| American Resilience Model Portfolio |

|

| Monthly Portfolio Review: March 2026Publication date: April 5, 2026 |

|

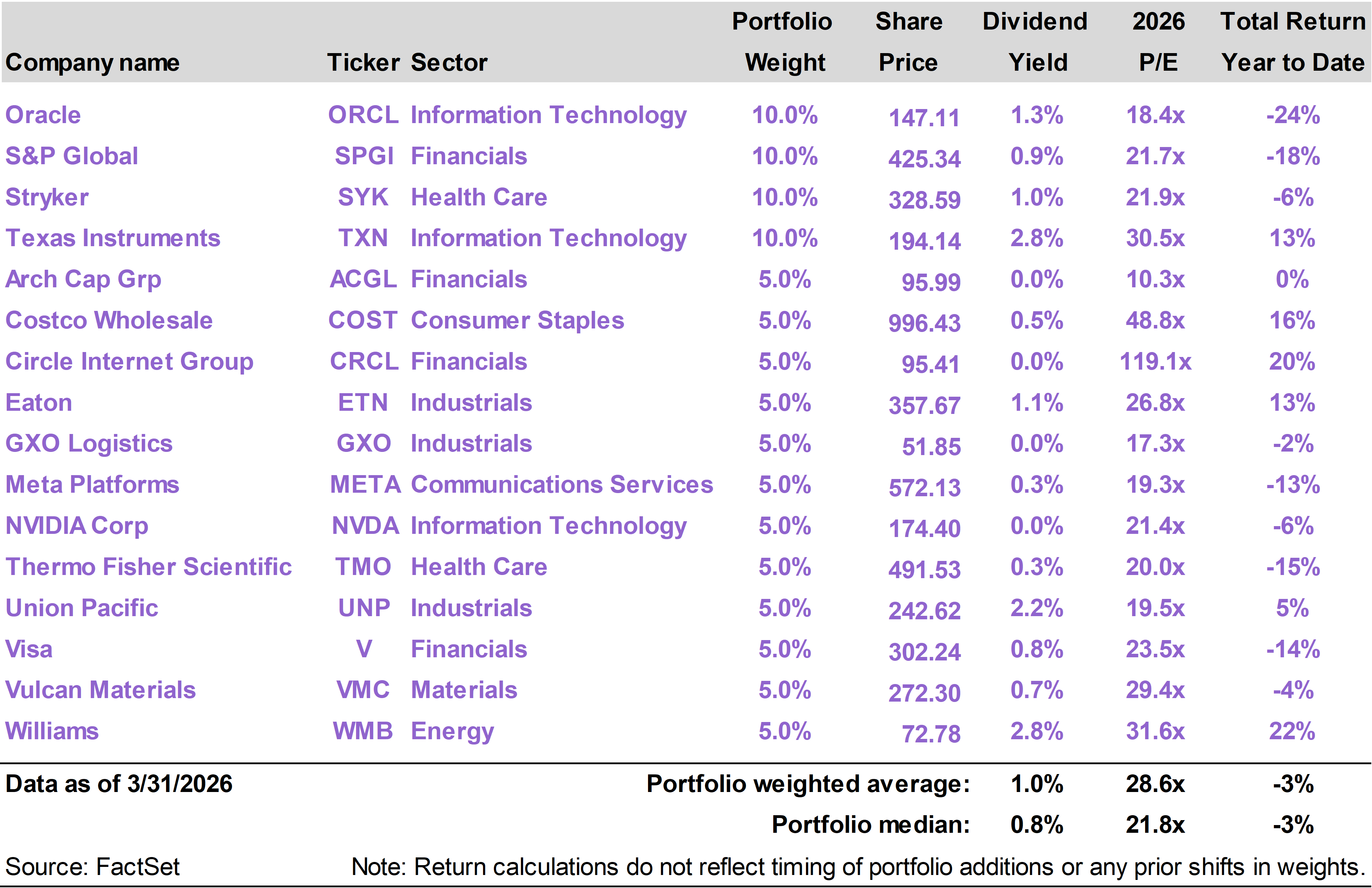

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

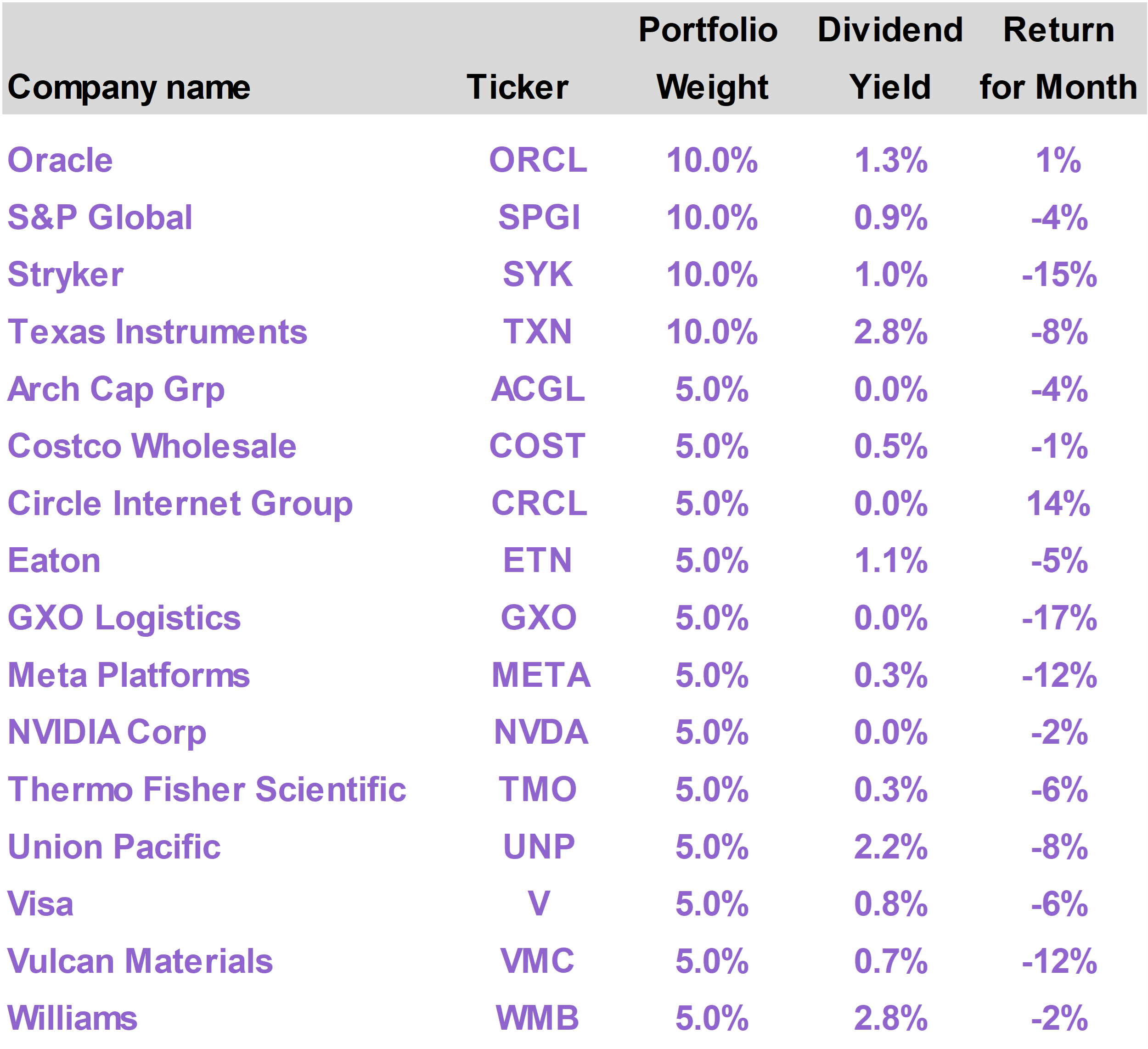

| | | With the notable exception of the Energy sector, March was a challenging month for stocks across the board. The spike in crude oil prices following the commencement of Operation Epic Fury drove a -5.0% return for the S&P 500. The American Resilience portfolio returned -5.6% this month. On a year to date basis, the portfolio has gained 0.2%, whereas the S&P 500 has declined 4.3%. The effective closure of the Strait of Hormuz disrupted energy markets, creating a new source of inflation risk. Both short-term and long-term interest rates rose in March as Fed officials grew less inclined to cut rates, which pressured stocks. Circle Internet Group (CRCL) led the portfolio again with a 14% return. GXO Logistics (GXO) and Stryker (SYK) were the largest detractors. With Trump now threatening severe escalation, the standoff over the Strait of Hormuz appears to be coming to a head. We believe, one way or another, the Strait of Hormuz will reopen, potentially in a matter of days or weeks, at which point investor sentiment should improve significantly.

|

|

| | | The American Resilience portfolio generated a total return of -5.6% in March, slightly trailing the S&P 500 Index return of -5.0%. On a year to date basis through the end of the month, the portfolio has returned 0.2%, outpacing the -4.3% return of the S&P 500.

The top performing portfolio positions in March were Circle Internet Group (CRCL), which returned 14%, and Oracle (ORCL), which returned 1%.

The worst performing positions in the portfolio this month were GXO Logistics (GXO), which returned -17%, and Stryker (SYK), which returned -15%. |

|

| Epic Fury pressures stocks

Operation Epic Fury, which kicked off at the very end of February, was the dominant factor in financial markets throughout the month of March. The main issue was the spike in oil prices, which had direct impacts on many companies and significant ripple effects across the entire market.

A down 5% month in the S&P 500—after a three-year run, leading up to the end of February, that produced an 81% total return in the index—is far from a catastrophe. While stocks certainly lost ground in March, it is notable that the stock market also showed a fair amount of resilience.

By any objective standard, the U.S. has exhibited unprecedented military dominance after making the decision to neutralize Iran as a threat.

In a matter of weeks, Iran’s conventional warfare capacity has been severely diminished, while its nuclear weapons program sustained another enormous setback. Multiple layers of the regime’s political leadership were destroyed.

Despite all the losses, Iran’s ability to wage war was not totally eliminated, leaving the regime one critical opportunity to push back. By threatening cargo ships in the Strait of Hormuz, Iran has been able to disrupt the flow of oil and other commodities out of the Persian Gulf.

It does not take much to stop commercial shipping vessels from going about their normal business. Iran took full advantage of this vulnerability.

The Iranian regime (or what remains of it) cannot stop the U.S. militarily, but it can manufacture a difficult economic and political scenario for Trump by interfering with global oil markets. This is the strategy they have unsurprisingly pursued.

Oil surges

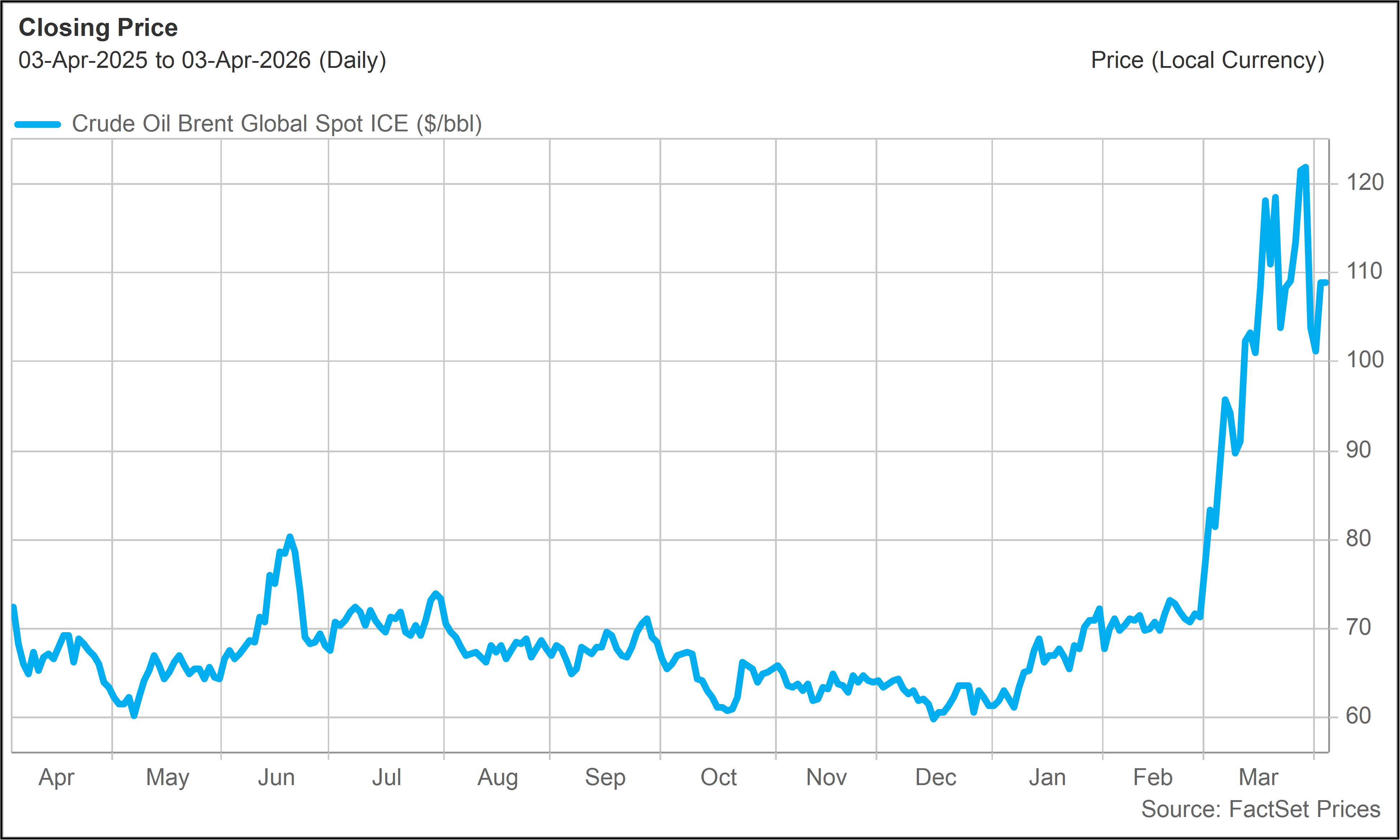

Global oil markets ended last year in a well-supplied state, with a barrel of brent crude having drifted as low as $60.

Spot crude oil prices then started to move upward in the beginning of 2026, especially as oil traders took note of rising tensions between the U.S and Iran in February, with U.S. naval assets being deployed to the Middle East.

Once Epic Fury began at the end of February, and it became apparent that tankers would at least temporarily not be able to make their way through the Strait of Hormuz, oil prices immediately surged.

Spot crude moved from around $70 at the start of the month to as high as $120 at one point, settling in the $100 to $110 range by the end of the month. |

|

|

| Brent Crude Oil($/barrel - Last 12 Months) |

|

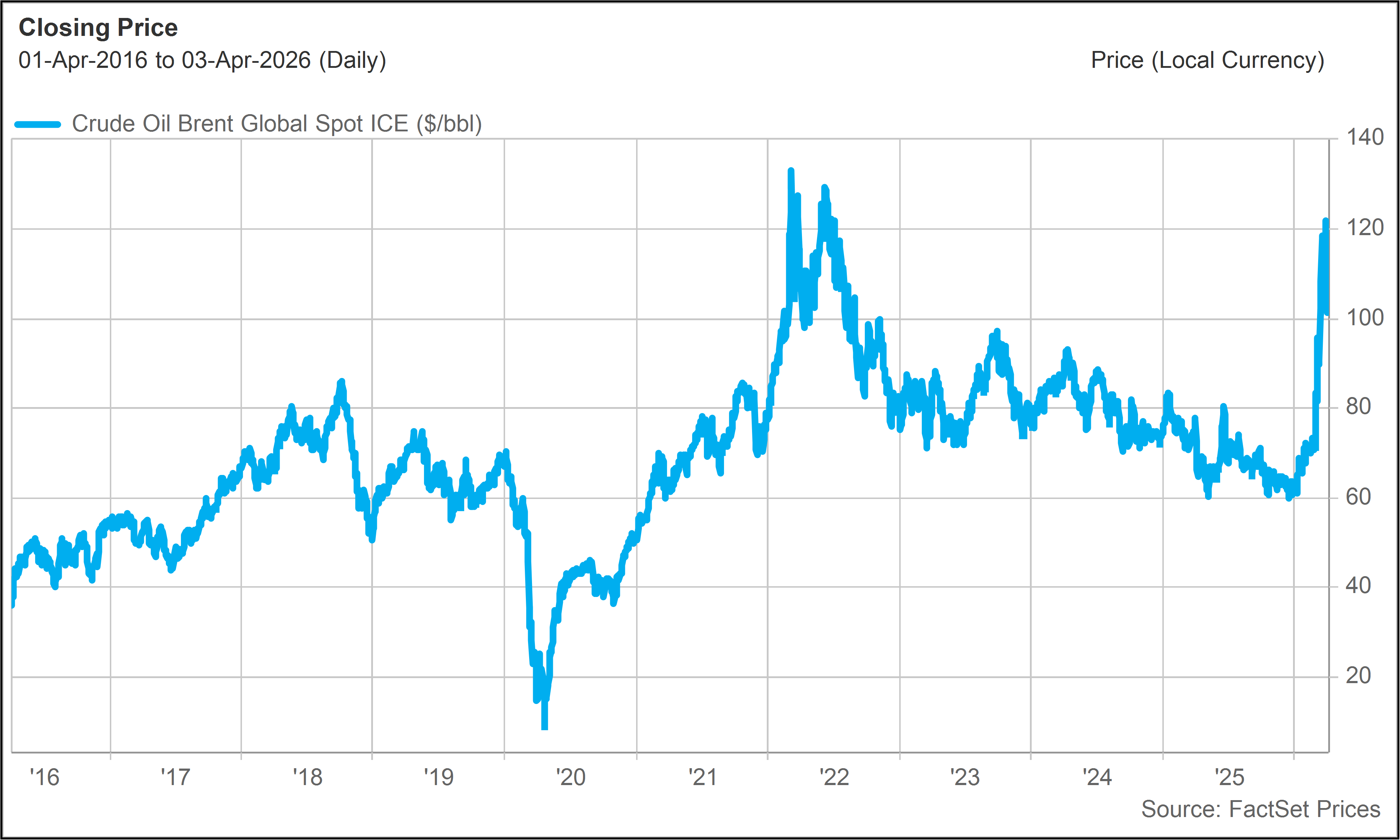

| The move in oil prices was abrupt, especially because oil prices were so low to begin with. It is worth noting, however, that over a longer time horizon, current oil prices are not especially stretched.

This should give investors some comfort in the global economy’s ability weather this storm. It also helps explain why the market is not reacting to this event as a full-blown crisis.

Current oil prices in fact remain below their highest levels of 2022, during the Russia-Ukraine conflict.

On an inflation-adjusted basis, current prices are largely in line with the 2018 peak in oil prices, north of $80 per barrel. Oil prices drifted higher in that time frame as a result of strong demand and restrictive global supply conditions. |

|

|

| Brent Crude Oil($/barrel - Last 10 Years) |

|

|

The ramifications of higher oil

Even after the March surge, oil prices are not at dangerously high levels from a historical perspective. And as a net exporter of all fossil fuels (albeit a net importer of crude oil), the United States is also relatively protected from energy shocks.

Furthermore, many companies and workers in the U.S. are connected to the energy sector, directly or indirectly, and therefore stand to benefit from higher energy prices and higher profits.

All that said, the marginal impact of the spike in oil prices on the economy and market expectations is material.

Everyone in the U.S. is a consumer of energy. High energy prices act like a tax on economic activity and in that way tend to depress economic growth.

Rising energy prices are also inflationary, which is particularly inconvenient in the current environment.

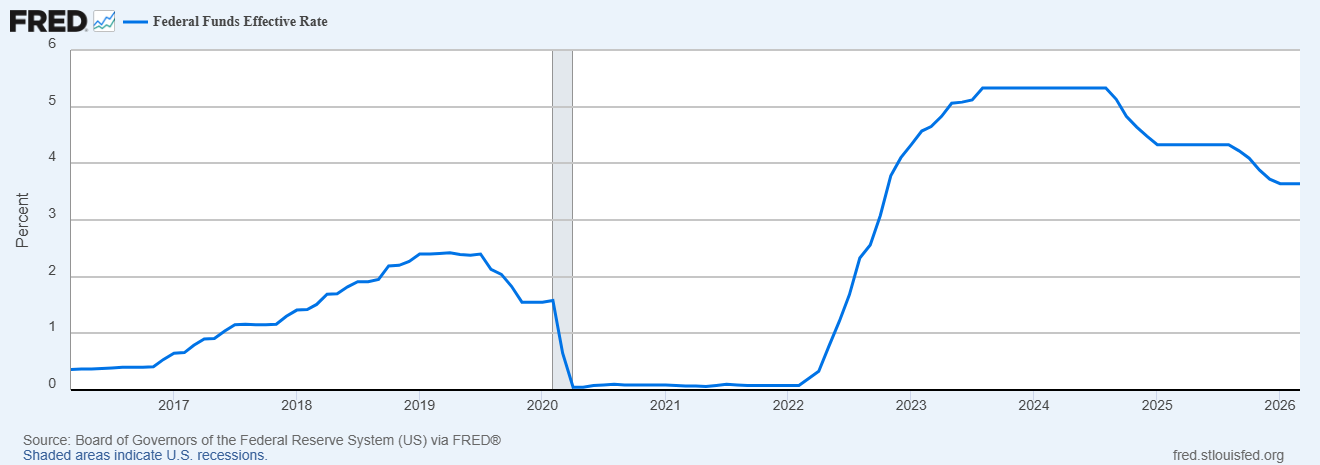

Inflation has come way down from Biden-era peaks, but the U.S. economy has not quite reached the Fed’s informal 2% inflation target, trending closer to 3%.

As a result, the Fed has kept short-term interest rates elevated, even though they have been causing significant friction in the housing market and other challenges for consumers. |

|

|

| Fed Funds Rate(Last 10 Years) |

|

| The Fed pivots hawkish

Perhaps the most significant market impact of the war in Iran has been on interest rates.

When Federal Reserve officials convened for the regularly scheduled FOMC meeting in the middle of March, they left the short-term Fed funds rate unchanged but signaled a more hawkish outlook.

For investors in stocks, the key takeaway from the Fed meeting was its reluctance, at least over the next several months, to stay on the rate-cutting path. Fed officials are concerned that higher oil prices will put upward pressure on inflation, which they believe rate cuts will only exacerbate further.

In anticipation of a shift in the Fed’s behavior, both short-term and long-term interest rates rose sharply in March, after steadily declining over the prior 12 months in response to subsiding inflation pressure.

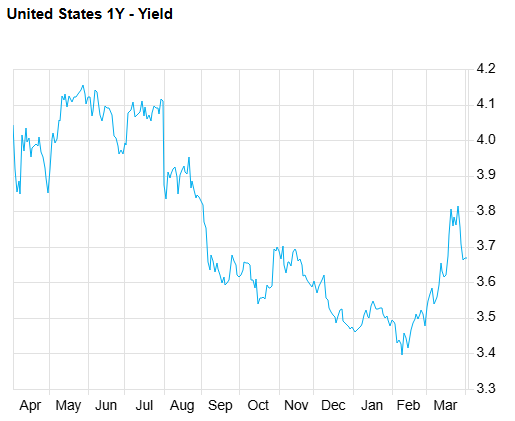

The 1-Year Treasury yield, which is a good indicator of where the bond market thinks the Fed funds rate is headed over the next year, rose approximately 0.2% in March. This is consistent with the idea that we may now see one less quarter-point rate cut this year (relative to what the market was expecting before the war began). |

|

|

| 1-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

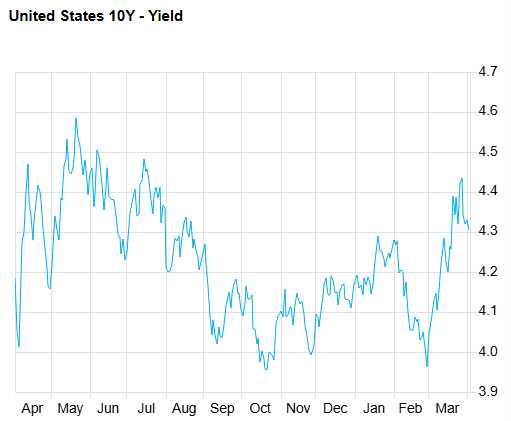

| The 10-Year Treasury yield also rose significantly, moving from approximately 4.0% at the end of February (close to its lowest level over the past year) toward 4.3% at the end of March. |

|

|

| 10-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

| All sectors suffer (except Energy)

Few businesses stand to benefit when there is a macro shift that threatens growth and at the same time leads to tighter monetary policy.

The only sector that performed well this month was, unsurprisingly, Energy. Oil and gas exploration and production stocks were particularly strong performers, as higher oil prices feeds directly into higher earnings. The Energy sector advanced 10%. |

|

|

| Defensive sectors, like Consumer Staples and Health Care, often perform well in periods of geopolitical turbulence. However, in this case, the impact on interest rates offset any perceived benefit of business stability.

When long-term interest rates rise, this can be especially damaging for defensive stocks that tend to be valued on the basis of their secure long-term cash flow potential. These stocks often trade in tandem with long-term bonds, which trade lower as interest rates rise.

At the same time, more cyclical sectors, like Industrials and Consumer Discretionary, also perform poorly in a period of heightened macroeconomic risk. Investors shunned these sectors as well in March.

Outside of Energy, there were not many places for investors to hide this month. |

|

| What comes next?

The S&P 500 drifted down steadily all month as oil prices climbed and investors grew increasingly nervous. The key question on every investor’s mind was when does the Strait of Hormuz reopen.

The index closed at its lowest level for the year on March 30, down 7% on a year to date basis. However, on the following day, the final day of the month, stocks rallied sharply in response to indications from President Trump that U.S. military engagement in the region will begin to wind down.

The situation remains highly fluid. This morning, Trump issued a not so gently worded message on social media, demanding that the Strait get reopened before Tuesday, at which point he will start targeting critical infrastructure.

Our expectation is that the Strait of Hormuz problem should be largely resolved in a matter of days or weeks, either through diplomacy or force.

Once traffic begins to flow through the Strait again, we would expect spot oil prices to subside along with some potential relief on interest rates. Risk appetite should also return to the stock market.

Given lingering uncertainty and the need for strategic stockpiling, oil prices likely will not immediately return to the historically low levels that we saw at the end of last year. But to the extent global energy flows normalize, market sentiment has the potential to improve noticeably.

Investors who view this as a short-term problem that will ultimately get sorted out are likely to be rewarded for having patience during this turbulent period. In the meantime, disturbing headlines and risk-off sentiment create opportunities for long-term investors to build positions at lower prices. |

|

| | |

The top performing stocks in the portfolio in March were Circle Internet Group (CRCL), which returned 14%, and Oracle (ORCL), which returned 1%.

The worst performing positions this month were GXO Logistics (GXO), which returned -17%, and Stryker (SYK), which returned -15%. |

|

| |

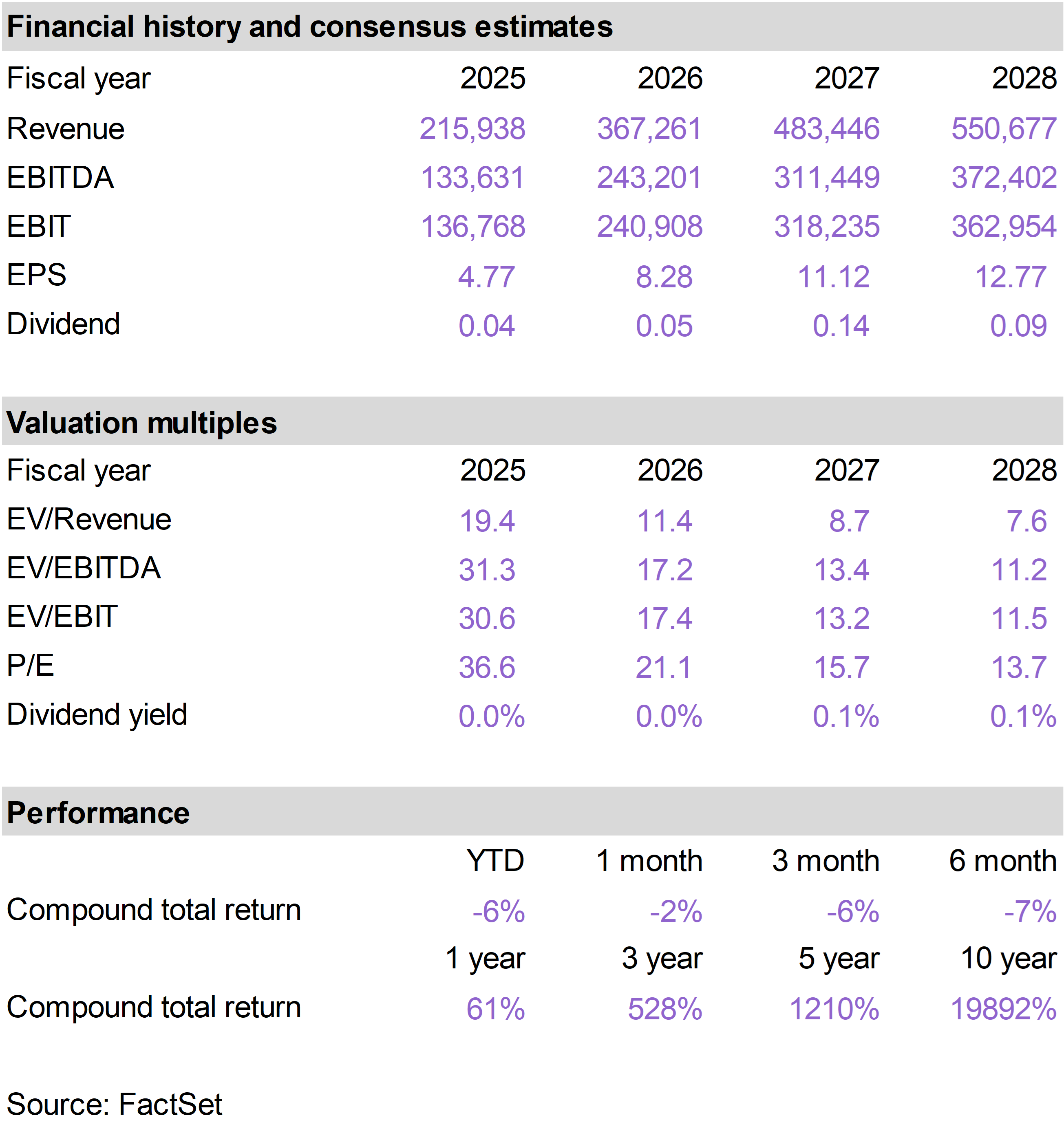

We remain highly optimistic about CRCL’s long-term prospects as the leading compliant stablecoin provider.

Its core product, USDC, continues to gain traction as stablecoins move beyond crypto trading and into the broader financial system—powering payments, settlement, and other real-world use cases.

USDC has also emerged as a leading payment technology for AI agents, which represents an extremely early but exciting growth avenue.

Although CRCL performed well this month, the stock did pull back from its highs as concerns emerged around new legislation in Washington—specifically the proposed CLARITY Act.

The CLARITY Act is part of a broader push by U.S. lawmakers to finally establish clear rules for digital assets—defining what falls under the jurisdiction of the Securities and Exchange Commission (SEC) versus the Commodities Futures Trade Commission (CFTC), and how different types of crypto products should be regulated.

Stablecoins are a key focus of this legislation, which already passed the House and now sits in the Senate. The latest controversy centers on one main issue: whether stablecoins should be allowed to offer yield.

USDC reserves are invested primarily in short-term U.S. Treasuries, which generate interest. Many crypto platforms—like Coinbase (COIN), which has a direct economic interest in USDC as well—pass a portion of that income on to users. This effectively allows people to earn a return on their USDC balances.

The concern is that once a stablecoin starts offering yield, it begins to look less like “cash” and more like a bank deposit. And the banks, apparently, are not keen to have to compete with crypto platforms for savings account deposits.

As a result, draft language tied to the CLARITY Act has apparently raised the possibility of limiting or restricting these yield-bearing features.

If platforms are no longer able to offer rewards on USDC, it could reduce one of the key incentives driving stablecoin adoption. That said, the primary use case of stablecoins is as a highly efficient medium of exchange, rather than a savings technology.

When platforms pay rewards on stablecoins like USDC, they are essentially relinquishing the vast majority of the underlying interest income to consumers. It is not highly profitable, but it enlarges the liquidity of the network and promotes adoption.

While a platform like COIN may have more to lose from being blocked from offering stablecoin rewards (it uses these rewards to attract new customers), the market may be overestimating the negative impact of such restrictions on CRCL.

If less of that interest income is shared with users and partners, more of it stays with the issuer. In other words, tighter rules could actually improve CRCL’s unit economics, while discouraging the formation of competing products.

The details of the CLARITY Act continue to be debated, and there have been indications that an acceptable compromise can be reached. Hopefully, the legislation passes this spring, which could represent a major catalyst for CRCL and the entire crypto industry. |

|

| |

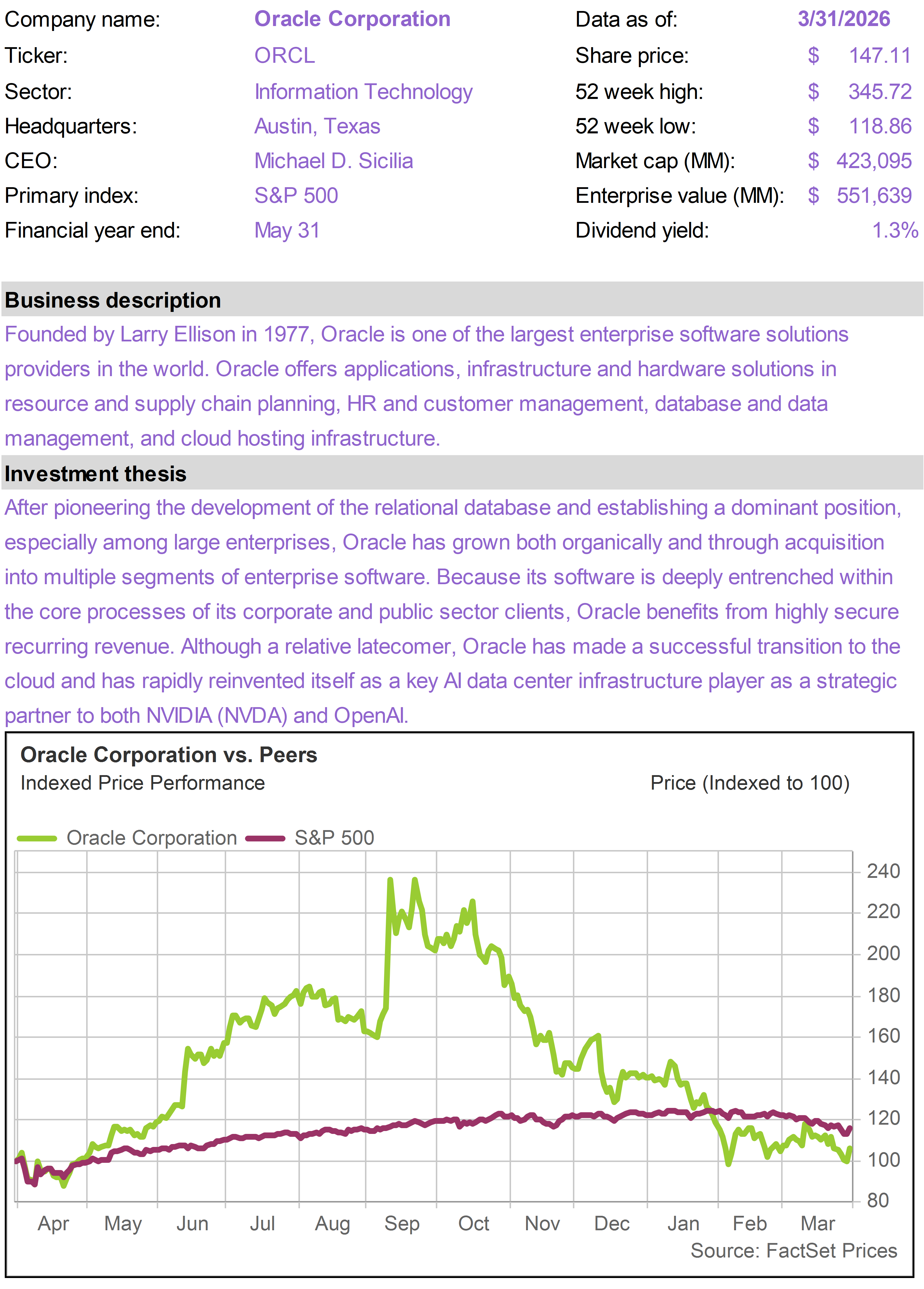

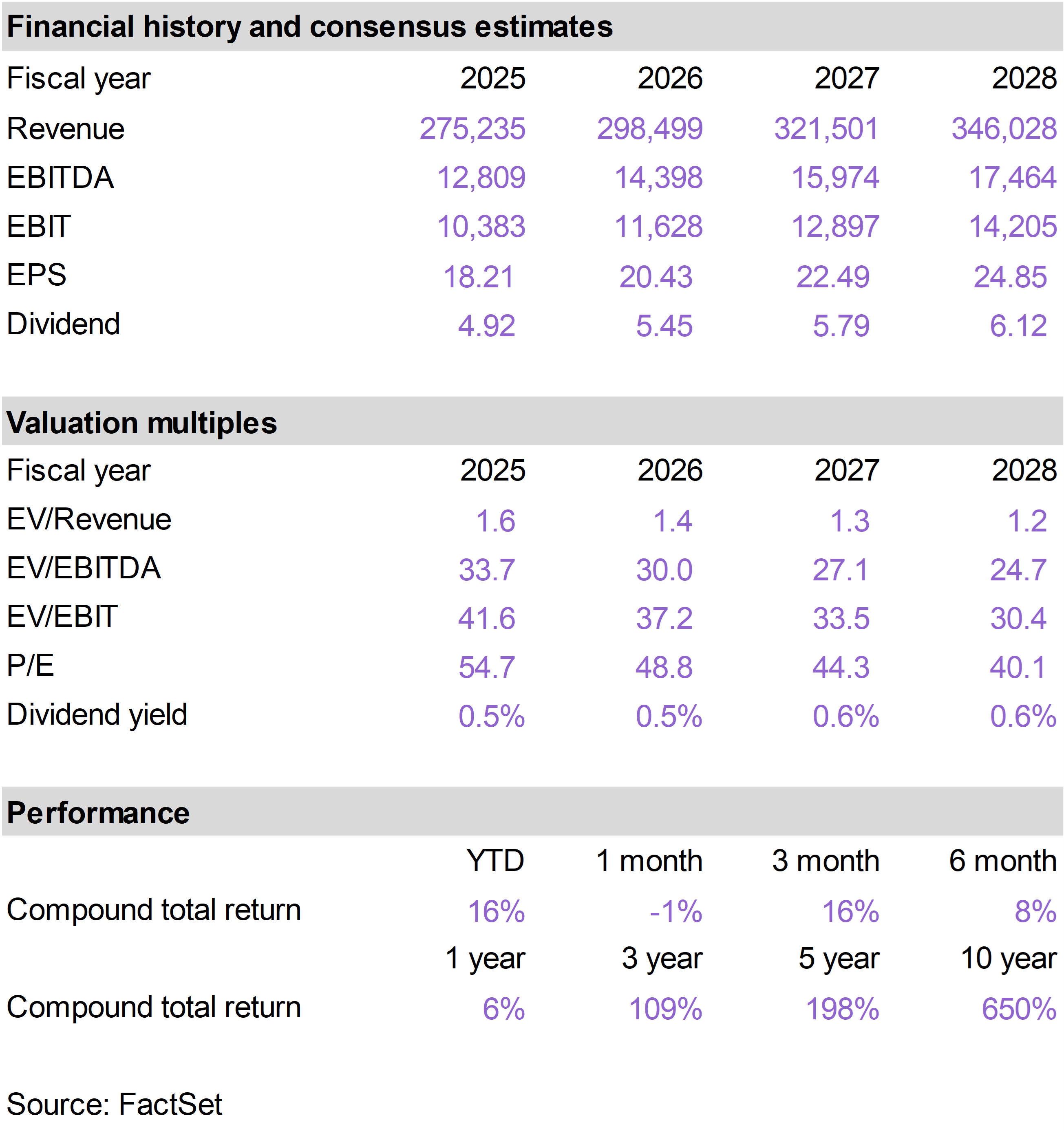

Shares of ORCL were modestly higher despite the broader market sell-off. We view this as an encouraging indication of valuation support, after the stock has suffered from negative sentiment toward both software names and AI infrastructure.

We believe ORCL’s growth strategy remains misunderstood by the market and that it now trades at compelling valuation metrics. |

|

| |

GXO shares were weak given pressure on global logistics plays, which tend to be more sensitive to energy costs and macro uncertainty.

Despite the setback, GXO remains well positioned. The company operates outsourced logistics—running warehouses and fulfillment operations for large customers—handling everything from inventory management to order processing and distribution.

Increasingly, GXO is moving into higher-value areas such as aerospace, defense, technology, and life sciences, where logistics is more complex and margins are higher. These segments remain underpenetrated and offer meaningful room for growth, particularly in the U.S. where outsourcing rates are still relatively low.

We also see GXO as an AI beneficiary. The business is investing heavily in technology, including its proprietary AI platform, which helps optimize labor, improve inventory management, and speed up warehouse ramp-ups. As this platform scales, it should enhance efficiency and create a competitive advantage versus peers.

Overall, GXO’s shift toward more complex logistics and greater use of automation positions the company for stronger growth and improved profitability over time. |

|

| | Shares of SYK were down with the pressure on health care stocks. SYK was also the victim of a widely publicized cyberattack in March. This created selling pressure, although it now appears that long-term damage to the business, if any, will be minor.

The investment thesis for SYK rests on a combination of durable medical procedure growth, strong competitive positioning, and increasing exposure to higher-value technology platforms.

SYK is leveraged to aging demographics, which drive steady demand for joint replacements, trauma care, and other mobility-restoring procedures. This creates a reliable, recurring volume base supported by implants and surgical consumables.

SYK is also interesting as a robotics play that stands to benefit immensely from advancements in “physical AI.” Its Mako robotic platform enhances surgical precision and outcomes while creating a sticky ecosystem that drives recurring revenue.

SYK also benefits from AI-driven structural shifts in healthcare toward efficiency, outpatient care, and data-driven decision-making. These trends support both higher procedure volumes and increased adoption of its integrated solutions.

Overall, SYK represents a high-quality compounder with both defensive characteristics and exposure to long-term innovation in medical technology. |

|

| | |

| | |

| | |

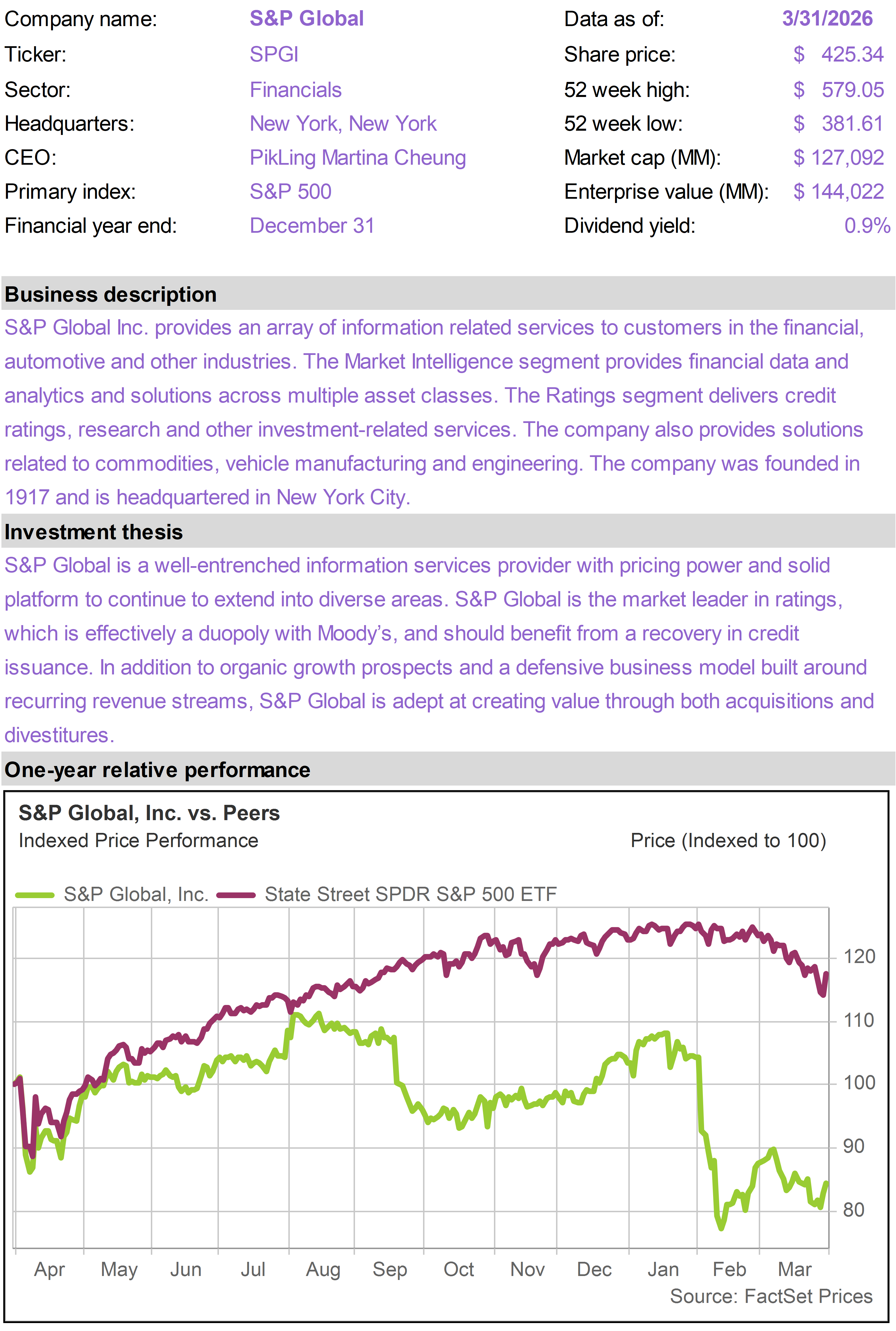

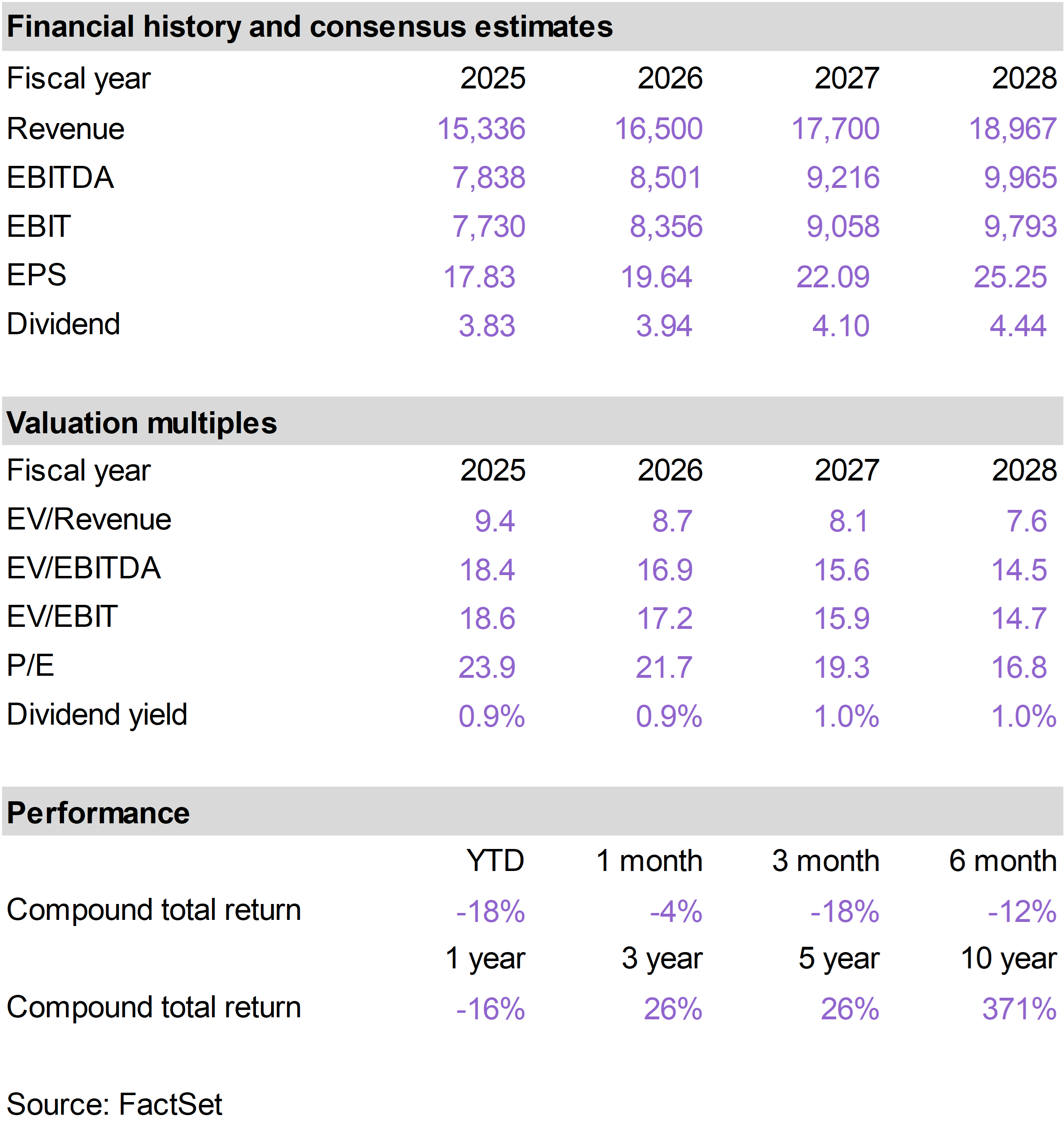

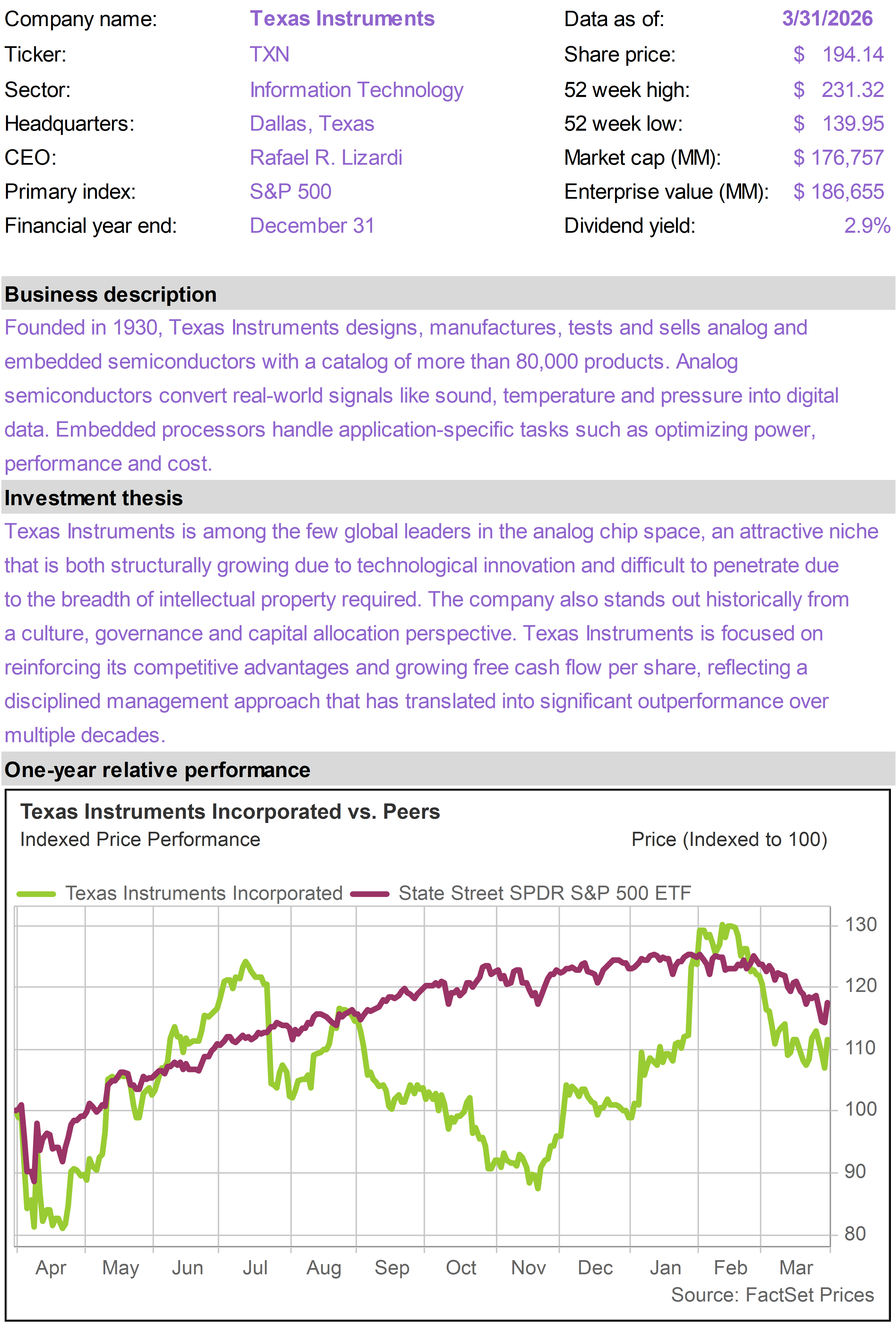

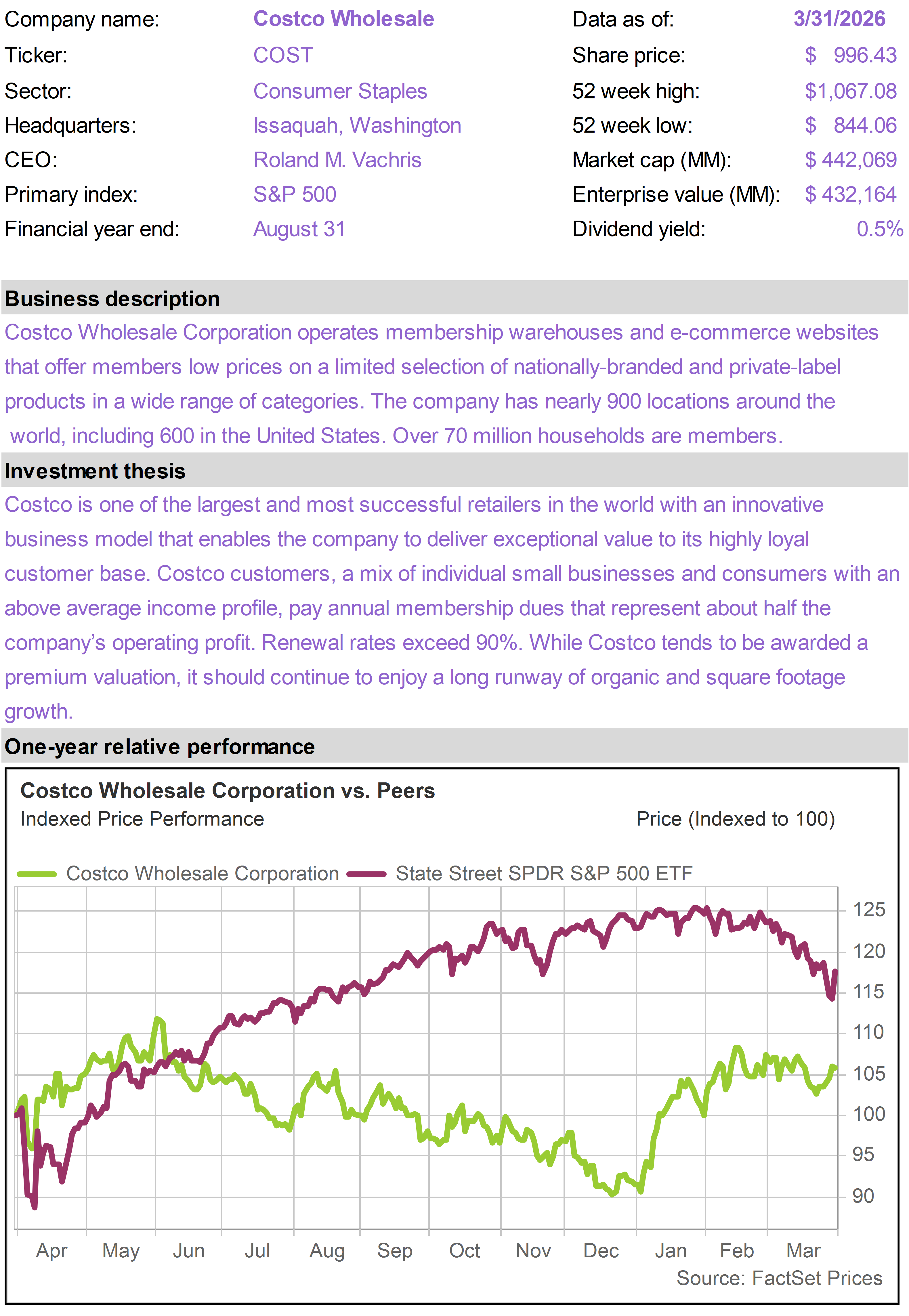

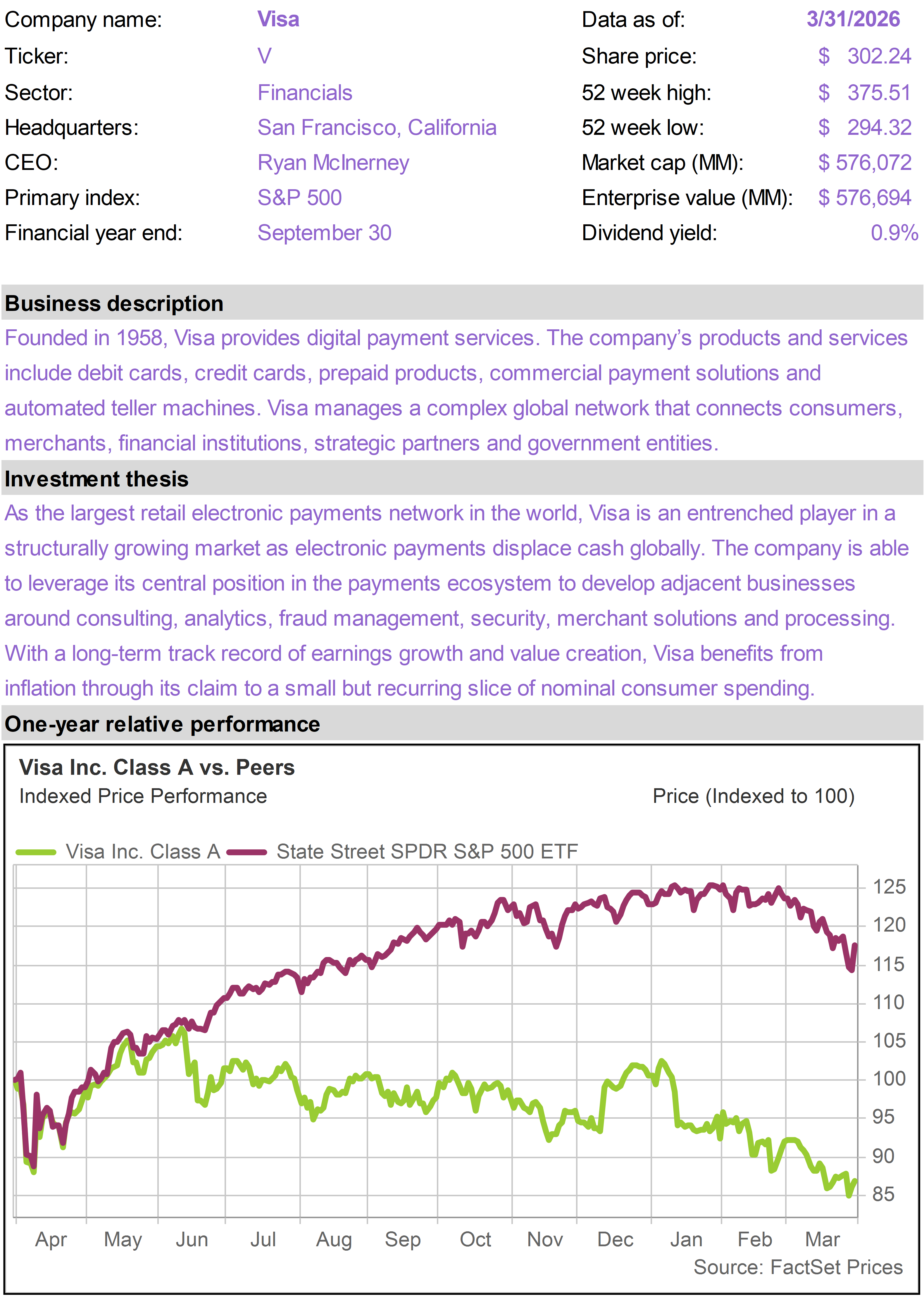

| | | Oracle Corporation (ORCL) |

|

|

|

| | |

|

| | |

|

| | |

|

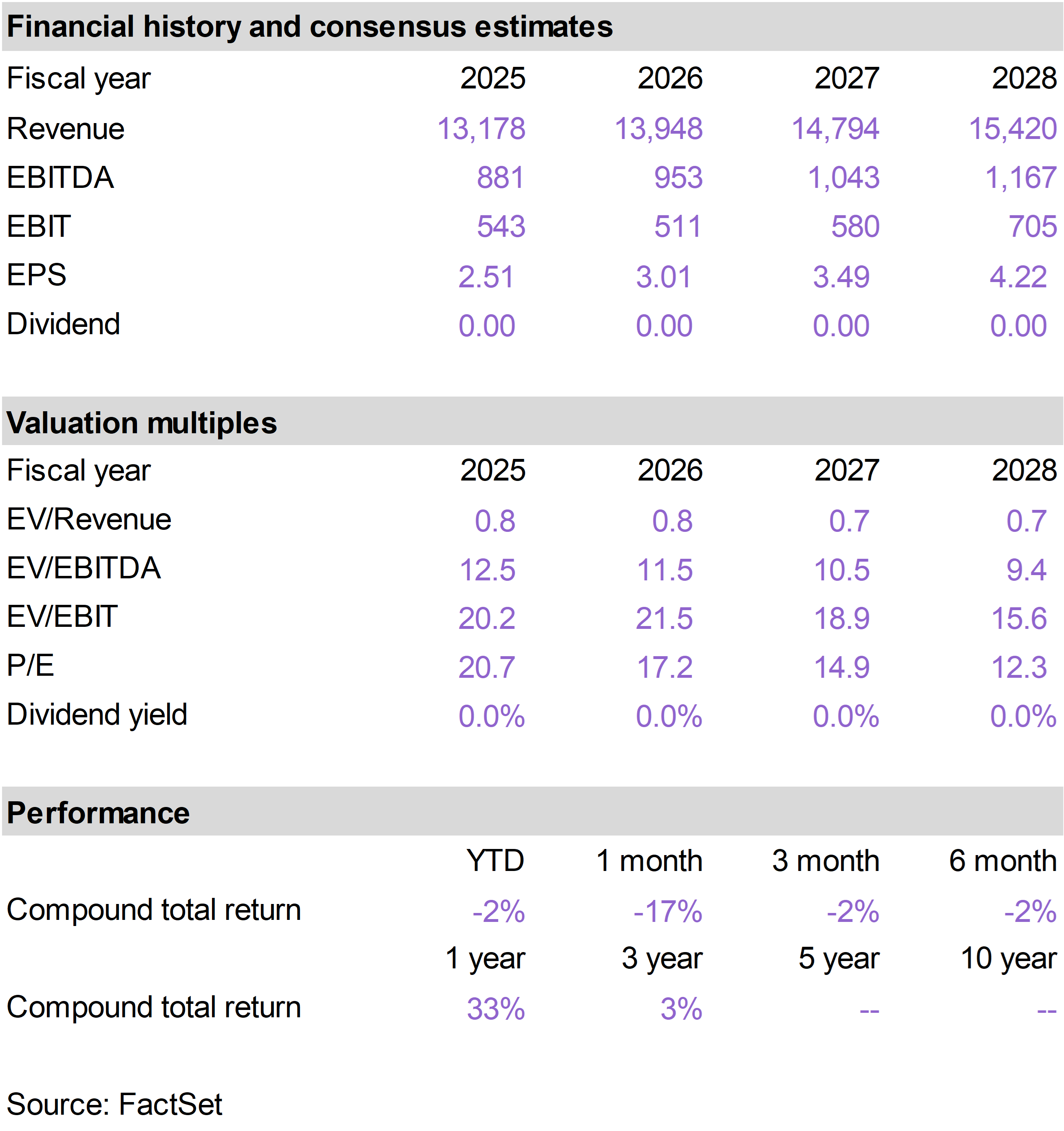

| | Arch Capital Group (ACGL) |

|

|

|

| | |

|

| | Circle Internet Group (CRCL) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

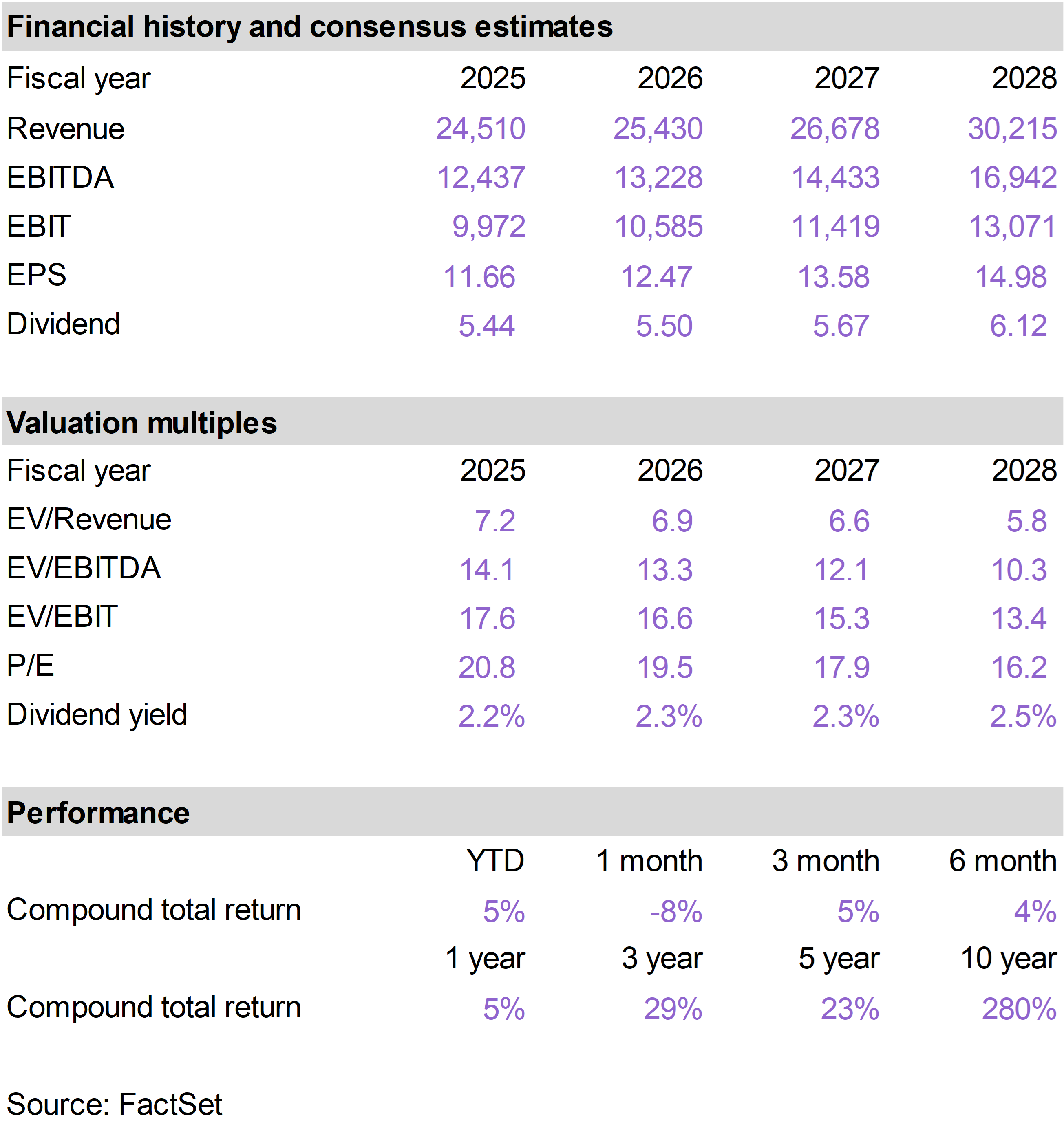

| | Thermo Fisher Scientific (TMO) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

| | The 76research American Resilience Model Portfolio is designed to provide exposure to growth businesses that operate with competitive advantages in structurally attractive markets. The objective is to identify businesses that can survive and thrive across different macroeconomic environments and whatever geopolitical crises may unfold. The holdings are intended as long-term investments to drive portfolio compounding with minimal need to realize taxable gains. Emphasis is placed on critical markers of business quality such as barriers to entry, physical scarcity of assets, balance sheet strength, effective capital allocation and durable long-term growth drivers. These assessments are paired with careful consideration of valuation and risk. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

|