaking this summer.