Investing is all about turning one dollar into two. Compound interest is the not-so-secret magic formula (or at least it used to be).

At a 10% annual rate of return, which approximately matches the performance of the S&P 500 over the past 20 years, it takes a little more than seven years to double your money.

But what if you could double (or triple, or pick your own multiple) your money in a matter of days?

There is a rapidly growing list of entrepreneurs out there now using Bitcoin for that exact purpose.

Welcome to the era of the Bitcoin Treasury Company.

Bitcoin Treasury Companies are publicly traded companies that have as their core asset a certain quantity of Bitcoin on their balance sheets.

Strategy (MSTR), founded by Michael Saylor and formerly known as MicroStrategy, is the pioneer, but there have been some high profile newcomers in recent weeks.

These include Twenty One Capital, which investors can currently access through a listed Special Purpose Acquisition Company (SPAC) called Cantor Equity Partners (CEP).

The Twenty One deal brings together Tether, the largest issuer of stablecoins; Bitfinex, a major crypto platform; and Softbank, the deep-pocketed Japanese technology investor.

The energetic and widely followed Bitcoin advocate Jack Mallers will be CEO of the new company.

Shares of CEP have skyrocketed since the transaction was made public. They were trading just above $10 per share before the announcement on April 23, got very close to $60 a few days later, and since seem to have settled in the $30s.

Then, on May 7, Strive Asset Management, the asset management firm founded by Vivek Ramaswamy, announced a deal with a listed company called Asset Entities (ASST) to form the “first publicly traded asset management Bitcoin Treasury Company.”

Whereas the parties involved in Twenty One are accessing public markets through a SPAC, the Strive deal is structured as a “reverse merger.”

The interesting twist with this one is that it contemplates the formation of a new company that will be capitalized with contributions of Bitcoin from outside investors.

Bitcoin owners will have the opportunity to transfer their Bitcoin holdings into the company and in return receive shares on a tax-free basis.

Shares of ASST were trading below $1 before the deal announcement and in the days that followed got close to $9.

It’s worth noting for future reference—investors in CEP and ASST were able to achieve enormous returns even after the announcements were made. If you were attentive enough to buy these stocks just after the deals were announced, you could have generated returns well above 100%.

Bitcoin Treasury Companies are now commanding valuations that represent, in some cases, very large premiums to underlying Bitcoin ownership.

With regard to CEP and ASST, the transactions required to form these companies are not even completed.

2008 all over again?

This may all sound like “irrational exuberance,” or even a scam—too good to be true.

How can someone just take a pile of money (whether crypto or fiat), hire some lawyers to build a company around it, and then it instantly becomes worth a lot more money?

It makes sense to approach all of these stocks with healthy skepticism.

Investors who were around in 2008 might recall the Collateralized Mortgage Obligation (CMO).

Financial engineers used leverage to buy up a bunch of mortgages, slice and dice them into various new securities, and “create value” out of thin air.

The global economy practically collapsed as a result of these activities. The mortgages that Wall Street CMO managers were buying were far riskier than they claimed.

Investors who then bought the securities that they manufactured typically had little understanding of what they owned. This is largely because ratings agencies were slapping the “investment grade” label on these instruments, even though many ultimately proved to be totally worthless.

So skepticism is warranted. But let’s not be too skeptical.

After all, the entire financial services sector—really all businesses—are built on the principle of taking a dollar of capital and, by adding value somehow, transforming it into many more.

It is therefore possible that these Bitcoin Treasury Companies are genuinely onto something. Investors in these companies are certainly encountering a very high level of success.

What is mNAV?

In the emerging world of Bitcoin Treasury Companies, the go-to metric is mNAV. This concept is a good starting point for anyone who wants to understand these business models.

mNAV refers to the enterprise value of the stock (market capitalization plus debt) divided by Bitcoin NAV (the total market value of all Bitcoin owned).

A hypothetical company with a market capitalization of $100 million, debt of $20 million, and Bitcoin on the balance sheet worth $60 million has an enterprise value of $120 million ($100 million + $20 million) and an mNAV of 2.0 ($120 million/$60 million).

mNav reflects how much more the company is worth than the Bitcoin that it holds. But it is really just a modification of the traditional valuation metric known as Price to Book (P/B).

The Price to Book ratio measures the share price in relation to the book value of the assets that the company owns (which sometimes reflects what a company actually paid for those assets and sometimes reflects their market value).

Companies that generate high returns on assets are rewarded with high P/B ratios, because they are putting their assets to good use.

Financial services stocks in the U.S. currently trade at just over two times Price to Book. Within financial services, banks tend to have somewhat lower ratios, while asset managers and service providers have much higher P/B ratios.

One could argue that banks are somewhat comparable to Bitcoin Treasury Companies in that their primary asset is financial capital.

Successful banks can have relatively high P/B ratios. JPMorgan Chase (JPM), for example, is the most valuable bank in the U.S. with a market cap around $700 billion.

JPM trades at approximately 2.2x its price to tangible book value (the net value of all the financial instruments it holds). JPM is valued in the stock market at a lot more than the financial assets it owns.

When a premium is warranted

If a company can legitimately create value off of its assets, it deserves to trade at a premium to asset value. The average stock in the NASDAQ 100, which is loaded with technology companies, trades at about 7.5x book value.

It is easy to understand how tech stocks can trade at big premiums to book value. The key assets are intangible and often never get reflected in any way on the balance sheet.

While Bitcoin Treasury Companies can be compared to banks, it may not be unfair to compare them to tech companies as well. Bitcoin represents a sort of intersection between money and technology.

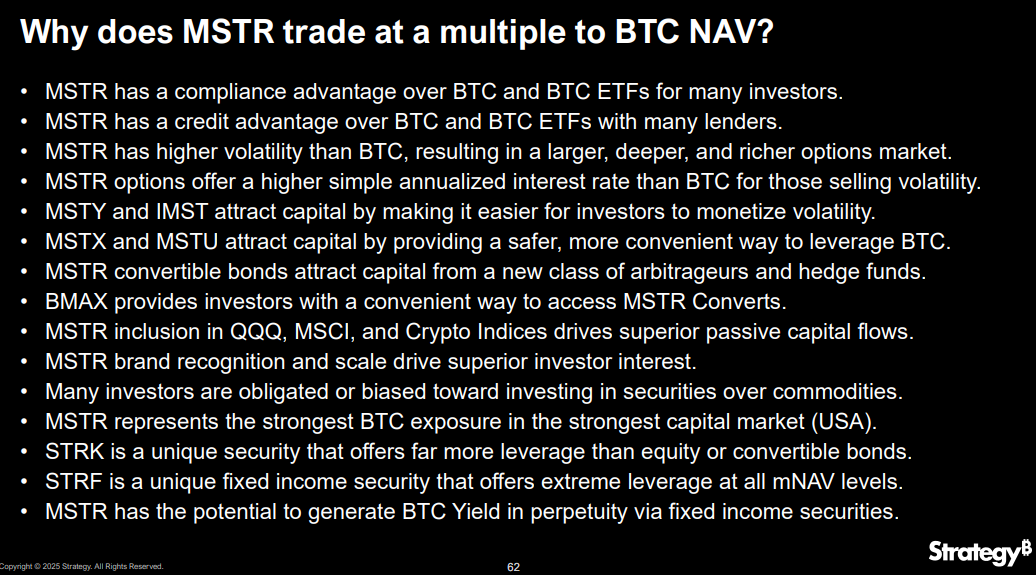

But for a Bitcoin Treasury Company to deserve a premium, one needs to be able to make the case that it can create value above and beyond appreciation of the Bitcoin that it owns.

Saylor’s story

Any discussion of Bitcoin Treasury Companies has to begin with Michael Saylor and MSTR.

In 2020, Saylor persuaded his Board of Directors to move the software company that he founded and ran for decades in a new direction. The business had a nice cash hoard, about half a billion dollars, but was struggling to grow in the context of Covid lockdowns.

Meanwhile, the Fed had knocked interest rates effectively to zero and was printing money with reckless abandon, depriving the company of the opportunity to earn a decent return on its cash balance, which was also getting debased in real terms.

As Saylor has pointed out many times in interviews, including his conversation with Trish in October 2024, he was desperate. Bitcoin was the solution.