Meanwhile, the S&P 500 is a little more than 1% off its all-time highest levels, with real GDP growth widely expected next year to come in at 2% or higher.

Long-term interest rates are at manageable levels. The 10-Year Treasury yield is now hovering around 4.1%.

Just on the basis of these objective markers, the economy appears to be in reasonably good condition.

What about tariffs?

If you were paying attention to business news in April of this year and the months that followed, the fact that the U.S. economy is now so healthy may come as a surprise.

“It's more likely than not that we're going to have a recession—and in the context of a recession, we'll see an extra 2 million people be unemployed.”

This was the dire prediction of Harvard economist Larry Summers, who served as Treasury Secretary during the Clinton administration, shortly after Trump’s Liberation Day tariff announcements in April 2025.

Even after Trump walked back his most extreme tariff proposals, Summers still insisted tariffs would crush growth and drive inflation higher.

“The core idea of tariffs as a device to extort concessions remains. Even if none of the suspended tariffs are ever put in place, we are still above Smoot-Hawley levels, and that will meaningfully increase inflation and unemployment.”

Summers has had to retreat from public view lately, not because his predictions were off but as a result of his personal association with Jeffrey Epstein. Yet he was hardly alone in his negativity this year.

In mid-April, a petition began to circulate called The Anti-Tariff Declaration, which to date has more than 2,000 signatures.

The document was put together by a collection of recognized economists on both sides of the political aisle. The statement warned that “American workers will incur the brunt of these misguided policies in the form of increased prices and the risk of a self-inflicted recession.”

The conventional wisdom across Wall Street and academia was that Trump’s tariff policies were ill-conceived and would be disastrous—a policy mistake of epic proportions.

Tariff anxiety peaked in April, about a week after Liberation Day and the day before Trump’s pivot to a more moderate stance. On April 8, 2025, the S&P 500 closed down more than 15% for the year and touched what would be its lowest level of the year.

At the time, we shared our view that Trump’s most extreme tariff scenarios would likely not come to pass and that the overall impact of tariffs on the economy was likely being exaggerated (“Will Trump Pivot?”).

After Trump backed away from his originally proposed tariff rates, the market began to recover. By the end of April, the S&P 500 was only down about 5% for the year.

The S&P 500 has now advanced more than 35% since the April depths, which in retrospect was pricing in an economic catastrophe that simply never happened.

What we now know

Stock market gains have been driven by earnings growth and encouraging economic data. This progress has occurred in the face of continued criticism of tariffs—with ongoing emphasis on “stagflation” scenarios.

Fast forward some eight months from Liberation Day, we are now in a much better position to see what sort of damage, if any, tariffs have actually done to the U.S. economy. It is no longer just a matter of speculation.

The results are quite encouraging. And the mild impact of tariffs, especially on inflation, is lending support to markets.

Even with substantial tariffs in place that have been generating hundreds of billions of dollars per year in revenue for the U.S. Treasury, a consensus appears to be forming that any harm has been relatively minor… and increasingly falling into the rearview mirror.

A less hawkish Fed

For most of 2025, Fed Chair Jerome Powell has been sounding alarm bells on tariffs—in particular, their potential to create inflationary pressure. It has been among his top reasons to resist steeper interest rate cuts as labor market conditions have deteriorated.

Echoing the conventional wisdom, Powell noted in April that tariffs were “highly likely to generate at least a temporary rise in inflation.”

With tariff-driven inflation top of mind, the Fed kept the Fed funds rate in the 4.25% to 4.5% range until September 2025. This was a level that is widely considered “restrictive,” meaning it is high enough to hurt demand and push down inflation pressure.

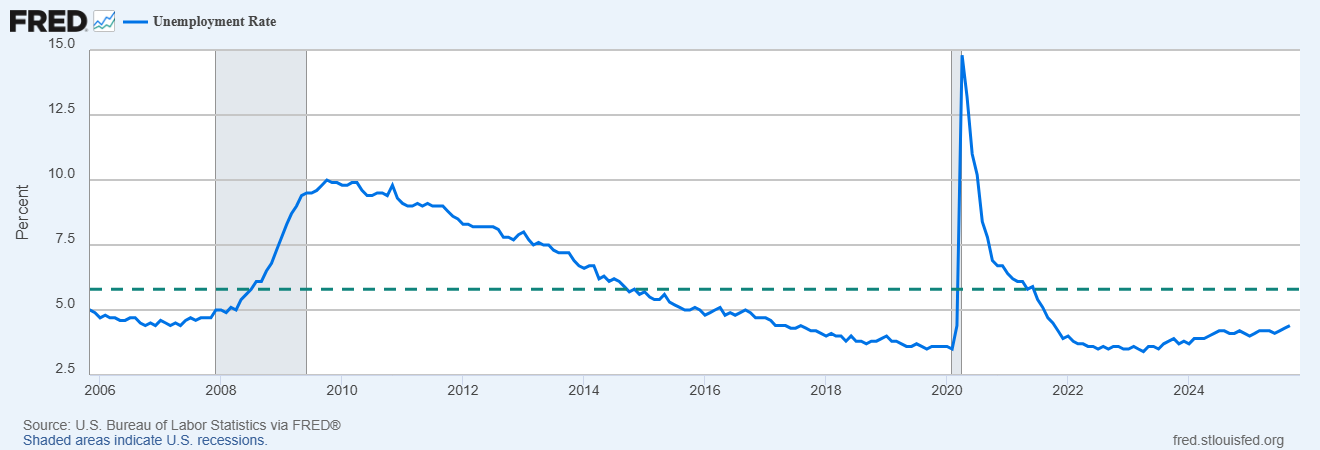

Although the Fed continued to flag inflation risk, weakening labor market conditions eventually prompted the Fed to start cutting again.

With inflation data coming in not too far above the 2% target, the Fed cut interest rates by 0.25% two more times, most recently on December 10. The Fed funds rate now sits in the 3.5% to 3.75% band.

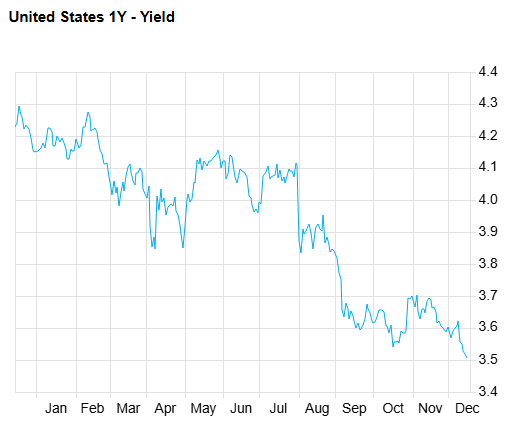

Expectations for short-term interest rates have fallen meaningfully over the course of the year. This can be seen in the 1-Year Treasury yield, which now sits at their lowest levels of the year, close to 3.5%.