| American Resilience Model Portfolio |

|

| Monthly Portfolio Review: June 2026Publication date: July 6, 2026 |

|

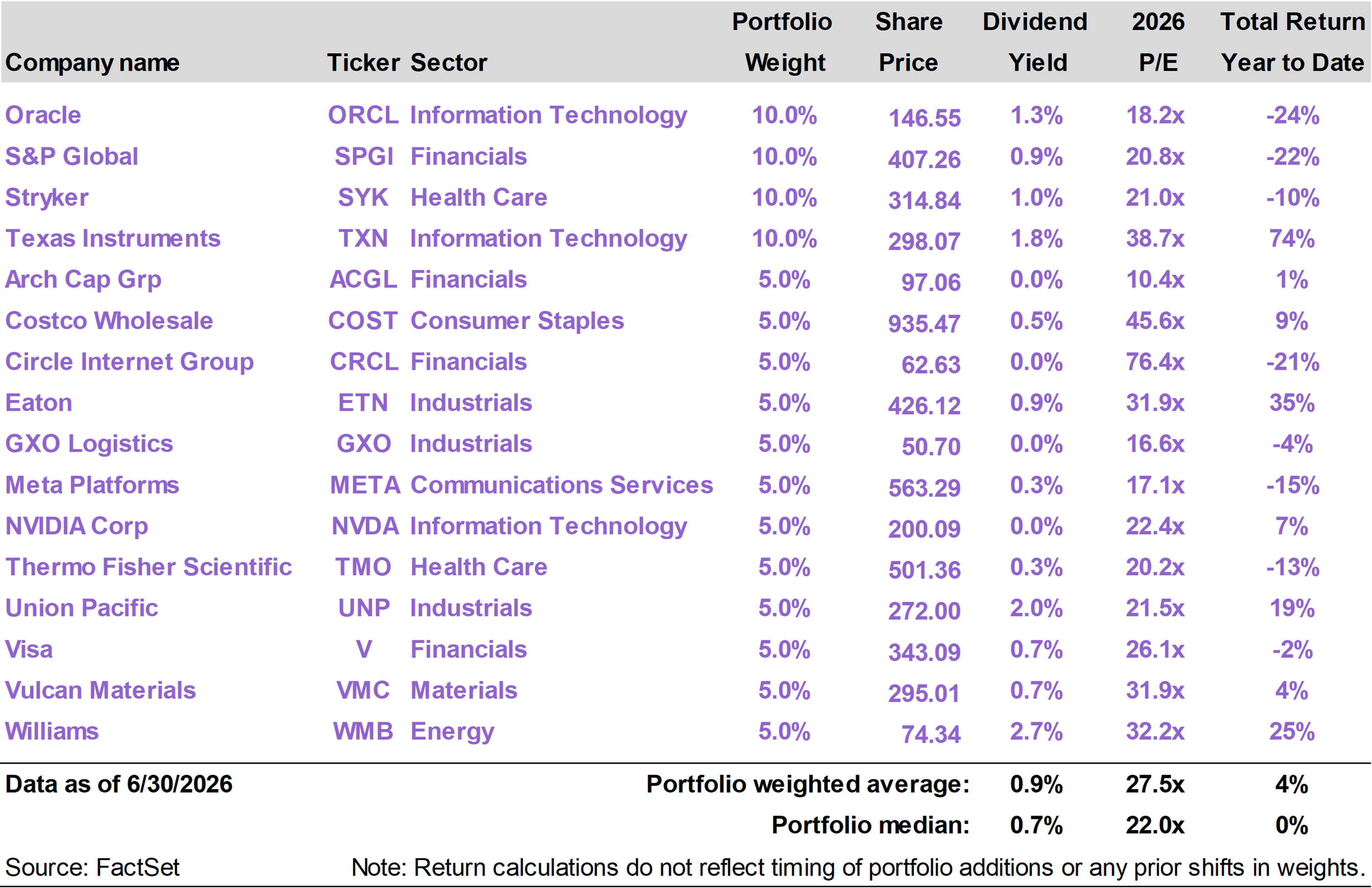

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

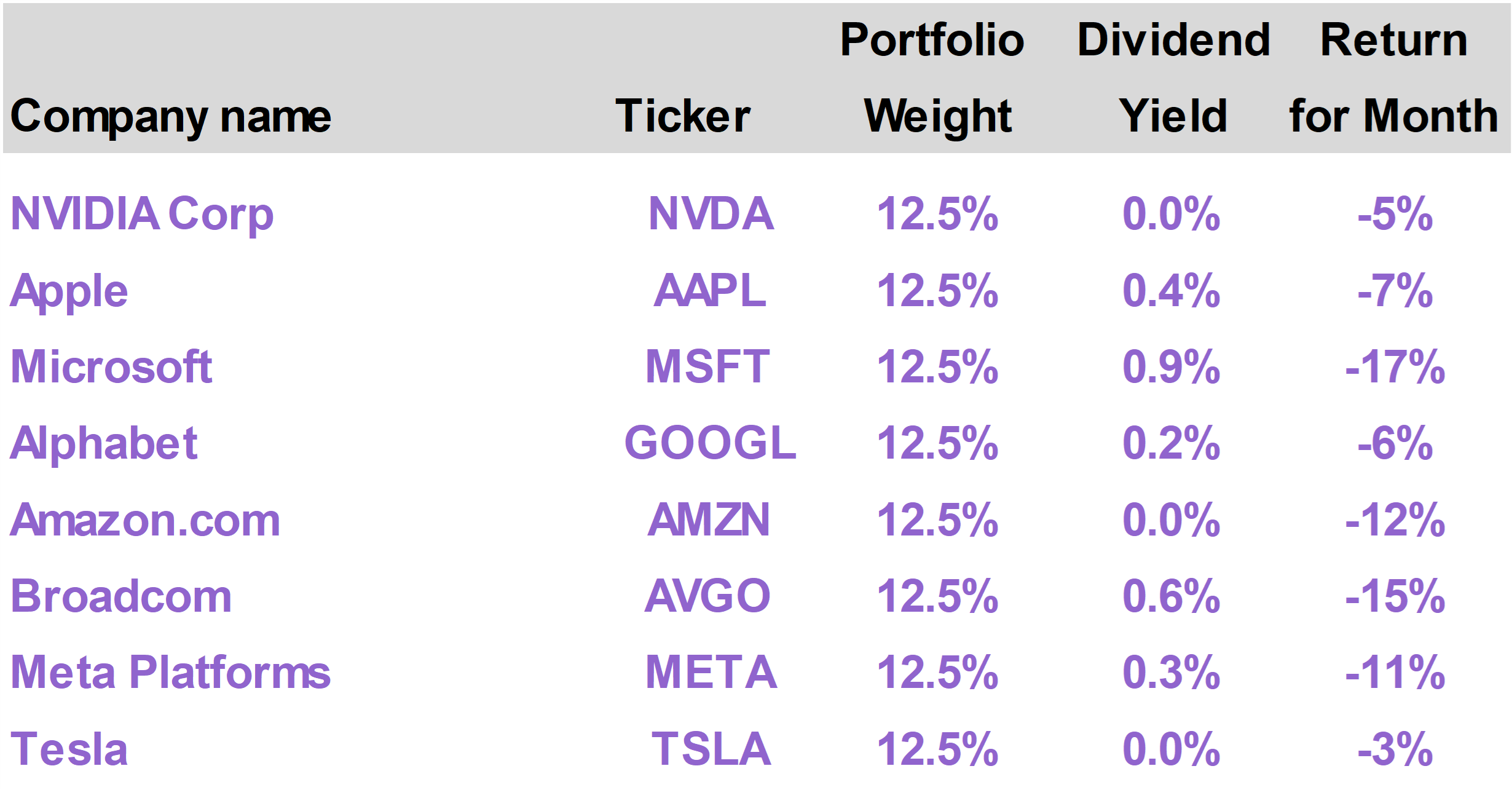

| | | Stocks declined in June with mega-cap Technology names significantly underperforming amid AI spending skepticism. While the average Mag 7 stock fell 10%, capital rotation into other sectors supported the overall market. The S&P 500 declined 1%. The American Resilience portfolio declined 5.1% as tech-related names like Circle (CRCL), Oracle (ORCL) and Meta (META) came under pressure. Arch Capital Group (ACGL), Eaton (ETN) and Williams (WMB) helped offset tech downside. Crude oil prices also fell sharply in June after the United States and Iran entered into a Memorandum of Understanding (MOU) that reopened the Strait of Hormuz. Yet short-term interest rates trended up after Kevin Warsh’s surprisingly hawkish debut as Fed Chair. Although the Fed is cautious at the moment, lower energy prices could lead to an improving outlook for interest rates over the balance of the year, potentially helping stocks and other risk assets.

|

|

| | | The American Resilience portfolio generated a total return of -5.1% in June, versus the S&P 500 Index return of -1.0%. On a year to date basis through the end of the month, the portfolio has returned 8.0%, versus the 10.2% return of the S&P 500.

The top performing portfolio positions in June were Arch Capital Group (ACGL), which returned 9%; Eaton (ETN), which returned 6%; and Williams (WMB), which returned 5%.

The worst performing positions were Circle Internet Group (CRCL), which returned -45%; Oracle (ORCL), which returned -35%; and Meta Platforms (META), which returned -11%. |

|

| Mega-cap tech slides

Following two very strong months, Technology stocks took a breather in June. Within the S&P 500, the Tech sector was actually flat, but this obscures more severe weakness among some of the largest capitalization tech names.

Every single mega-cap tech (or tech-adjacent) stock that we cover within our MAG7 MONITOR generated a negative return in June. The average Mag 7 stock declined 10%, contributing to a 2.8% decline in the NASDAQ Composite in June. |

|

|

| | Semiconductor stocks offset much of this weakness, with High-Bandwidth Memory plays like Micron (MU) and Sandisk (SNDK) continuing to deliver strong upside. The VanEck Semiconductor ETF (SMH) advanced 9.7% in June, propelled by memory names.

Within Technology, investors rotated capital from the customers of these supply-constrained semiconductor players (such as the Mag 7 hyperscalers) to the suppliers themselves.

The SpaceX (SPCX) IPO on June 12, the biggest IPO in history, was also a likely headwind for mega-cap tech stocks. The eventual inclusion of SPCX in various indexes means fund managers need to sell down other positions to raise cash for SPCX allocations.

As investors pulled money from the largest cap names in June, the Communication Services sector, dominated by Amazon (AMZN) and Meta (META), was the worst performer.

By contrast, sectors that have underperformed Technology in recent months, notably Industrials, Health Care and Financials, did comparatively well. |

|

|

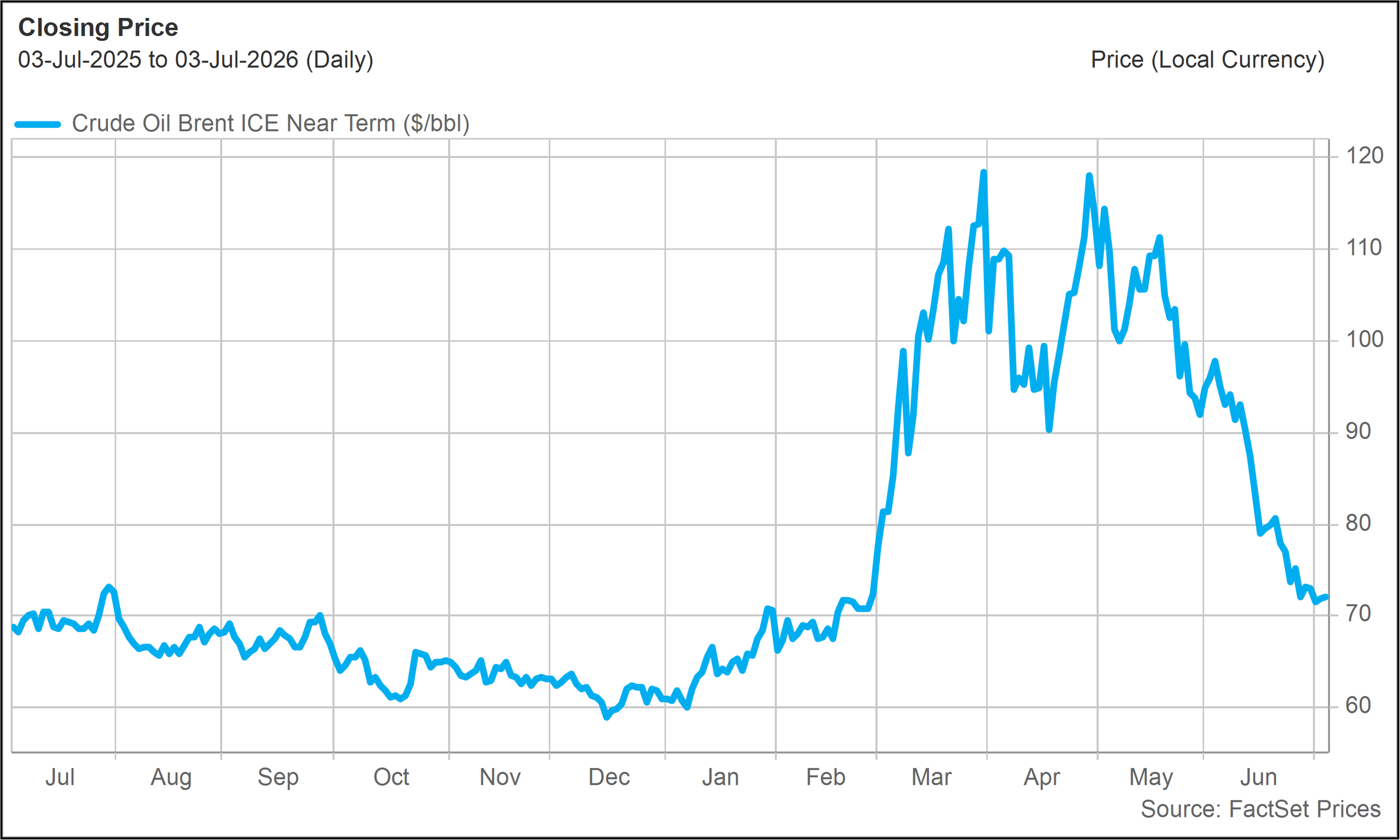

| Energy stocks also lagged in June as oil prices declined with the mid-month signing of a Memorandum of Understanding (MOU) between the United States and Iran.

The agreement is a prelude to what is expected to be a longer lasting peace deal that, among other things, will keep the Strait of Hormuz open for commercial traffic.

The immediate impact on oil markets has been sharp. Spot prices for Brent Crude Oil approached $70 per barrel by the end of June. They began the month north of $90. |

|

|

| Brent Crude Oil($/barrel - Last 12 Months) |

|

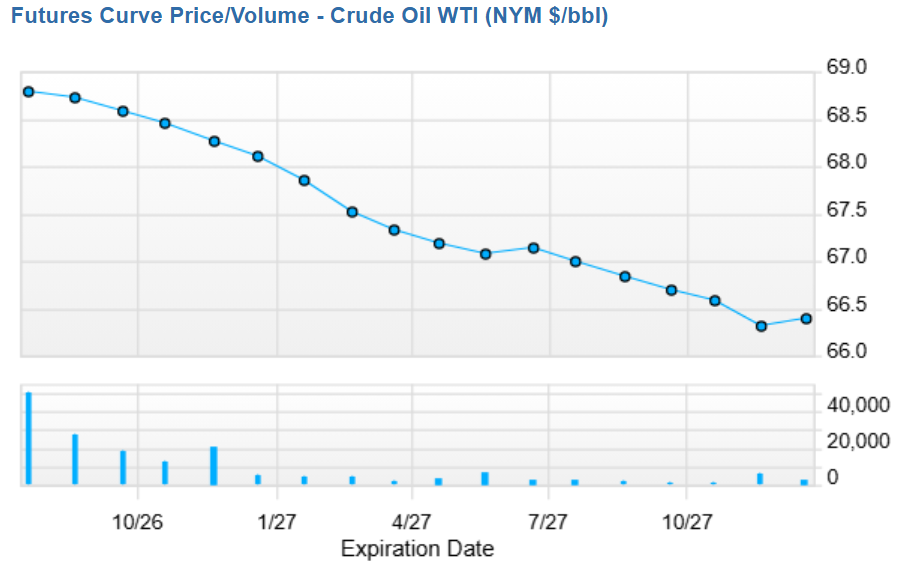

| As we have noted in previous reports, futures markets in oil have, throughout the war, indicated much lower oil prices in the months and years ahead. Futures markets are now pricing in even lower oil prices, with implied expectations in the mid-$60s range one year from now. |

|

|

| Crude Oil Futures Curve(Source: FactSet) |

|

| Is the inflation threat gone?

One might have assumed that the peace deal with Iran and subsequent decline in oil prices would have had a meaningful impact on inflation expectations and, by extension, interest rates.

After all, it was the outbreak of hostilities in the Middle East and closure of the Strait of Hormuz that caused short-term interest rates, as reflected by the One-Year Treasury yield, to rise sharply earlier this year. Between February and May 2026, One-Year Treasury Yields rose approximately a quarter-point to approximately 3.8%.

With the Fed funds rate now in a 3.5% to 3.75% band, this upward move reflected a sense that at least one previously expected rate cut will not materialize in the year ahead, along with some potential for a rate hike. |

|

|

| One-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

| Yet even though oil prices are now close to where they were in February, short-term interest rate expectations have not budged. In fact, the One-Year Treasury yield advanced approximately 0.15% in June, as oil prices collapsed.

Warsh’s surprising hawkishness

The new Fed Chair Kevin Warsh oversaw his first Federal Open Market Committee (FOMC) meeting and held his debut press conference on June 17. Warsh was handpicked by President Trump, whose strong desire to see the Fed cut interest rates has been made abundantly clear.

Warsh was nominated in part because he conveyed a path to lower interest rates through his focus on tech-driven disinflation and his stated desire to dial back the Fed’s long-term bond positioning. Warsh believes that shrinking the Fed’s balance sheet may potentially put some upward pressure on long-term bond yields but frees the Fed’s hand to have lower short-term rates.

The bond market expected a dove. Yet rather than come out with a strong rate-cutting message, Warsh spoke about the need to bring inflation back to target levels.

He also presented himself as a consensus-builder who would work collaboratively with other Fed officials, many of whom are now talking about the possibility of even having to raise rates.

To be fair, the recent inflation data, published toward the end of June, gives Warsh little room to sound too dovish at the moment. Headline inflation moved back above 4% in May, largely because of the energy shock, while core inflation, excluding food and energy, remained well above the Fed’s 2% target at 3.4%.

Playing the long game

Warsh may still be keen to bring interest rates down, but he needs to bring the other voting members of the FOMC onboard. Coming out too aggressively could undermine his ability to lead the Fed in that direction.

He also likely saw no need to make enemies during his first few weeks on the job by taking a belligerent attitude toward incumbent Fed Governors. He spoke positively about them during the press conference.

Warsh has consistently emphasized that the Fed under his leadership will be data-dependent. With inflation still elevated, the data does not currently support an aggressive dovish pivot.

But with oil prices headed sharply down, the data should soon follow. This will leave Warsh in a stronger position to advocate for lower rates as the impact of lower energy prices becomes reflected in consumer price readings going forward.

Even Trump seems content with the situation, noting that Warsh “has to do what he has to do” to overcome Fed board members who are “a little bit hostile.”

Stubbornly high interest rates remain a headwind for both the stock market and the economy but also a source of untapped upside. With oil now close to pre-Epic Fury levels, we may see the macro picture develop in a favorable way over the rest of the year. |

|

| | |

The top performing stocks in the portfolio in June were Arch Capital Group (ACGL), which returned 9%; Eaton (ETN), which returned 6%; and Williams (WMB), which returned 5%.

The worst performing positions this month were Circle Internet Group (CRCL), which returned -45%; Oracle (ORCL), which returned -35%; and Meta Platforms (META), which returned -11%. |

|

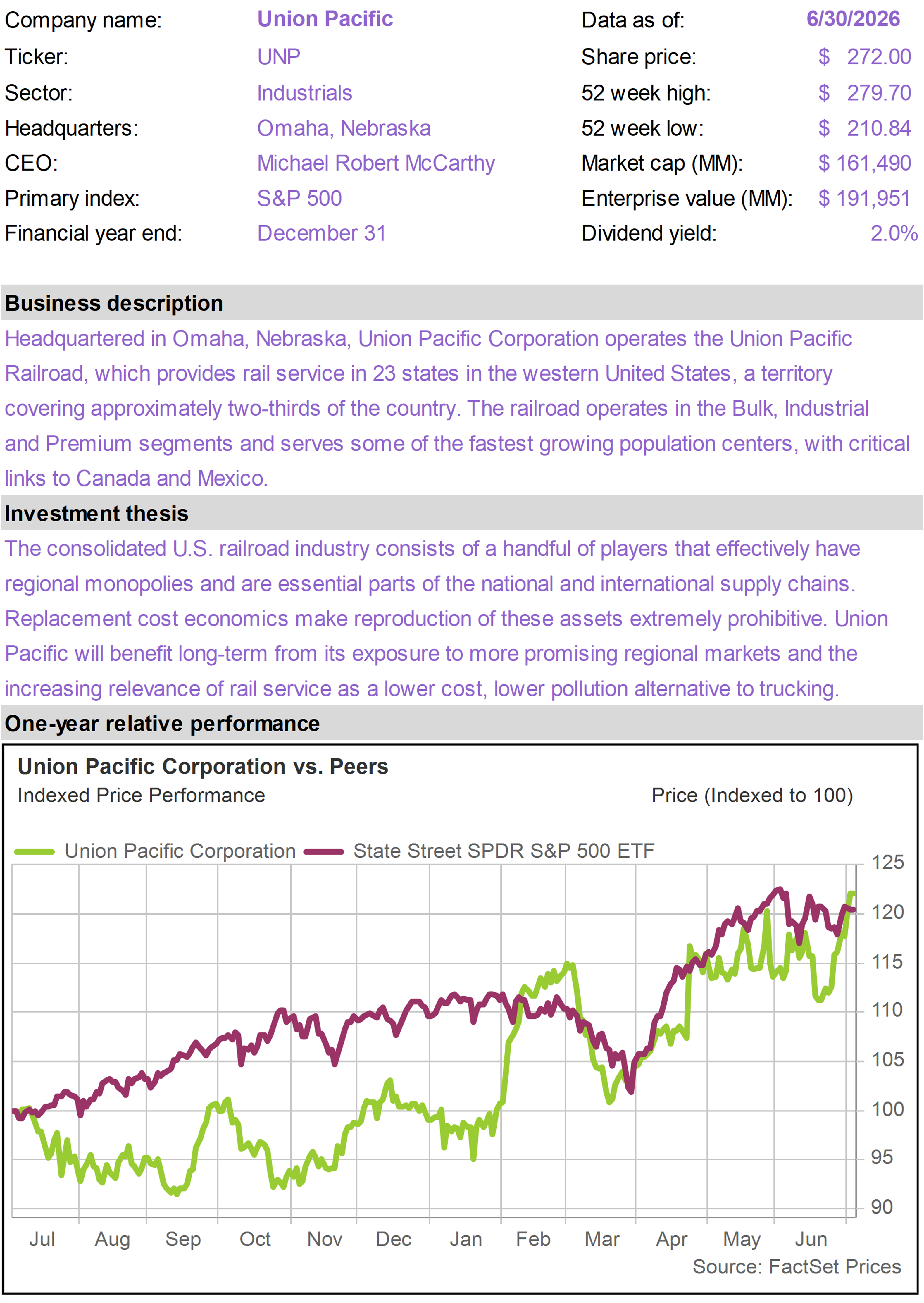

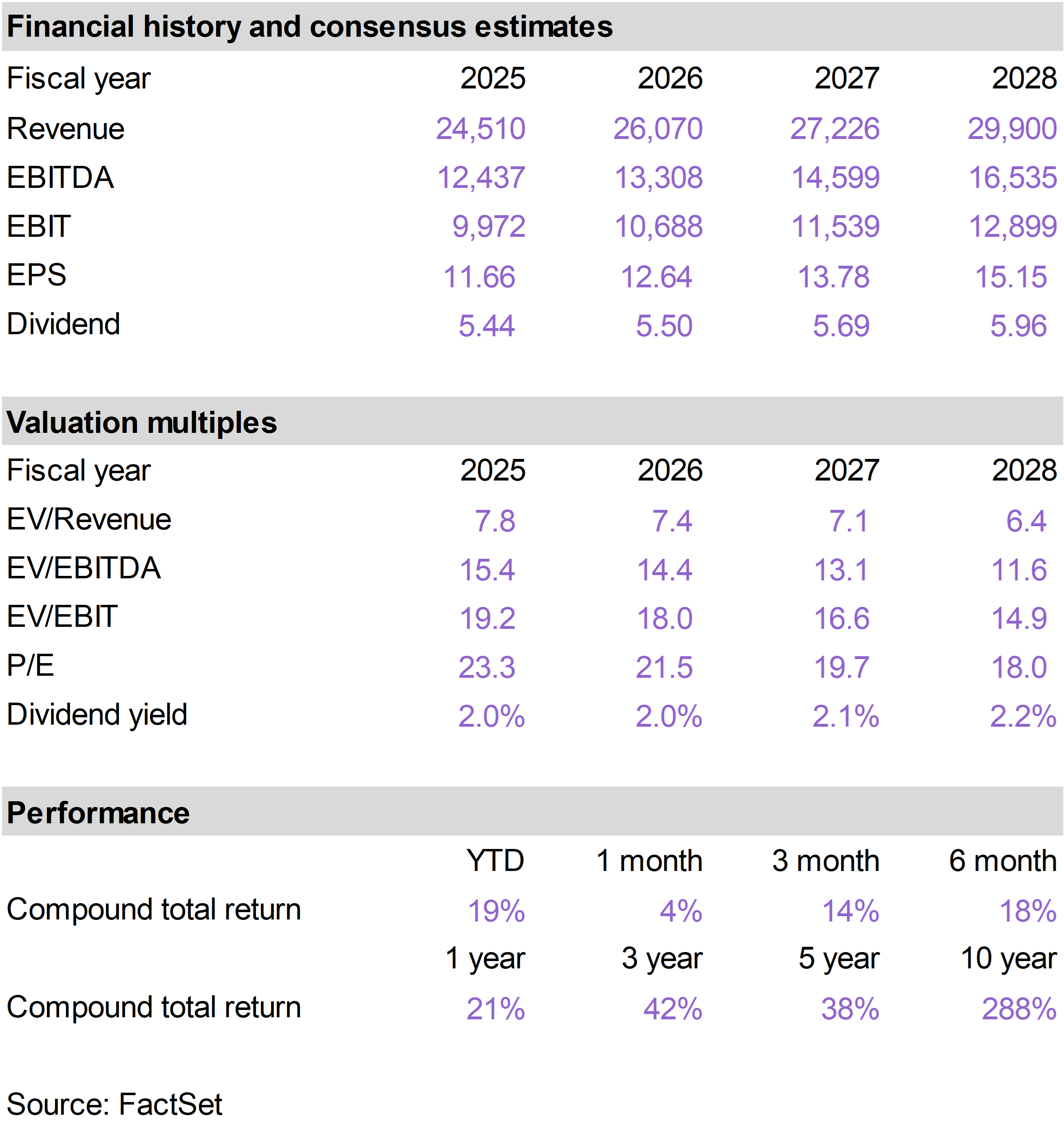

| | ACGL, a global specialty insurance and reinsurance company, performed well in June as investors rotated toward companies with visible earnings and less dependence on speculative growth.

The company had recently reported strong first quarter results, including significant share repurchases. Its reinsurance business also continued to generate attractive underwriting profitability.

The interest rate backdrop is helpful for ACGL. Even though oil prices collapsed late in the month, short-term rates did not fall meaningfully as discussed above. Higher short-term rates support investment income on its large fixed-income portfolio.

Early in the month, ACGL also announced a senior management change. Maamoun Rajeh, who had been leading the company’s Reinsurance business, was elevated to sole President and given oversight of Insurance as well. This positions Rajeh as the likely next CEO, which was well-received by investors.

In a month when large-cap technology lost momentum, ACGL offered disciplined underwriting, strong capital returns, current earnings power, and a valuation that already reflected a more cautious view of the insurance cycle. |

|

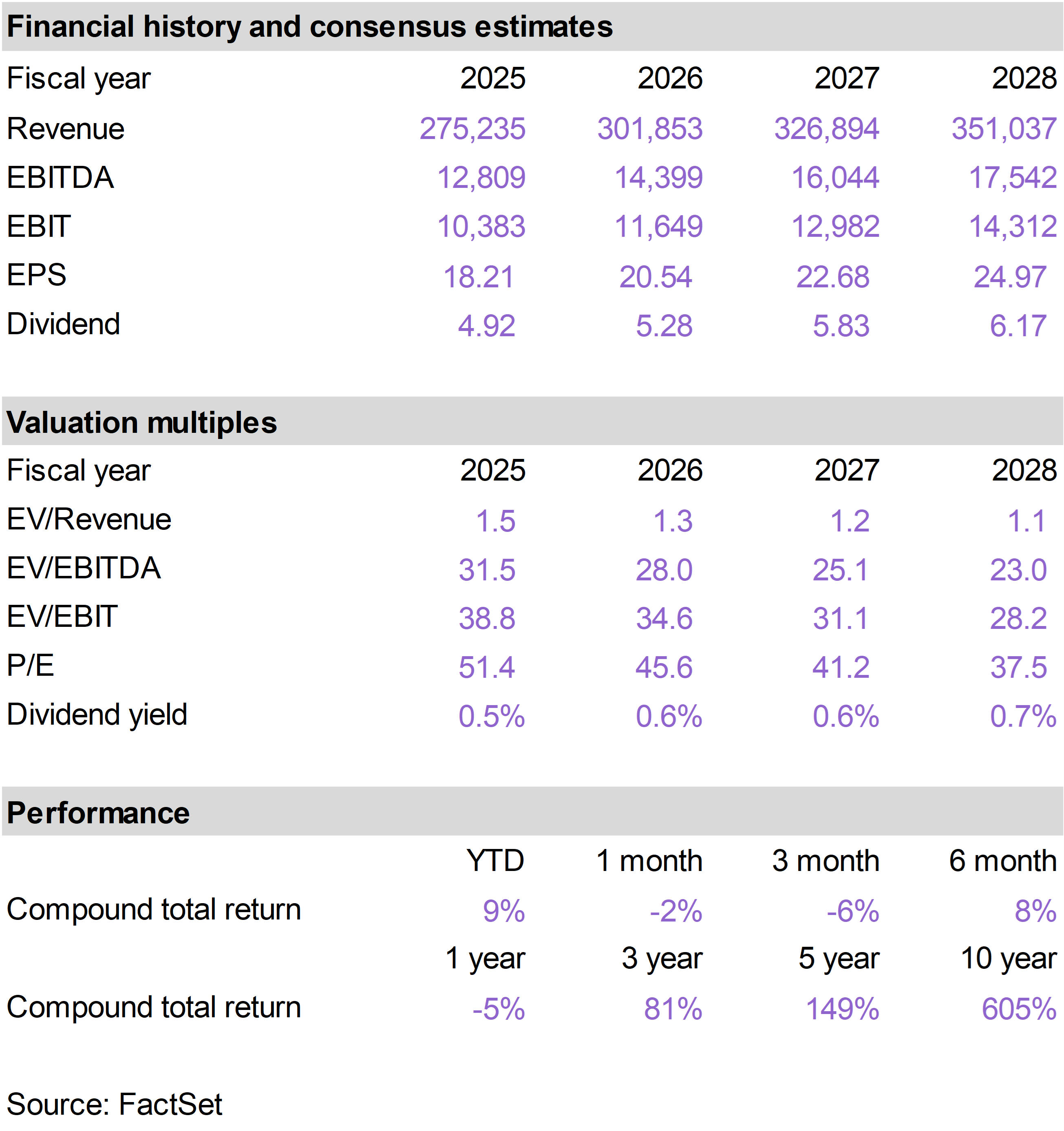

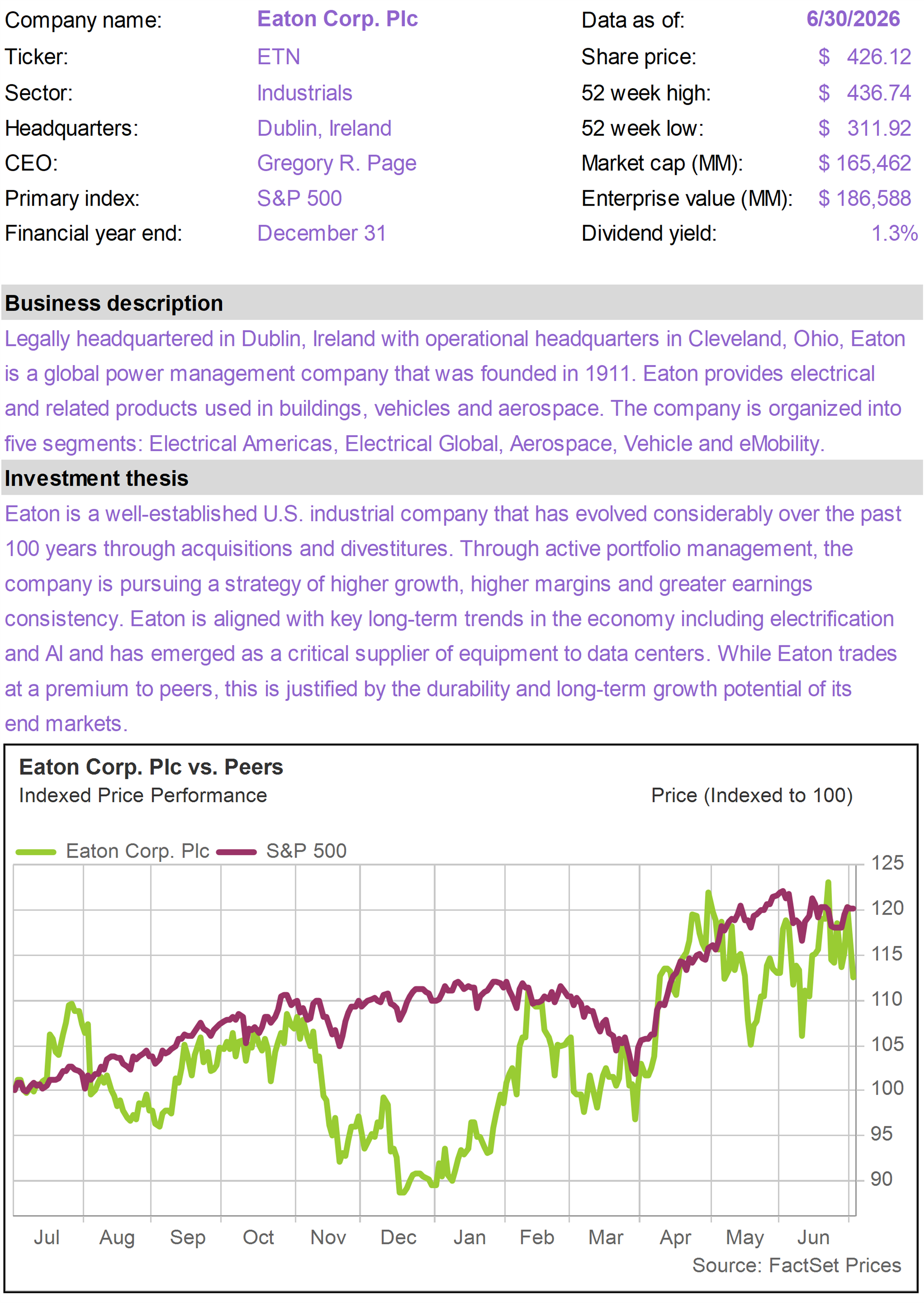

| | Shares of ETN advanced as investors continued to reward companies tied to electrification, grid investment, data centers, and aerospace demand.

ETN has increasingly become a play on the long-term need for more electrical infrastructure, especially as AI data centers, reshoring, and grid modernization drive demand for power distribution and related equipment.

During the month, ETN announced a transaction to separate its Mobility business through a combination with Dana (DAN). This was a meaningful portfolio-cleanup move. Mobility is a lower-margin, slower-growth business relative to ETN’s core Electrical and Aerospace segments.

The transaction is expected to modestly dilute near-term earnings, but improve ETN’s longer-term growth rate and margin profile. It also gives ETN a cleaner story: less exposure to traditional vehicle components and more exposure to higher-quality industrial and electrical markets. |

|

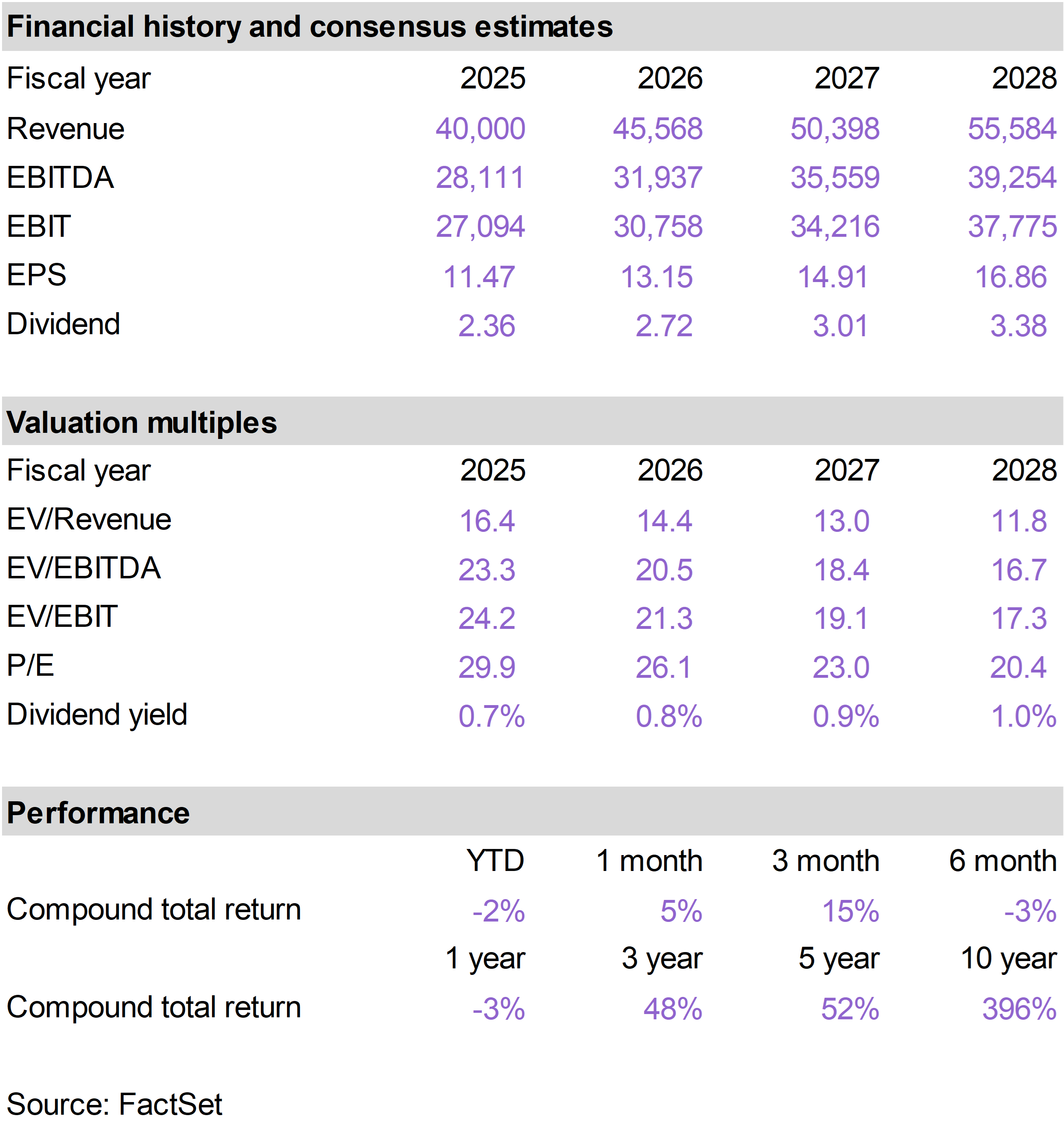

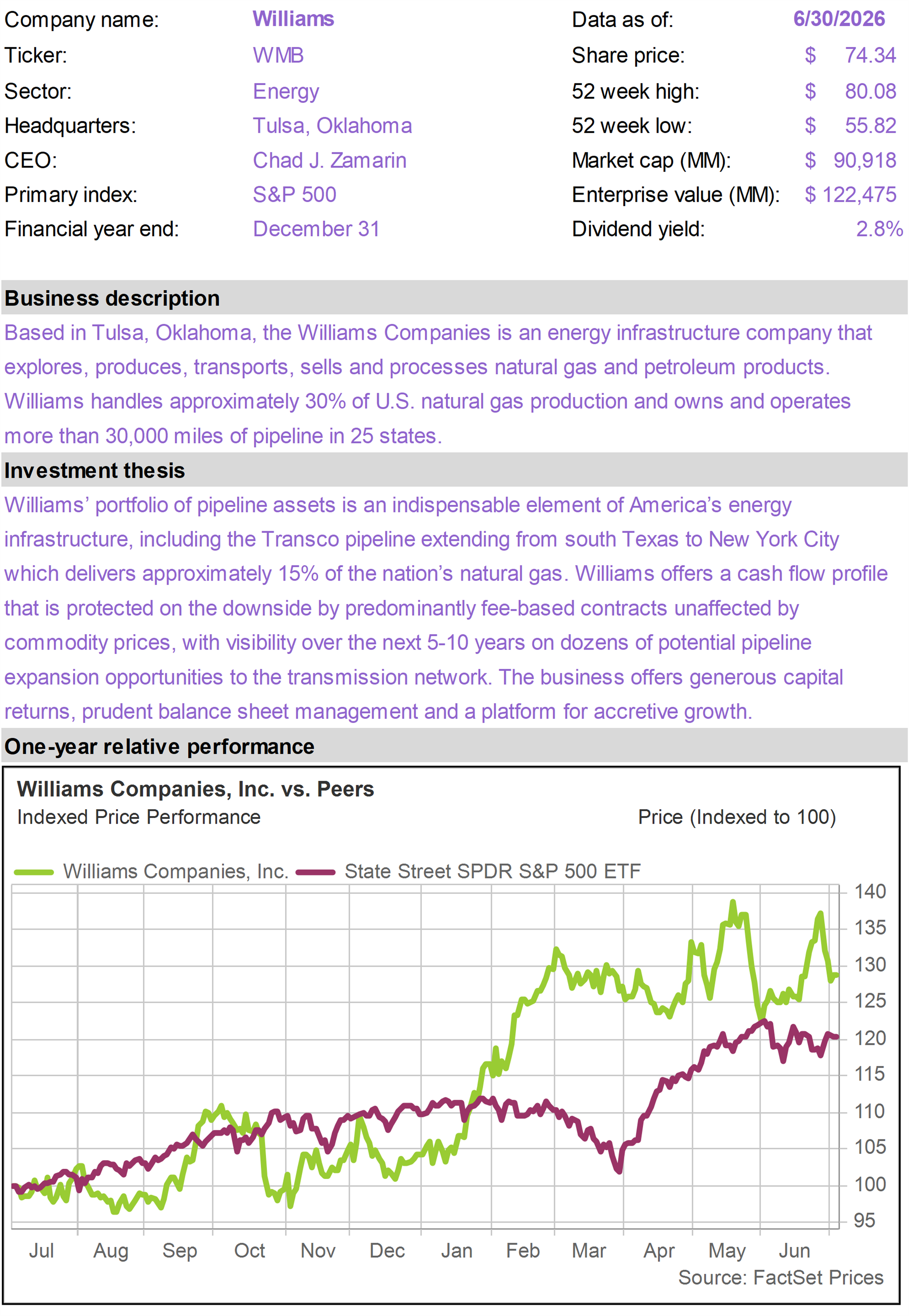

| | Despite significant energy sector weakness, WMB performed well in June as investors continued to recognize the strategic value of natural gas infrastructure in a power-constrained economy.

One the largest U.S. natural gas infrastructure companies, the investment case continued to broaden in June.

WMB is increasingly viewed not just as a traditional midstream company, but as an infrastructure beneficiary of AI-driven power demand. The company is working on “behind-the-meter” power solutions for hyperscale data centers, where access to gas, turbines, siting, and execution speed can be major competitive advantages.

Management commentary during the month reinforced the idea that WMB may have many years of visible growth ahead, driven by data center power needs, utility demand, storage expansion, and Liquefied Natural Gas (LNG) exports. The company is also exploring creative financing structures that could help fund growth projects without putting excessive pressure on the balance sheet.

Late in the month, reports indicated that WMB was in advanced talks to acquire Momentum Midstream, a private natural gas infrastructure company with a significant Haynesville Shale footprint. If completed, the transaction would strengthen WMB’s position in one of the most important gas supply basins serving Gulf Coast LNG exports, industrial demand, and power generation. |

|

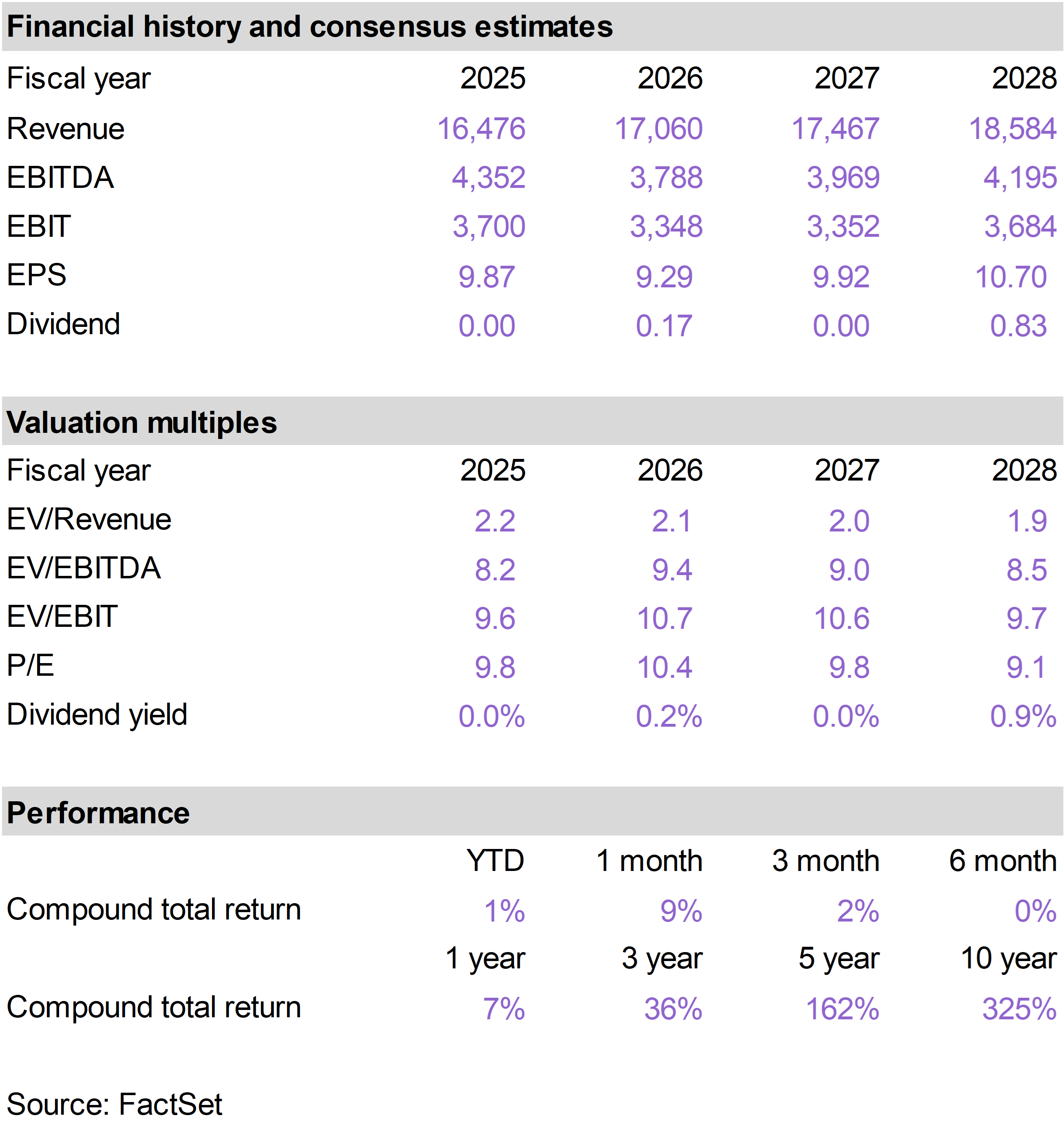

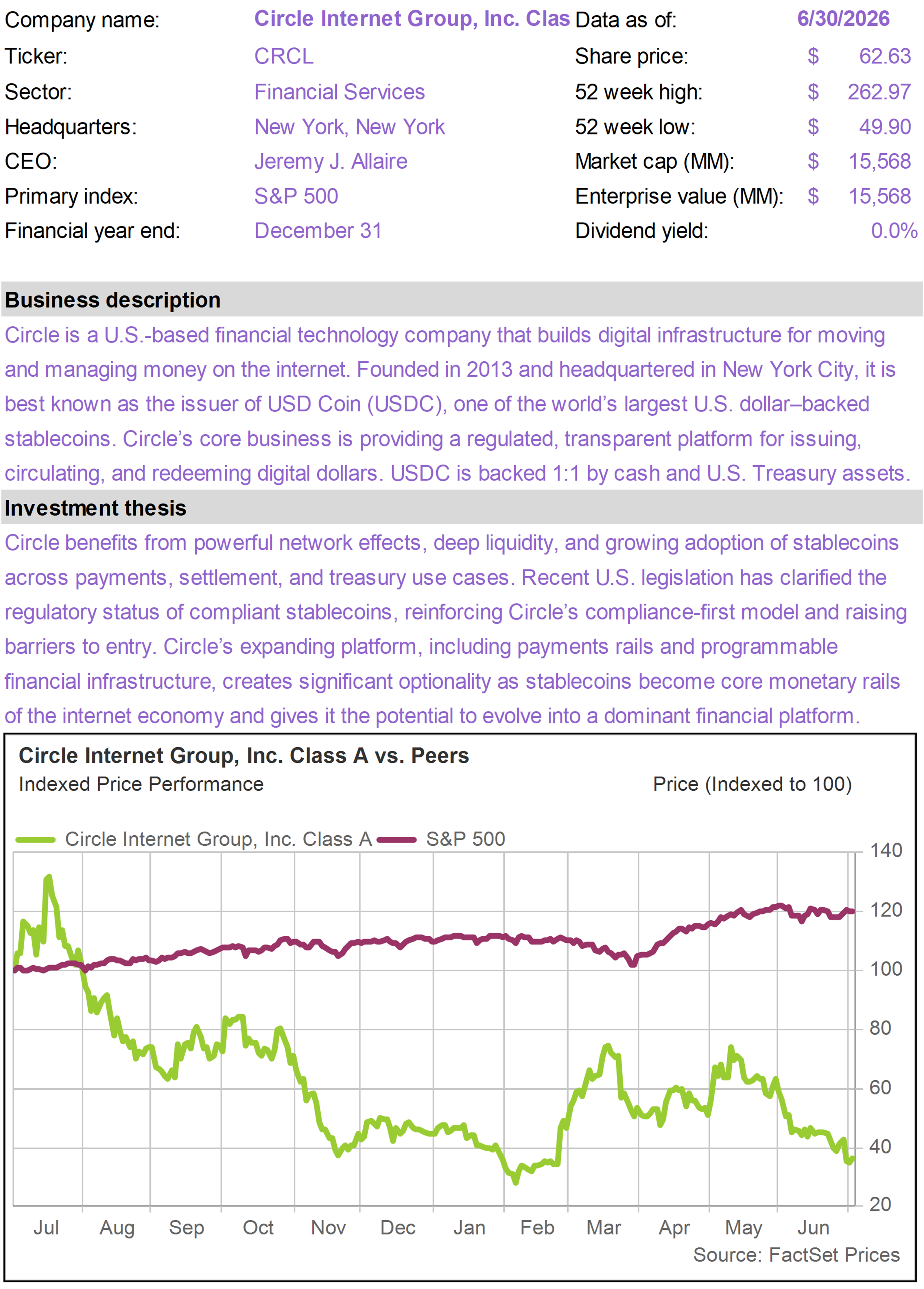

| | After strong performance in May, CRCL traded down sharply in June with weak crypto sentiment weighing on digital-asset-related equities and investors reacting negatively to a new competitive threat in stablecoins.

CRCL is the issuer of USDC, the second-largest stablecoin in the world. While the stock was pressured by the broader risk-off move in crypto, the sharper concern late in the month was the announced launch of a competing stablecoin, Open USD.

We believe the market reaction was excessive. Competition in stablecoins is inevitable, especially given the enormous potential size of the market. But competition also validates the opportunity. New entrants are effectively confirming that regulated digital dollars are becoming a major financial infrastructure category.

CEO Jeremy Allaire made a similar point in response to the Open USD announcement. He emphasized that stablecoins are platform and network-effect businesses, where liquidity, integrations, regulatory reach, and repeated transaction usage compound over time.

In other words, the threat is not simply whether a consortium can announce a competing stablecoin; the real test is whether it can build the trusted, liquid, widely integrated network that USDC already has. Consortiums like this have a poor track record of commercial success.

USDC already has a roughly $73 billion market capitalization, nearly 15 times larger than the closest GENIUS Act-compliant competitor.

Open USD does not appear to solve a problem that USDC has failed to address. CRCL already offers the scale, liquidity, regulatory positioning, partner incentives, and stablecoin movement infrastructure that a new entrant would need years to replicate.

In our view, the June selloff appears more like a sentiment-driven reset than a broken investment thesis. Crypto weakness and fear of competition hurt the stock, but the underlying case remains intact: USDC has scale, regulatory positioning, brand trust, and infrastructure advantages that will be difficult for new entrants to replicate. |

|

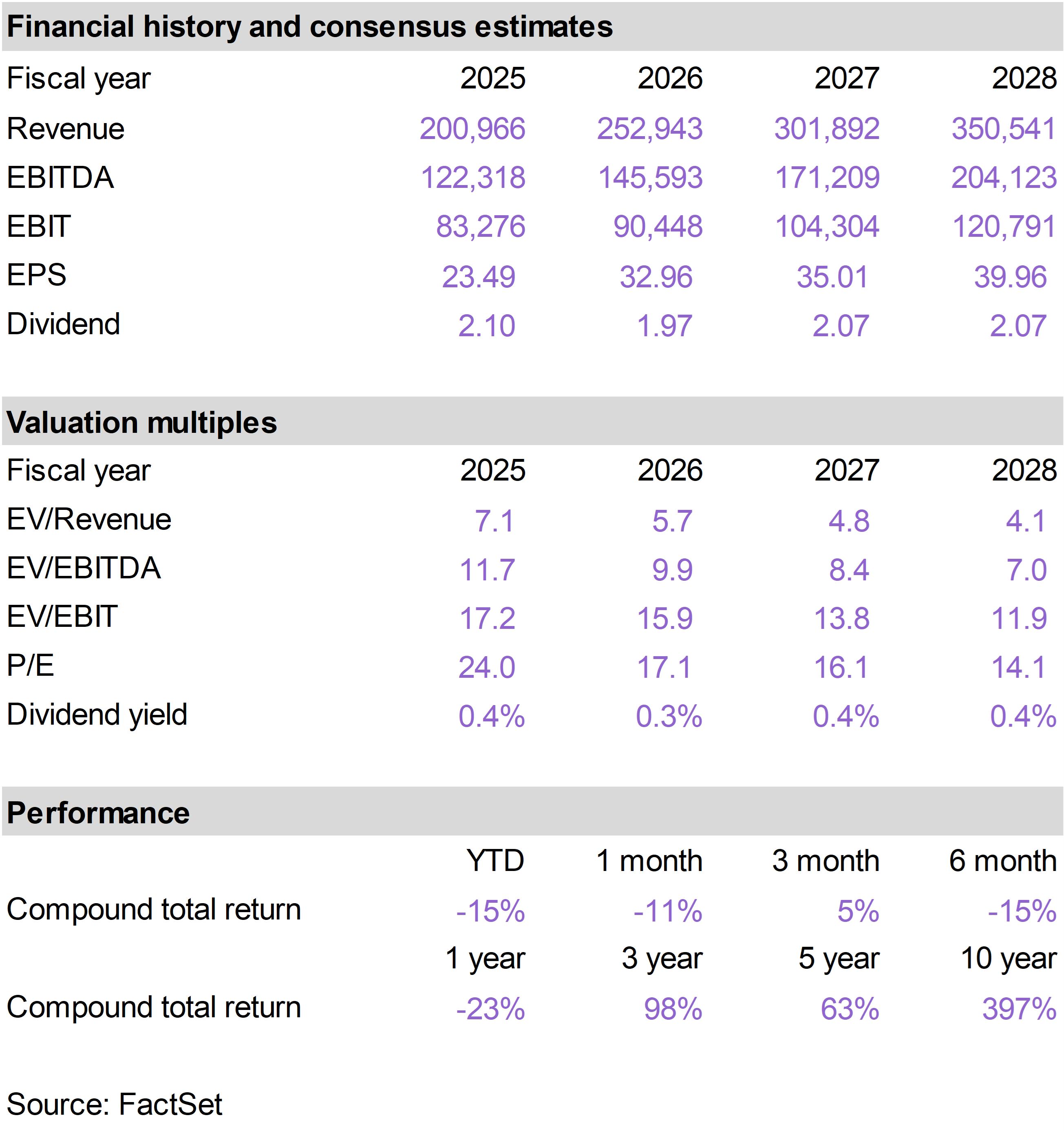

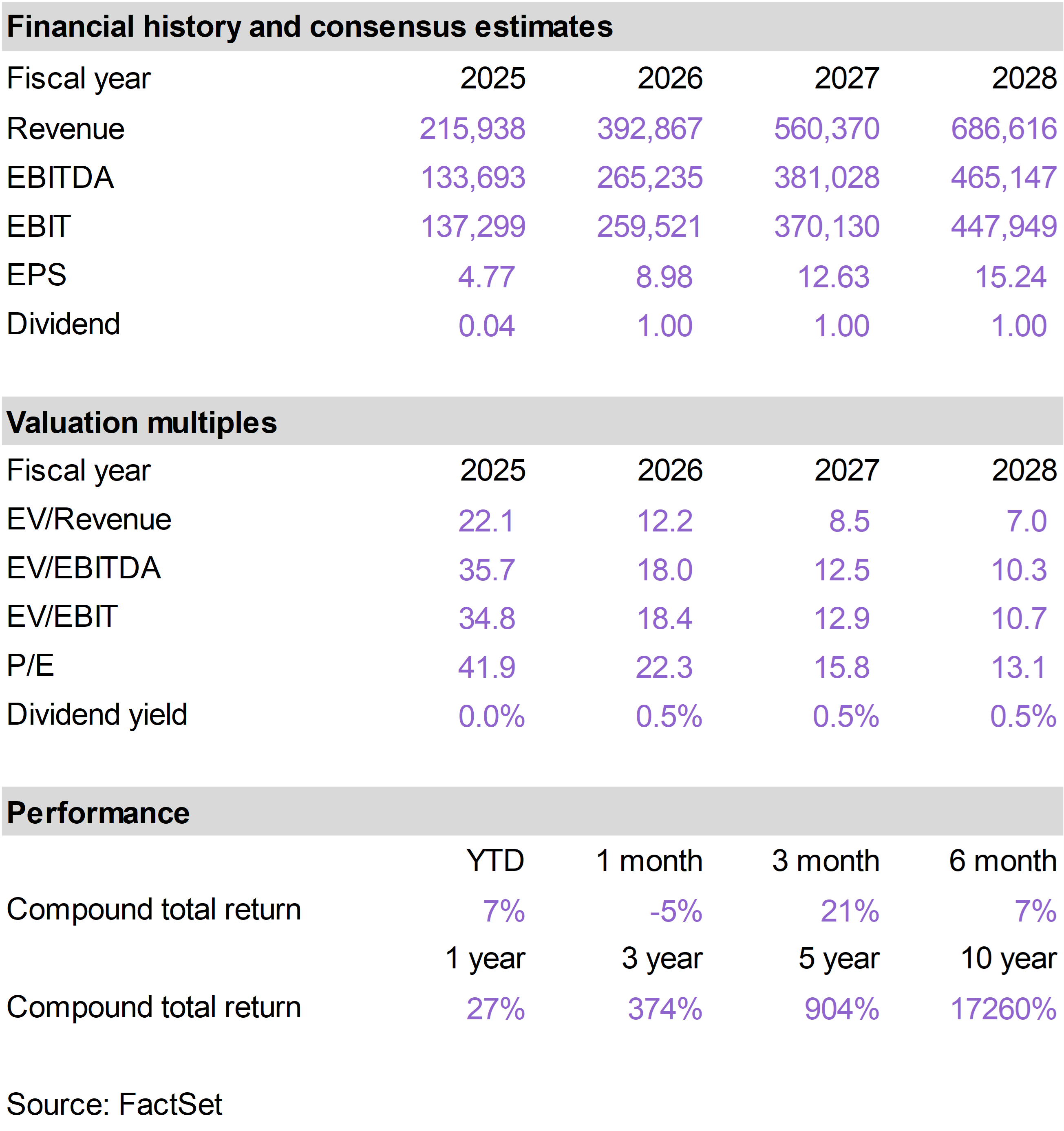

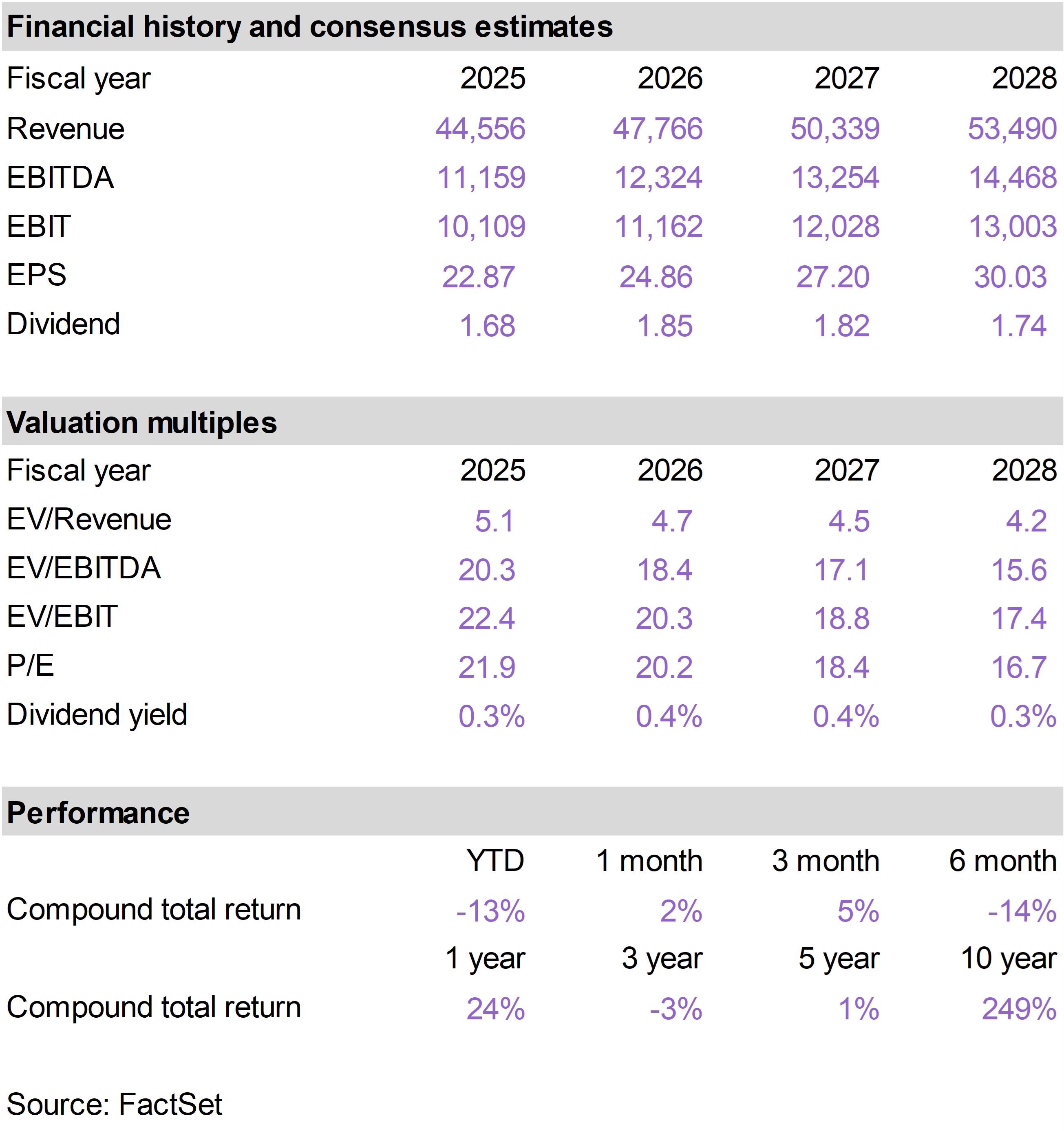

| | Over the course of June, ORCL also gave back strong performance that was generated in May. Investors weighed ORCL’s extraordinary AI-driven backlog growth against concerns about the massive capital spending required to build out Oracle Cloud Infrastructure.

The positive side of the story is demand.

ORCL reported a huge increase in remaining performance obligations in June, with backlog rising to approximately $638 billion, up more than 360% year-over-year. That backlog provides unusually strong revenue visibility and supports the view that ORCL is becoming a major beneficiary of AI compute demand.

Oracle Cloud Infrastructure revenue rose more than 100% year-over-year in the quarter, helping drive total revenue growth of roughly 21%.

The chief concern is capital intensity.

ORCL guided to approximately $90 billion to $95 billion of fiscal 2027 capital spending, which raised investor questions about free cash flow, financing needs, and balance sheet leverage. However, the company is using customer prepayments, “bring-your-own-hardware” arrangements, and equity-linked financing to help fund the buildout while preserving its investment-grade credit profile.

In a month when investors became more selective toward AI-related stocks, ORCL remained a debated name. The opportunity is enormous, but the market is demanding proof that the company can finance the buildout, protect margins, and turn AI infrastructure demand into durable earnings growth. |

|

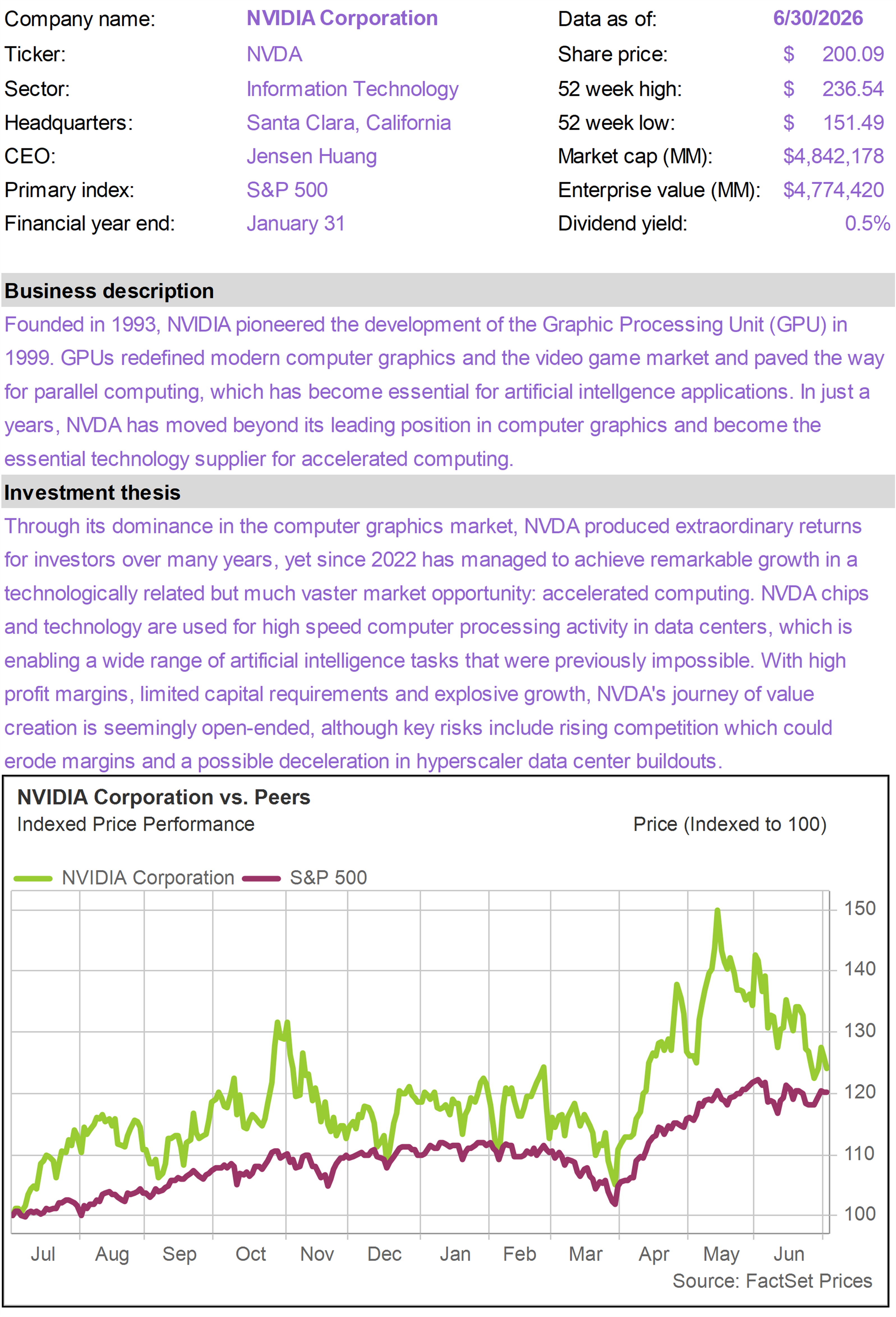

| | Along with its Mag 7 peers and other AI hyperscalers, META was pressured in June as investors continued to scrutinize the scale of AI-related capital spending across the largest technology platforms.

As the parent company of Facebook, Instagram, WhatsApp, Messenger, and Threads, META has one of the largest consumer attention and digital advertising platforms in the world. The core business remains highly profitable, but the stock has increasingly been judged by whether it can turn massive AI investment into new revenue streams.

One important development in June was META’s introduction of Business Agent at its Conversations 2026 event. The product is designed to let businesses automate customer communication across WhatsApp, Messenger, and Instagram, including customer service, appointment booking, transactions, analytics, and escalation to human support when needed.

This builds on a business messaging opportunity that is already gaining traction.

META’s Family of Apps “Other” revenue, which includes WhatsApp Business Platform revenue, has grown rapidly, and paid messaging on WhatsApp has already crossed a $2 billion annual run-rate. Business Agent and related messaging products could eventually address a $75 billion-plus market opportunity.

Recent reporting that META is exploring a cloud business to sell excess AI computing capacity is also relevant.

While some investors viewed the story as evidence that META may have overbuilt AI infrastructure, we see a more constructive interpretation: if META can monetize unused compute, it may be able to offset part of the cost burden from its AI buildout and turn a perceived capital-spending problem into another revenue opportunity.

In a month when investors were increasingly skeptical of AI capex, META suffered from the same concern affecting other mega-cap platforms. But the investment case remains attractive: the core advertising engine is powerful, the valuation has compressed, business messaging and agents create a potentially underappreciated growth driver, and excess compute monetization could help address one of the market’s biggest objections to the stock. |

|

| | |

| | |

| | |

| | | Oracle Corporation (ORCL) |

|

|

|

| | |

|

| | |

|

| | |

|

| | Arch Capital Group (ACGL) |

|

|

|

| | |

|

| | Circle Internet Group (CRCL) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Thermo Fisher Scientific (TMO) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

| | The 76research American Resilience Model Portfolio is designed to provide exposure to growth businesses that operate with competitive advantages in structurally attractive markets. The objective is to identify businesses that can survive and thrive across different macroeconomic environments and whatever geopolitical crises may unfold. The holdings are intended as long-term investments to drive portfolio compounding with minimal need to realize taxable gains. Emphasis is placed on critical markers of business quality such as barriers to entry, physical scarcity of assets, balance sheet strength, effective capital allocation and durable long-term growth drivers. These assessments are paired with careful consideration of valuation and risk. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

|