He is not alone. Seth Klarman of Baupost Capital and Peter Lynch of Fidelity also focused on spin-offs as a form of “special situations” investing.

Investors in special situations (typically hedge funds) look for unique opportunities to take advantage of anomalous market conditions.

Dan Loeb, founder of Third Point, recently reflected on this theme in an interview. He described how event-driven investors often find opportunity in situations where a new security was created and the natural shareholder base has not yet formed.

A spin-off can create exactly that situation.

After the Board of Directors of a public company decides to spin off a business, shareholders automatically receive shares in the new company.

Some shareholders may not understand the business. Some may not be permitted to own a smaller company. Some may sell because the position is too small to matter.

Others may sell simply because the stock showed up in their account and they do not want to do the work.

That selling pressure can temporarily depress the price of the new company. This is one reason spin-offs have historically attracted value-oriented investors.

But there is another reason. Businesses often perform better after they are separated.

Inside a large parent company, a business may be underappreciated, under-managed, or under-incentivized.

The parent company usually has higher priorities. Management teams running the smaller business unit often have limited autonomy. Capital allocation tends to be dictated by the needs of the larger enterprise.

But once the business becomes independent, the incentives change.

Management gets its own stock. The board of the new company is focused on a single business line. Capital allocation can be tailored to the company’s specific opportunities.

Whereas the business unit may have previously been a rounding error in a much larger operation, investors can now evaluate the company on its own merits. In many cases, the business becomes sharper, more focused, and more efficient.

This does not mean all spin-offs are good investments. Many are not.

Sometimes the parent company is getting rid of a weak business. Sometimes the spin-off is burdened with too much debt or other liabilities, such as lawsuits. Sometimes the business is structurally challenged or the apparent cheapness is justified.

The old mechanical strategy of buying into almost every spin-off no longer works the way it once did. Markets are more efficient. Investors are more aware of the playbook. There are many more professional investors searching for the same set-ups.

Investors in spin-offs nowadays therefore need to be more discriminant than they perhaps were in the past. Yet the right ones can still be quite attractive.

What makes this one interesting

The newly received security—which was spun off by a financial services stock that is held within the American Resilience Model Portfolio—has several characteristics we like.

The underlying business is subscription-based, with sticky recurring revenue.

It has high profit margins, serving a large addressable market with well-known brands.

It leverages hard-to-replicate proprietary data sets and has become embedded in customer workflows.

The market is just now coming to terms with this opportunity. The shares have been trading for less than two weeks.

Below, we share what we have learned about this business… and why we view it as a keeper.

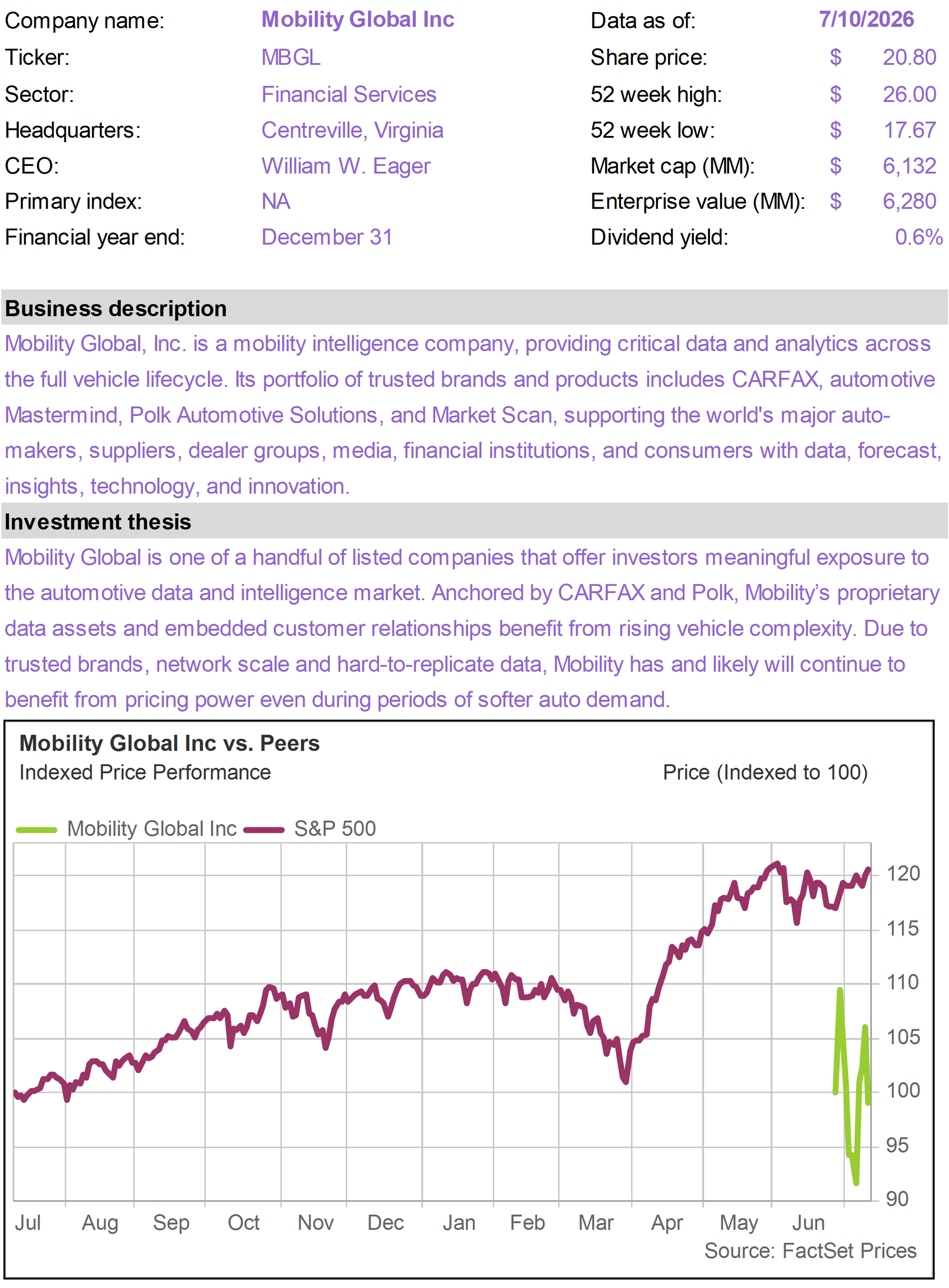

Introducing Mobility Global (MBGL)

Mobility Global (MBGL) was recently spun out of S&P Global (SPGI), a current holding of the American Resilience Model Portfolio.

Shares of MBGL began trading on the New York Stock Exchange on July 1, 2026. Shareholders of SPGI as of the close of business on June 15, 2026 received one share of MBGL for every share of SPGI they owned.

SPGI is best known for its ratings business, market intelligence, indices, and commodities data. MBGL is different. It is also a data business, but it targets the automotive industry.

Its focus on the auto sector, rather than financial services, made it interesting—but also somewhat non-core (along with the fact that it represented less than 10% of total company revenue).

By separating the business, SPGI became cleaner and more focused, while shareholders received ownership in a standalone automotive data and analytics platform.

At first glance, automotive data may not sound especially exciting.

The auto industry is cyclical. Vehicle affordability is under pressure. Dealers face margin pressure. EV penetration is changing the industry. Tariffs, supply chains, and regulation are all creating uncertainty.

But that growing complexity is exactly why the data matters.

MBGL is not an automaker. It is not an auto parts supplier. It is not a car dealer. It is an information-services business whose end market happens to be automotive.

The company operates through two main segments: CARFAX and B2B Solutions.

CARFAX represents about 65% of revenue. B2B Solutions represents about 35%. Combined, MBGL generated approximately $1.75 billion of revenue in 2025, consisting of roughly 81% subscription revenue.

CARFAX: The crown jewel

For many used car buyers, a CARFAX report is not merely a report. It is a trust signal.

Used car transactions are filled with information gaps. The seller always knows more than the buyer. The buyer worries about accidents, title problems, odometer issues, maintenance history, recalls, prior ownership, and hidden defects.

CARFAX helps reduce that uncertainty.

According to the company, CARFAX has 96% in-market awareness and 85% mascot recognition, making it the most relied-upon brand among third-party automotive providers.

It also has more than 38 billion vehicle history records from more than 177,000 sources, including dealers, service shops, police agencies, and OEMs. This represents a data network that was built over decades and cannot be easily replicated by competitors.

The power of CARFAX comes from the combination of consumer awareness and dealer adoption. Consumers ask for CARFAX by name. Dealers need the product because consumers trust it.

Dealers and service shops contribute data. More data improves the product. A better product reinforces consumer trust. That is the flywheel.

CARFAX also extends beyond the traditional vehicle history report.

Its products include dealer subscriptions, vehicle listings, service retention tools, consumer alerts, lender and insurer products, and CARFAX Car Care. The company has more than 53 million Car Care users, giving it a large consumer audience beyond the moment of vehicle purchase.

The more CARFAX can expand from “vehicle history report” into a broader vehicle ownership platform, the more valuable the brand becomes.

B2B Solutions: Strategic upside

The B2B Solutions business is less familiar to consumers but strategically important.

This segment includes brands and platforms such as Polk, automotive Mastermind, Market Scan, Data Studio, VIN Solutions, Recall, forecasting tools, and supply-chain intelligence.

These products help automakers, suppliers, dealers, lenders, and other industry participants make better decisions around what products to build, how to allocate production, pricing, marketing, and inventory management.

These are high-stakes challenges. MBGL provides data and analytics to help address them.

The company serves 100% of the top 40 global automakers, 94% of the top 100 automotive suppliers, and more than 40,000 dealer customers. It has approximately 60 billion vehicle records and 177,000+ data sources.

MBGL is not only helping consumers understand a used car. It is also helping the entire automotive ecosystem plan, market, sell, finance, service, and analyze vehicles.

This gives the company multiple ways to grow.

Why the spin-off may be mispriced

MBGL currently trades at a lower multiple than many premium information-services companies.

There are valid reasons for that.

It is newly public. It has no long standalone track record. It is exposed to a single end market. It began life with debt. Some investors may view it as an auto-adjacent business rather than a data compounder.

There may also be the usual technical selling pressure. Many SPGI shareholders did not intend to own an automotive data company. They bought SPGI for ratings, indices, market intelligence, and financial data.

When those shareholders received MBGL shares, some likely sold without much analysis.

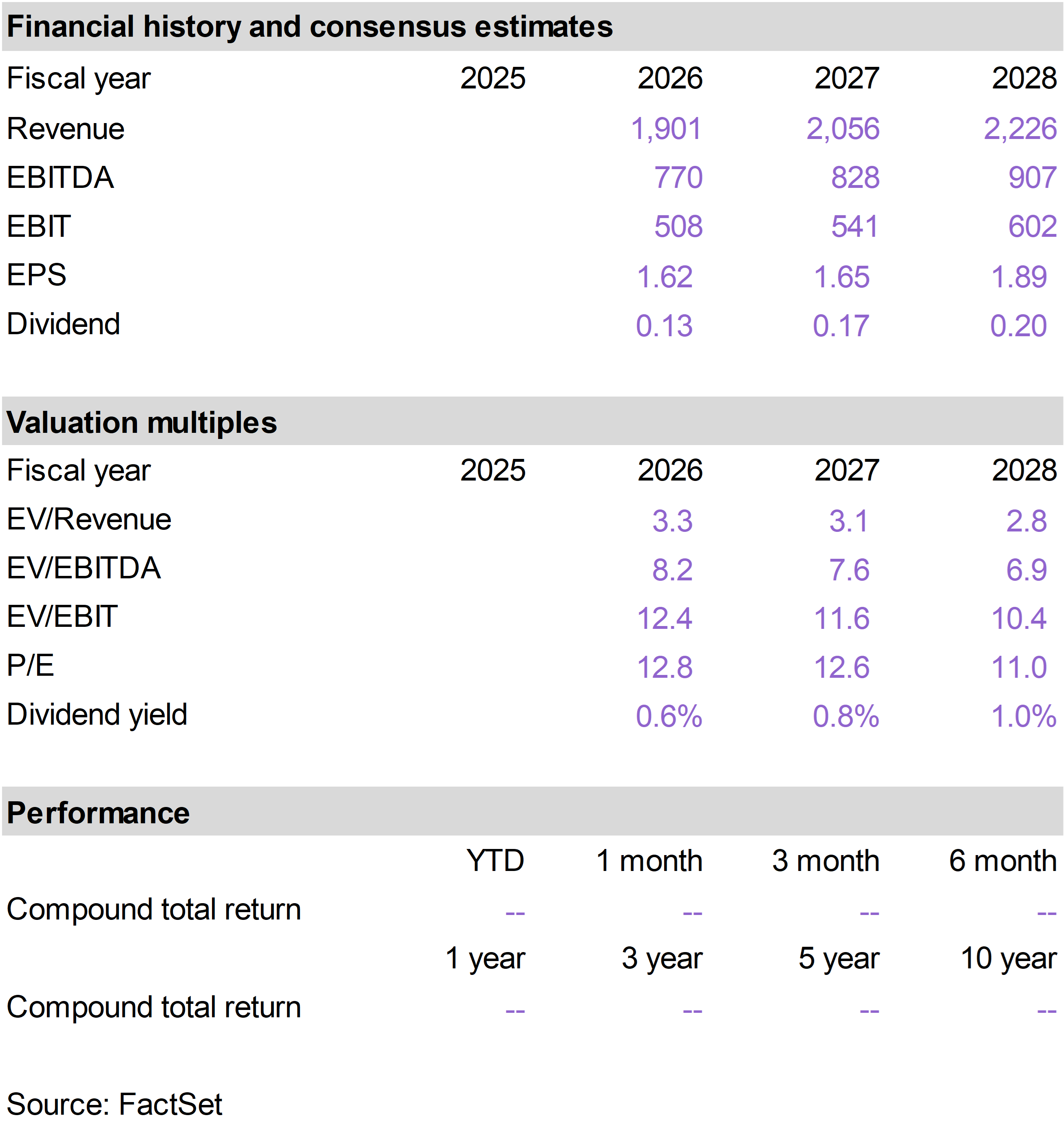

The key question is whether the valuation discount is justified by business quality. MBGL now trades at less than 13 times 2027 consensus earnings estimates, versus approximately 19 times for the S&P 500.

Yet MBGL has many of the characteristics investors typically reward in high multiple information-services companies: proprietary data, recurring revenue, high margins, strong brands, embedded workflows, low capital intensity, and meaningful free cash flow generation.

Management is targeting 7.5% to 10% annual organic revenue growth, 8% to 11% adjusted EBITDA growth, roughly 50 basis points of annual margin expansion, and the return of 75%+ of free cash flow after investments to shareholders annually.

If management executes, the stock should not trade like a discarded auto-related spin-off. It should increasingly be viewed as a high-quality vertical data platform.

Electric vehicles: Threat or opportunity?

EVs are growing as a percentage of the automotive fleet. Today, they represent less than 10% of new light-duty vehicle sales. Over the next 10 years, many forecasts suggest penetration could approach 50%.

Will the shift to EVs hurt CARFAX or MBGL? We think the more likely answer is the opposite. The reason is that EVs increase vehicle complexity.

A used EV buyer still cares about accident history, ownership, title status, service records, recalls, and valuation. But the buyer also needs to understand battery condition, software updates, charging history, range degradation, warranty status, repair complexity, and residual value.

That creates new demand for trusted data. For the B2B Solutions segment, the EV transition may even become more relevant.

Automakers and suppliers need forecasting, production planning, supply-chain analysis, tariff modeling, battery sourcing insight, and technology roadmaps. The more complicated the automotive industry becomes, the more valuable decision-grade data becomes.

To be fair, there are risks. EVs may reduce some traditional dealer service revenue. Direct-to-consumer models could pressure the dealer channel over time. OEMs may control some EV-specific data more tightly.

But the global vehicle base turns over slowly. MBGL serves a massive installed base of vehicles, and its relationships with OEMs, dealers, suppliers, and service shops give it a strong position to adapt.

Over time, EV penetration could actually make MBGL more valuable if CARFAX becomes the trusted third-party record for battery health, software history, ownership cost, and EV-specific vehicle condition.

Other risks

The biggest risk is end-market concentration. MBGL is tied to the automotive ecosystem. A severe downturn in vehicle sales, dealer profitability, used-car transactions, or OEM marketing budgets could pressure growth.

Competition is also real. Experian AutoCheck competes with CARFAX in vehicle history. Cox Automotive, Kelley Blue Book, Autotrader, J.D. Power, Black Book, and others compete across different parts of the ecosystem.

There is also AI risk. AI could make it easier for competitors to build new interfaces, automate workflows, or aggregate data in new ways.

But AI also increases the value of proprietary datasets. Generic models need differentiated data to produce differentiated insights.

MBGL’s data is not generic. That is why we view AI more as an opportunity than a threat, provided management executes well.

Reasons to hold

MBGL is a newly independent company with a strong brand, proprietary data, high margins, recurring revenue, attractive free cash flow, and a potentially misaligned initial shareholder base.

The market may currently be valuing the company as an auto-exposed spin-off. We think it deserves to be analyzed as a vertical information-services platform.

CARFAX brings consumer trust. Polk and B2B Solutions give it enterprise relevance. The dealer and OEM network gives it distribution. The subscription model gives it resilience.

The spin-off structure may offer investors an attractive entry point, as it often does.

Over time—as management executes, the shareholder base matures, and investors recognize that MBGL is a better business than the initial multiple implies—shareholders could see solid outperformance.