Can it keep going?

We have consistently advocated portfolio allocations to gold since we launched 76research in early 2024. The gold streaming stocks that are held within our Inflation Protection Model Portfolio have been among our best performers, significantly outpacing the stock market and gold itself in 2025.

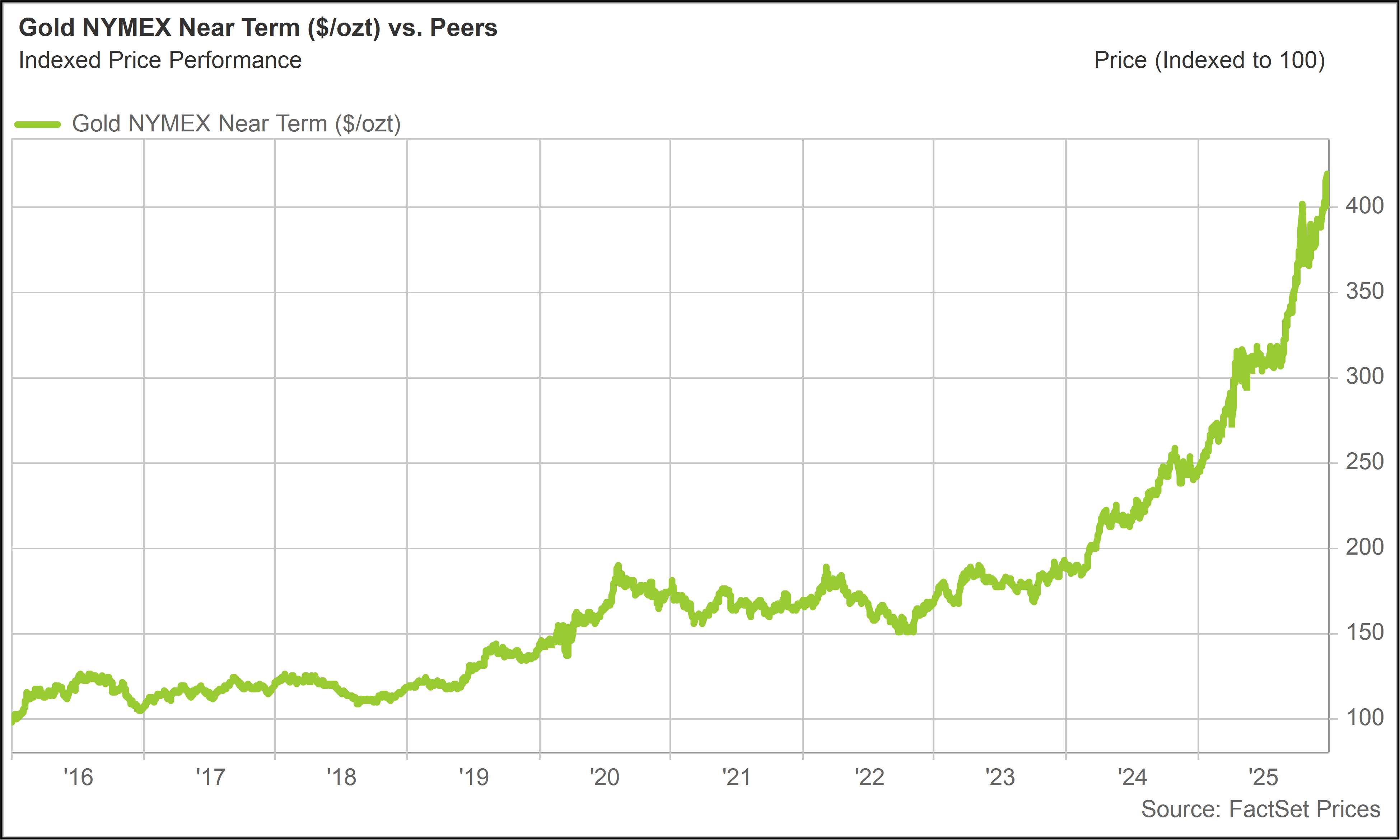

With gold prices having more than doubled over the past two years, it is reasonable to ask whether the asset has simply become too expensive.

We continue to like gold for several reasons:

(1) Monetary policy is turning supportive again.

The post-pandemic inflation cycle is ending. While inflation proved persistent for longer than many expected, the direction is now clear.

Even where tariffs added pressure, the effect appears modest. New York Fed President John Williams recently estimated that tariffs contributed only about 0.5% to inflation in 2025 — a conclusion we view as reasonable.

With tariffs already embedded in prices, their incremental inflationary impact should fade. Meanwhile, labor markets are showing signs of slack, which gives the Fed a green light to continue easing.

Looking ahead, whoever President Trump appoints as Jerome Powell’s successor is likely to arrive with a strong preference toward rate cuts and easier monetary conditions, reinforcing a more gold-friendly backdrop.

(2) AI-driven productivity supports easier policy over time.

At its core, AI replaces and amplifies human intelligence. As AI spreads through the economy, its impact will be increasingly profound.

Productivity gains from AI should strip costs from the economy in a sustained way. Businesses will be able to deliver goods and services more efficiently—in some cases with fewer workers.

This directly influences the long-term trajectory of monetary policy.

The Federal Reserve targets price stability and maximum employment and maintains a long-run inflation goal of 2%.

If productivity suppresses price pressures and reduces labor demand, the Fed and other central banks will have strong incentives to inject liquidity to sustain growth and prevent inflation from undershooting targets.

In short, AI-driven productivity growth should lead to easier monetary policy, which favors scarce assets like gold.

As the supply of fiat money expands alongside productivity-driven wealth creation, demand rises for stores of value, while the gold supply increases at only 1%–2% per year.

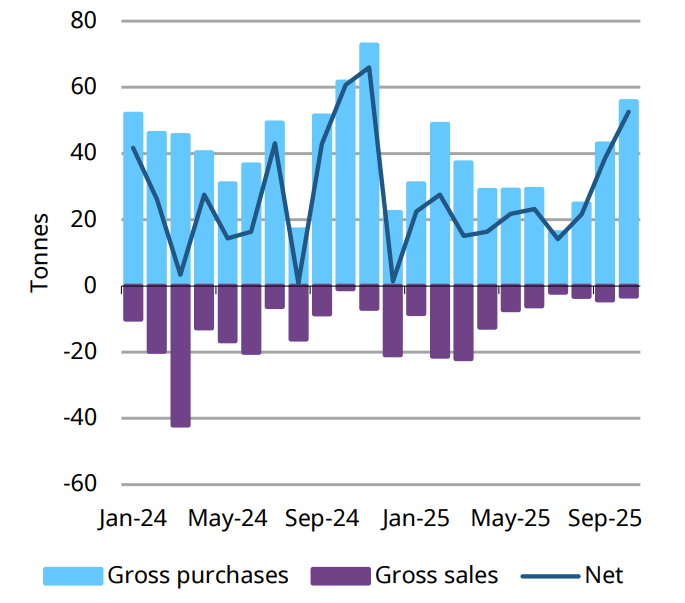

(3) Central banks are unlikely to stop buying.

Central bank demand is the cornerstone of the gold market.

Western economies such as the United States, Germany, Italy, and France hold disproportionately large gold reserves built up over decades. Much of the rest of the world remains structurally under-allocated.

To put that imbalance in context, the U.S. and Western Europe collectively hold roughly 19 million tons of gold. All Asian nations combined (representing the majority of the global population and nearly 40% of world GDP) hold about 5.5 million tons.

The factors that reignited central bank demand in 2024—ballooning U.S. debt, geopolitical risk, and concerns over reserve security—have not diminished. If anything, they have intensified.

(4) Tokenization is still in its infancy.

Tokenization represents a structural expansion of gold’s addressable market.

We are at the very early stages of digitizing real-world financial assets. McKinsey estimates that tokenized assets—excluding cryptocurrencies and stablecoins—could reach $2 trillion by 2030.

Markets naturally evolve toward systems that are faster, cheaper, and easier to use. Tokenization allows assets to be bought, sold, and transferred instantly and continuously, without paperwork, intermediaries, or settlement delays.

Tokenized gold lowers barriers to ownership worldwide, particularly in emerging markets where domestic currencies are unstable and traditional financial infrastructure is unreliable.

Owning tokenized gold does not require a bank account—only a smartphone. Roughly two-thirds of the world’s population already has one.

Tokenization does not eliminate counterparty risk. Investors must still trust the custodian and the legal jurisdiction backing the asset. But it offers a potentially compelling and convenient alternative to physical ownership and ETFs that require brokerage access and financial intermediation.

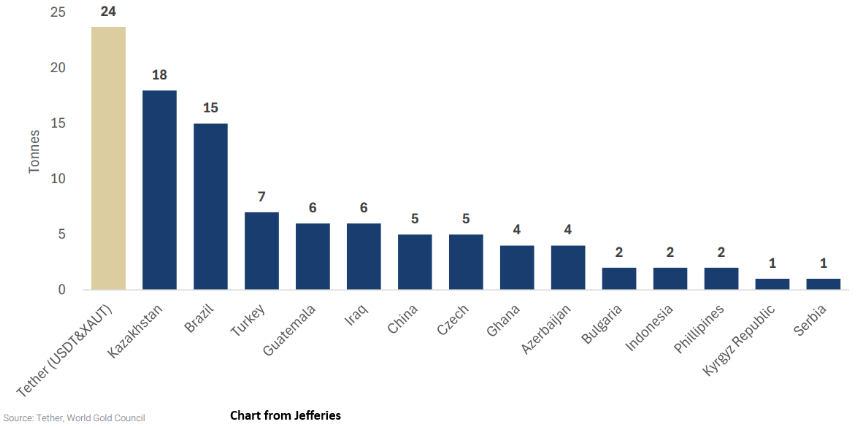

Tether’s recent gold accumulation suggests tokenization has already begun to influence the physical gold market. As digital platforms scale, tokenization represents an open-ended source of incremental demand for gold—one that should not be underestimated.

What about crypto?

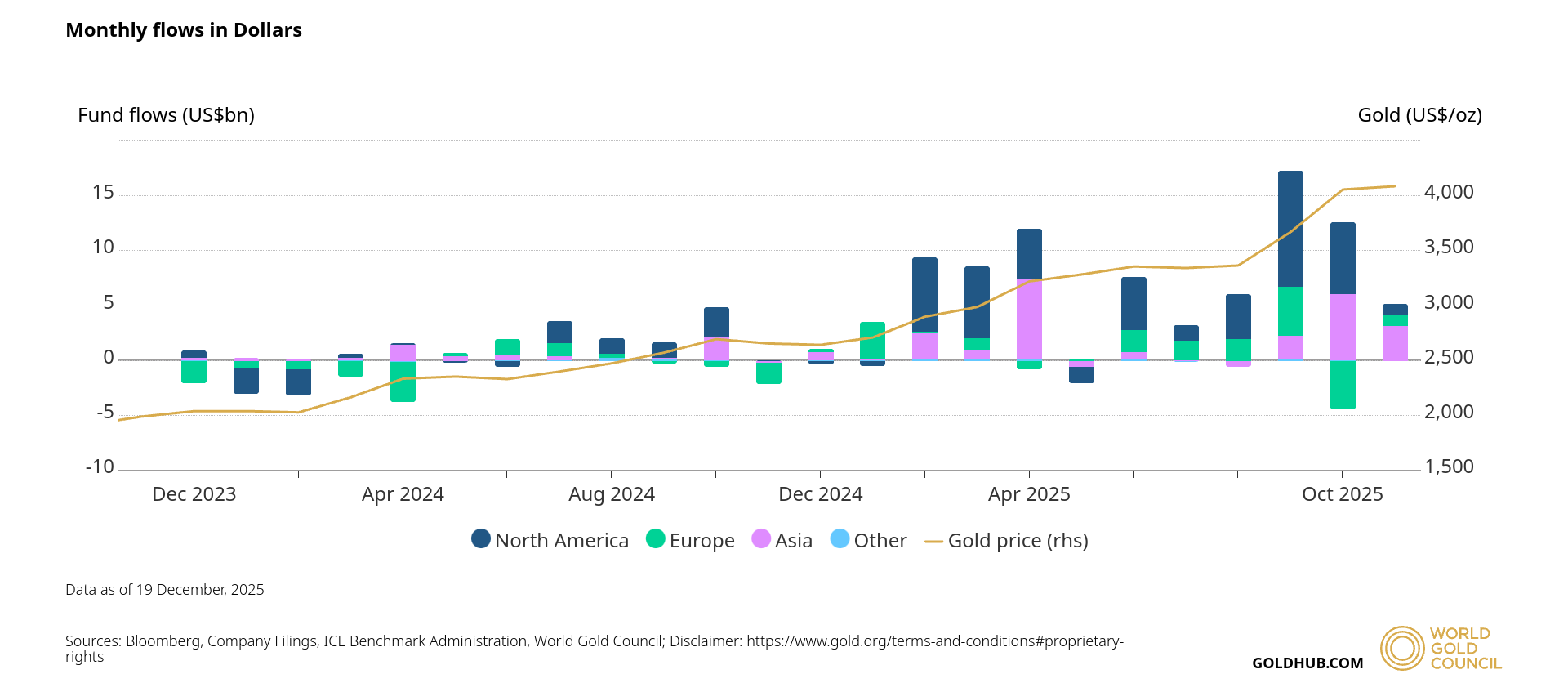

Gold clearly won the debasement trade in 2025 and enters the new year with momentum.

Investors should not necessarily expect another doubling over the next two years, and volatility is always a risk. But the key structural demand drivers supporting gold remain intact.

Bitcoin and the broader crypto market faced greater challenges, particularly in the latter part of the year, despite meaningful progress on regulation, legal clarity, and institutional adoption.

Crypto’s underperformance does not invalidate the thesis—but it does demand explanation.

We look forward to revisiting what went wrong for crypto in 2025 and why Bitcoin and digital assets may reassert themselves as the debasement trade evolves in the year ahead.

Until then, we wish you a happy, healthy, and prosperous new year.