| American Resilience Model Portfolio |

|

| Monthly Portfolio Review: May 2026Publication date: June 1, 2026 |

|

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

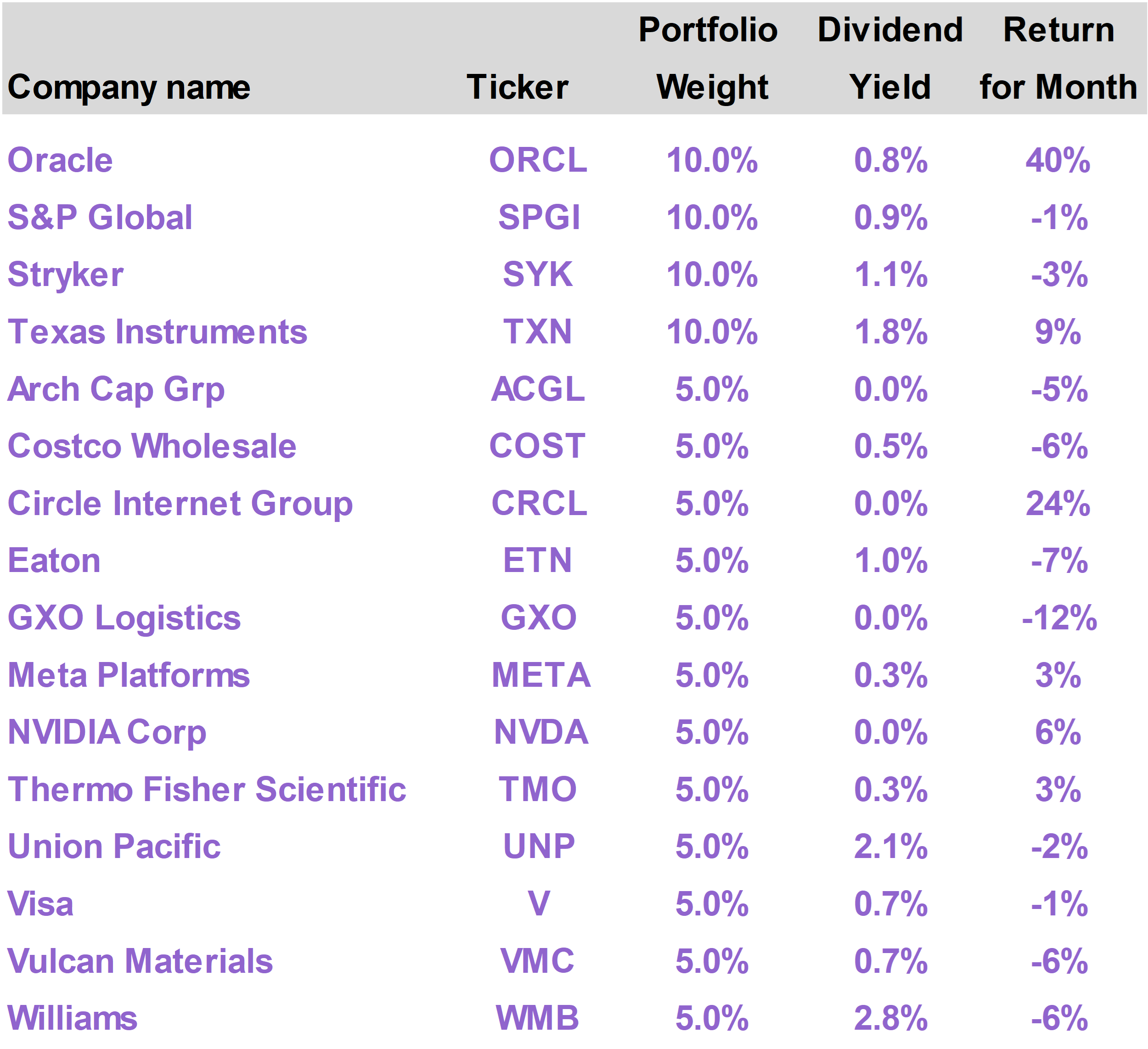

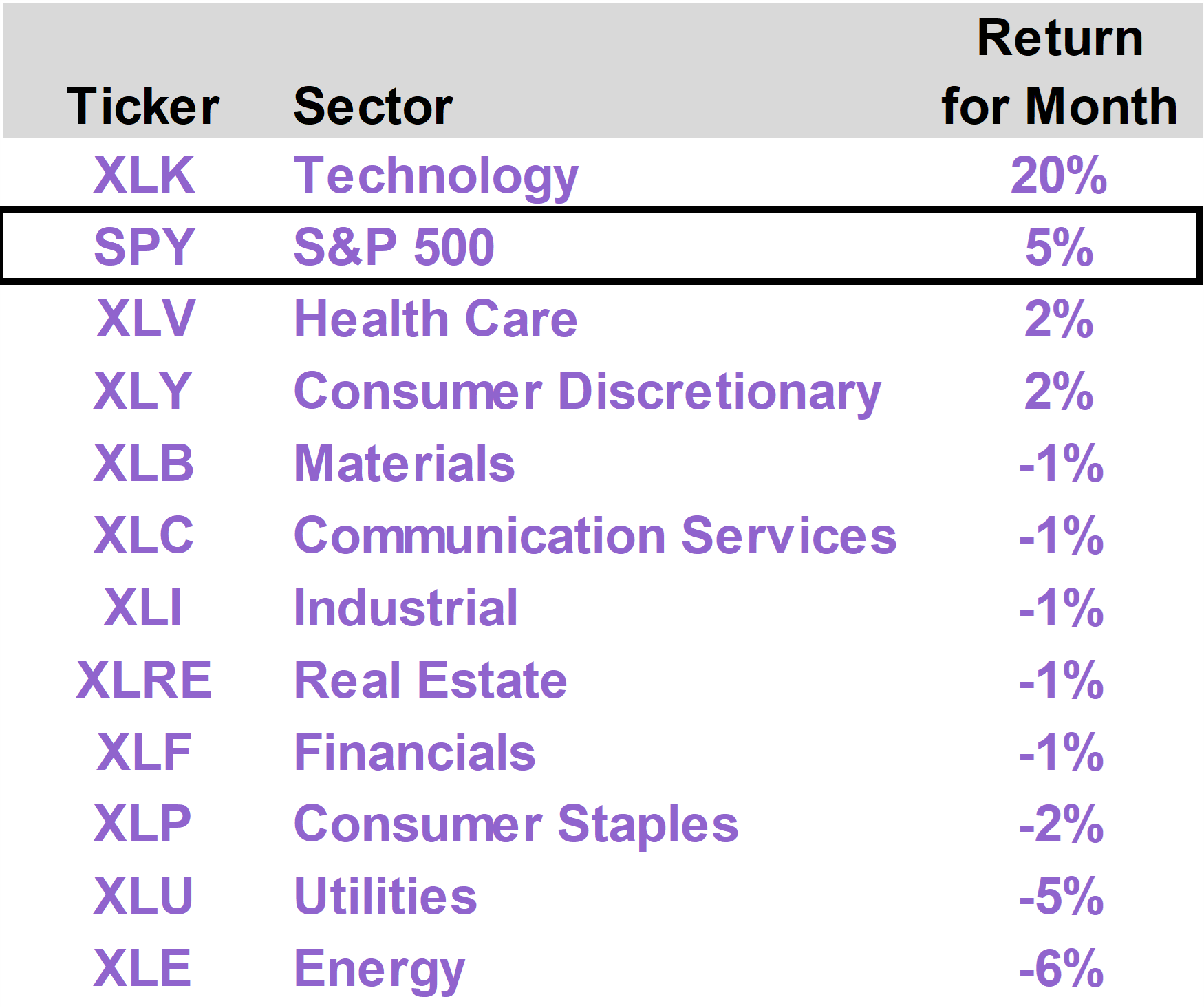

| | | Tech earnings drove stock indexes higher in May, as AI spending continues to exceed expectations. The S&P 500 advanced 5.3%, with the Technology sector returning 20%. Yet most industry sectors were down, pressured in part by inflation concerns and rising long-term interest rates. Crude oil prices were volatile but by the end of the month retreated to their lowest level since March, signaling meaningful progress towards an end to the Iran conflict. The American Resilience portfolio advanced 4.0% in May and has returned 13.9% on a year to date basis, versus 11.3% for the S&P 500. Performance was led by Oracle (ORCL), which surged 40%, reflecting renewed investor confidence in its AI infrastructure strategy. While AI remains the key growth driver, we see the normalization of energy prices as offering potential relief on the inflation front over the remainder of the year, benefiting the market more broadly.

|

|

| | | The American Resilience portfolio generated a total return of 4.0% in May, versus the S&P 500 Index return of 5.3%. On a year to date basis through the end of the month, the portfolio has returned 13.9%, outpacing the 11.3% return of the S&P 500.

The top performing portfolio positions in May were Oracle (ORCL), which returned 40%; Circle Internet Group (CRCL), which returned 24%; and Texas Instruments (TXN), which returned 9%.

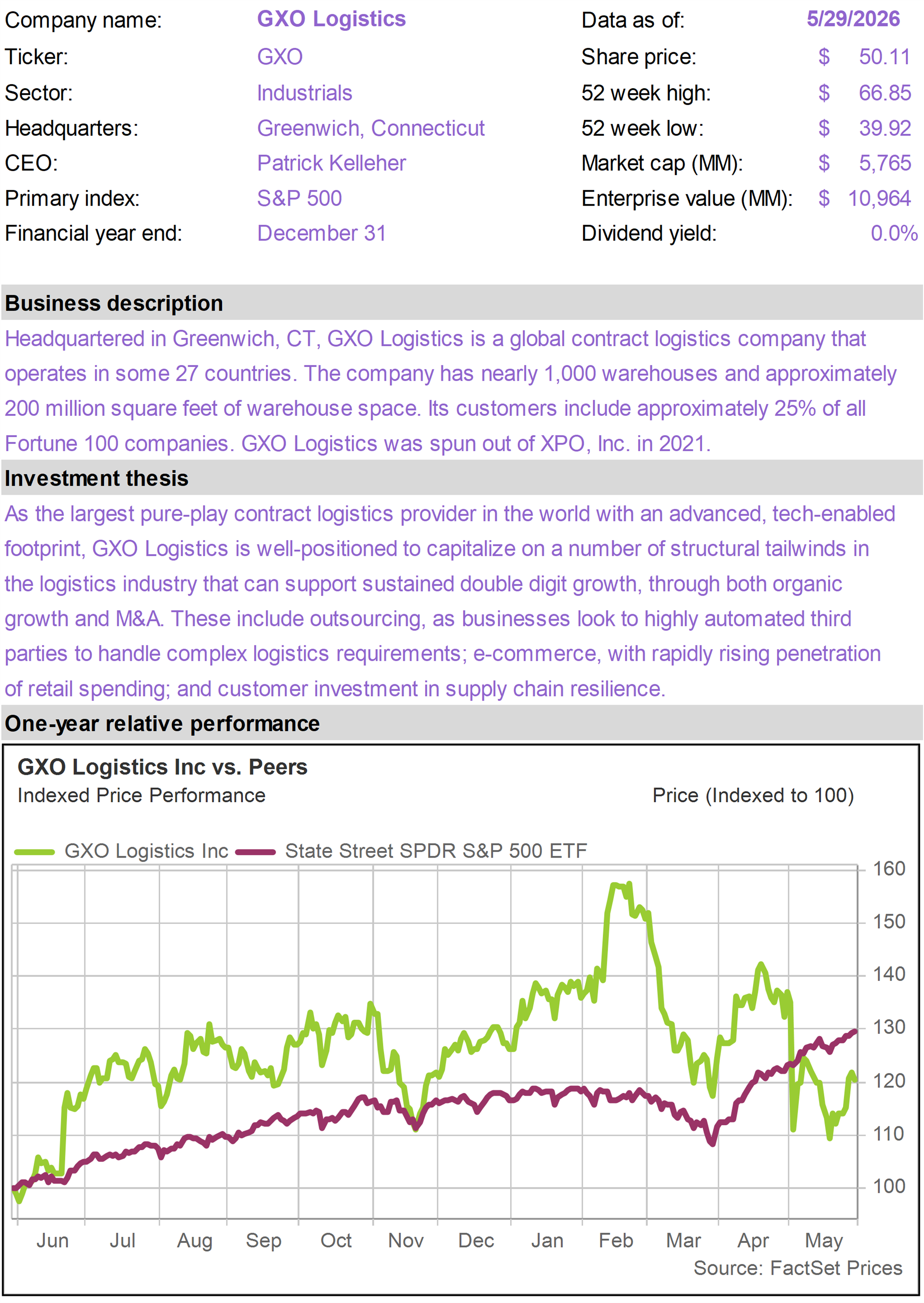

The worst performing positions were GXO Logistics (GXO), which returned -12%; Eaton (ETN), which returned -7%; and Williams (WMB), which returned -6%. |

|

| Tech dominates again

Investors in Technology stocks were once again the big winners in May. For the second straight month, the Tech holdings of the S&P 500 Index generated a 20% total return.

Tech, which now represents just under 39% of the entire index, effectively accounted for more than 100% of the total gain of the index this month.

All other sectors generated either marginally positive or negative performance. In fact, despite the strong overall performance of the index, most industry sectors (8 out of 11) actually delivered a negative result. |

|

|

| Tech performance was extremely strong, but it was driven by a small group of stocks. Notably, among large-cap tech stocks with greater than 0.5% representation in the S&P 500, Micron (MU) returned of 88%, Advanced Micro Devices (AMD) returned 46%, and Oracle (ORCL) returned 40%.

All three companies benefited from growing investor confidence in AI-related demand, especially in certain areas that may have been previously underestimated.

MU broke one trillion dollars in market cap as demand for High-Bandwidth Memory (HBM)—a critical component used alongside AI chips—continued to outpace expectations.

AMD surged after investors became increasingly optimistic that the company could capture a larger share of the rapidly expanding AI accelerator market.

ORCL surged on growing enthusiasm for its cloud infrastructure business, reversing doubts that have surfaced in recent months over the pace of its AI data center investments.

There were a number of other, somewhat smaller tech names that also performed extremely well as a result of surprisingly strong AI-related demand.

Dell Technologies (DELL), for example, gained sharply after reporting blowout results that highlighted accelerating demand for its AI-optimized servers. DELL was the single best performer in the index, returning 101% in May.

These companies illustrate how the AI boom is expanding beyond the most obvious beneficiaries and driving up earnings expectations for companies that occupy critical niches of the broader buildout.

In many of these cases, the market was caught off-guard by the sheer strength of demand, from memory and semiconductors to cloud computing and data center capacity.

Iran coming to a close?

Stock market returns in May were largely driven by company-specific earnings surprises, but the broader macro backdrop continued to improve with apparent progress toward a resolution in Iran.

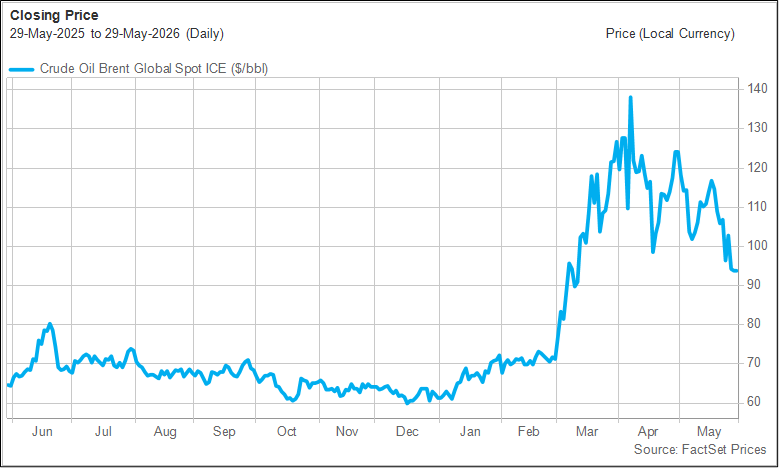

The ultimate barometer of progress in the Middle East is the price of crude oil. As markets sense an improved probability that the Strait of Hormuz will finally reopen and get back to normalized traffic levels, the price of oil drops.

Oil started the month over $120 per barrel and ended just below $95, the lowest level since mid-March. The decline followed a series of developments that suggested the conflict was moving toward de-escalation.

Over the course of the month, fears of a prolonged disruption in the Strait of Hormuz dissipated as reports emerged of backchannel negotiations between the United States and Iran and growing diplomatic efforts by Gulf states to broker a settlement.

As progress toward a ceasefire became increasingly apparent, the geopolitical risk premium embedded in oil prices began to fade. By the end of the month, investors were increasingly pricing in a diplomatic resolution, helping drive crude oil below $95 per barrel. |

|

|

| Brent Crude Oil($/barrel - Last 12 Months) |

|

|

Energy stocks were the worst performing sector in May, declining 6%. The decline reflects lower oil prices and likely some unwind of hedge positions in the sector that investors established over the course of the conflict.

While the normalization of the situation in the Persian Gulf has taken longer than most investors would have liked, we remain optimistic that the Trump administration is committed to bringing the disruption to an end.

Rate volatility

Strong tech earnings ultimately led to a positive result for the stock market as a whole in May, but investor sentiment was negatively affected by bond market volatility.

Long-term bond yields spiked in the middle of the month, feeding concerns that higher interest rates could eventually weigh on economic growth and stock valuations.

The yield on the 30-Year Treasury bond broke through 5% in May, almost getting as high as 5.2% in the middle of the month, levels not seen in years. |

|

|

| 30-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

| The primary catalyst was the sharp rise in oil prices towards the middle of the month as negotiations with Iran appeared to break down. Bond investors were also responding to the April Consumer Price Index (CPI) report, which showed inflation rising to 3.8%, its highest level in roughly three years.

The inflation report primarily reflected the direct impact of the spike in oil prices on gasoline prices and other energy expenses, which accounted for the vast majority of the increase.

As oil prices later receded, Treasury yields stabilized, removing an important headwind for equities.

The sharp decline in oil prices has also had an impact on perceptions on future rate cuts. The higher than expected inflation report fueled speculation that rather than continuing on the rate-cutting path, the Federal Reserve may even have to hike rates.

Following the pattern of the 30-Year, short-term interest rates rose slightly in the middle of the month before retreating.

One-Year Treasury yields still remain about a quarter-point higher than where they were before the war in Iran started.

With the Fed funds rate currently set within the 3.5% to 3.75% band, and One-Year Treasury yields just below 3.8%, the bond market is signaling that there is at least the potential for an additional rate hike in the next 12 months. |

|

|

| One-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

| A positive inflation surprise?

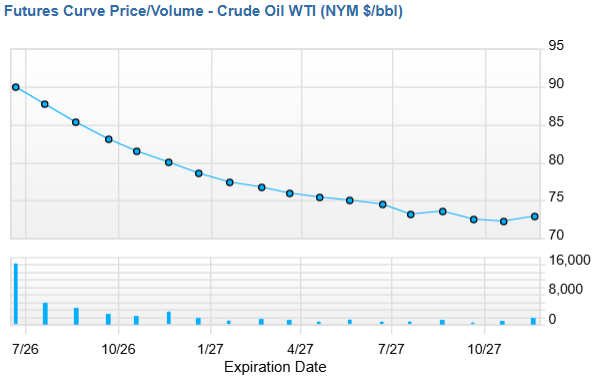

With oil prices still elevated relative to pre-war levels, and heavy spending on AI leading to some supply constraints (for example, in memory), the market remains focused on inflation risk.

While the mood toward inflation is currently cautious, there are reasons to be optimistic.

Futures markets price in significantly lower oil prices going forward, suggesting we are on a path toward lower energy costs. As spot oil prices come down, it is possible that forward pricing could come down even further. |

|

|

| Crude Oil Futures Curve(Source: FactSet) |

|

|

From a more long-term perspective, the energy crisis we have experienced over the past several months is likely to produce a significant supply response.

Higher oil prices will encourage greater oil production and, over a multi-year period, the creation of new pipelines that bypass the Strait of Hormuz.

On the other hand, heavy spending on AI infrastructure is injecting demand into the economy for labor, commodities, and equipment. All of this is ultimately positive and pro-growth but likely contributes to short-term inflationary pressure.

But as Kevin Warsh begins his tenture as Fed Chair, we should not lose sight of one of his most important messages—that AI, as it gets deployed throughout the economy, has enormous potential to deliver increased productivity and thereby serve as a disinflationary force.

While the stock market has performed well on the back of strong earnings growth, rising inflation risk, manifesting as rising long-term interest rates, has been a headwind.

Any sign that inflation risk is receding over the course of the year could allow the new Warsh Fed to get back on the rate-cutting path. This in turn could serve as a meaningful source of support for the market, particularly sectors outside of technology that stand to benefit from relief on interest rates. |

|

| | |

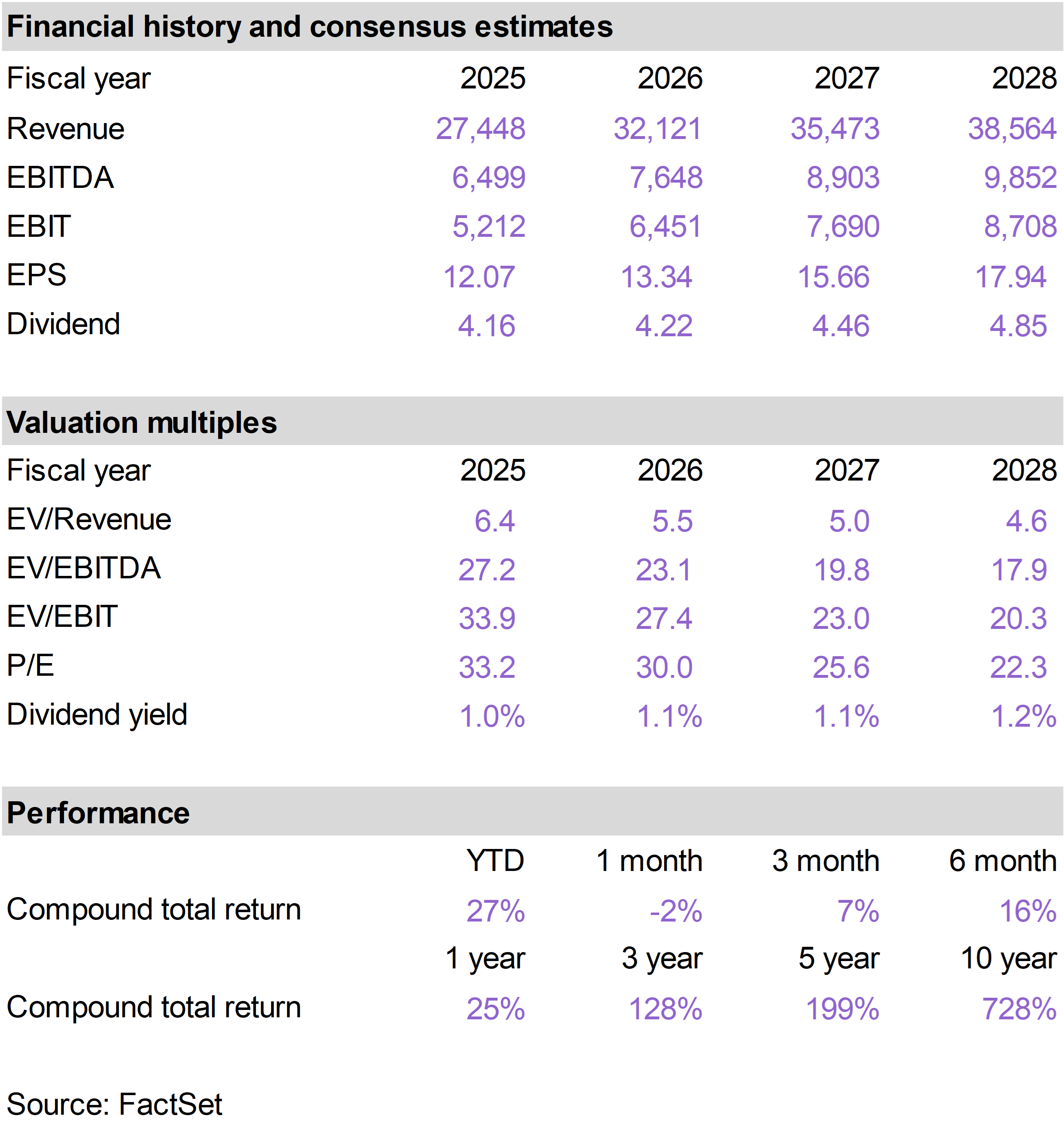

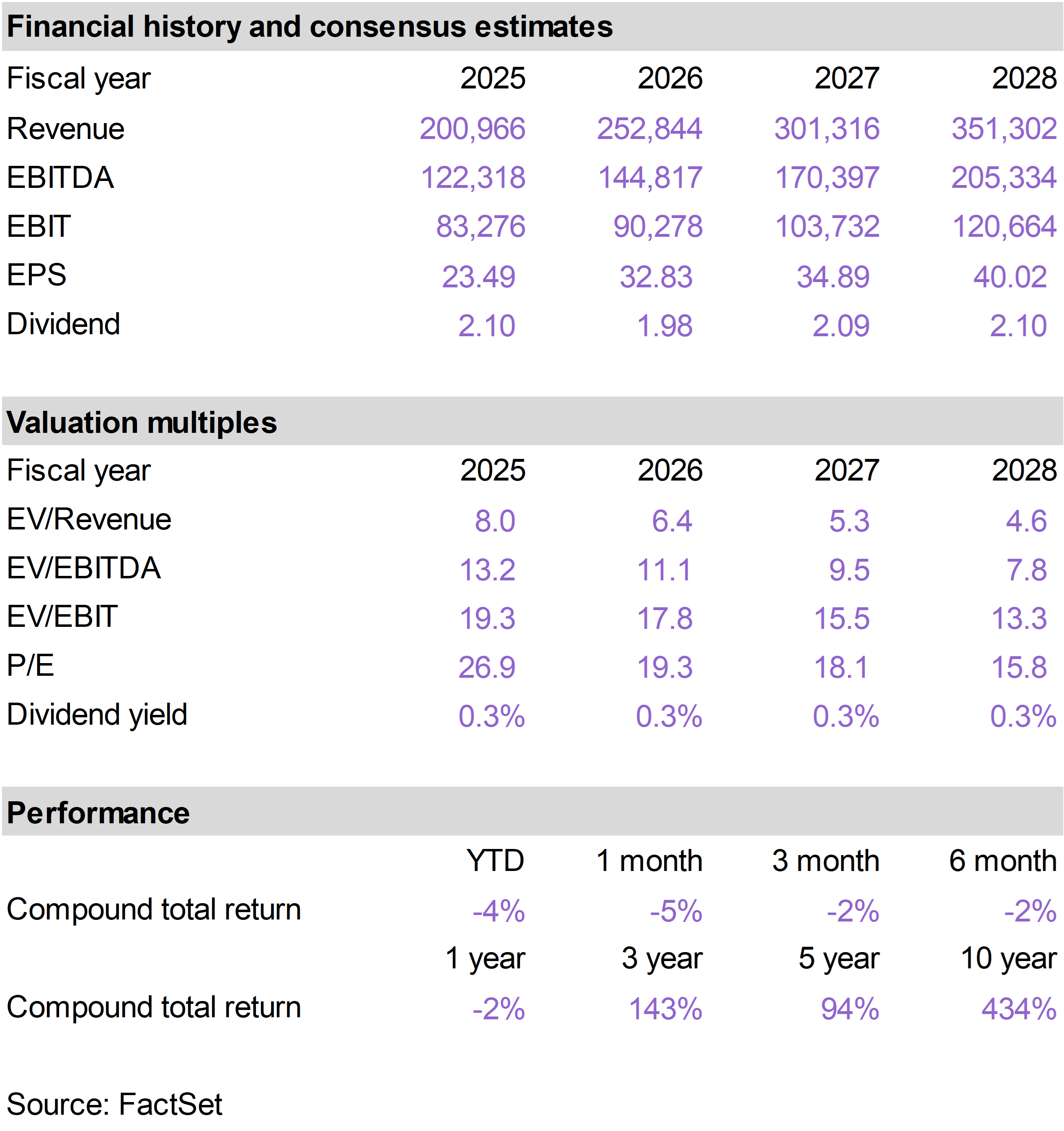

The top performing stocks in the portfolio in May were Oracle (ORCL), which returned 40%; Circle Internet Group (CRCL), which returned 24%; and Texas Instruments (TXN), which returned 9%.

The worst performing positions this month were GXO Logistics (GXO), which returned -12%; Eaton (ETN), which returned -7%; and Williams (WMB), which returned -6%. |

|

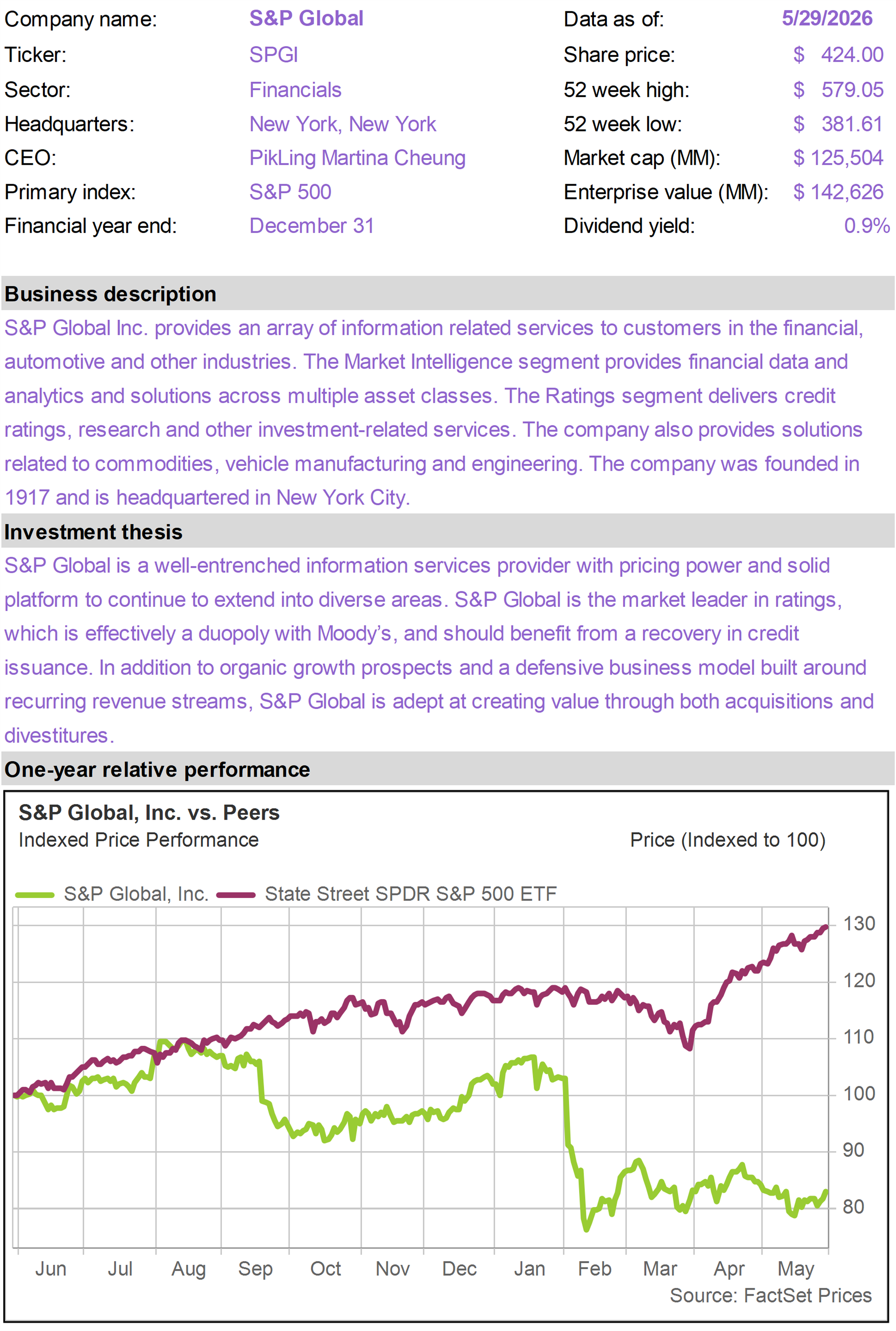

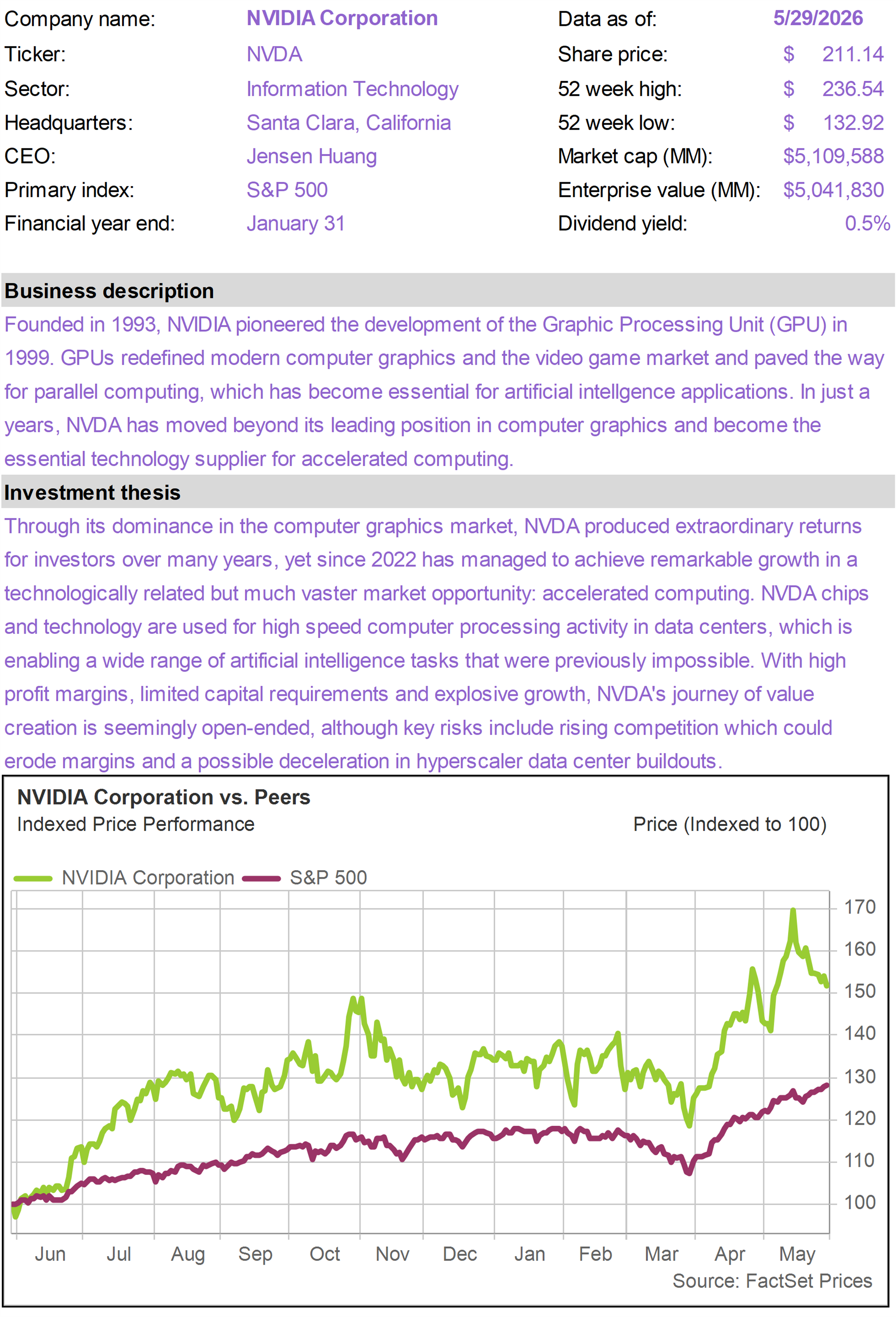

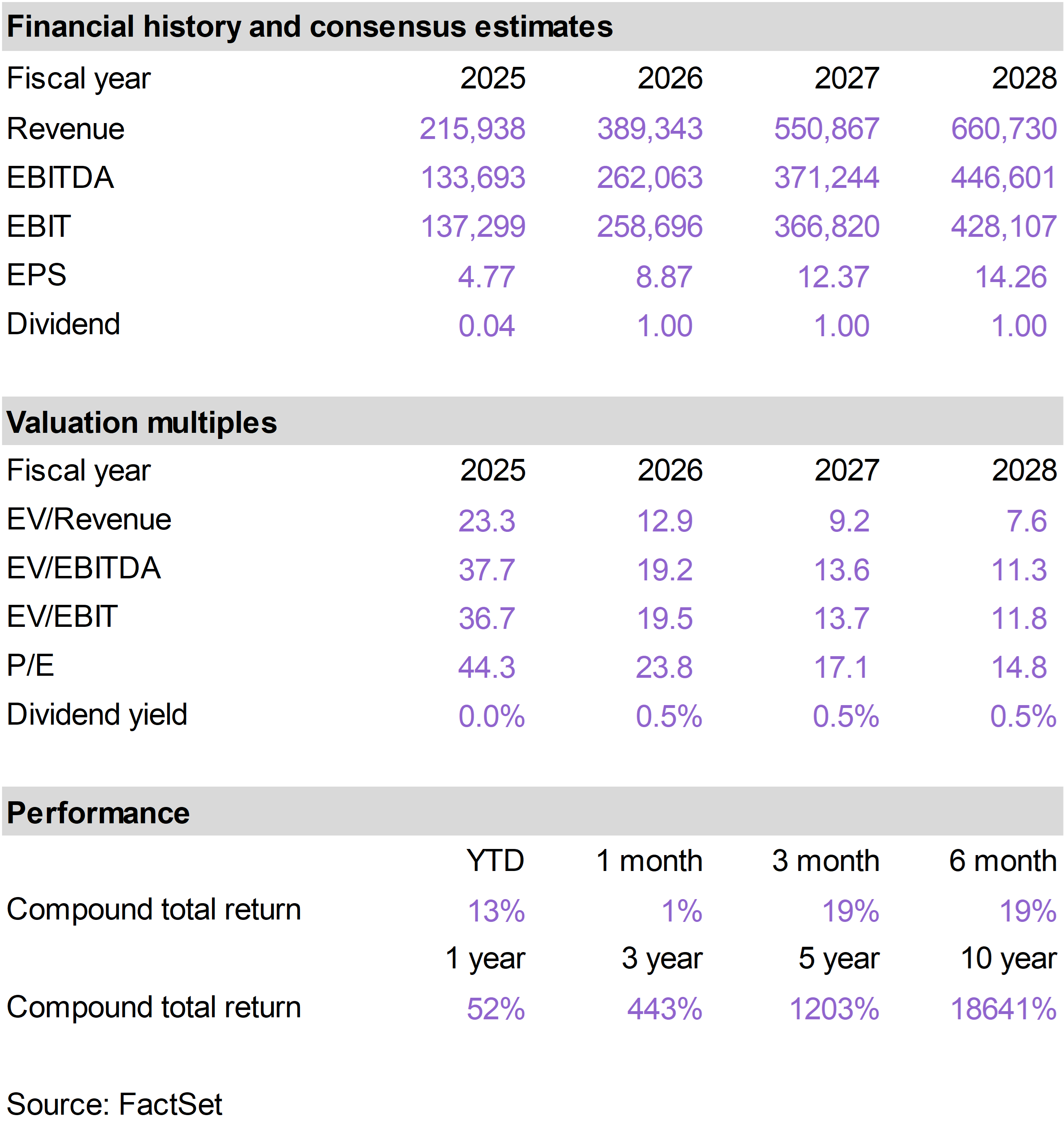

| | As noted above, ORCL was among the top performing stocks in the S&P 500 in May, driven by renewed confidence in its long-term AI strategy.

ORCL has fluctuated significantly over the past 12 months. Shares surged last fall when the company disclosed massive increases in its future revenue commitments from customers. Investor sentiment toward ORCL then saw a sharp reversal, for two primary reasons.

First, investors became concerned about ORCL’s high reliance on OpenAI for all of this expected growth. To some extent, the market started viewing OpenAI’s spending commitments as a potential liability for ORCL rather than a source of growth, given the upfront capital spending required to accommodate OpenAI’s capacity needs.

Second, while the long-term growth of ORCL is based on its AI infrastructure platform, its legacy database business means ORCL is classified as a “software” stock. For example, ORCL is among the top holdings of the iShares Expanded Tech-Software ETF (IGV), which traded off sharply in early 2026 on concerns that enterprise software would be disrupted by AI.

With demand for AI capacity now exceeding expectations, investors appear to be recognizing that these concerns were overblown.

ORCL's AI opportunity extends well beyond a single customer relationship. While OpenAI remains an important partner, ORCL has built one of the world's largest AI infrastructure businesses, supported by a rapidly growing backlog of contracted revenue commitments. The company is spending heavily today because demand already exists, not because management is speculating about future demand.

At the same time, the legacy database business represents a critical advantage as AI demand shifts toward the enterprise segment. Most enterprises want AI systems that can interact securely with their proprietary corporate data. ORCL remains the world's leading provider of enterprise databases.

As companies move from experimenting with AI to deploying it throughout their organizations, ORCL is well positioned to help bridge the gap between AI models and real-world business applications.

The narrative that ORCL’s growth strategy was exceedingly ambitious (and therefore risky) is fading. As demand for AI compute continues to surge, enthusiasm around ORCL as one of the key beneficiaries of the global data center buildout is gradually being restored.

Despite the strong recent performance, ORCL shares remain around 25% below their highs of third quarter 2025. |

|

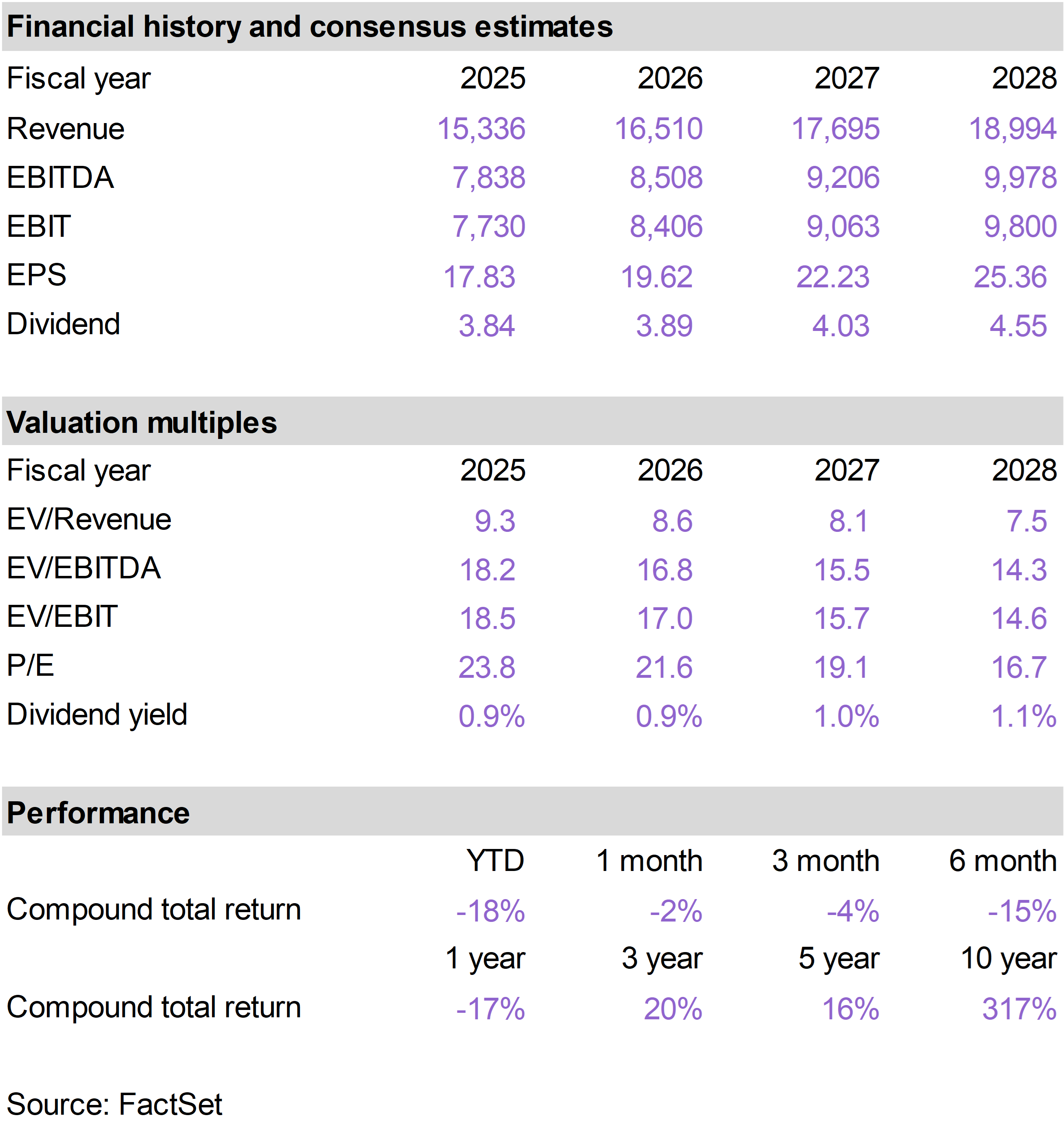

| | Shares of CRCL performed well in May due to a combination of favorable regulatory developments and a strong earnings report.

On the regulatory front, the CLARITY Act moved closer to becoming law after advancing through the Senate Banking Committee with bipartisan support. Investors increasingly view the legislation as a potential turning point for the digital asset industry.

In particular, investors took comfort that the dispute over stablecoin yield will be resolved in an acceptable manner. Under the anticipated compromise, holders of CRCL’s USDC stablecoin will be able to earn rewards that are similar to interest payments on bank savings accounts.

The company's first quarter earnings report also helped boost sentiment. CRCL exceeded earnings expectations and demonstrated that demand for USDC remained resilient despite weakness in broader crypto markets.

Management also highlighted several new growth initiatives. CRCL announced the successful $222 million presale of its ARC token, implying a network valuation of roughly $3 billion, while also highlighting progress on new payment, settlement, and transaction services built on its blockchain platform.

We view CRCL as one of the most innovative and well-positioned players in digital finance, targeting enormous long-term addressable markets. As stablecoins, tokenized assets, blockchain payments, and AI-driven commerce gain adoption, CRCL stands to benefit from multiple growth drivers. |

|

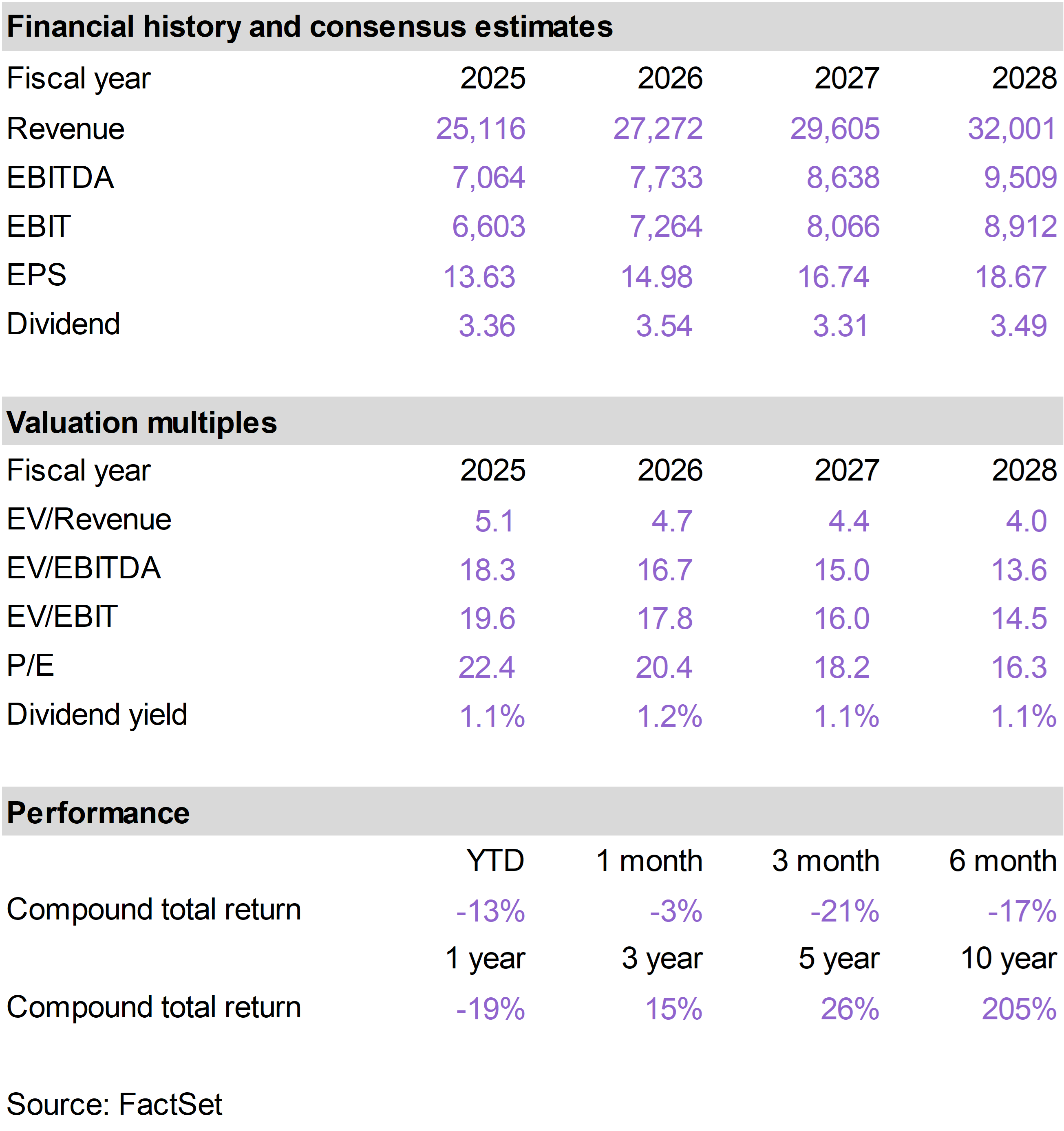

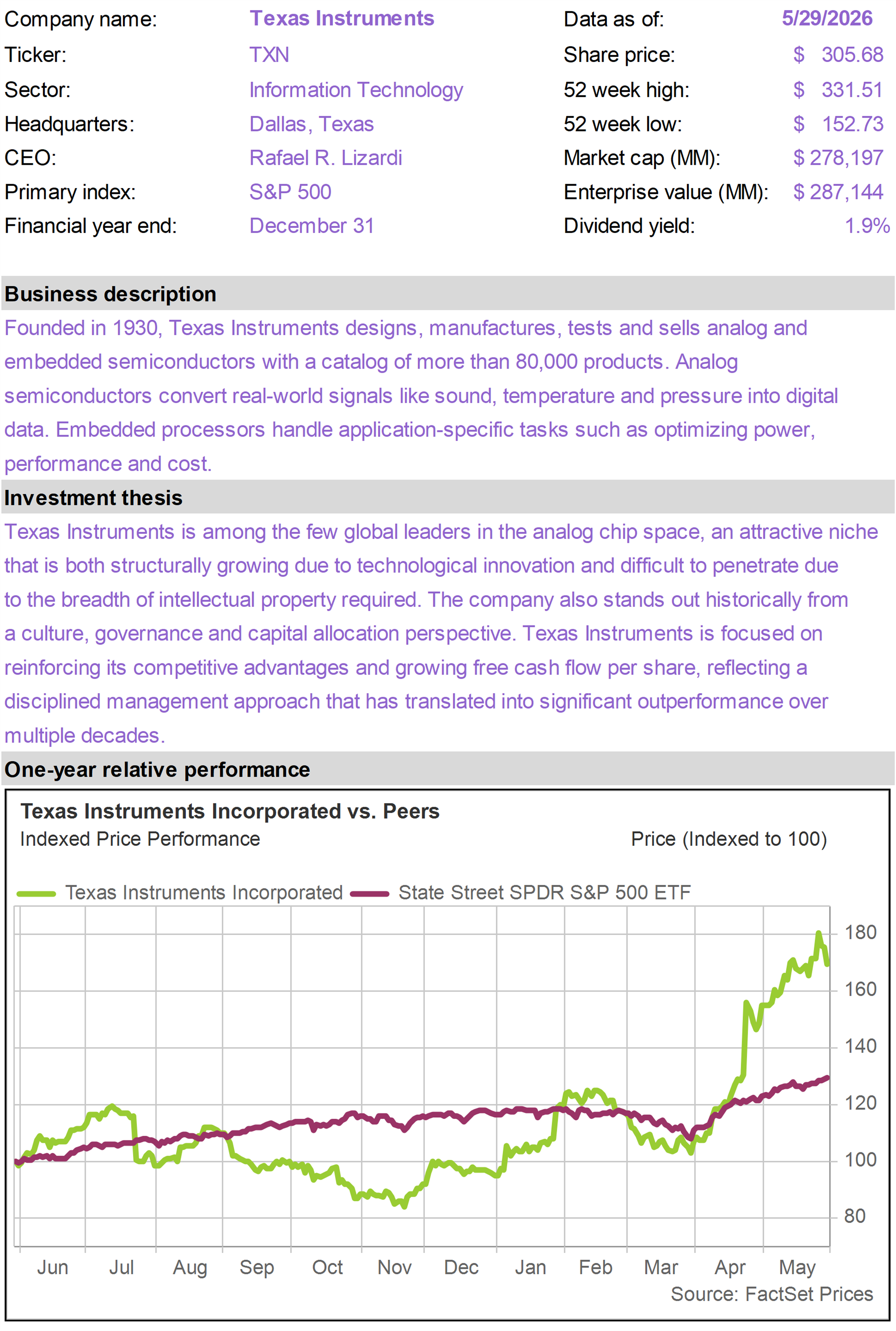

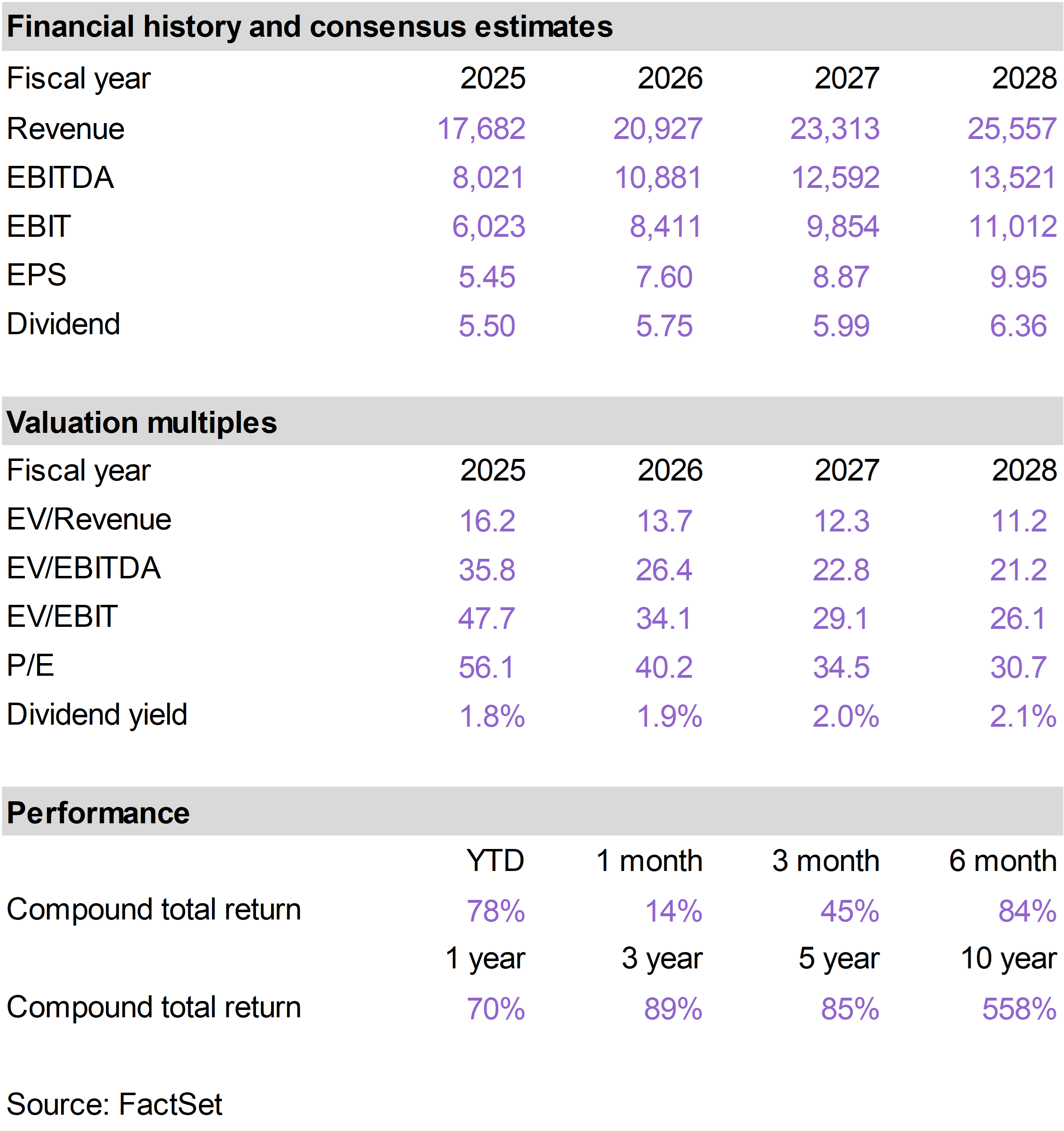

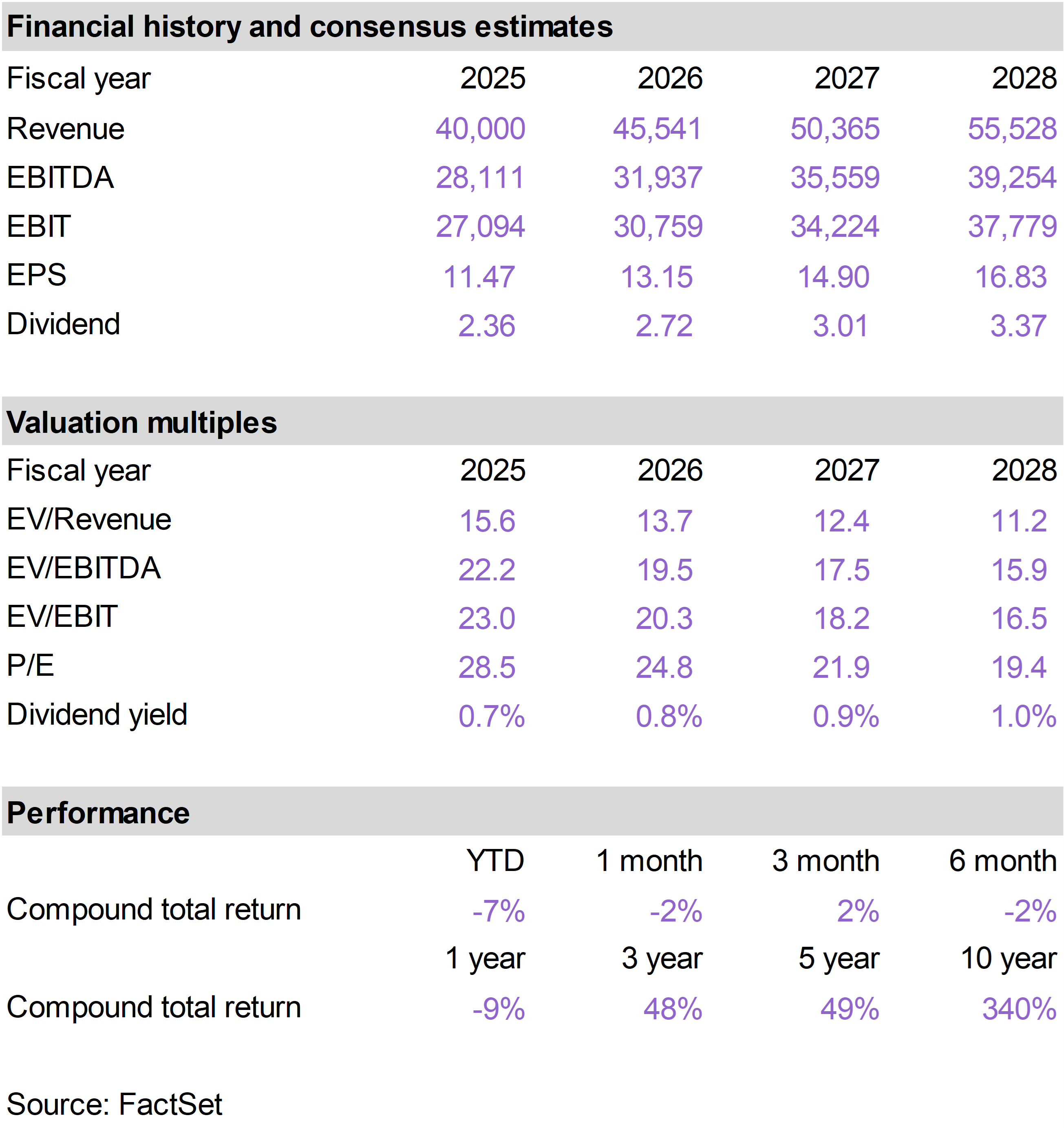

| | TXN continued to advance this month and is enjoying a breakout year, up nearly 80% on a year to date basis through the end of May.

For years, investors viewed TXN primarily as an industrial and automotive semiconductor company. The market is increasingly recognizing the relevance of analog chips (where TXN benefits from an enormous market share and cost leadership position) to the broader AI story, from data centers to physical AI.

Tangible evidence of surging data center demand for TXN chips is perhaps the most notable shift in TXN's growth outlook this year. During the company's most recent quarter, management disclosed that data center revenue increased approximately 90% year-over-year and 25% sequentially, marking the eighth consecutive quarter of growth.

As hyperscalers continue investing hundreds of billions of dollars into AI infrastructure, demand is rising for the analog and power management chips that help regulate electricity, monitor performance, and keep power-hungry AI systems operating efficiently. TXN is one of the leading suppliers of these components.

Perhaps most importantly, the recent surge in demand is validating management's long-term strategy. TXN spent years investing heavily in new manufacturing capacity despite a weak semiconductor cycle, a decision that was unpopular with many investors at the time because it pressured free cash flow.

Today, as industrial markets recover and AI infrastructure spending accelerates, that capacity is becoming a major competitive advantage. What looked like excess spending a few years ago now looks like one of the smartest decisions management has made.

TXN has ample excess capacity in its new semiconductor fabs to meet all of this growing demand. This excess capacity means incremental revenue comes with high profit margins, setting TXN up for record levels of free cash flow in the years ahead. |

|

| |

Despite strong first quarter earnings, GXO underperformed this month on investor concerns about potential competition from Amazon (AMZN), which is targeting the logistics space. We believe those concerns are overstated and continue to appreciate GXO's long-term growth potential.

The concern stems from AMZN's decision to begin offering logistics and supply chain services to third parties. While the announcement initially pressured GXO shares, the reality is that the two companies largely serve different markets.

AMZN's offering is designed around standardized fulfillment services, whereas GXO specializes in highly customized warehouse operations that are deeply integrated into customers' supply chains. Many GXO clients entrust the company with sensitive inventory, manufacturing, and distribution processes that would be difficult—and in some cases undesirable—to hand over to AMZN.

Meanwhile, GXO's underlying business continues to perform well. First quarter revenue increased nearly 11%, adjusted EBITDA grew more than 20%, and the company ended the quarter with a record $2.7 billion sales pipeline. Management also raised its full-year profitability outlook.

AMZN's entry may actually reinforce the long-term investment case for GXO. The contract logistics market remains enormous, with a large percentage of supply chain operations still managed internally. Increased attention from AMZN highlights the attractiveness of the opportunity and could accelerate outsourcing adoption across the industry. |

|

| |

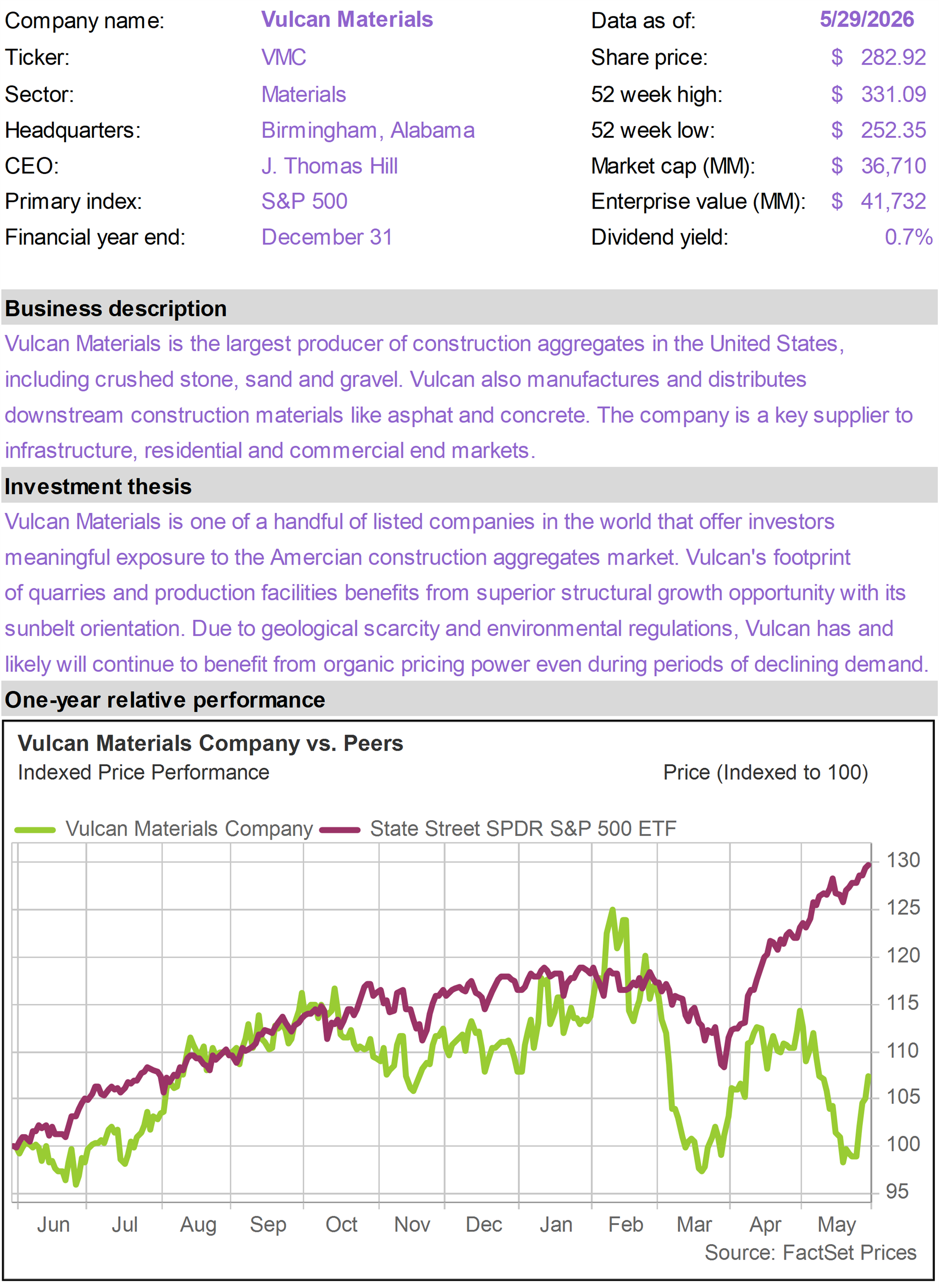

ETN retreated modestly in May, with some pressure on industrial names, but is still outperforming on a year to date basis with a 27% total return.

As we discussed last month, we view ETN as a prime long-term beneficiary of the AI boom and the broader electrification trend, given its specialization in high-demand electrical equipment. |

|

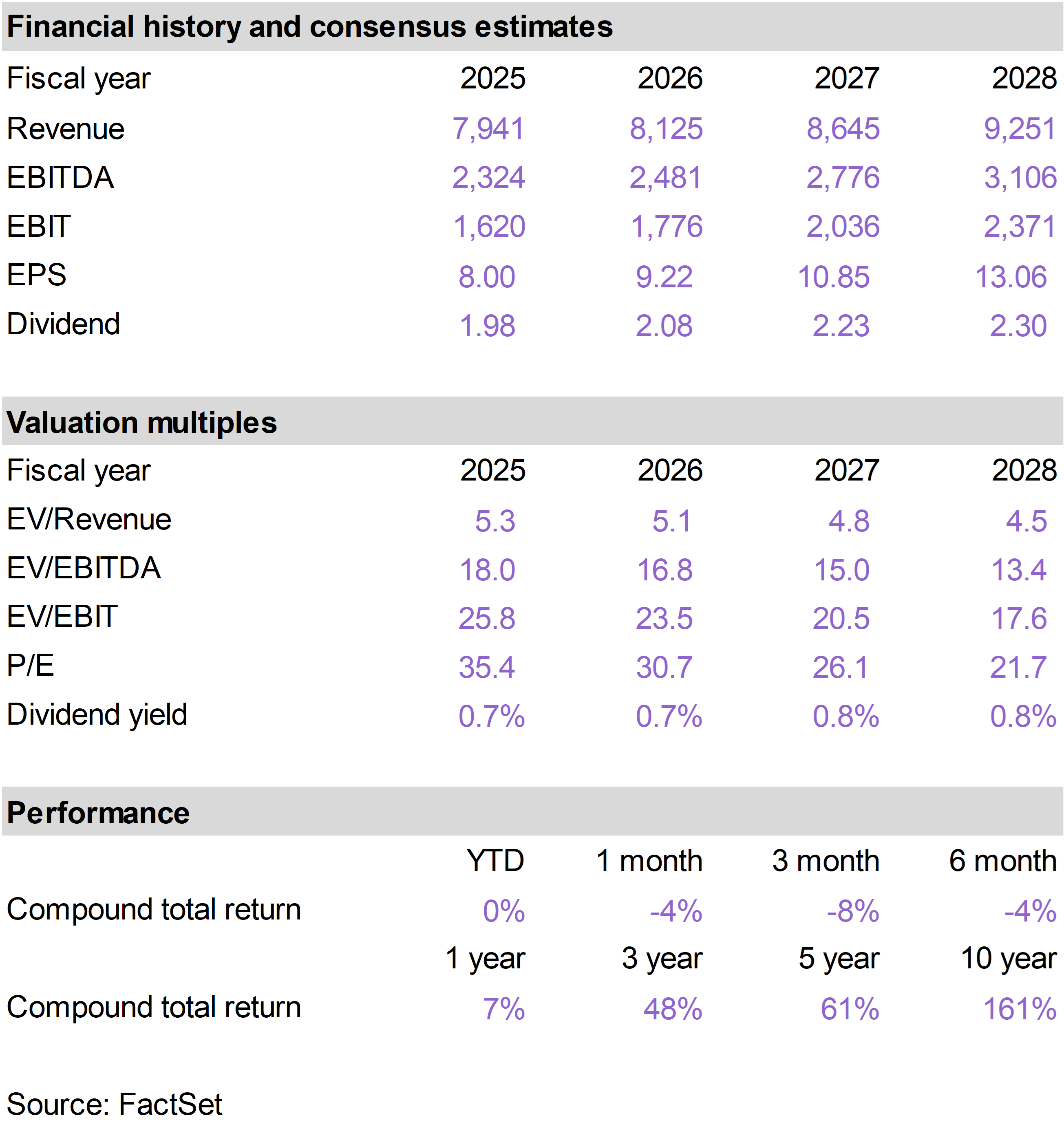

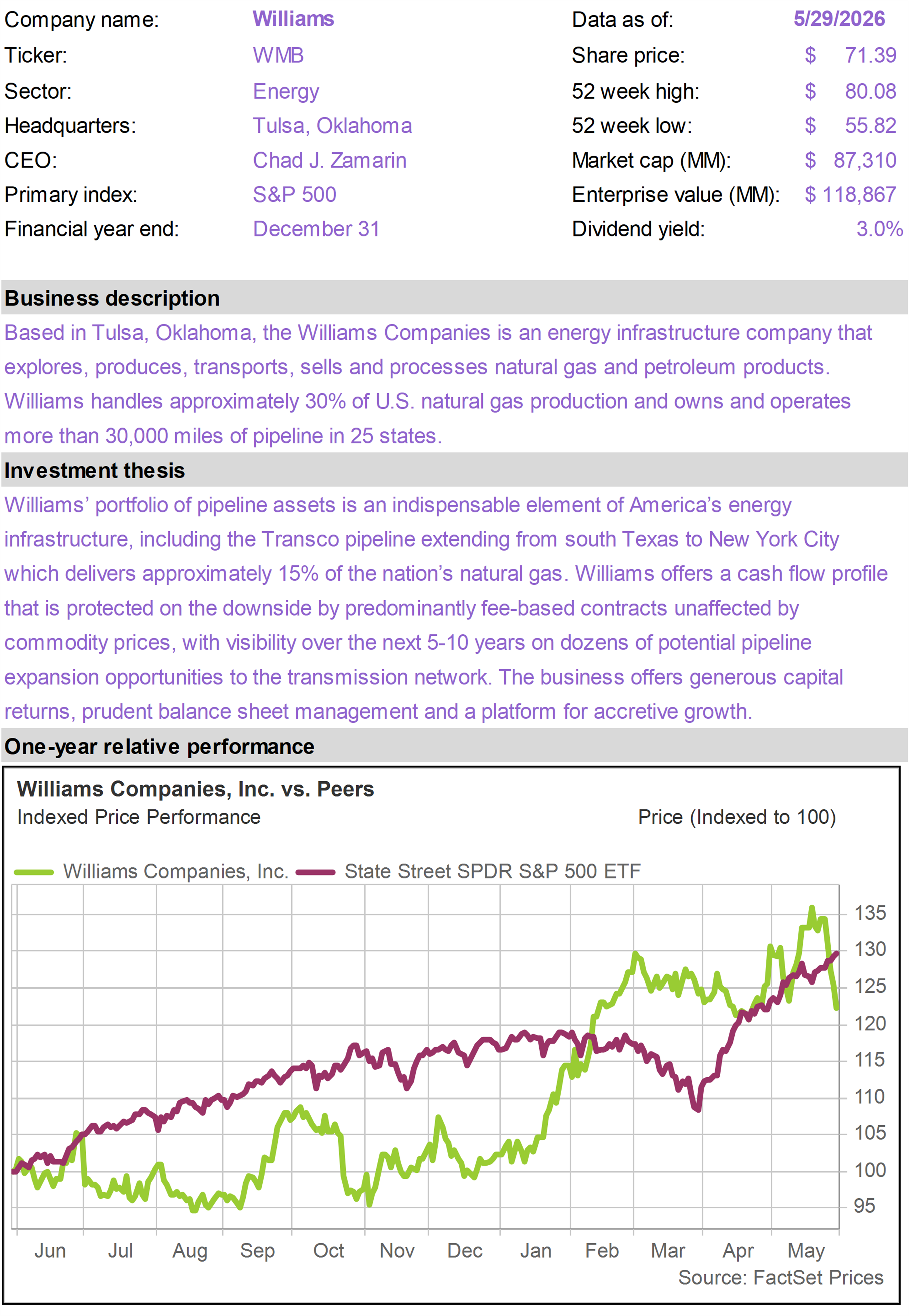

| | WMB shares declined in-line with the energy sector. We would note, however, that as a natural gas pipeline operator, it has minimal direct connection to oil prices.

We continue to view WMB as indispensable infrastructure underpinning America's energy renaissance. As natural gas demand rises from LNG exports, power generation, and AI-driven data center growth, WMB owns many of the critical pipelines needed to move that gas to market.

Importantly, these assets would be extremely difficult to replicate today, giving WMB a durable competitive advantage and positioning the company to benefit from growing electricity demand for years to come. |

|

| | |

| | |

| | |

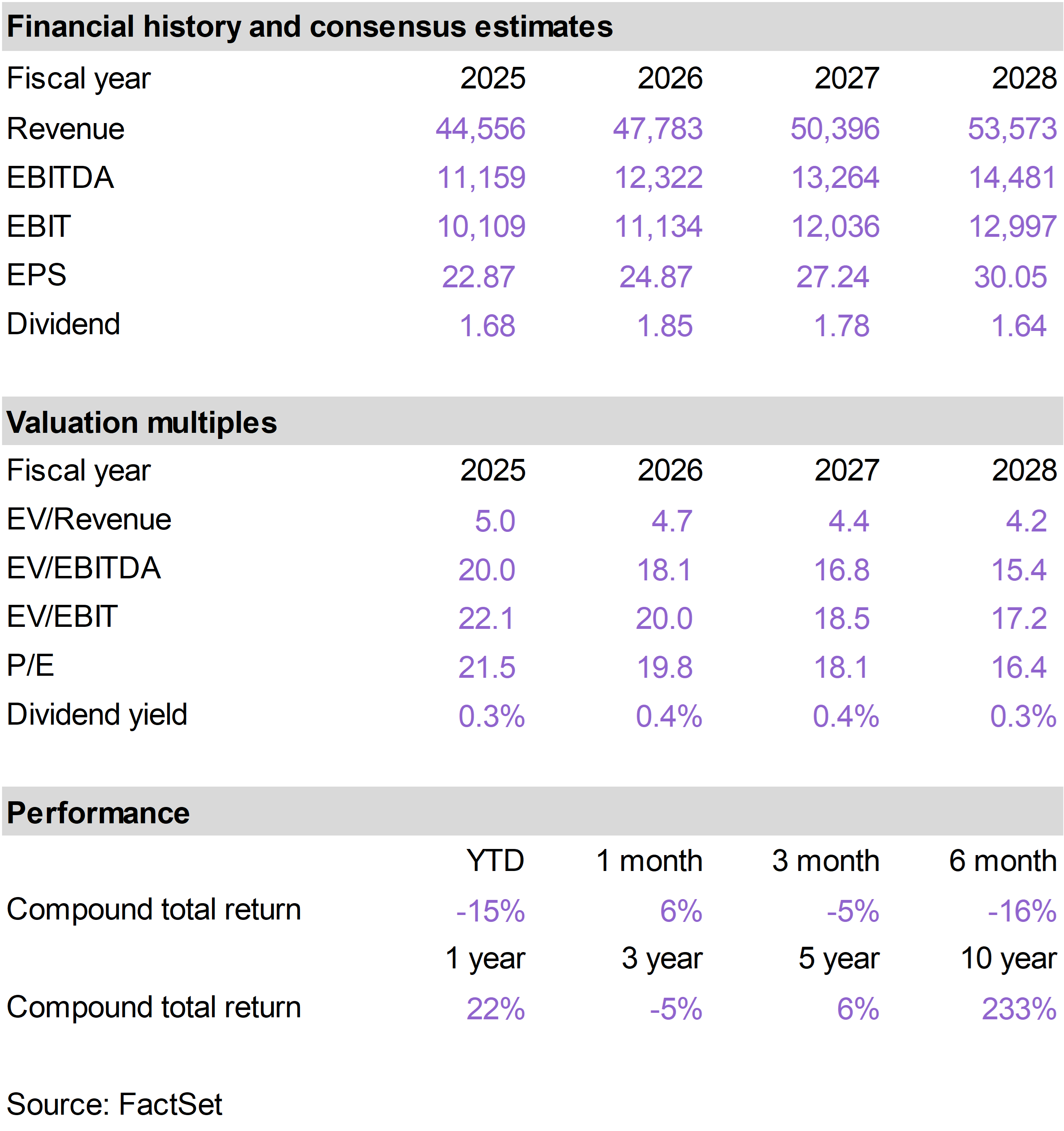

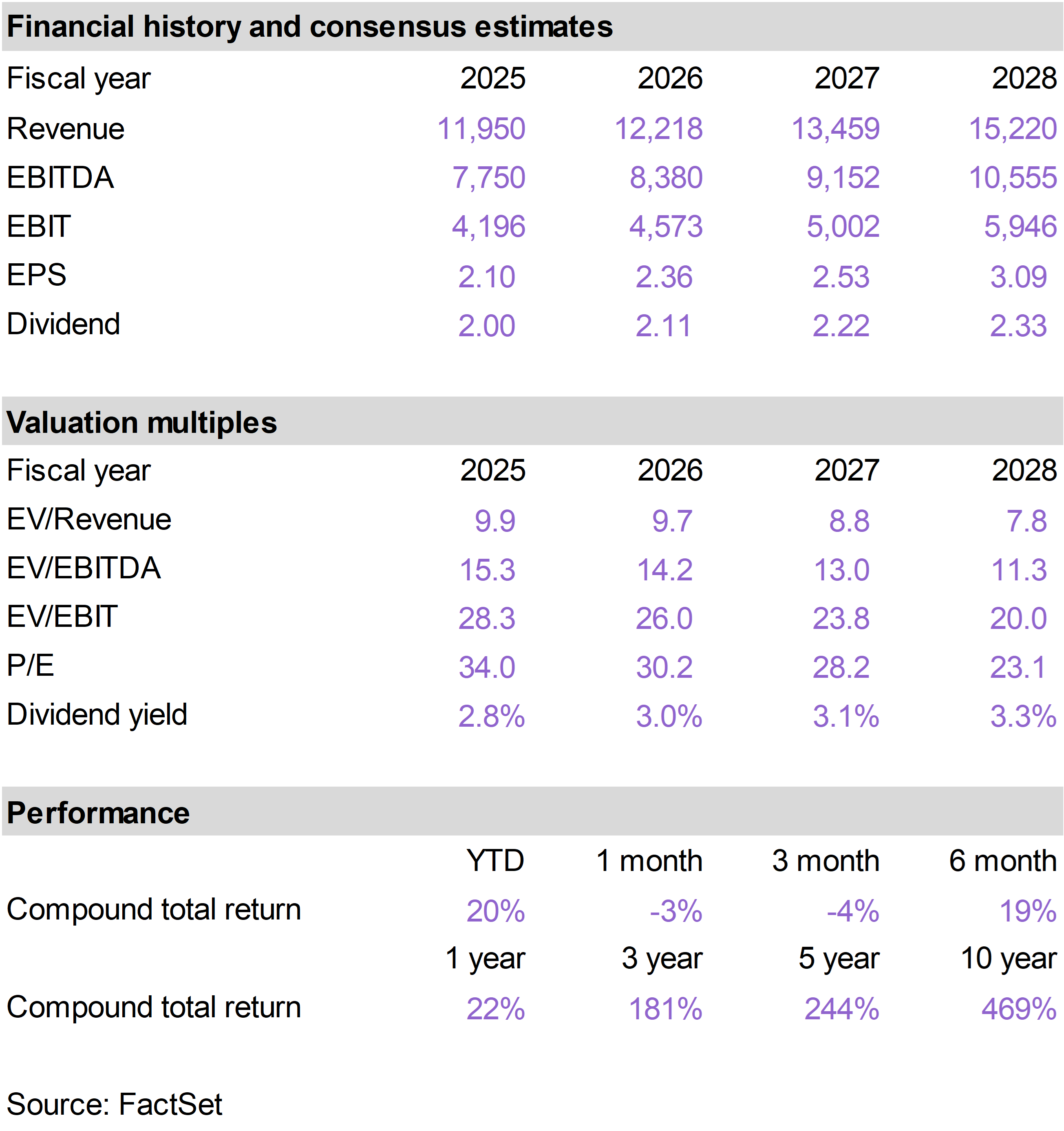

| | | Oracle Corporation (ORCL) |

|

|

|

| | |

|

| | |

|

| | |

|

| | Arch Capital Group (ACGL) |

|

|

|

| | |

|

| | Circle Internet Group (CRCL) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

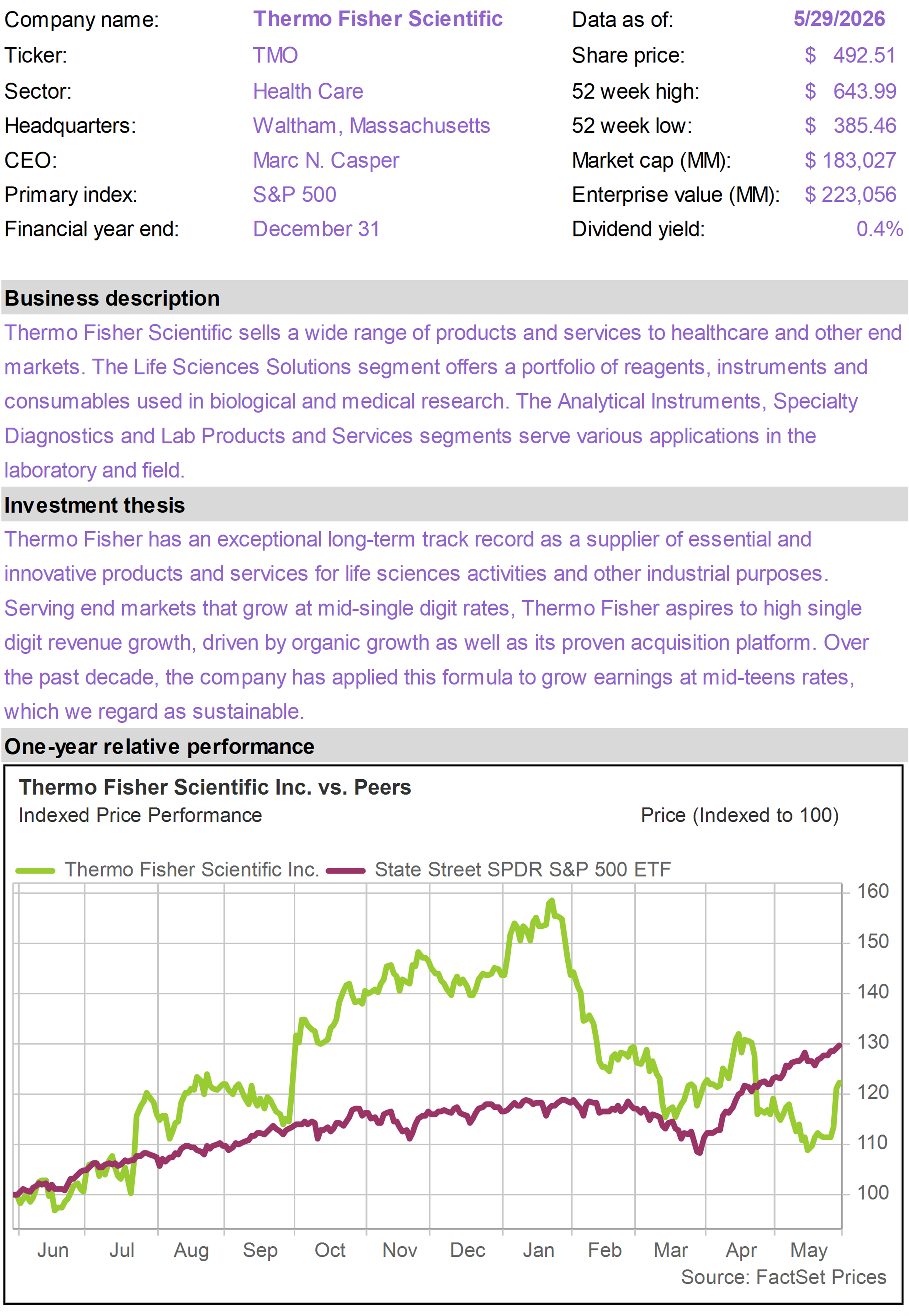

| | Thermo Fisher Scientific (TMO) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

| | The 76research American Resilience Model Portfolio is designed to provide exposure to growth businesses that operate with competitive advantages in structurally attractive markets. The objective is to identify businesses that can survive and thrive across different macroeconomic environments and whatever geopolitical crises may unfold. The holdings are intended as long-term investments to drive portfolio compounding with minimal need to realize taxable gains. Emphasis is placed on critical markers of business quality such as barriers to entry, physical scarcity of assets, balance sheet strength, effective capital allocation and durable long-term growth drivers. These assessments are paired with careful consideration of valuation and risk. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

|