There is an important asterisk: the decade ended with a tech bubble that ultimately burst.

The subsequent three year period was a time frame in which stock market performance was also significantly impacted by the 9/11 terrorist attack. The S&P 500 declined 38%.

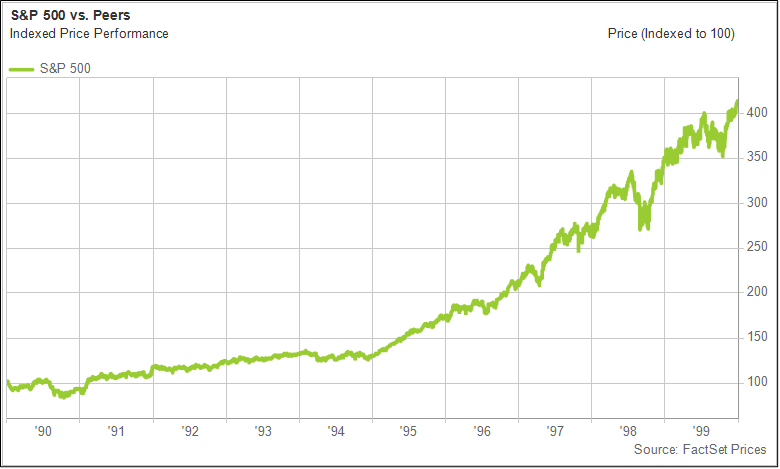

Yet even if we add these three years to the calculation, returns still averaged 10% from the beginning of 1990.

The power of productivity

The key driver of that non-inflationary growth was a powerful productivity wave sparked by the internet and advances in communication technology.

Investors spent much of last year worrying about whether today’s market enthusiasm could morph into another tech bubble. But AI, much like the internet in the 1990s, has the potential to drive real productivity gains across the economy.

That brings us back to the jobs report. In a productivity-driven expansion, slower job growth is not a warning sign—it is a feature. When businesses can generate more output with fewer workers, growth becomes less inflationary.

That is what happened in the late 1990s, when strong GDP growth coexisted with declining inflation.

AI and related technological advances have the potential to create a similar dynamic today by augmenting labor, improving efficiency, and expanding margins without igniting wage pressure.

The inflation–employment tradeoff

Traditional economic thinking often referenced the Phillips Curve—the idea that very low unemployment eventually fuels inflation. While that relationship has weakened over time, it has not disappeared entirely.

We saw the extreme case in June 2022, when inflation peaked above 9%, while unemployment sat at just 3.6%. As businesses reopened post-pandemic, against the backdrop of enormous fiscal and monetary stimulus, they were scrambling to find enough workers.

This contributed to inflation by causing inefficiencies, squeezing margins, and pressuring firms to raise prices.

Today’s environment looks quite different. Employment remains healthy, but it is no longer red-hot. Businesses have room to maneuver.

Tech-led growth with Fed flexibility

The extraordinary performance of the stock market in the 1990s rested on two key pillars: a transformative technology wave and a supportive Federal Reserve.

The second half of the decade was the strongest. From 1995 to 2000, the S&P 500 surged more than 150% as productivity accelerated and inflation stayed contained.

At one point, inflation even dipped below 2%, allowing the Fed to keep rates steady despite rapid growth. Between 1995 and 2000, the Fed funds rate was essentially unchanged despite GDP growth consistently above 4%.

Today’s jobs report fits that same template. A bit of softness in hiring is not a problem—it signals rising productivity and preserves expectations for further rate cuts.

As we close out the first full week of the new year with stocks off to a strong start, the message from the data is clear: the macro backdrop remains favorable.