META’s recovery

META has had a tough stretch in recent months, irritating investors with aggressive spending on AI, but appears ready to make a comeback.

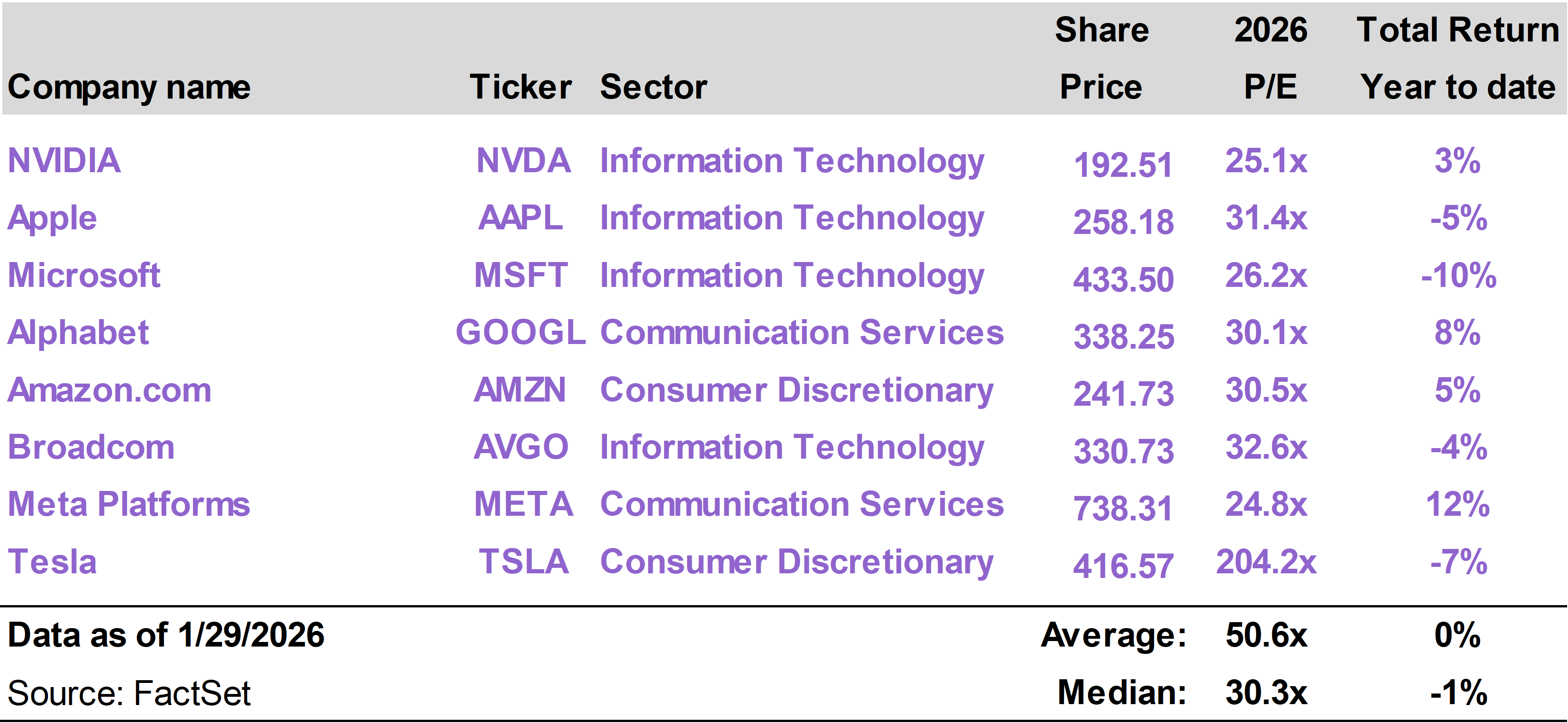

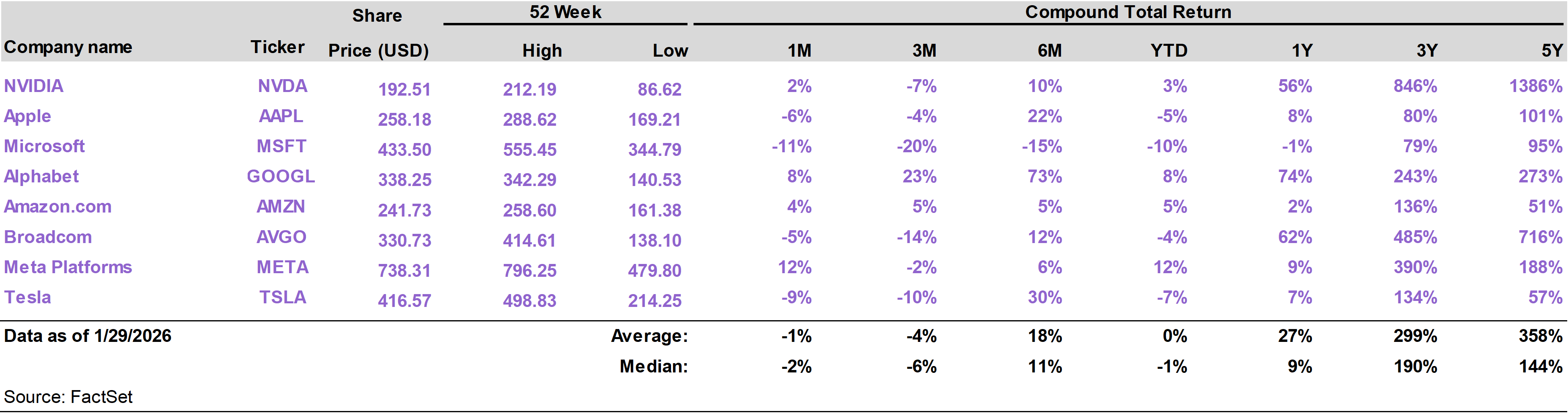

Through yesterday, META was the cheapest stock among the Mag 7 (relative to 2026 expected earnings). It was also last in terms of one-year stock performance.

On January 15, we sent an update to American Resilience Model Portfolio subscribers, adding META to the portfolio and eliminating another technology name. Since then, the shares have returned approximately 19%.

As we explained in that note, the decision to include META was based on several compelling factors, including:

(1) Mispriced quality

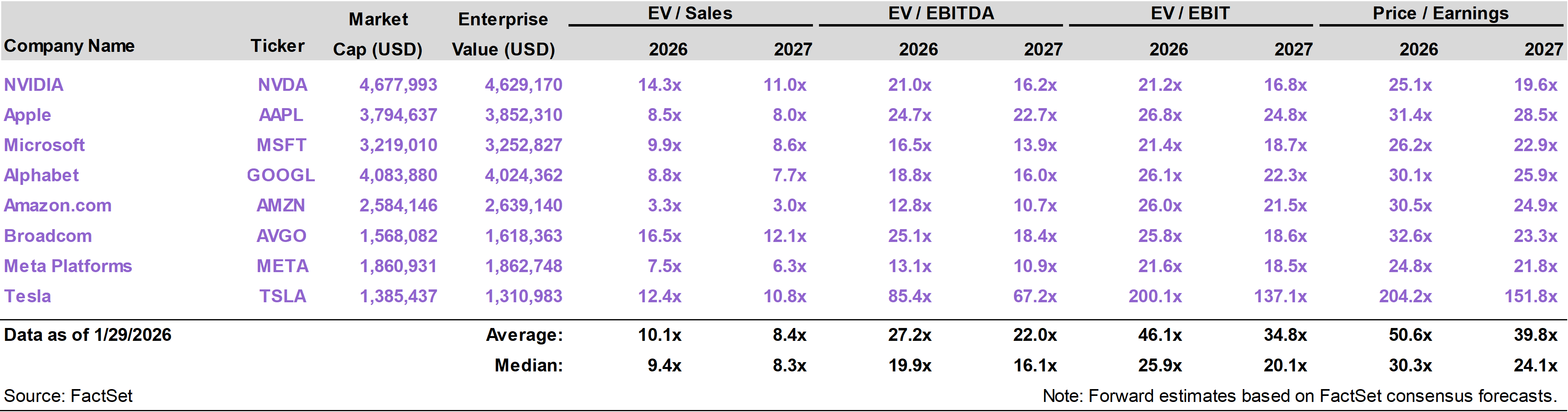

META combines one of the most profitable core businesses in global technology with durable growth, yet was trading at less than 21× 2026 consensus earnings—below both the median Mag 7 multiple (~30×) and even the broader S&P 500.

This discount existed despite operating margins near 40%, strong free cash flow generation, and mid-20% advertising revenue growth.

(2) AI monetization at scale

META has already been translating AI investment into tangible financial returns. Its LLaMA AI models are improving ad targeting, creative optimization, and content recommendations across Facebook, Instagram, and WhatsApp, driving measurable increases in advertiser Return on Investment (ROI).

Given META’s scale—over $50 billion in quarterly revenue—even modest AI-driven improvements generate billions of dollars in incremental revenue. This is likely only beginning, with significant additional upside in the future as AI agents become embedded within messaging, commerce, and business tools.

(3) Strategic and financial flexibility

While META’s current earnings are somewhat depressed by elevated AI infrastructure spending and ongoing losses in Reality Labs (its virtual reality initiative), these investments are largely discretionary.

Management retains the ability to moderate capital expenditures or further reduce non-core initiatives if returns do not justify spending levels. This flexibility provides a margin of safety for investors, while preserving substantial upside should META’s AI strategy deliver as expected.

In light of the strong fourth quarter financial results, we continue to view META as a highly attractive long-term AI beneficiary.

META uniquely combines frontier AI leadership with unmatched global distribution and immense financial firepower. Despite the recent upside, we still believe the current valuation does not adequately reflect the durability of META’s cash flows or the long-term potential of its AI strategy.

META, along with NVDA, is now one of two Mag 7 stocks included in the growth-oriented American Resilience portfolio, which currenlty includes 14 other stocks across multiple industry sectors.