Gemini is one of a small handful of leading “frontier” AI models globally, alongside models from OpenAI (closely tied to MSFT), Anthropic (closely tied to AMZN), META, xAI, and a few others, that operate at the cutting edge.

In recent tests, Gemini has performed extremely well. The latest version, Gemini 3 Pro, ranked at or near the top across several independent benchmarks, showing clear strength in complex reasoning, science questions, and tasks that combine text, images, and video.

In head-to-head comparisons, it outperformed most rival models on difficult, real-world problem-solving tests, including “Humanity’s Last Exam,” a widely used standard for measuring AI capabilities.

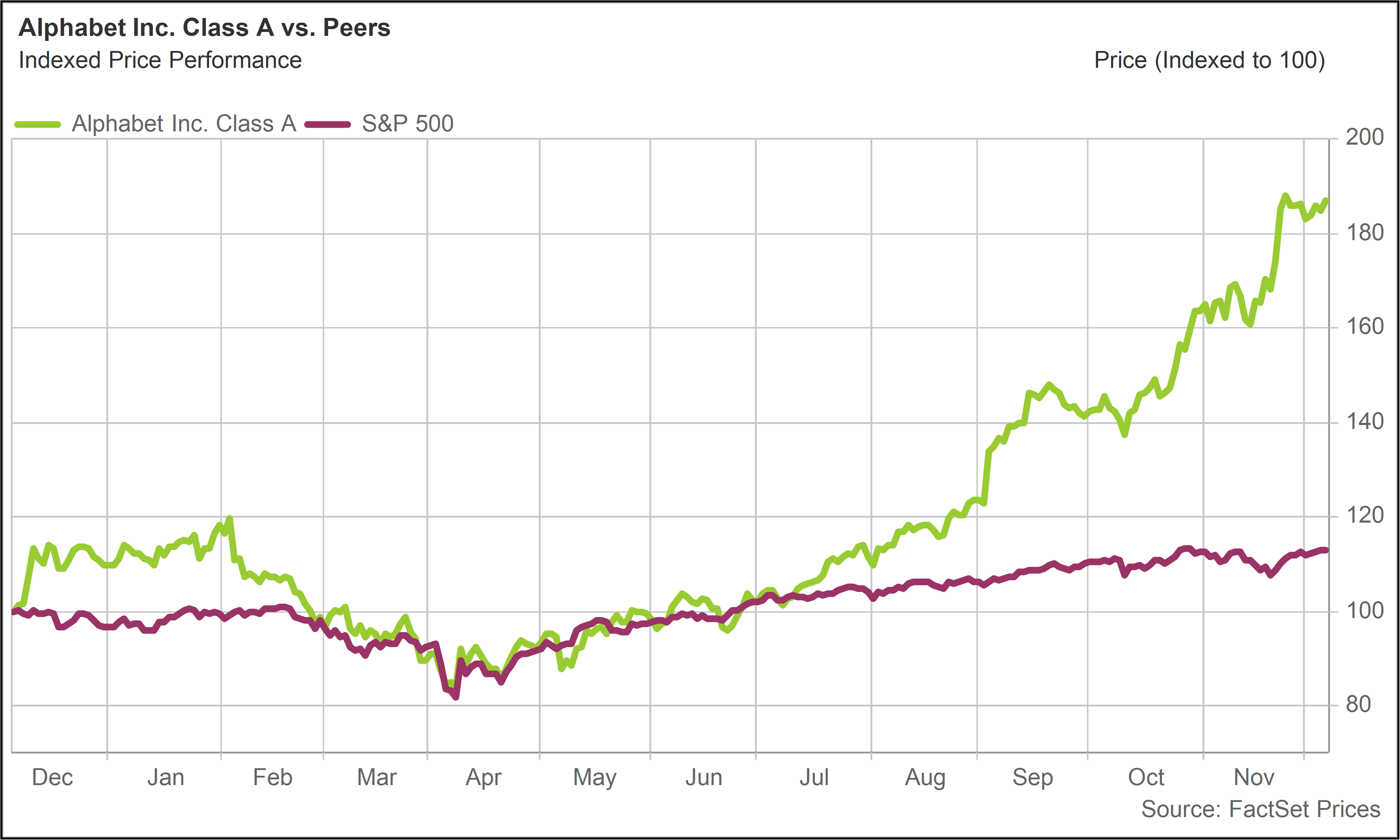

No longer seeing GOOGL as a fading search franchise, investors have been scooping up shares. GOOGL has begun weaving Gemini into Search, Gmail, Docs, Android, and other core services. This all suggests AI will enhance its ecosystem rather than replace it.

Implications for NVDA

GOOGL’s AI resurgence has had an unintended side effect: it has reopened debate around NVDA’s role in the AI ecosystem.

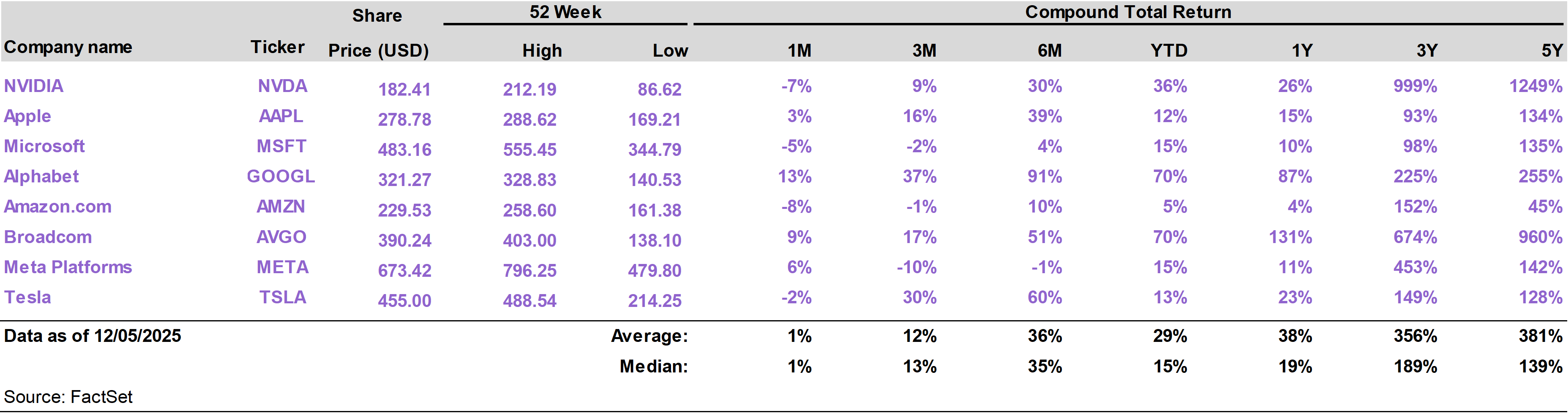

This debate helps explain why NVDA’s share price has been relatively restrained in recent weeks, even after posting excellent earnings results in November that comfortably beat growth expectations.

The controversy centers on GOOGL’s heavy use of Tensor Processing Units (TPUs) instead of NVDA’s Graphics Processing Units (GPUs).

GPUs, like those NVDA produces, are general-purpose AI chips. They are flexible, widely supported, and easy for developers and companies of all sizes to use.

TPUs, by contrast, are custom chips that GOOGL builds for itself. They are optimized specifically for its own models, software stack, and data centers.

Because GOOGL operates at massive scale—running search, ads, recommendations, and AI inference billions of times per day—even small efficiency gains matter. TPUs help GOOGL lower costs and maintain control over its infrastructure, especially during periods when GPUs are scarce or expensive.

This has unsettled some NVDA investors. If GOOGL can run cutting-edge AI models like Gemini on its own chips, then perhaps NVDA’s growth will slow as its biggest customers design around it.

In our view, that concern, while understandable, likely overstates the risk to NVDA.

First, GOOGL is an unusual case. Very few companies have the scale, engineering talent, and capital required to design and deploy their own AI chips. For the vast majority of enterprises, startups, and governments, NVDA GPUs remain the only practical solution.

Second, TPUs do not replace GPUs across the AI lifecycle. Training frontier models still relies heavily on GPUs, and even within GOOGL, NVDA hardware remains core. Custom chips tend to complement, not eliminate, general-purpose compute.

Third, GOOGL’s success expands the entire AI market. When Gemini improves, AI usage grows. When AI usage grows, overall demand for compute rises.

NVDA benefits from the fact that AI is spreading beyond a handful of labs into every industry, every workflow, and every enterprise. GPUs remain the default choice for that broader adoption.

GOOGL’s success with Gemini may ultimately reinforce NVIDIA’s long-term position by accelerating the world’s transition toward an AI-first economy that still, overwhelmingly, runs on GPUs.

NVDA still attractive

Much of the recent debate around NVDA has focused on potential long-term competition from custom AI chips. These concerns have likely kept the share price suppressed despite the strong earnings results and outlook.

But NVDA’s position today is anchored by overwhelming demand, deep customer lock-in, and an ecosystem advantage that is proving remarkably durable.

The demand picture remains exceptional. Every major cloud provider is not only spending aggressively on AI infrastructure but continuing to raise guidance. Data center capital spending growth among the major hyperscalers is 40 to 70%.

At the same time, sovereign AI initiatives across the Middle East, Europe, and Asia are moving from concept to execution, adding another long-cycle source of demand.

On the supply side, NVDA has strong visibility. Its Blackwell chips are essentially spoken for well into 2026, and early traction for the next-generation Rubin platform suggests no meaningful slowdown. Customers are planning around NVDA’s roadmap, not away from it.

Most custom chips (like GOOGL’s TPUs) are designed for narrow, internal workloads, while the most complex and capital-intensive AI work—large-scale training and clustered compute—still overwhelmingly runs on NVDA.

NVDA remains the backbone of the AI economy. To the extent custom chips spur AI adoption, this reinforces, rather than weakens, that role.

NVDA is truly the company that figured out how to bring the world mass-market AI. Investors should not lose sight of its capacity to innovate. The business can handle some competition on the edges.

Meta pivots

Mark Zuckerberg seems to be getting tired of being in last place.

In stark contrast with GOOGL, shares of META have lagged the rest of the Mag 7 over the past three months and six months, returning -10% and -1% respectively.

Reports surfaced last week that META, in connection with its annual budget exercise, is planning on sharp cuts to its “metaverse” initiatives. This could potentially involve spending reductions as high as 30% next year in this area.

Zuck renamed the company from Facebook to Meta Platforms in late 2021, based on his sense at the time that the company could dominate the commercialization of immersive digital environments.

Investors may recall technology stocks performed extremely well until the very end of 2021 thanks to ultra-low interest rates and high consumer technology utilization (Covid lockdowns).

AI was on the radar when META planted its flag in the metaverse… but far in the background.

For perspective, in 2021, NVDA’s data center segment was still smaller than its video gaming segment. Just four years later, in 2025, NVDA’s data center revenues are more than ten times larger than its gaming revenues, which have grown modestly.

The problem with the metaverse is the uncertain payoff from the billions that have been poured into virtual reality goggles and other initiatives.

META’s pivot signals a shift toward AI, where it has tangible advantages and multiple paths to monetization. These include using AI to improve ad targeting and measurement, strengthening content recommendation algorithms across its social media platforms, and building consumer-facing AI assistants.

META is also taking a leading role in open-source models through its own frontier AI model, Llama, which positions it uniquely in enterprise adoption.

META is re-centering itself around businesses and technologies that already demonstrate clear user demand, real revenue opportunities, and strong competitive positioning. This represents a more disciplined, near-term value-creating strategy.

META shares responded positively to this news. But META still has a meaningful valuation gap relative to Mag 7 peers after six months of underperformance.

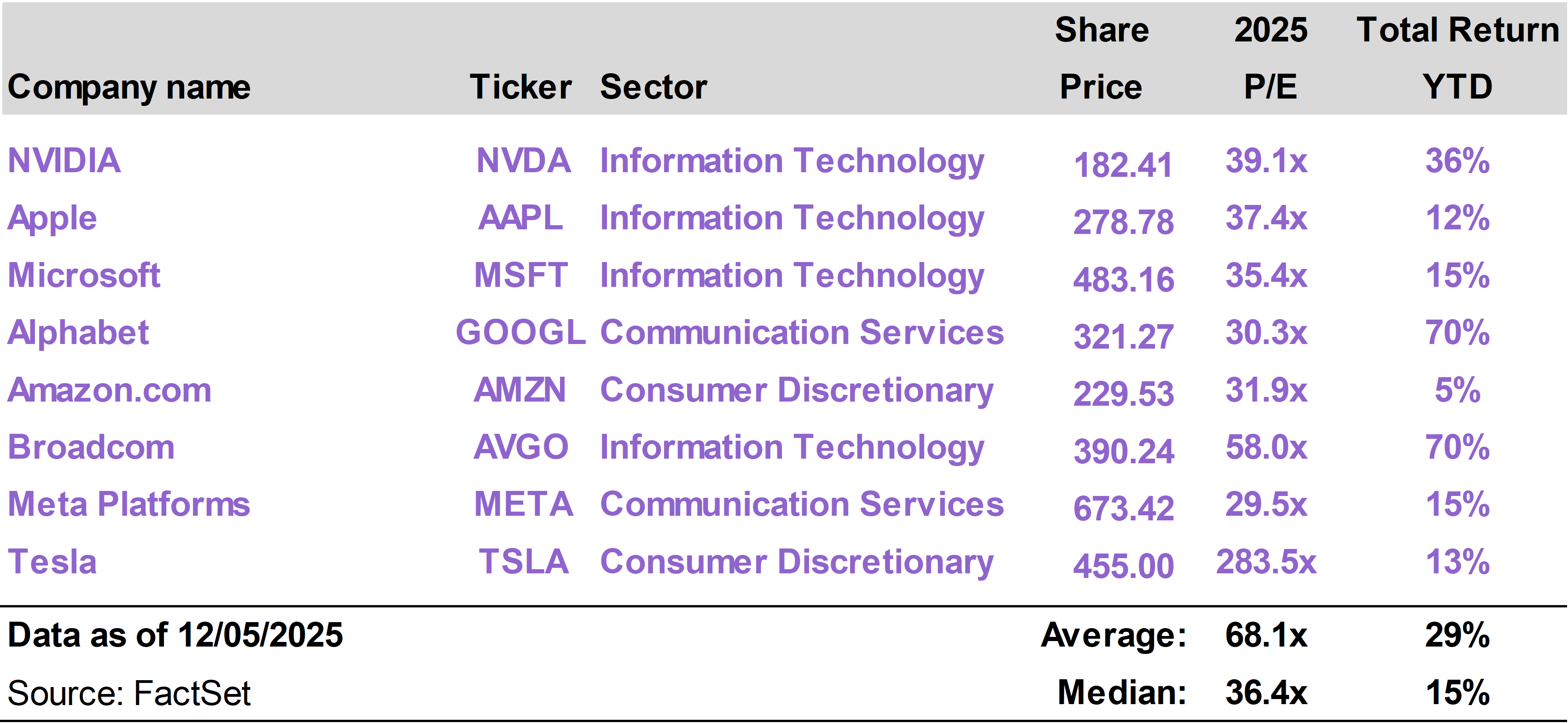

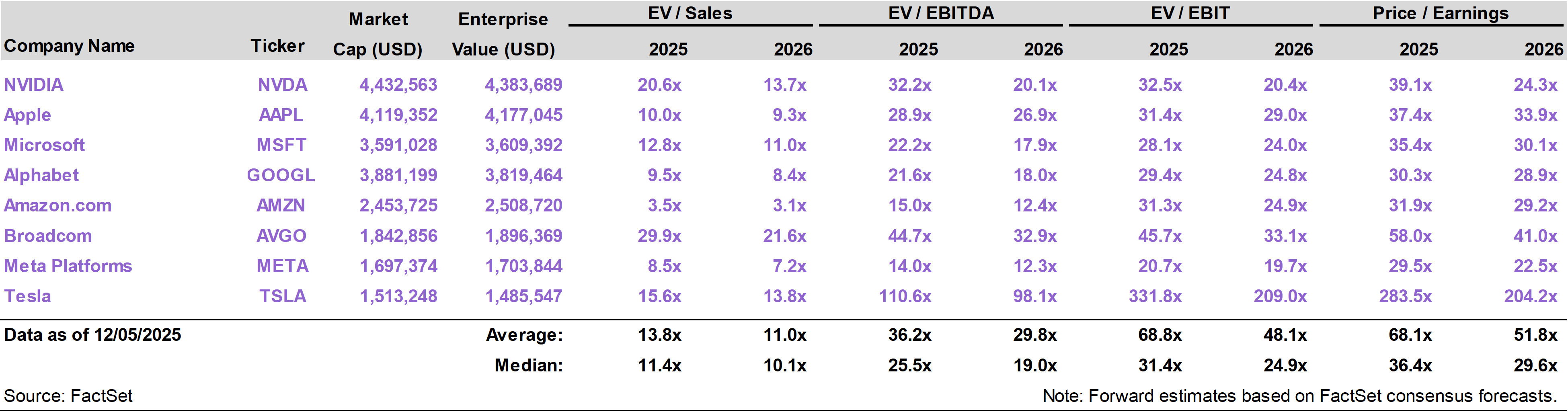

The stock now trades at an undemanding 22.5 times 2026 consensus earnings per share. This multiple is the lowest in the group and approximately in-line with the S&P 500 as a whole.

META’s recent underperformance, combined with the pivot toward AI (which was likely prompted by the underperformance), sets up an interesting case for META as a Mag 7 “value play.”

It is worth noting that both NVDA and META now have the lowest multiples on the basis of 2026 estimated earnings.