A potential first day pop is certainly inspiring a lot of interest in SpaceX among retail investors, who are being afforded the rare opportunity to subscribe to the offering. The latest reports indicate that retail investors have submitted orders for more than $100 billion of SpaceX shares.

Typically, IPOs are limited to a carefully chosen group of the underwriters’ institutional clients. Pricing tends to be relatively favorable, leading to short-term upside under normal circumstances.

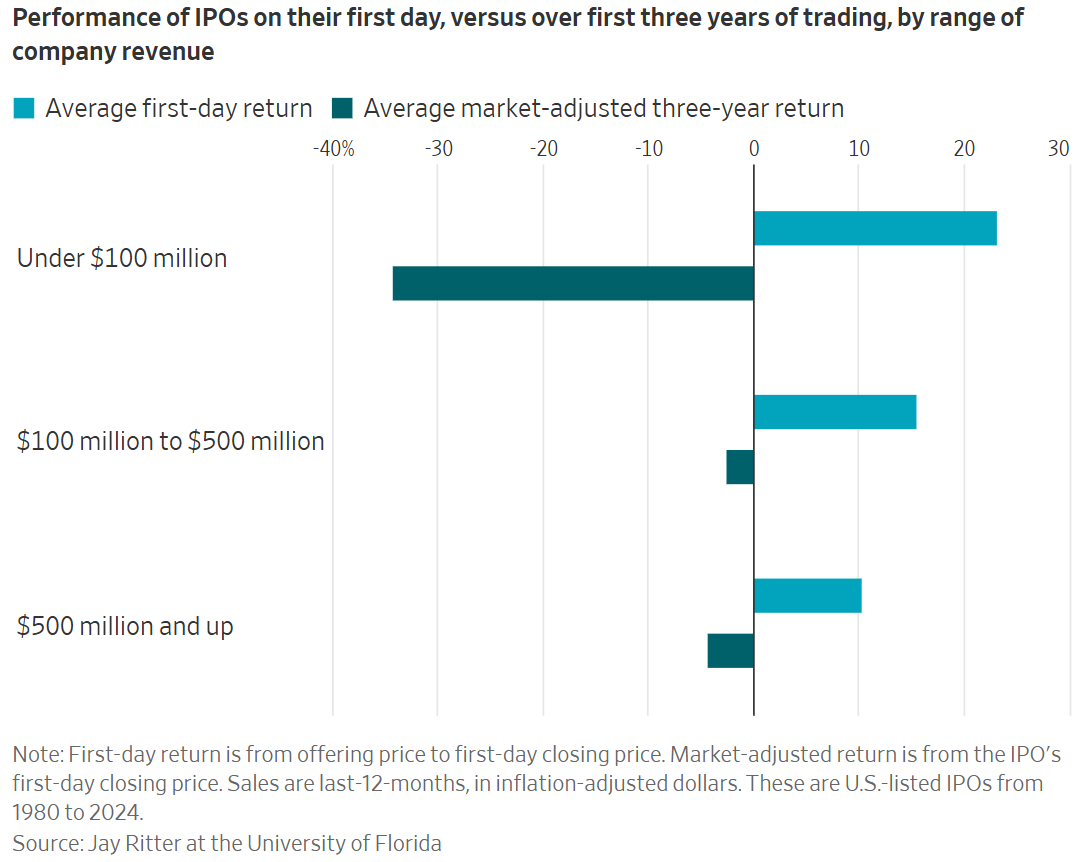

Even in this case, a short-term pop is possible.

The structure of the SpaceX IPO appears almost engineered to create scarcity dynamics. With only a relatively small percentage of shares expected to trade publicly initially, demand could overwhelm supply.

Index dynamics

There is also a critically important passive investing angle.

A number of large index providers such as Nasdaq, MSCI, FTSE Russell, and CRSP are likely to move SpaceX into various growth-oriented indexes relatively quickly following the offering.

As a result, many index funds and Exchange Traded Funds (ETFs) may soon become forced buyers of the stock. That could be quite impactful because passive investing today exerts enormous influence over capital flows.

And the fact that SpaceX will have a low float relative to its total market cap adds another wrinkle to this analysis.

The vast majority of the shares of other public companies with greater than trillion dollar valuations are contained in the public float. SpaceX will be an extreme outlier.

In many cases, index representation is based on market cap. So index funds could find themselves in the position of competing over a relatively small quantity of SpaceX shares to fulfill a much larger index representation.

The same potentially goes for active managers who are benchmarked to an index and do not want to be “underweight” SpaceX.

If the price of SpaceX rises as investors compete for shares, its market capitalization and index weighting could increase further—forcing passive funds and benchmark-driven investors to buy even more stock.

Interestingly, this could also create downward pressure elsewhere in the market.

To make room for SpaceX, both passive and active funds may need to trim positions in existing mega-cap technology holdings. Some of the very companies that powered the AI rally—including the Magnificent Seven—could face selling pressure as investors rotate capital.

It is therefore at least plausible that some of the recent weakness in markets has been connected to the need to free up funds for SpaceX.

S&P on the sidelines, for now

It is worth flagging—Standard & Poors is one index provider that will not immediately include SpaceX across any of its indexes, including the S&P 500.

S&P requires a company to be public for at least 12 months before it is eligible for index inclusion. SpaceX may have to wait even longer due its lack of profitability.

Additionally, the NASDAQ-100 (the underlying index of the widely owned QQQ ETF) is expected to include SpaceX within 15 days of the IPO. However, unlike many indexes, it does take float into account.

As a result, SpaceX is expected to receive an allocation closer to 0.6%-0.85% within the NASDAQ-100 Index. It would be significantly higher if it were purely based on market cap, like many other indexes are.

But what happens down the road?

The case for a short-term pop hinges on these index-related supply-demand dynamics along with old-fashioned investor psychology.

Notwithstanding recent volatility, the IPO is arriving at a moment when investors are once again becoming enthusiastic about AI after the recent market rebound. A strong narrative combined with limited supply can produce explosive early price action.

Investors who are getting in on SpaceX may well see an initial pop, but they are contending with an enormous supply of stock that the market will have to absorb.

Initially, this supply will be limited, but over time, insiders will be permitted to sell. Employees, venture investors, and other insiders will gradually gain the ability to sell shares as lockups expire and trading restrictions ease.

This does not necessarily mean a giant flood of stock hits the market all at once. The company is structuring unlocks in stages rather than through one massive release event. Elon Musk himself is expected to remain heavily restricted from selling for an extended period.

Still, the market will ultimately need to digest a dramatically larger float over time. As additional shares gradually become eligible for sale, there will need to be sustained demand to absorb the growing supply.

And to the extent index inclusion is based on market cap, the expanded float will for the most part not trigger incremental demand from index buyers, just incremental supply.

Investors in SpaceX should recognize that the IPO itself may only represent the beginning of the true capital markets event. The much bigger story may unfold over the following 12–24 months as privately held shares slowly migrate into public markets.

Then there is valuation…

Sentiment and technical factors can prop a stock up, or suppress it, for some period of time, but ultimately, markets are effective and prices tend to converge on fair fundamental value.

There is little debate that SpaceX is one of the most extraordinary businesses ever brought public.

The company has transformed the economics of space launch, built a rapidly expanding global communications platform through Starlink, and sits at the intersection of AI infrastructure, robotics, autonomous systems, defense, and satellite networking.

But investors should be careful not to confuse a great company with a great stock at any price.

At its expected valuation, SpaceX would immediately become one of the most valuable companies in the world despite being years away from profitability and generating only a fraction of the revenue of many of its mega-cap peers.

SpaceX vs. NVIDIA

The SpaceX story is compelling, but so is the NVIDIA (NVDA) story. Both represent extraordinary achievements in technology.

Comparing SpaceX to NVDA is illuminating.

NVDA, with a market cap around $5 trillion now, is still just about three times more valuable than SpaceX.

But the financial metrics associated with each business show just how much more stretched the SpaceX valuation actually is and how much future growth is required to justify it.

According to analyst consensus estimates, NVDA is currently expected to generate more than $550 billion in revenue next year. NVDA is also extremely profitable with operating margins exceeding 65%.

NVDA now trades at roughly 9x revenue and 16.5x earnings based on 2027 estimates.

SpaceX, by contrast, will debut at dramatically higher implied valuation multiples.

In 2025, SpaceX generated revenue just under $20 billion. This is generally expected to grow to around $40 billion in 2026 and then around $60 billion in 2027. The business is projected to achieve breakeven profitability in 2027 or 2028.

So, whereas NVDA is valued around 9x times 2027 sales, with more than half of that revenue flowing through as net profit, SpaceX will likely be valued around 29x 2027 sales, with no material profitability yet.

To justify its current share price, NVDA arguably only has to deliver sustained growth at moderate rates (subject to debate, but perhaps as low as 10%) going forward after next year.

SpaceX by contrast needs to grow its revenues from tens of billions to hundreds of billions and in the process move from roughly break-even profitability to high margins.

We are not arguing SpaceX cannot deliver on its extremely ambitious growth plans—just that its ability to do so is already priced into the shares and that the contrast with NVDA is stark.

Investors comparing the two opportunities should ask themselves…

Which outcome has a higher probability?

NVDA achieving modest growth beyond next year, or SpaceX achieving explosive growth?

There is also a fascinating intellectual disconnect between the two valuations.

Consider a world in which SpaceX is able to generate hundreds of billions of revenue in future years—presumably as a result of vast demand for AI compute that supports successful execution of its space-based data center strategy.

Should not NVDA, the undisputed leader in AI hardware, also be in a position to generate significantly higher growth than what is currently implied by its share price?

In this sense, if SpaceX’s valuation is reasonable, NVDA is arguably dirt cheap.

Key turning point for markets

The success or failure of the SpaceX IPO could have an outsized impact on broader market psychology.

If the deal performs extremely well, it may reignite enthusiasm across the entire AI complex and accelerate the coming IPO wave involving companies like Anthropic and OpenAI.

Investors may interpret a successful offering as evidence that public markets remain eager to fund massive AI-related expansion. That could create another leg higher in speculative sentiment.

On the other hand, if the IPO struggles or trades poorly after launch, investors may begin questioning whether the market is becoming saturated with AI-related capital raising and whether expectations across the sector have become too aggressive.

Either way, investors should avoid losing sight of the bigger picture. AI will transform the global economy regardless of how individual IPOs perform in the short run, creating tremendous value along the way across many businesses.

The key challenge is determining which companies will ultimately capture that economic value—and what price investors should be willing to pay for that future today.