In terms of the impact of AI on the economy, we need to consider not just what AI will do but what AI requires to do it. In addition to lots of GPUs and data centers, AI needs an enormous amount of electricity and related infrastructure.

An AI roadmap for investors

We may not know what AI will look like 5, 10 or 25 years from now, but we have a directional sense of the changes ahead.

There will be productivity gains (potentially vast), there could be negative impacts on labor markets (potentially vast), and there will be disparate outcomes across companies and industries.

Below, we highlight four actionable steps investors can take both to protect themselves from potentially negative consequences of AI-related change and to take advantage of upside opportunities.

(1) Save and invest!

Like eating right and exercising, saving and investing is arguably sound advice under any circumstances. This advice is particularly relevant today, if AI is indeed moving the pendulum from labor to capital as explained above.

One way to think about AI is as if an army of highly intelligent, immensely hard workers with minimal compensation expectations arrived on the doorstep of the company that employs you.

Who do you want to be in that scenario? The guy who owns the company or the employee constantly pressuring him for a raise, more time off, and better health care benefits?

AI is a boon to business owners, who can replace workers with technology. The good news is, anyone can become a business owner by investing in stocks.

The worst case scenario for workers—AI leads to massive labor market slack—could be the best case scenario for stocks.

Massive efficiency gains lead to higher profit margins as fewer workers are needed. A larger pool of unemployed workers means there will be less upward pressure on wages.

In this highly disinflationary scenario, the Federal Reserve and central banks around the world will likely pursue monetary policies that are highly accommodative in order to promote employment and support consumers.

In other words, they will print money.

Owners of stocks have the opportunity to win twice in a sense—earnings grow (thanks to higher profit margins and monetary easing) and the earnings become more valuable as the cost of capital plunges.

Historically, one might have thought of stocks as adding to one’s overall financial risk profile—what if there is a recession that causes a stock market downturn and increases the risk that I lose my job?

AI potentially reverses the relationship. In an AI economy, one’s increased risk of job loss is essentially the reason stocks will perform well.

(2) Figure out the AI winners

Stock pickers who are fundamental investors—meaning they look at company-specific attributes when making buy or sell decisions—typically have a checklist.

People may place emphasis on different variables—growth rates, management quality, balance sheet strength, cash flow—but they typically share the same overall objective. They are all trying to figure out if a given business will become more or less valuable over time.

We are now at the point where AI opportunities and risks need to become one of the first items of consideration. AI has the potential to transform industries and the economy as a whole in ways that other technological trends have not.

As we research and manage our Model Portfolios, evaluating the company’s long-term AI positioning has become the first order of business. Not every stock needs to be NVDA (i.e., a direct AI play), but every company needs to have a strong case for winning in the context of this structural trend.

(3) Figure out the AI losers

Not losing can be as important as winning. Investors should be as focused on downside risk scenarios as they are on upside potential.

Every company will have an AI strategy that they communicate to investors, but some will be more viable than others.

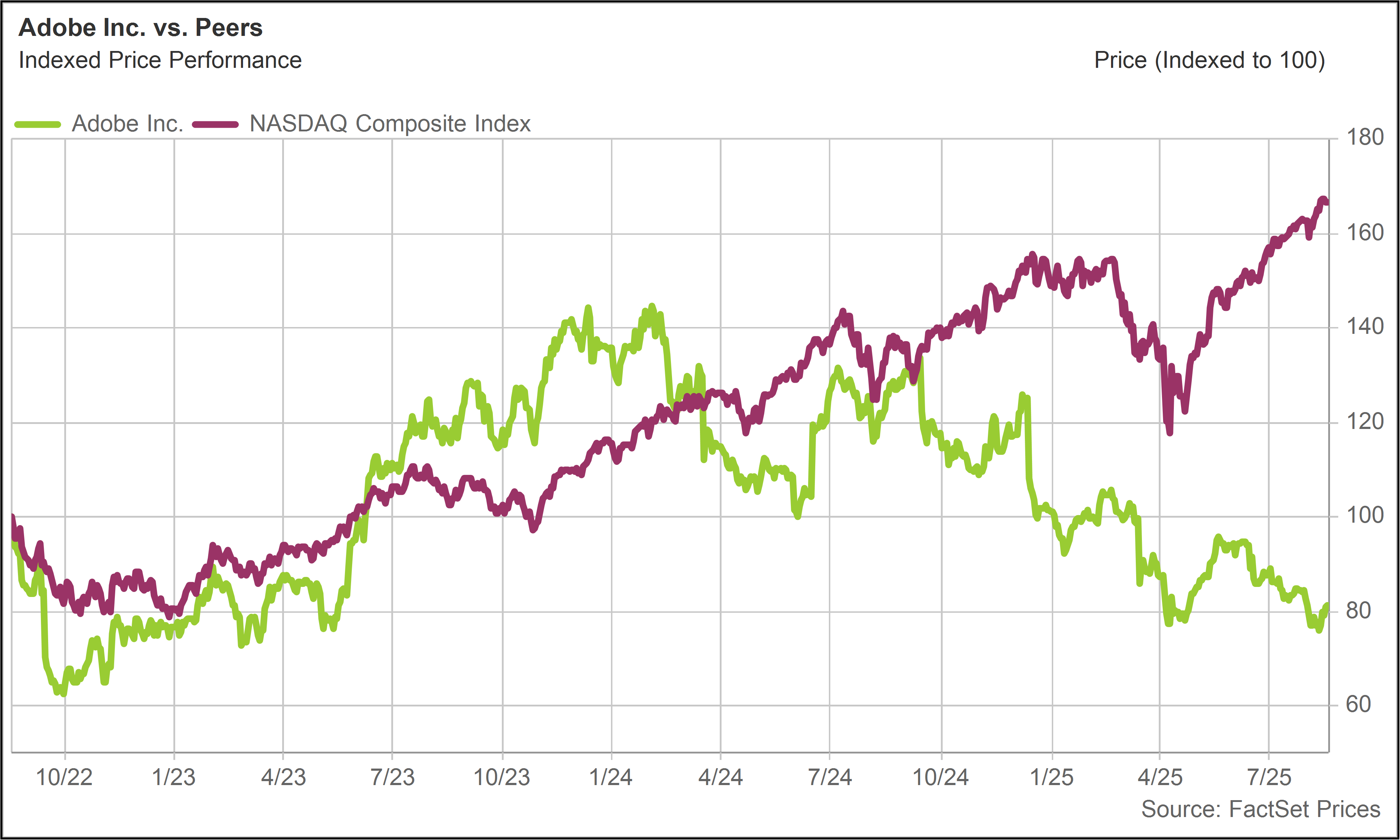

Interestingly, some of the stocks that are most vulnerable to AI disruption will be technology stocks. In recent weeks, several software stocks have traded down on fears that AI models will undermine their value proposition with clients.

Adobe (ADBE) is a good example of how even well-managed, entrenched tech stocks can become an AI casualty.

ADBE has been a leading technology play for many years, with some 60% share of the graphics-intensive “creative software” market. But ADBE has drastically underperformed over the past 12 months.