|

| | | | The Great Debasement Theory |

|

|

Wall Street is finally waking up to a macroeconomic reality that has guided our investment thinking ever since 76research began in early 2024…

The foundations of the global fiat money system are eroding. From private individuals to central banks, investors are gravitating toward assets that will protect them in an era of monetary fragility.

Earlier this month, Nikolaos Panigirtzoglou, a widely followed market strategist at JPMorgan, highlighted in a note to clients what he called “the debasement trade.”

Debasement, or monetary debasement, refers to the decline of the real value, or purchasing power, of a currency as a result of the actions of the central bank.

The concept originates in ancient times, when metallic coins would be melted down and remixed so that they had less gold and silver content—in other words, physically debased (made less pure) with lower value metals like copper or lead. |

|

|

| A debased Roman coin, circa 270 AD (Less than 5% precious metal) |

|

| The JPMorgan report describes a structural shift, encompassing both institutional and retail investors, away from fiat assets that are backed solely by government issuance and toward commodity-based and digital stores of value—most notably, gold and Bitcoin.

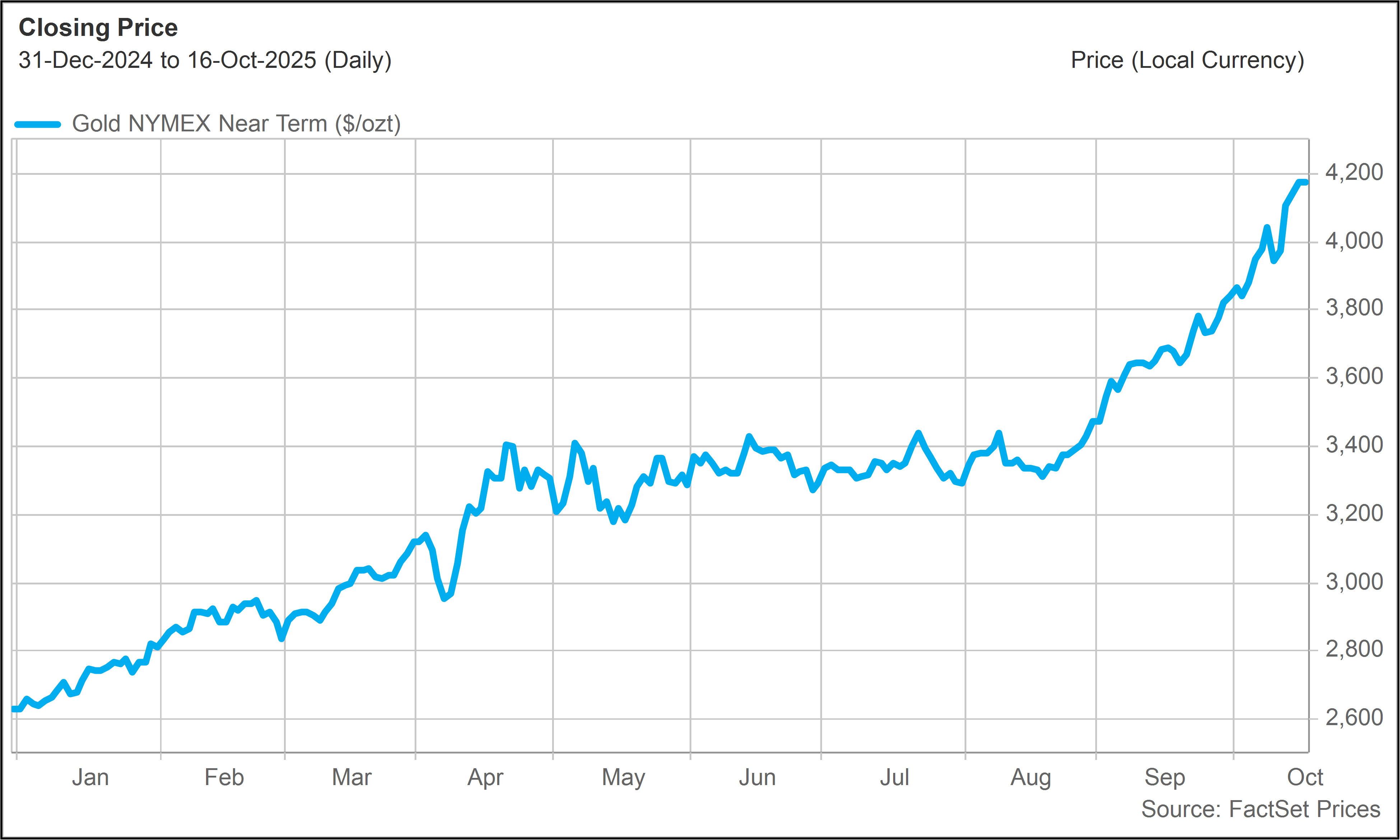

There are hundreds of different Wall Street strategists emailing reports every day, but this note in particular has sparked a great deal of discussion. We suspect it is because the mainstream investment community, along with the financial media, is trying hard to make sense of the extraordinary recent performance of gold.

After a strong start to the year, gold leveled off around $3,400 per ounce, where it then lived for most of the spring and summer. But gold has since skyrocketed through $4,200 per ounce. |

|

|

| Gold price - Year to Date |

|

|

Gold has benefited from a momentum shift which we anticipated in our September 2, 2025 note to subscribers (Pressure on Fed Reignites Demand for Gold).

The main catalyst, as we explained at the time, was Fed Chair Jerome Powell’s pivot toward easier monetary policy to combat a weakening labor market outlook—the key message of his late August speech at Jackson Hole. |

|

| | Low interest rates and easier monetary policy also mean more liquidity in the financial system, i.e. more money that can find its way into hard assets like gold. The prospect of interest rate cuts, as Jerome Powell outlined at Jackson Hole, is music to a gold owner’s ears. - 76report (9/2/2025) |

|

| |

Wall Street’s fiat bias

Wall Street is essentially the fiat money establishment. It manufactures and sells fiat-based financial instruments—equity, credit, and derivatives—which are all ultimately tied to a single, government-sponsored production line at the center of the system: the Federal Reserve.

It is not surprising then that, within Wall Street, there is an institutional bias against monetary alternatives to the U.S. dollar, as well as a lack of understanding of them.

JPMorgan is the largest and most valuable bank in the United States. The firm’s CEO Jamie Dimon, who has in the past compared Bitcoin to a “pet rock,” is now begrudgingly conceding that it is now “one of the few times in my life [when] it’s semi-rational to have some [gold] in your portfolio.”

This is a remarkable and somewhat perplexing statement, coming from someone who could be described as the most powerful figure in the traditional financial world.

Gold has advanced around 60% this year, which is about four times better than the performance of the S&P 500 Index. Over the past 20 years, gold has returned nearly 750%, versus (a still impressive) total return around 450% for the S&P 500. |

|

|

| Gold vs. S&P 500(Total Return - Last 20 Years) |

|

| Looking back over the past 20 years, it seems that it would have been a lot more than “semi-rational” to have had gold exposure.

Gold has not only outperformed stocks, but it has also in many years demonstrated low or negative correlation with stocks. Gold behaving differently from stocks was especially valuable in the post-Global Financial Crisis time frame, when stocks performed quite poorly.

Over the past two decades, gold has provided great long-term returns and has performed well as a hedge when the stock market was weak. From a portfolio perspective, what more could a semi (or even fully) rational investor want? |

|

| | All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident. - Philosopher Arthur Schopenhauer |

|

| | Better late than never

What we find most interesting about the JPMorgan report on the debasement trade is not so much its observations but that the mainstream financial community found them so noteworthy. From the standpoint of investors in gold and Bitcoin, these insights are quite familiar and obvious.

The JP Morgan note connects the debasement trade to a “combination of factors,” ranging from “elevated geopolitical and policy uncertainty, to uncertainty about the longer-term inflation backdrop, to concerns about ‘debt debasement’ due to persistently high government deficits across major economies, to concerns about Fed independence, to waning confidence in fiat currencies in certain emerging markets in particular, and to a broader diversification away from the US dollar.”

In other words, investors are now responding to all of the core macroeconomic themes we have been explaining to subscribers over the past two years, from our April 2024 note on gold (Gold Advances, Justifiably) to our September 2024 note on Bitcoin (Dollar-Proofing Your Portfolio).

How far will the debasement trade go?

Wall Street conventional wisdom is perhaps finally catching up. For those who may already be positioned to benefit from the monetary debasement theme, the key question is how much further can it go and what are the best ways to play it.

These are complicated questions, given that the debasement trade has multiple drivers. Below, we will provide our updated thinking on the key asset classes connected to the debasement trade: gold, crypto and stocks. |

|

| | GOLD

When discussing monetary debasement, there is a tendency to think about the price of gold as having a direct relationship to the supply of paper money. This is a good framework to start with… but potentially limiting.

To the extent the supply of paper money, either U.S. dollars or all global fiat money, grows at a rate that exceeds the supply growth rate of gold (typically 1% to 2% per year), it makes sense to expect the value of gold (in fiat money terms) to keep pace.

As a thought experiment, imagine the U.S. government declared that every dollar will tomorrow be worth two dollars. In that hypothetical scenario, there would instantly be twice as many dollars, and the value of gold should be twice as high in dollar terms (just to stay at the same level in real terms).

So the more the supply of money grows, the more valuable gold should become even if it is just holding its relative value.

But that is only part of the story. The 60% surge in gold this year cannot be explained by money supply growth, which in the U.S. is now running at around 4.5% per year.

What is happening is not merely a response to monetary expansion—it is a response to monetary distrust. The rally in gold reflects a revaluation of confidence rather than a simple adjustment to supply.

Bulging debt-to-GDP ratios, persistent deficit spending, and the politicization of central banking are forcing investors to consider a deeper question: what is the true store of value in an era of perpetual monetary intervention, where every economic hiccup is papered over with an injection of cash into the system?

In this sense, gold’s rise is not just about the quantity of dollars or Euros or yen. It is about the credibility of the institutions printing them and the monetary options available to the governments behind them to keep their economies growing.

The fiscal dominance problem

Fiscal dominance is an economic predicament that develops when a country has taken on so much debt that its central bank has to keep monetary policy exceedingly easy, and interest rates exceedingly low, or the national government will simply not be able to meet its bond payment obligations.

While normally thought of as an emerging market phenomenon, fiscal dominance is becoming a reality in the United States and throughout the developed world.

The U.S. federal government, with some $37 trillion in debt and growing, cannot tolerate high interest rates. It also cannot tolerate a private sector economy that falters and therefore fails to generate adequate tax receipts.

Powell’s late August pivot reflects this dilemma. Monetary policy is too restrictive (i.e., rates are too high). It is suffocating the private sector, leading to higher unemployment, which has the potential to snowball into a recession or worse.

To avoid disaster, the Fed therefore has to continue to supply the economy with high levels of liquidity, even if it may mean structurally higher inflation rates going forward.

Central banks lead the way

Central banks around the world have taken note of the troublesome U.S. fiscal situation. They have also taken note of how the U.S. government and European governments weaponized their banking systems and froze Russian financial instruments as the Ukraine conflict developed.

As a result, central banks, especially in emerging markets, have been accumulating gold at the fastest pace in modern history, while simultaneously reducing exposure to dollar-denominated reserves. |

|

| |

| Gold as % of central bank reserves |

|

|

Private investors have been responding to the same signals. Gold-backed Exchange Traded Funds (ETFs) are seeing large inflows after several years of flat or negative fund flows. September 2025 represented a monthly record at $26 billion.

As a supply-constrained asset, the price of gold could continue to rise considerably to the extent this high demand persists. Even though gold has performed extremely well, we continue to think investors should maintain allocations to gold, considering the diversity and durability of its demand drivers.

We would be more concerned about a potential retracement if this gold rally were just driven by speculative retail buying.

Retail demand is part of this move, but it appears primarily driven by increased institutional allocation and long-term strategic accumulation by central banks around the world.

Emerging market central banks like those of China and India have much lower gold holdings than their western counterparts and would likely respond to any price weakness with more aggressive buying. |

|

| |

CRYPTO

Crypto assets like Bitcoin may one day make their way into central bank reserves in a serious way, and there are some very early indications of progress. For now, the success of the crypto asset class is a mostly private market phenomenon.

Bitcoin, like gold, is a non-sovereign monetary alternative that cannot be debased by governments. Individuals and private institutions are buying Bitcoin because it is essentially digital gold, a form of money with limited future supply growth.

And like gold, Bitcoin stands to benefit, rather than suffer, from the financial mismanagement of governments.

But there is another, more positive, driver of demand for cryptocurrencies, which is less about debasement and more about displacement.

Yes, much of Bitcoin’s appeal stems from the fact that it largely operates outside of political influence, and it represents an alternative to the highly flawed fiat money system. But Bitcoin and crypto adoption is also being driven by purely technological factors.

Just as essentially all forms of computing have migrated to the cloud, the financial system is moving to the blockchain because it is faster, more secure and more efficient.

We are in the early stages of this process, but it is happening quite quickly. It is being spurred on by major legislative and regulatory developments, like the GENIUS Act and the CLARITY Act, which have been championed by the Trump administration.

Crypto assets like Bitcoin, Ethereum, and various other tokens are emerging as the building blocks of a new financial architecture that is purely digital.

Bitcoin represents the monetary foundation of this system. It is the base layer of the digital asset economy with the largest, most decentralized computing network ever created.

Ethereum, on the other hand, is now widely viewed as the most important token within the infrastructure layer—the programmable settlement network upon which the new digital asset economy is being built.

Ethereum enables tokenized assets, stablecoins, and decentralized applications that can integrate directly with machine systems. As AI agents gain autonomy to move money, Ethereum provides the trusted environment in which machines can transact without human intermediaries.

Together, Bitcoin and Ethereum are forming the monetary and computational backbone of the post-fiat world. And AI will likely accelerate demand for both.

In this sense, crypto is not just a hedge against monetary debasement; it is the technological foundation for a new, more efficient monetary system.

The debasement trade remains a key element of the crypto story, but even if governments miraculously got their fiscal houses in order, cryptocurrencies should continue to attract capital.

For investors interested in this theme, we recently highlighted BitMine Immersion Technology (BMNR) as a play on stablecoin growth and tokenization (Is BitMine (BMNR) the Next Crypto Superstar?).

To be clear, this is a highly volatile, speculative stock, but it has the potential to perform extremely well over the long-term. We encourage all investors to familiarize themselves with BMNR—at the very least to understand how blockchain technology has the potential to transform the financial world.

We remain optimistic on Bitcoin. Investors can own Bitcoin directly through crypto exchanges or obtain Bitcoin exposure through a number of low-fee ETFs.

We note as well that Strategy’s 8% Convertible Perpetual Preferred Stock (STRK) has relinquished recent gains with declining sentiment in recent months towards Bitcoin Treasury Companies. The security now offers a greater than 9% dividend yield.

The issuer, Strategy (MSTR), remains immensely overcollateralized in terms of its Bitcoin holdings relative to its debt and preferred stock obligations. In addition to the yield, STRK investors have the potential to benefit from long-term appreciation in MSTR.

We view the recent weakness in STRK as sentiment-driven, not fundamental. For more details on STRK, refer to High Yield with Bitcoin Upside. |

|

| | STOCKS

As alternative forms of money, gold and crypto are naturally the first assets one might consider as monetary debasement plays. But stocks can be as well.

A share of stock is an ownership interest in a business. A business is a toll collector on economic activity. The value of a share of stock is ultimately based on the value of the tolls the underlying business collects.

The more fiat money circulating within the economy, the more tolls can be collected. This will tend to get reflected in higher share prices as corporate profits rise, at least in nominal terms.

Stocks are also often leveraged. If a business has debt, monetary debasement makes the money it owes to creditors less valuable in real terms.

Stocks are often misunderstood as fiat money instruments, like bonds, but they are really not. Unlike bonds, which promise fixed nominal payments in a depreciating currency, stocks represent claims on productive assets. Companies can raise prices and thereby capture the inflationary flow of new money.

Across our Model Portfolio strategies, we are looking for scarcity—assets, business models, and technologies where supply cannot easily expand and where competitors cannot easily take share.

Scarcity is the common denominator that links gold, Bitcoin, and productive equity ownership. Whether it is in the form of finite digital code, a physical resource constraint, or irreplaceable intellectual capital, scarcity is what preserves purchasing power in the context of open-ended money creation.

One could reasonably argue that the strong performance of the stock market is itself a reflection of the debasement trade in action. Investors are realizing that the best way to protect their savings over the long-term is to own a piece of the real economy, rather than parking their capital in financial assets that can be diluted into oblivion.

Pure fiat investments like bank accounts and bonds do offer short-term stability and low volatility, but in the context of the monetary debasement trend, this short-term safety comes with substantial long-term risk. |

|

| | Playing the transition

The global economy is being reshaped by two big forces, monetary inflation and technological acceleration. Investors are adapting accordingly.

Capital is moving out of assets that depend on government credibility and into assets that derive value from scarcity, energy, and innovation.

That means owning hard assets like gold and Bitcoin. It also means owning businesses that can raise prices and control scarce inputs and infrastructure. It also means owning businesses with competitive advantages in AI and blockchain, technologies that will define the economy of the future.

Investments that protect purchasing power and participate in the systems replacing fiat money are the natural winners in this changing landscape. Wall Street may have only just discovered the debasement trade—but it has been unfolding for years, and it shows no signs of slowing down. |

|

| | Click HERE to learn more about our Model Portfolio subscription plans. |

|

|

| | | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

| |

|