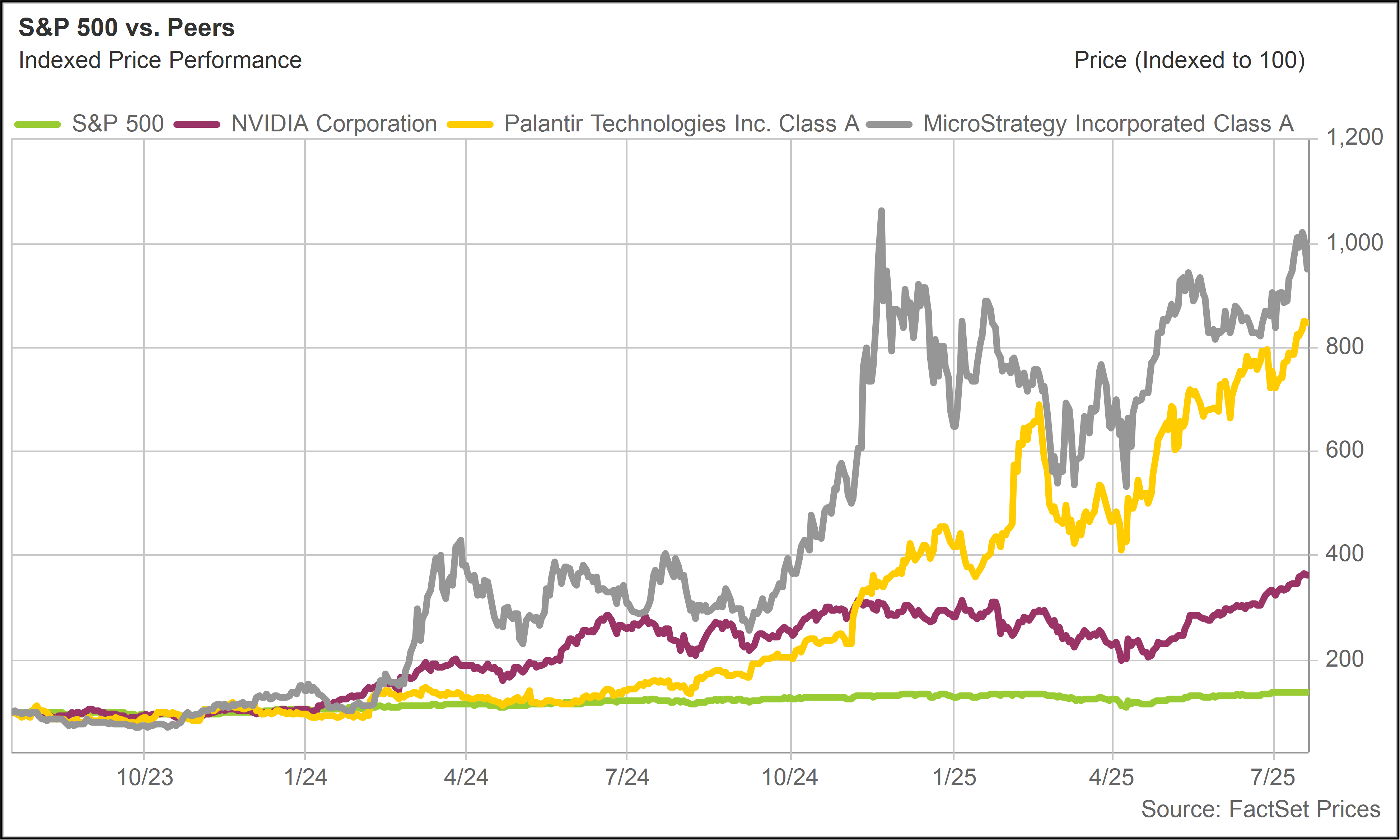

Crypto is another area of markets where retail saw it first. Digital assets are now going mainstream, but it was small investors who initially seized the opportunity.

While Wall Street institutions poked fun at Bitcoin—with JPMorgan’s CEO Jamie Dimon famously calling it a “pet rock”—regular folks, often quite young, were accumulating it. The ones who got into Bitcoin early enough made millions off investments of just hundreds or thousands of dollars.

Only now are institutional investors dipping their toes into Bitcoin and other crypto investments. Yet many remain steadfastly opposed or simply uninterested in the space.

The old stereotype

Retail investors are historically depicted as underinformed, susceptible to hype and prone to panic, whereas professionals are supposed to be knowledgeable and even-keeled.

It is of course foolish to make sweeping generalizations about a group of people that is now some 60 million strong and represents nearly one-quarter of the adult U.S. population.

Inevitably, there will be many misguided investors among them who fall into the old traps. But the retail investment landscape has changed dramatically—in large part thanks to technology.

Today’s retail base casts a wide net: retirees managing their own IRAs, professionals reallocating 401(k)s, high-income earners using brokerage accounts as tax-efficient savings vehicles, and Gen Z investors getting market exposure through mobile platforms.

Many of these investors are entirely self-directed. They are not relying on legacy asset managers or traditional financial advisors. They are relying on direct access, research platforms and their own independent judgment.

They are also turning to information sources outside the financial mainstream. Social media, especially X, is filled with investment content—not to mention podcasts and independent web-based research services like 76research.

To become an astute investor in the past, one perhaps had to attend business school or receive direct training at an investment firm.

Today, regular people with basic literacy and math skills are not only able to educate themselves on investment fundamentals but also have ample access to information about the companies and opportunities they are researching.

With the advent of AI, access to knowledge and information is increasing exponentially. The only limiting factor on becoming a good investor seems to be curiosity.

Where the pros fail

If individual investors, in the worst case scenario, are ill-informed and emotionally erratic, professional investors are potentially held back in many ways themselves.

Drawing upon decades of firsthand observations, we can think of several ways in which professionals are actually disadvantaged versus the “amateur” investor.

Group think

Professional investors work in organizations with distinct personalities and brand identities.

These organizations are typically led by people, usually older, who tend to have strong and sometimes inflexible views on investing. They also control compensation.

Whereas individual investors are basically thinking for themselves, decisions in asset management organizations are often made by committee.

Alternatively, there may be some kind of opaque, semi-political decision-making process in which only a few individuals have final say.

Some firms have strong investment cultures that invite dissenting views, but many times biases just get reinforced. Mistakes get covered up and ignored.

Asset management firms are as much as about marketing as they are about delivering performance. This leads to inertia. Investment strategies may fail to evolve because the firm’s commercial positioning needs to remain consistent and “on brand.”

Incentives

Individual investors naturally want to do as well as they can with their own savings—subject to certain parameters, like volatility and liquidity.

Professional investors often have entirely different goals. These may range from maximizing their personal compensation to playing office politics to just avoiding getting fired.

Generally speaking, investment professionals want to be associated with good outcomes, but there are many distractions and competing priorities. Being the best investor in the office is not necessarily the path to becoming the most successful employee.

Tunnel vision

Most asset managers have their teams organized by industry sector. In some cases, especially at larger firms, analysts can be hyper-focused on subsectors, such as food retail or medical equipment.

Industry specialists may end up with more extensive information about the companies they cover than anyone else. But this narrow focus comes at a cost if they lack the broader perspective to compare these opportunities to others.

While sector experts may end up with a very good understanding of how a particular set of companies work, they may have almost total ignorance of other related industries. This could become a huge blind spot.

The key to successful fundamental investing is having a firm grasp on the things that matter most—not drowning oneself in trivia.

Risk aversion

The old adage that “nobody ever gets fired for buying IBM” applies to asset management firms as well as any corporation.

Sometimes, the smart thing to do as an investor is to bear an elevated amount of risk (perhaps with a smaller amount of capital) because the upside potential is so attractive. We have discussed Bitcoin in this context (see The Bitcoin Endgame).

These “asymmetric” bets are often the most compelling, but they may also have a higher failure rate.

Asset management professionals understand that mediocrity, and even somewhat disappointing performance, can easily be tolerated or overlooked in a corporate setting, especially if the boss likes you.

Extremely bad outcomes, however, need a scapegoat. This creates a bias towards playing it safe and avoiding anything new and unfamiliar.

Political bias

A professional investor’s political and ideological views can also compromise their objectivity and therefore their ability to invest well. This phenomenon seems to have become more prevalent in recent years, especially when it comes to Trump.

Professional investors are not robots. They are human beings with political opinions and attitudes.

They are often educated at elite universities. They tend to live in major financial capitals like New York, Boston, San Francisco and Los Angeles. Their political views often reflect the perspectives that are dominant within their environments.

American companies lead global markets, representing about two-thirds of the market cap of all the stocks in the world. But a very large swath of global money managers are European, either based in European cities like London, Paris and Frankfurt, or working from the U.S.

We can count on one hand the number of European investment professionals we have met in our careers who align in any respect with the current American President.

An intriguing academic paper was released in 2024 that documented the effect of political bias on mutual funds.

A finance professor at Washington University in St. Louis, in conjunction with a researcher at a large asset manager, discerned a measurable difference in how portfolios were constructed based on the fund manager’s partisan affiliation.