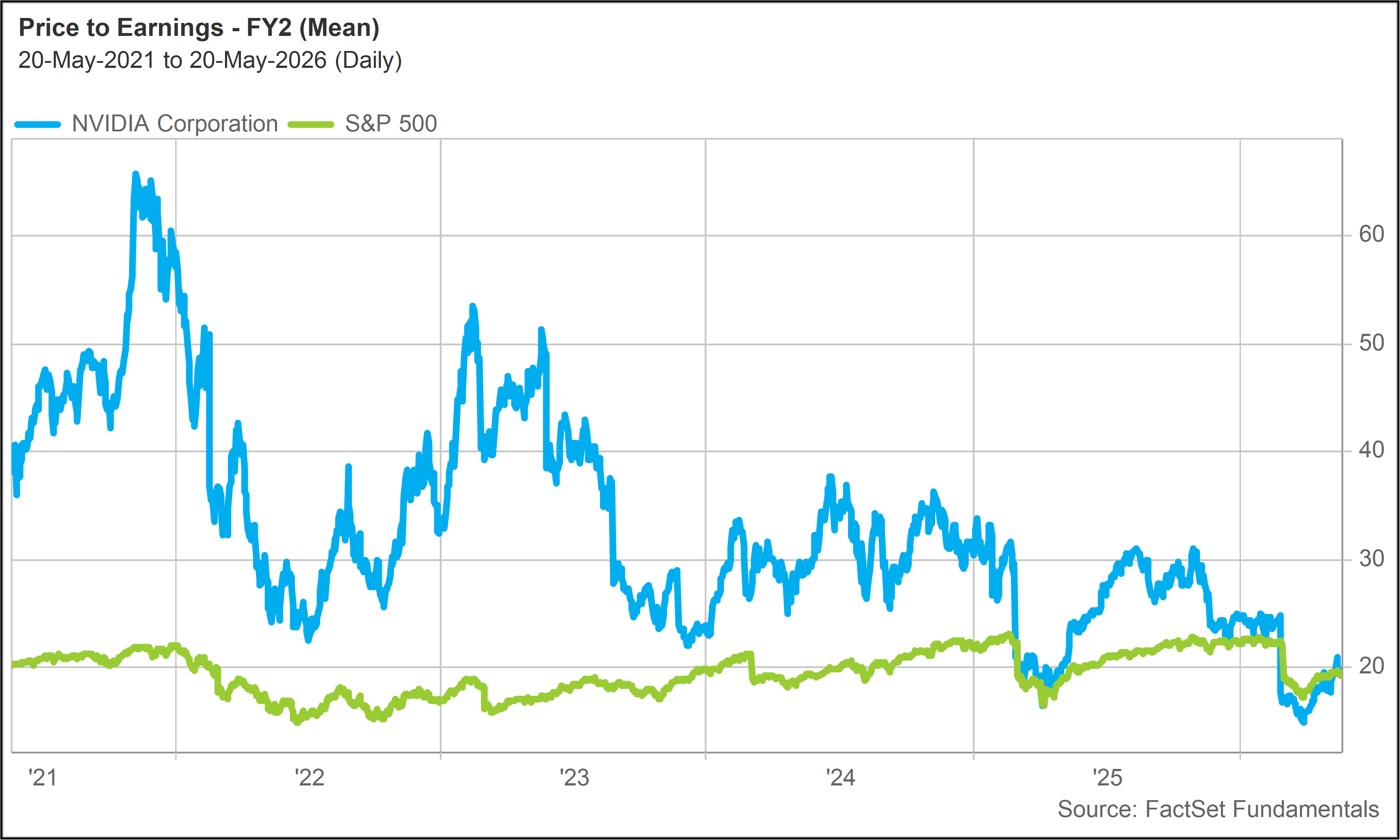

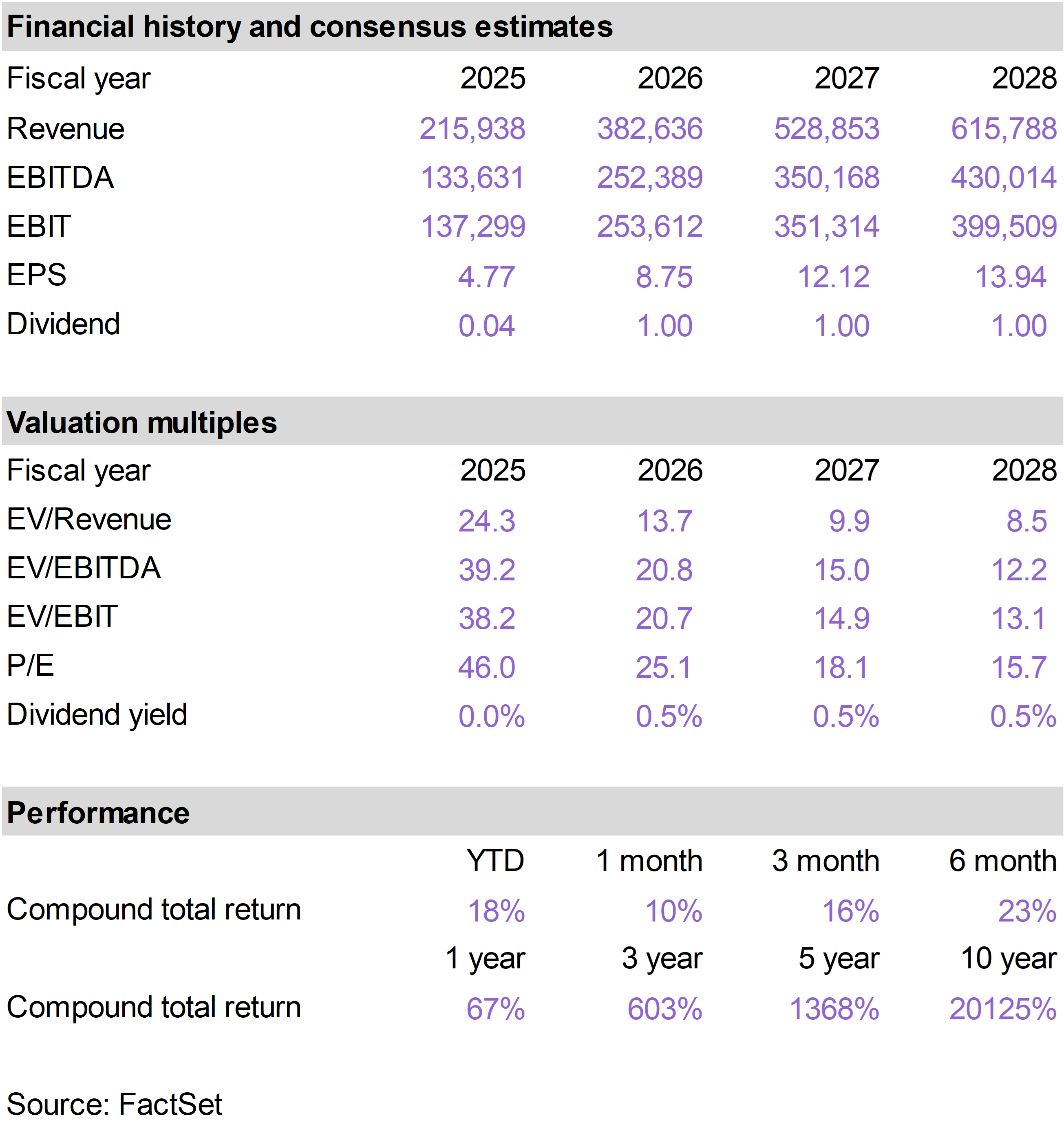

After reviewing the earnings results and conference call, we remain confident that this disconnect between NVDA’s long-term growth prospects and valuation represents an opportunity for investors.

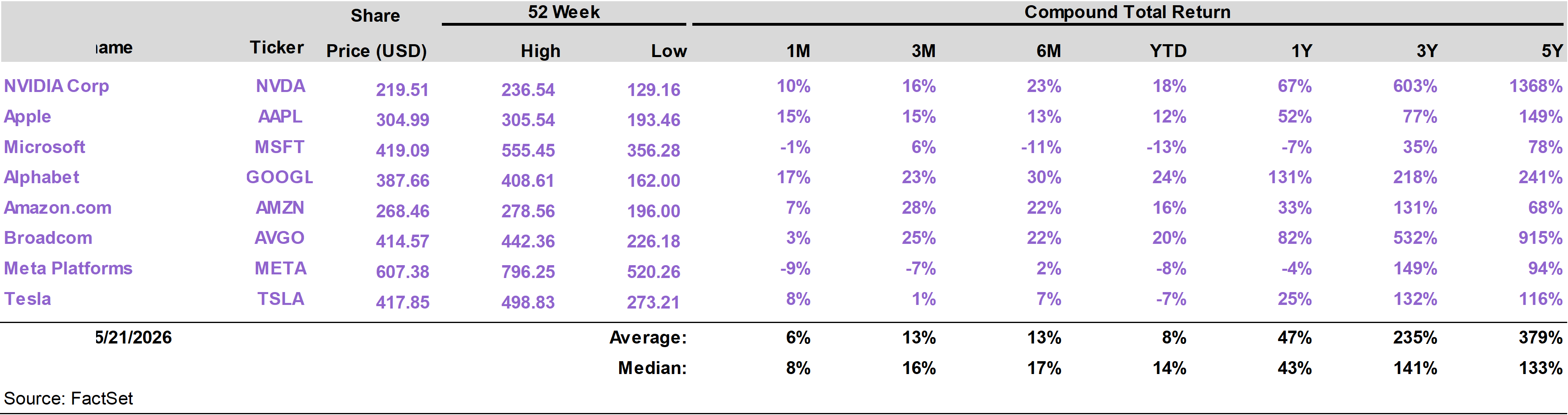

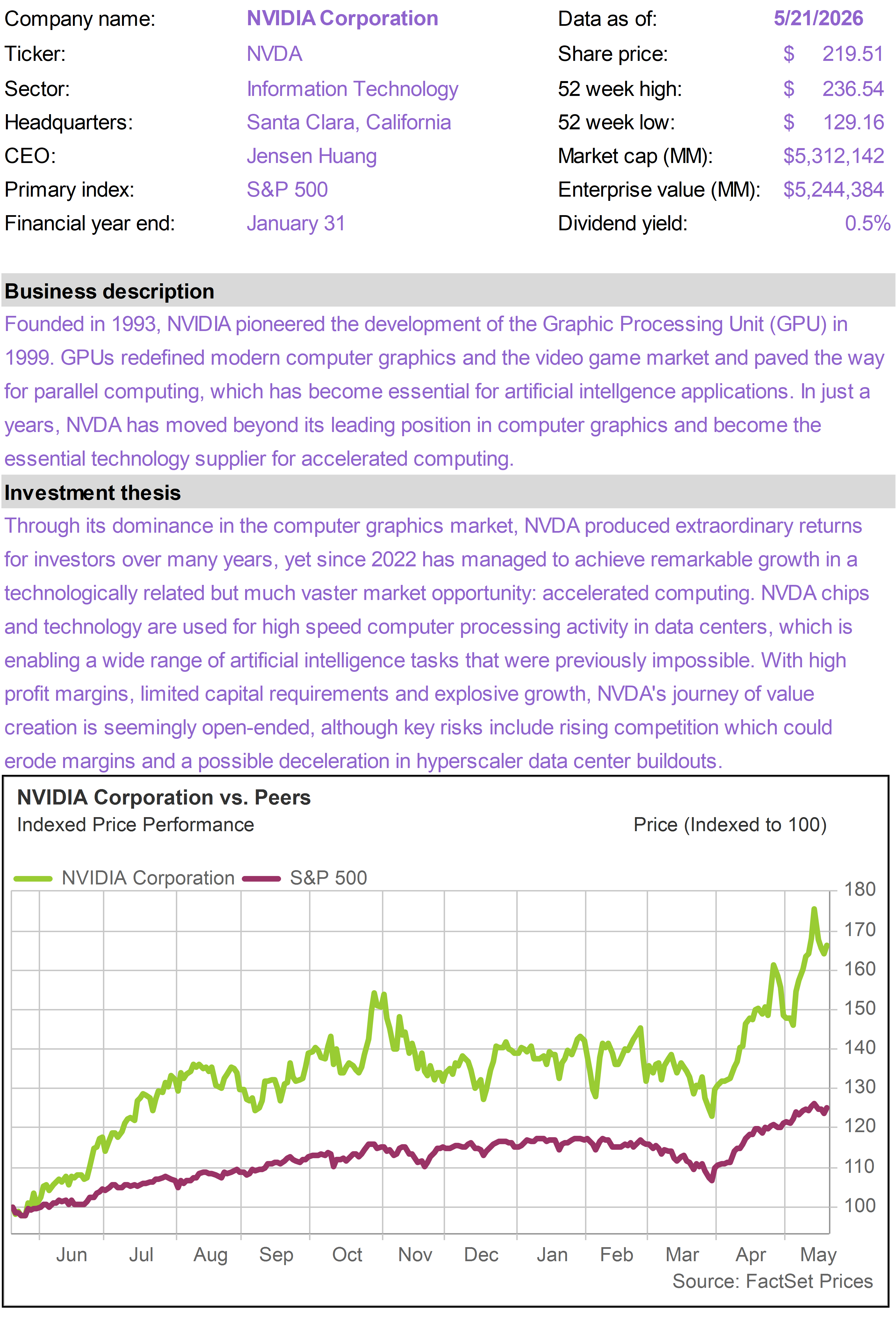

NVDA is a core position within our American Resilience Model Portfolio. While the shares have already delivered exceptional returns since we added it to the portfolio on March 11, 2025 (106% versus 35% for the S&P 500), the company still strikes us as conservatively valued relative to the scale of what may lie ahead.

Neutral reaction

Despite beating expectations and raising guidance, the market reaction was relatively muted, with shares fluctuating modestly following the release. NVDA closed down just under 2% today.

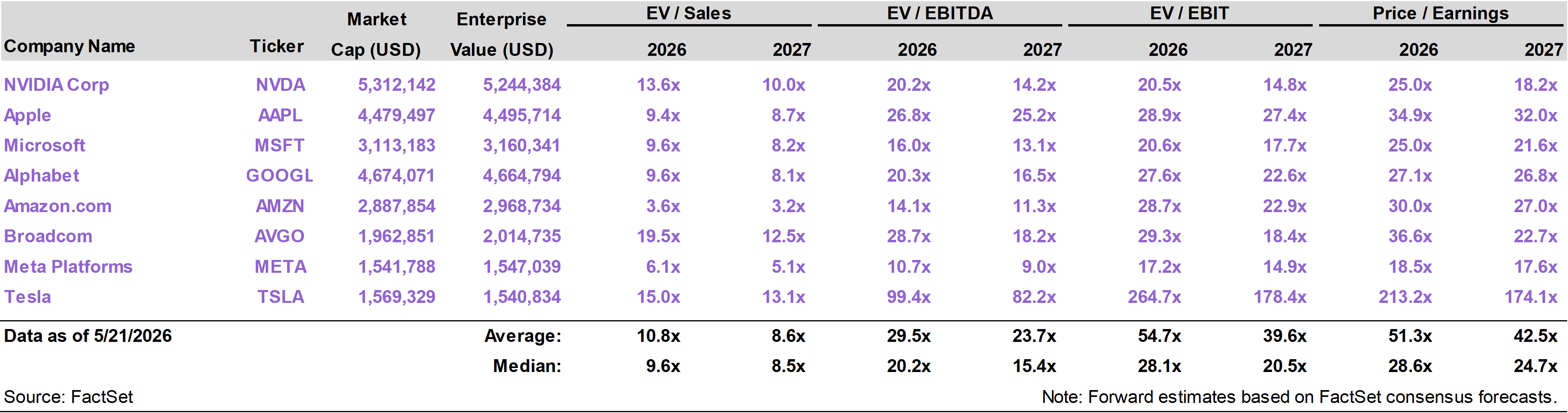

In the first quarter, NVDA reported record quarterly revenue of $81.6 billion, up 85% year-over-year and 20% from the prior quarter. Data Center revenue (the core AI business) surged to $75.2 billion, up 92% from a year ago.

Operating income jumped 147% year-over-year to $53.5 billion, while earnings per share climbed 214% to $2.39.

Management guided next quarter revenue to roughly $91 billion, which represents double-digit quarter-over-quarter growth. No contribution was assumed from China given ongoing uncertainties related to NVDA’s legal access to that market.

Growing beyond the hyperscaler core

One of the most important takeaways from the quarter is that NVDA is seeking to decrease its reliance upon the handful of giant tech companies that still represent its main customer base.

To help investors track this shift, management announced a restructuring of its segment reporting. The business is being reorganized around two main units—Data Center and Edge Computing.

Within Data Center, NVDA will now separate Hyperscale customers—companies like Microsoft, Amazon, and Google—from a more diffuse category called ACIE: AI Clouds, Industrial, and Enterprise.

While the AI boom was initially concentrated among a few hyperscalers racing to build giant data centers, it is now rapidly spreading into governments, industrial companies, robotics firms, healthcare companies, and businesses across nearly every sector of the economy.

CEO Jensen Huang refers to these operations as “AI factories”—massive infrastructure platforms designed to generate intelligence the same way traditional factories generate products.

Sovereign AI—nationally controlled AI infrastructure and data center systems—falls within the ACIE bucket. NVDA disclosed that revenue from sovereign AI surged more than 80% year-over-year.

NVDA now has sovereign AI platforms deployed across nearly 40 countries representing roughly $50 trillion in GDP.

ACIE also includes AI cloud providers, which are a newer layer of companies, like CoreWeave (CRWV), that rent AI compute capacity to customers. They are effectively AI-native cloud platforms built around NVIDIA infrastructure.

Enterprise customers, on the other hand, are traditional businesses outside big tech—industrial companies, banks, healthcare systems, telecom firms, manufacturers, energy companies, and others—building or deploying AI systems for their own operations.

While Hyperscalers remain the biggest piece of the business, NVDA is increasingly selling to a rapidly expanding ecosystem of AI-native infrastructure providers and enterprises across the broader economy. Revenue tied to these customers more than tripled year-over-year.

With investors concerned about this sustainability of Mag7 investment in AI capacity, this expansion and diversification of the customer base is a notable pivot.

The new Edge Computing segment, representing less than 10% of total revenues, includes the legacy video gaming business, but also nascent business lines linked to physical AI, including automotive and robotics.

Edge Computing revenue grew 29% year over year, held back to a large extent by the slower growth gaming unit. But it has the potential to accelerate in the future as physical AI gains traction.

Moving into CPUs

Another major theme from the quarter was NVDA’s push deeper into the AI infrastructure market.

NVIDIA has dominated the GPU (Graphics Processing Unit) market—a legacy of its leadership in video games and high-performance computing—while companies like Intel and AMD historically controlled much of the CPU (Central Processing Unit) market.

GPUs excel at handling massive amounts of parallel processing simultaneously, making them ideal for training and running AI models. CPUs, like those found in any laptop or desktop PC, are designed for more general-purpose computing.

Ironically, as AI evolves into agentic AI—AI systems capable of performing tasks autonomously—the role of CPUs is becoming increasingly important, though in a very different way than in the pre-AI era.

The world still needs CPUs, but increasingly those CPUs must be optimized to support AI workloads. They are essentially becoming complementary to the GPUs that do the heavy lifting.

NVDA is uniquely positioned to deliver the next generation of CPUs. Its new Vera CPU platform is viewed by the company as a potential $200 billion market opportunity.

On the call, management disclosed visibility into roughly $20 billion in standalone CPU revenue this year.

Jensen described a future where billions of AI agents eventually exist, each effectively operating like its own digital worker. AI-optimized CPUs are needed in this future reality.