(5) Productivity and corporate profits are rising

One of the most encouraging trends in the economy is the clear improvement in productivity. Companies are becoming more efficient—helped by better technology, streamlined processes, and normalized supply chains.

ChatGPT, the first widely adopted generative AI model, may have launched only three years ago. Yet the productivity impact of generative AI is starting to show up in economic data.

Economists at the St. Louis Fed highlight that from 2015–2019, labor productivity grew 1.43% annually. From the fourth quarter of 2022—when ChatGPT debuted—through the second quarter of 2025, productivity accelerated to 2.16% per year.

To test whether AI adoption was a driver or if this was just a coincidence, they compared productivity growth across industries. They found that sectors with higher levels of AI adoption experienced meaningfully faster improvement relative to their pre-pandemic trends.

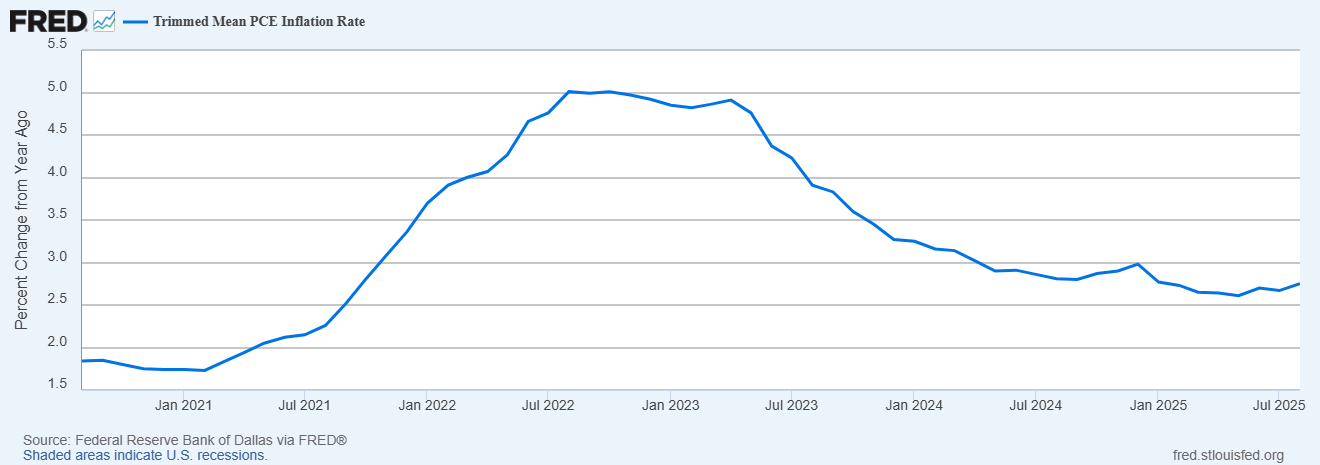

Higher productivity is the essence of economic prosperity: it holds down inflation, lifts profit margins, and supports long-term growth. While automation may reduce labor demand and slow wage growth, a cooling labor market helps bring down inflation and gives the Fed more room to pivot toward easier monetary policy.

(6) The OBBB will kick in next year

The One Big Beautiful Bill (OBBB) is poised to deliver a significant economic boost starting in January. Its mix of tax relief, investment incentives, and targeted spending directly supports both consumers and businesses.

Middle-class tax cuts and enhanced family credits increase disposable income and reinforce household demand. Business provisions—expanded expensing, R&D incentives, energy and manufacturing credits—lower the cost of capital and encourage new investment in equipment, AI infrastructure, reshoring, and energy build-outs.

Housing and workforce measures, permitting reforms, and infrastructure spending expand supply and improve long-term productivity.

In contrast to the end-of-year slowdown caused by reduced government spending and the temporary shutdown, the OBBB is likely to catalyze a meaningful uptick in private sector activity as 2026 begins.

(7) Geopolitics are stabilizing

Geopolitical shocks were a major contributor to the inflation and disruption that hindered stock market performance in 2022 and 2023. Today the backdrop looks considerably calmer. Energy prices have stabilized, trade routes are open, and supply-chain friction has eased materially.

Tariffs generated a brief market scare in April and remain a source of uncertainty. But the broader geopolitical picture has markedly improved.

Iran appears neutralized as a regional military threat. The Israel–Hamas conflict has largely wound down. Russia and Ukraine are reportedly in advanced negotiations toward a peace deal.

The defining geopolitical relationship of our era remains the one between the United States and China. Despite deep economic interdependence, strategic tensions—especially around Taiwan—are real.

Recent diplomatic engagement has been productive, however. In late October, the two countries reached a trade agreement that secured U.S. access to rare earth minerals in exchange for tariff reductions and other concessions.

The year ahead

For much of November, markets have been preoccupied with downside risks. But the broader investment environment remains fundamentally strong.

Technology continues to advance rapidly and deliver measurable productivity gains. Monetary policy is turning more supportive as inflation cools. Pro-growth legislation is weeks away from taking effect. And the global landscape is far more stable than it was a year ago.

None of this guarantees a smooth path forward, but it does provide a basis for optimism. As we enter the holiday season, we are grateful for your trust and partnership—and we look forward to navigating the opportunities ahead together.