|

| | | | How to Play the Zohran Exodus |

|

| The prediction markets have been saying it was inevitable for months, but it was still hard to believe. Last night, it went from high probability scenario to fact. Zohran Mamdani is going to be the next Mayor of New York City.

Mamdani’s political views represent a uniquely disturbing blend of socialism, tolerance of crime and anti-Zionism that is unprecedented in New York, if not American, politics.

Cities can only thrive when individuals are interested in living in them and businesses are motivated to commit capital to them.

While Mamdani will not have unlimited power, we view his election as a serious threat to the economic health of New York City.

Below, we revisit an investment idea that we highlighted following Mamdani’s primary victory in June—and why it now carries even greater relevance.

We both know New York City quite well. Trish came to New York to attend Columbia University and then built her career and started her family there. Rob was born in Manhattan and likewise studied, lived and worked in the city for decades.

Under the leadership of Rudy Giuliani and then Michael Bloomberg, New York City thrived as the global financial capital of the world. Together, these two mayors built a strong economic foundation for the city out of the wreckage of the 1980s crack epidemic.

Subsequent mayors may have been less talented but at least benefited from a strong hand that was left to them.

Cities, like countries, do not just thrive on their own. Success requires leadership.

Bloomberg leans left on many social issues, but he was relatively tough on crime. In fact, his support for “stop-and-frisk” policing practices helped end his very short-lived bid to become the 2020 Democrat Presidential candidate.

Bloomberg also deserves credit for several smart moves to develop New York economically and catalyze the city’s transformation into a major technology hub.

As an entrepreneur, Bloomberg sat at the intersection of finance and technology. He built from scratch what would become the world’s most important and relied upon financial information provider.

Thanks in no small part to various initiatives of his administration, leading tech companies—including Meta, Amazon, Microsoft, IBM, Shopify, and TikTok—established a large presence in the city. In the venture capital industry, New York now ranks second in the United States, trailing only Silicon Valley.

After the Global Financial Crisis, Bloomberg concluded that New York was too dependent on finance and wanted to build a stronger engineering and innovation economy.

In 2010, his administration launched the Applied Sciences NYC competition, offering Roosevelt Island land and $100 million in city funding to a university willing to build a new applied tech campus.

Cornell University, partnering with Technion-Israel Institute of Technology, won the bid to build a campus on Roosevelt Island. Bloomberg personally championed the project through rezoning, permitting, and financing decisions.

Cornell Tech opened in 2017. It has since produced thousands of highly trained computer science graduates, playing a role similar to Stanford or Berkeley in the Bay Area. Talent-driven big tech firms have repeatedly cited the institution as a reason that they set up shop in New York.

What’s next for NYC?

A newly elected mayor who cares about economic growth should be excited to inherit an asset as valuable as Cornell Tech. But Zohran Mamdani (who founded the Students for Justice in Palestine chapter at Bowdoin College, from which he graduated in 2014, a year after Bloomberg’s final term ended) has different priorities.

“There are ways to make what seems to be an international battle into a local one,” Mamdani said in 2020. “If you were to look at the lens of BDS [Boycott, Divestment and Sanctions] and how it applies here in New York City, you would say that Cornell-Technion is something you would be talking about.”

“Technion University is an Israeli University that has helped to develop a lot of weapons technology used by the IDF [Israel Defense Force],” he warned.

Mamdani has since stated that he intends to reassess the city’s commitment to Cornell Tech if elected, drawing from the BDS playbook of using political power to penalize Israel economically.

The Cornell Tech initiative is not the lynchpin of the New York City economy, but Mamdani’s hostility to it exemplifies his mindset. This is one of many positions held by Mamdani that have the potential to erode New York’s attractiveness as a destination for employers.

The anti-Bloomberg

If mayors like Giuliani and Bloomberg was committed to making New York an economic success story, Mamdani’s policy plans seem purpose-built for turning it into a disaster zone.

Consider his plans to change corporate tax rates. Mamdani wants to bring the highest marginal rates on corporate income up from an already high 7.25% to 11.5%, giving firms an immediate financial incentive to relocate.

Perhaps the most important variable that companies consider when setting up shop or expanding in a particular location is, will prospective employees want to live here?

People tend to think that companies lease fancy office space to impress customers or investors, but the main priority—as any major office landlord will tell you—is to attract workers.

Who wants to work in an inconveniently located office with no amenities, bad views, outdated fixtures and broken elevators?

The same logic applies to the city in which these offices are located. There is no point in leasing office space in a city this is unappealing to potential workers.

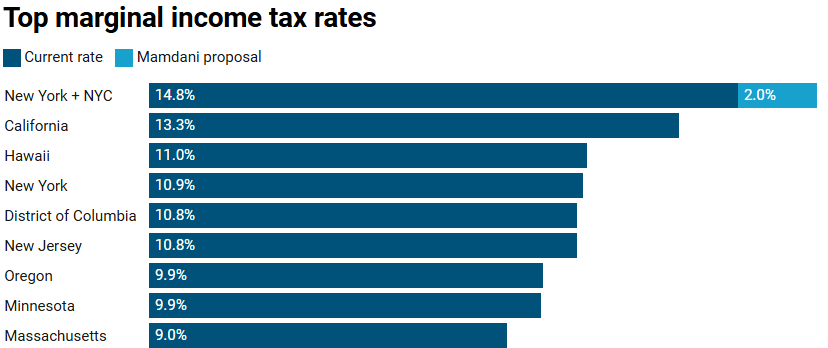

Mamdani intends to raise the marginal income tax rate by 2% on the city’s highest earners. This would make marginal individual income tax rates by far the highest in the U.S. |

|

|

| | Most people, especially parents of young children, want to live somewhere that is safe and secure. Even though Mamdani is only 34 years old, he has a long track record of expressing hostility to law enforcement and thinks “violence is an artificial construction.” |

|

|

| The son of an academic theorist who believes that “[s]uicide bombing needs to be understood as a feature of modern political violence rather than stigmatized as a mark of barbarism,” Mamdani is also intensely committed to the Palestinian cause. His radicalism on this particular issue creates another risk factor that businesses, as employers, will need to consider going forward.

Mamdani’s views on Middle Eastern politics and track record as an activist and agitator have the potential to turn New York City into a very hostile environment for a large proportion of its population, to put it mildly.

The blockchain challenge

We have seen exit poll data suggesting women under 29 had the highest propensity to vote for Mamdani—north of 80%. These self-described “hot girls for Zohran” may have elevated perceptions of their own appearance, but they may not fully understand what is coming down the pike for the financial services sector.

The next big transformation of the financial services industry is tokenization. This refers to putting records of ownership—of stocks, bonds, funds, or real estate—on digital ledgers that update instantly.

Tokenization reduces the need for many of the middlemen and slow settlement processes that have long defined Wall Street. A big reason there are financial hubs in the first place is the traditional benefit of having everything in one place: the banks, the lawyers, the exchanges, and the regulators.

That closeness creates a powerful network effect—firms really need to be in New York or other established financial centers to do business efficiently.

But tokenized markets make geography less important. If assets settle instantly and custody is handled digitally, a firm no longer needs to sit near a clearinghouse or a large legal complex. Instead, companies can focus on lower costs, business-friendly rules, and flexible regulatory environments.

Here comes the Texas Stock Exchange

This is where cities like Dallas—and the emerging Texas Stock Exchange—gain appeal. As tokenization grows, the advantages that once made New York inevitable begin to fade.

The Texas Stock Exchange is positioning itself to be the first major U.S. exchange built with tokenized trading in mind from the start.

The goal is to move toward same-day or instant settlement rather than the two-day delay that still exists on most U.S. trades. This will enable companies to move capital faster, reduce the fees they pay to middlemen, and make it easier for investors to transfer or collateralize shares.

TXSE is already working with firms that handle digital custody and transfer of tokenized securities, so that when regulations allow, it can flip the switch and begin offering tokenized shares as a standard listing option.

Whereas Mamdani sees the corporations within his city as a resource he can access to fund free social services, the Texas state legislature has passed the 2025 Texas Capital Markets Package.

This is a set of state-level reforms designed to make Texas a more attractive home for financial firms, public listings, and investment operations—essentially laying the groundwork for the Texas Stock Exchange to compete with New York.

The legislation streamlines securities registration, reduces certain state-level compliance costs, and clarifies rules for tokenized ownership. It offers targeted incentives for financial institutions relocating headquarters or establishing trading desks in Texas, while shielding them from some of the more aggressive regulatory approaches seen elsewhere.

Just as Mamdani prepares to make conditions inhospitable for productive New Yorkers and large organizations, technology is rapidly shifting to undermine the city’s grip on the financial sector.

Where will everyone go?

For the most part, the American population is shifting to sunbelt states, where taxes are lower, the business climate is friendlier and politicians like Zorhan Mamdani are nowhere to be found.

Recent IRS data indicate significant net population gains in states like Florida, Texas, North Carolina, South Carolina and Tennessee. Comparable population losses have occurred in California, New York, Illinois, Massachusetts and New Jersey.

Mamdani’s election should only accelerate this trend, bolstering the case for an investment idea that we profiled at the end of June.

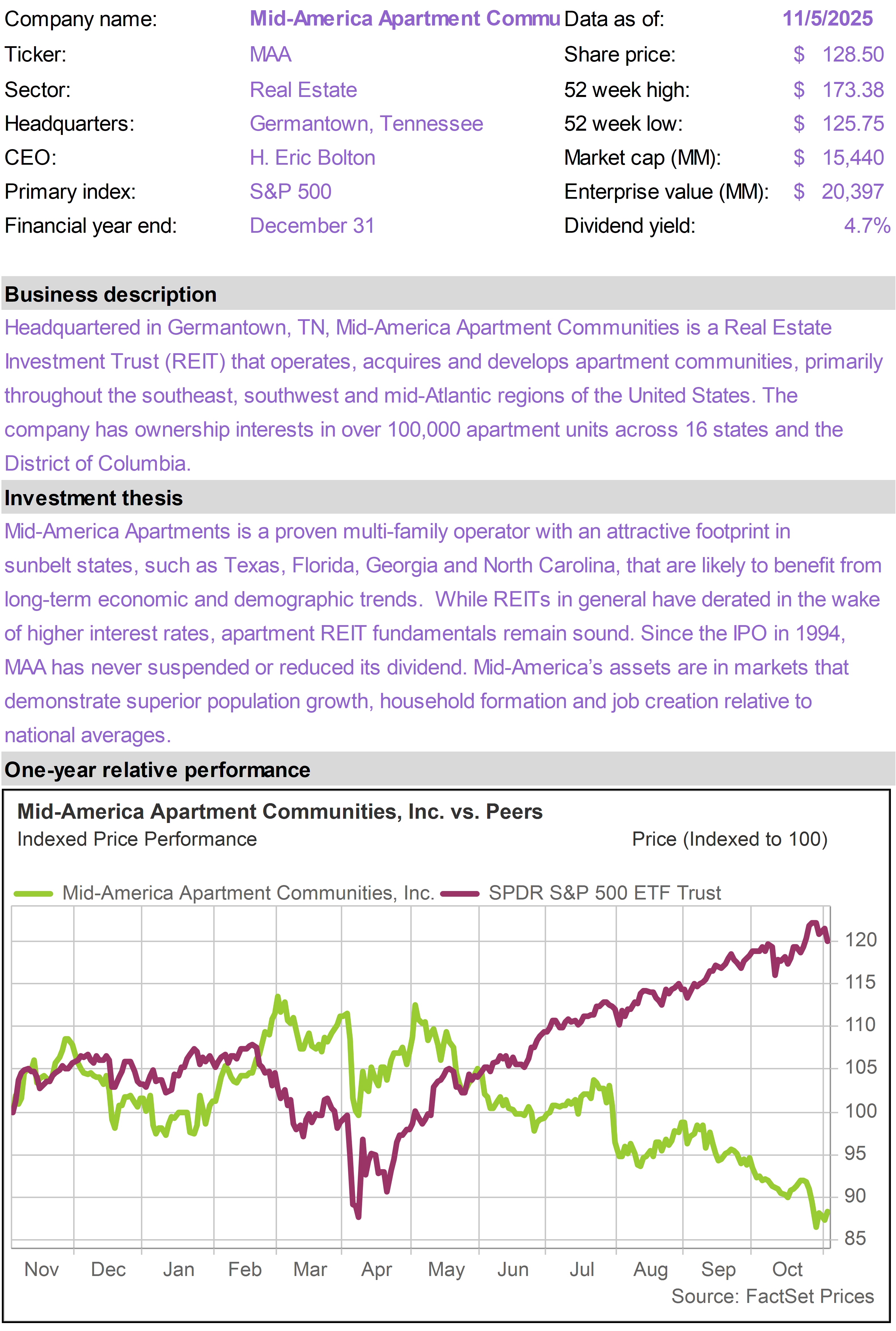

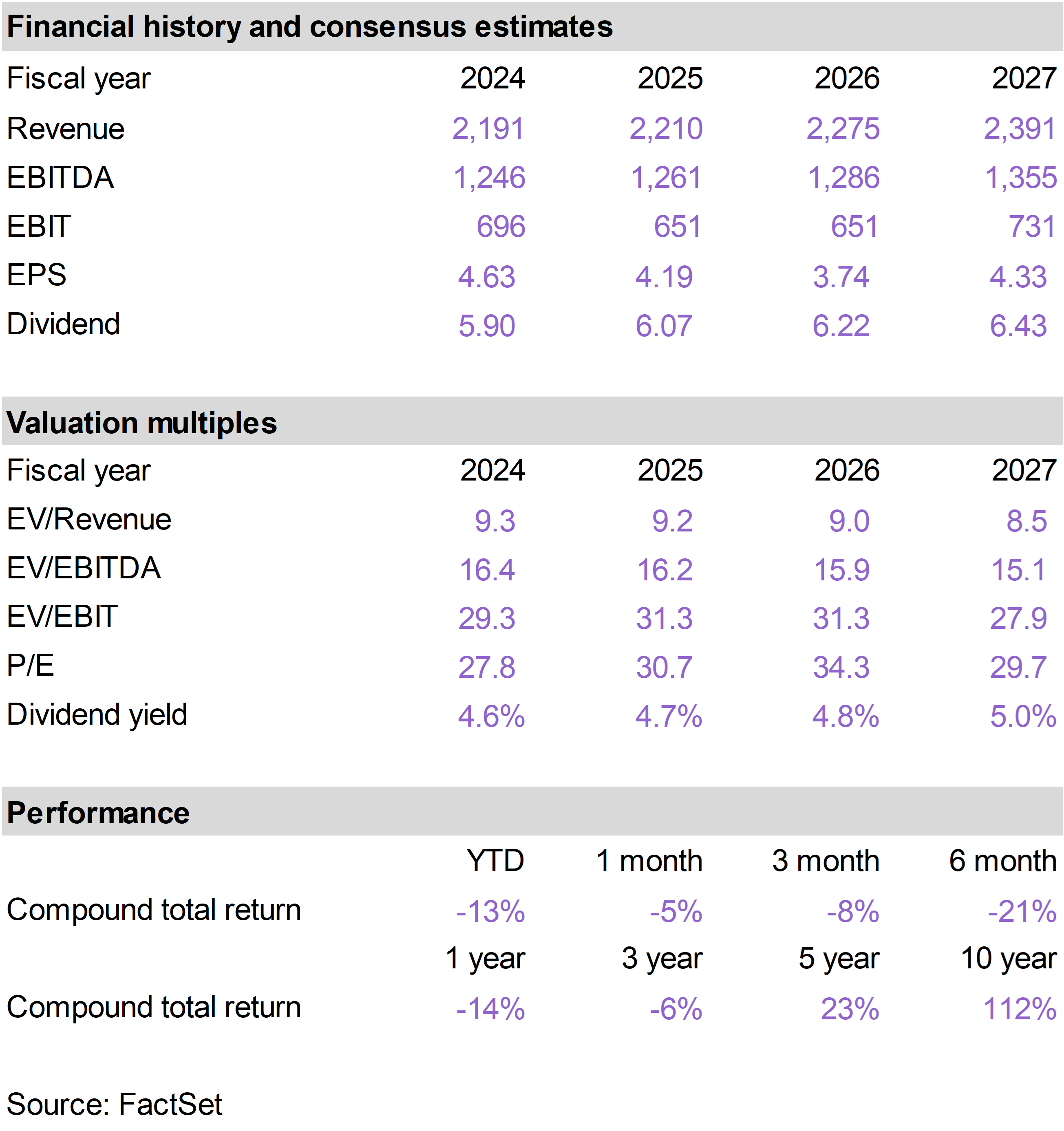

Below, we provide an updated Company Snapshot of Mid-America Apartment Communities (MAA), an apartment landlord with the vast majority of its properties in southern states.

MAA is organized as a Real Estate Investment Trust (REIT), which means almost all of its net income typically gets paid out as dividends to shareholders.

Texas is the company’s largest single state exposure, representing approximately one-quarter of the portfolio’s Net Operating Income. Dallas alone represents nearly 10%.

Shares of MAA have lagged the market over the last three to six months, with investors gravitating toward tech plays rather than more mundane dividend growth opportunities. The dividend yield has drifted up close to 5%.

We also provide below our June 30, 2025 76report note on MAA, in which we explain the apartment portfolio’s gradual emergence from post-pandemic excess supply conditions.

On the most recent earnings call at the end of October, management emphasized that renewal rent growth and collections remain healthy, aided by strong demographics and limited tenant move-outs for home purchases.

Looking ahead, the company expects conditions to improve meaningfully in 2026. Management highlighted that construction starts are running well below historical norms, positioning the portfolio for strengthening pricing power as the market tightens.

Although interest rates have trended in the right direction, investors in apartment REITs have been somewhat skittish about labor market conditions, leading to the stock’s currently more attractive valuation metrics.

New York City will not fall over night, hopefully, and the quality of the city’s mayors have fluctuated over time. But Mamdani’s election—coming at a moment when technological forces, from remote work to tokenization, are undermining the city’s main economic draw—strikes us as highly damaging to the city’s long-term prospects.

Americans are continuing to move to metropolitan areas, mostly southern, that are well-governed and respectful of business interests. These cities are becoming increasingly relevant to the national and global economy.

In addition to a large and growing dividend, MAA offers long-term exposure to economic development in these markets in the form of a high-quality residential real estate portfolio and proven management team. |

|

| | Mid-America Apartment Communities (MAA) |

|

|

|

| | The Anti-Zohran Trade (June 30, 2025) |

|

| A 33-year old, self-described socialist emerged from the New York City Democratic mayoral primary last week as the presumptive nominee. Prediction markets now assign a better than 70% probability to Zohran Mamdani becoming the next mayor of the largest and most economically important city in the United States.

If he is successful, Mamdani will not be the first politician with extreme progressive views to take over a major American city. And he probably won’t be the last.

Regardless of political orientation, investors need to be objective about how political developments and trends can impact the companies they own.

As we reflect on the events that took place last week in New York City, we are reminded of the main reason we have included one particular stock as a holding within our Income Builder Model Portfolio.

We believe this name offers compelling value at current levels and share our full analysis below.

This is a stock that benefits from the enduring structural shift, in terms of both population and economic activity, towards sunbelt states.

There is more to this trend than good weather. Governance matters.

In contrast with certain highly populated states on the coasts and in the Midwest, many sunbelt states offer businesses and workers low taxes, low crime, less regulation, a high quality of life and a commitment to economic growth.

Long-term investors stand to benefit from being on the right side of this trend.

Who is Zohran Mamdani?

Zohran Mamdani is a State Assemblyman from New York. He was born in 1991 in Uganda and is of Indian-Muslim descent.

Mamdani’s mother is a famous filmmaker named Mira Nair. She directed Monsoon Wedding, which was nominated for an Academy Award in 2001, and has worked on various projects for Disney.

His father, Mahmood Mamdani, is a professor at Columbia University with expertise in “postcolonial studies.”

Columbia was also the home of Edward Said, the famous scholar who pioneered postcolonial studies and became the leading academic voice for the Palestinian resistance movement.

As a child, Zohran followed his parents around the world but spent many years in New York City. The future socialist politician attended the elite Bank Street School for Children on the Upper West Side of Manhattan (tuition currently exceeds $65,000 per year).

He later attended and graduated from Bowdoin College, a small and highly selective liberal arts college in Maine, as a member of the Class of 2014.

While at Bowdoin, Zohran no doubt made his father proud when he became one of the founders of the local chapter of Students for Justice in Palestine (SJP). SJP is the organization that has been at the center of violent campus protests nationwide.

Zohran Mamdani is both a socialist and a fervent anti-Zionist. He has vowed as mayor to arrest Israeli Prime Minister Benjamin Netanyahu whenever he visits New York City (even though he would have no legal basis at all to do so). |

|

| | As mayor, New York City would arrest Benjamin Netanyahu. This is a city that our values are in line with international law. It’s time that our actions are also…. It’s time that we actually step up and make clear what we are willing to do to showcase the leadership that is sorely missing in the federal administration. - Zohran Mamdani (11/25/2024) |

|

|

| Mamdani at an anti-Israel protest in Manhattan |

|

| Mamdani’s foreign policy positions will no doubt alienate many New Yorkers and, on that basis alone, force them to re-evaluate their commitment to the city as a place to live, work or operate a business.

His economic agenda is also highly concerning. New York City, which represents the headquarters of nearly 10% of all Fortune 500 companies, is America’s financial capital and home to many highly paid business professionals.

Mamdani has proposed a millionaire’s tax (an incremental 2% flat tax on anyone earning more than a million dollars per year). He also has proposed an increase in the city corporate income tax rate from 7.5% to 11.5%.

Mamdani’s socialism in infused with woke race ideology. His campaign materials call for higher property taxes for those who live in “richer and whiter neighborhoods.”

These potential tax hikes would be used to fund a wide array of spending programs, including free public transportation and free child care. He has also wants to create grocery stores that will be owned and operated by the city itself.

Other policies he champions include strengthening rent control laws and gradually lifting the minimum wage to $30 per hour.

Will New York City be safe?

Crime is another variable that New York businesses and residents now must revisit.

Using abstract academic language that would make his Columbia professor father beam, but perhaps terrify subway riders, Mamdani has declared that “violence is an artificial construct.”

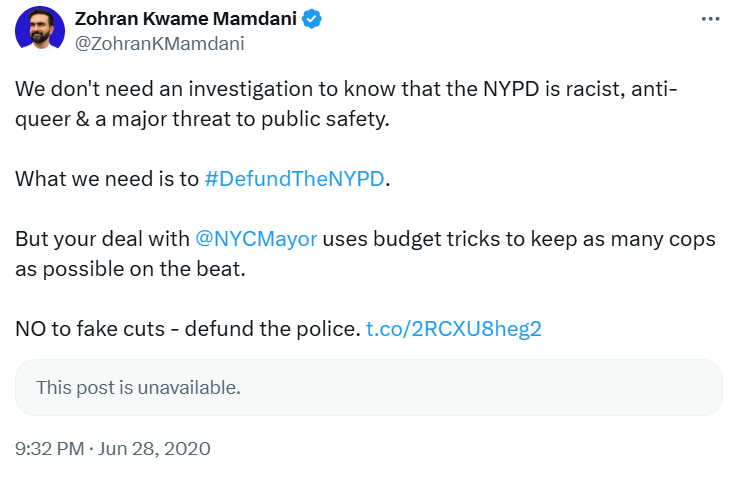

When it comes to the police, Mamdani softened his rhetoric a bit during the campaign. There are deleted tweets from 2020, however, that seem to reveal his real inclinations. |

|

|

| Real estate agents are already hitting social media with stories of New York residents seeking a new home and would-be buyers losing interest.

We also saw an immediate market reaction in certain Real Estate Investment Trusts (REITs) that have assets that are predominantly located in New York City.

Three prominent REITs with large New York City exposure are Vornado (VNO), SL Green (SLG) and Empire State Realty (ESRT). These stocks declined between 6% and 8% in the days following the election, while the REIT Index as a whole was down less than 1%.

A Zohran-proof investment

One REIT that does not stand to lose from Mamdani becoming Mayor of New York is Mid-America Apartment Communities (MAA), a holding within our Income Builder Model Portfolio.

Headquartered in Germantown, Tennessee, MAA owns, operates and develops apartment communities in the southeast, southwest and mid-Atlantic regions of the United States. The company’s assets include over 104,000 rental apartment units.

New Yorkers who may now be contemplating a move may want to take a hard look at one of MAA’s many upscale apartment communities across 16 states.

Investors interested in a high dividend yield and solid long-term growth prospects may want to take a hard look at the stock.

As a REIT, the company is required to pay a large portion of its earnings as dividends. The stock currently offers a 4.1% dividend yield.

Since its IPO in 1994, MAA has consistently paid quarterly dividends. The dividend has never been reduced, even during the 2008-2009 financial crisis. |

|

|

| MAA annual dividends since IPO(Source: MAA) |

|

| Over the past 31 years, the company has unquestionably delivered for shareholders. MAA has generated an annualized total return of 12.5%, versus a 10.5% total return for the S&P 500. |

|

|

| MAA vs. S&P 500(Total return since January 1994) |

|

| MAA’s apartment portfolio is diversified across various sunbelt metropolitan markets with strong growth characteristics. |

|

|

| | The company caters to young, affluent professionals with a median age of 35. The most represented industry sectors that employ MAA tenants are healthcare, technology and financial services.

MAA is essentially a play on economic growth in highly attractive markets that have attributes that appeal to workers as well as employers. Texas and Florida alone represent approximately 40% of the apartment portfolio as measured by property-level income. |

|

|

| MAA’s Apartment Portfolio(Source: MAA) |

|

| Rental apartments in the sunbelt have delivered strong returns for decades… but the journey has not always been a straight shot up.

MAA shares have in fact faced a number of headwinds in recent years. We see strong potential upside in MAA as these headwinds reverse.

Even though the dividend per share is as high as it has ever been, MAA shares are down more than 30% from their all-time high achieved in January 2022. Shares are also currently down more than 10% from their highest levels of 2025, reached in March. |

|

|

| MAA share price(Last 5 Years) |

|

| Cyclical opportunity

MAA has faced two key challenges in recent years: excess supply and interest rates.

MAA performed extremely well in the aftermath of the pandemic, which accelerated the long-term population shift towards the sunbelt states.

MAA and its peers experienced strong rental growth trends in this time frame, and residential development in sunbelt markets picked up considerably.

What resulted a few years later has been a material—not severe, but material—mismatch between apartment supply and demand. New apartment units arrived on the market just as many renters were struggling to keep up with the inflation wave that followed the pandemic.

A new multifamily residential development (i.e., a rental apartment complex) typically requires 18 to 36 months to create, from site selection to construction to leasing.

Developers moved aggressively in the pandemic time frame, especially given the very low interest rate environment, and initiated many new projects.

The tide is turning

Given the lag effect from Covid-era development, new project launches in MAA markets peaked towards the end of 2024. But they are now trending down.

Meanwhile, rental demand has picked up as inflation has subsided and the economy has strengthened. Excess supply is now being absorbed. |

|

|

| | Supply in MAA markets is expected to decline further in the years ahead. The market conditions that gave rise to the pandemic development wave have essentially reversed.

Development activity has slowed down as a result of high interest rates, stagnating rents, and higher vacancy levels. This is visible in market data on new multifamily starts in MAA markets, which are at their lowest levels in years and below long-term trends. |

|

|

| | New starts peaked in the first quarter of 2022 at 1.6% of existing market supply (not so coincidentally as the MAA share price peaked and real estate developer enthusiasm was at maximum levels).

Fast forward three years, new starts were only 0.3% of total market supply in the first quarter of 2025.

Given the approximately two year time lag associated with new development, we know with a fair amount of confidence what the supply picture will look like in MAA markets over the next several years.

Market conditions should be relatively tight. If demand is at least stable, this should translate into higher occupancy and higher rental growth rates for owners of existing supply like MAA.

The impact of interest rates

Interest rates have a complicated impact on the MAA share price. When MAA shares peaked in January 2022, the 10-year Treasury yield was approximately 1.6%. Today, the 10-year yield is around 4.3%.

Higher long-term interest rates have been negative for the MAA share price for two reasons.

First, MAA, like all REITs, has debt on its balance sheet, although its leverage is relatively conservative. MAA is in fact one of only ten REITs that has a credit rating of A- or higher by the major rating agencies.

Notwithstanding the conservative balance sheet, higher interest rates do have a marginally negative effect on the company’s cash flow. So the rise in long-term interest rates in recent years has been a negative in that sense.

Second, high interest rates have been a problem for the MAA share price because real estate competes with bonds for investor capital.

The required dividend yield on REITs as an asset class goes up when investors can buy Treasuries at higher yields. When MAA shares peaked back in early 2022, opportunities in the bond market were far less attractive.

But unlike many other areas of the real estate market, high long-term interest rates can also be positive for apartment building owners.

Rent versus own

High interest rates not only discourage new supply, since developers need to borrow money to finance their projects, but they have an impact on tenant behavior.

Apartment landlords are not only competing with other landlords but single family homes as well. A young professional is often faced with a choice: do I continue to pay rent, or do I buy a house?

One of the most important variables affecting the rent versus buy decision is mortgage rates. The higher long-term interest rates are, the more expensive it is for a potential house buyer to own a house and the more difficult it is to qualify for a mortgage.

Mortgage rates have not only gone up in recent years, but single family housing supply growth has been constrained, which has put upward pressure on house prices.

Single family home starts nationwide have followed the same trajectory as multifamily starts since early 2022 (to a large extent a function of inflation and high building material prices). Single family starts are currently at their lowest level since 2020 (when lockdowns interfered with construction activity). |

|

|

| Housing starts (Last 5 Years) |

|

| What has emerged in recent years within MAA’s markets is a severe affordability gap between renting an apartment and buying a new home.

The rent versus own math in MAA’s markets has become highly skewed towards renting. Rental rates have been suppressed by the temporary over-supply situation, while home ownership costs have gone up dramatically. |

|

|

| | As the supply/demand picture shifts the balance of power from tenants to landlords in the years ahead, MAA should have plenty of room to nudge up rents given the high cost of single family housing.

If long-term interest rates do come down in the years ahead, this will make mortgage rates lower, but it may also stimulate buying demand, which would tend to make home prices even higher.

A low interest rate environment may also lead to a favorable economic environment, lifting employment and wages.

Strong economic growth translates into higher demand from tenants, who will be in a better position to compete for rental units in desirable apartment communities like those owned and managed by MAA.

Our expectation is that a scenario of declining long-term interest rates would overall be a strong positive for the MAA share price. Investors in all REITs should benefit from a decline in rates, as they have historically.

On the other hand, to the extent long-term rates stay level or even climb, this would only exacerbate the affordability problem for people who may aspire to live in single family homes.

In the context of limited future supply, MAA will therefore have room to raise rents and drive operating income growth across its portfolio. This should ultimately translate into healthy dividend and share price growth.

The place to be long-term

While we find the medium-term supply/demand dynamic very encouraging, it is important to stay focused as well on the long-term outlook for these markets.

States like Texas and Florida are likely to continue to drive economic growth in the United States, in no small part because they are governed well.

As the technology sector comes to play an increasingly important role across the economy, it has moved well beyond Silicon Valley. We now see tech hubs sprouting up all over the country.

AI data centers require vast amounts of energy. Cities and states that have the willingness and ability to meet these energy requirements should outperform economically.

Consider MAA’s home state of Tennessee, where some 7% of its apartment units are located across the Nashville, Memphis and Chattanooga sub-markets.

Elon Musk is reportedly in talks with Tennessee officials, via The Boring Company, to build a five to ten mile tunnel that will connect the Nashville airport to downtown Nashville.

Last year, Musk, via xAI, launched the “Memphis Supercluster,” which he has described as the “most powerful AI training cluster in the world.” Also known as Colossus, the supercomputer is located in a converted Electrolux factory.

Earlier this year, Musk bought another one million square foot site in Memphis to expand Colossus, which is powered by natural gas plants owned by the Tennessee Valley Authority.

While New York’s likely next mayor lobbies for government-run grocery stores, in states like Tennessee, local leaders are laying the groundwork for the AI revolution and America’s industrial renaissance.

The contrast in political visions is almost startling.

Investing often comes down to common sense. Long-term investors should prioritize investments in jurisdictions where voters are focused on growth and opportunity.

MAA offers investors a relatively high dividend yield backed by a high quality collection of real estate assets in markets with attractive long-term prospects.

MAA shareholders also have the opportunity to participate in a gradually improving supply/demand dynamic that is likely to support solid financial performance over the next three to five years. |

|

| | |

| Click HERE to learn more about our Model Portfolio subscription plans. |

|

| | | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | | |

|

|

|

|

| |

|