| Income Builder Model Portfolio |

|

| Monthly Portfolio Review: April 2026Publication date: May 4, 2026 |

|

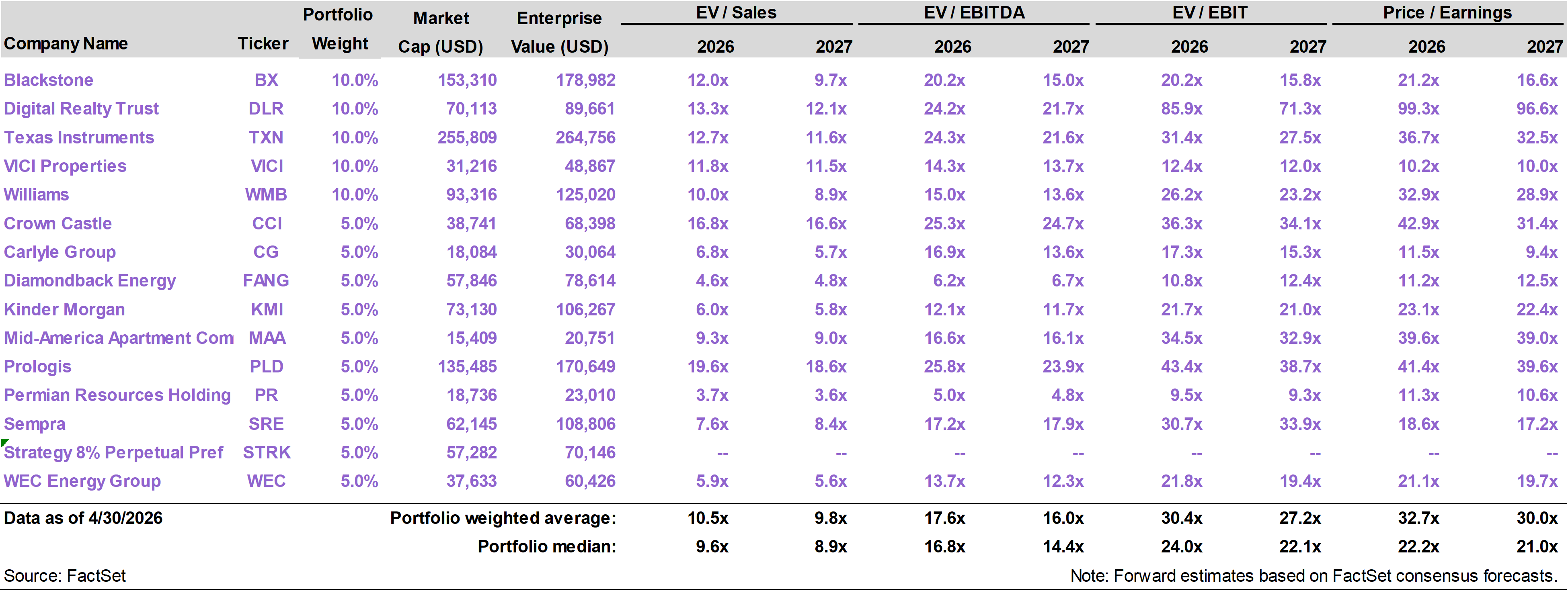

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

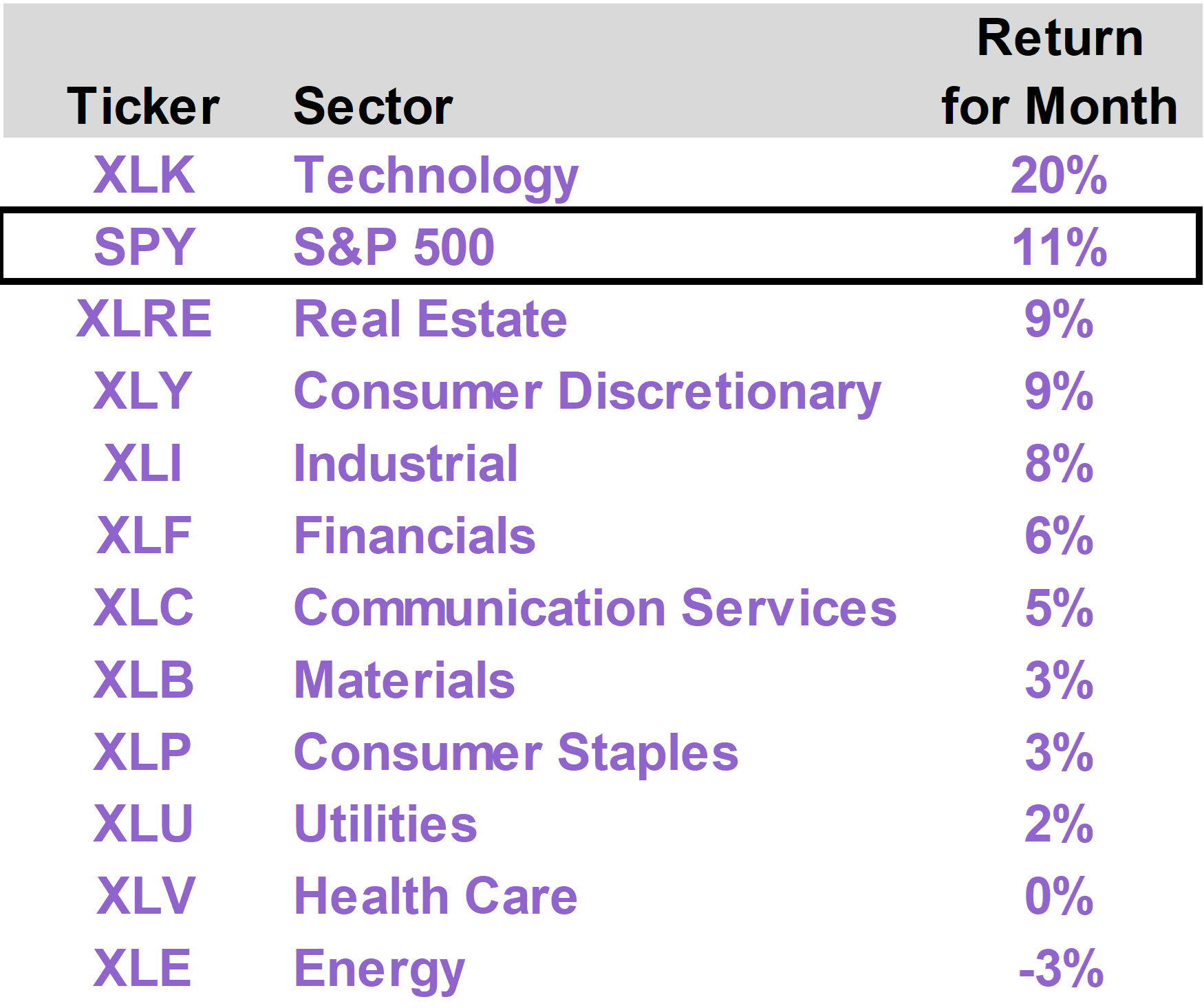

| | | A sharp rebound in the Technology sector, sparked by impressive first quarter earnings reports, sent stock indexes to new highs in April. Meanwhile, investors grew more confident that the situation in Iran would ultimately find a favorable resolution. The S&P 500 advanced 10.5%, as tech stocks advanced 20%. Energy lagged the market, delivering modestly negative performance. The Income Builder portfolio generated a total return of 9.8% in April. On a year to date basis, the portfolio has returned 17.0%, versus 5.7% for the S&P 500. The top performing position in the portfolio was Texas Instruments (TXN), which gained 45% after blowout first quarter earnings demonstrated surprisingly strong AI data center demand. Portfolio detractors included several names in underperforming sectors, but losses were modest. With the Iran crisis receding, we see a solid foundation emerging for sustained earnings growth across a wide range of industries.

|

|

| | |

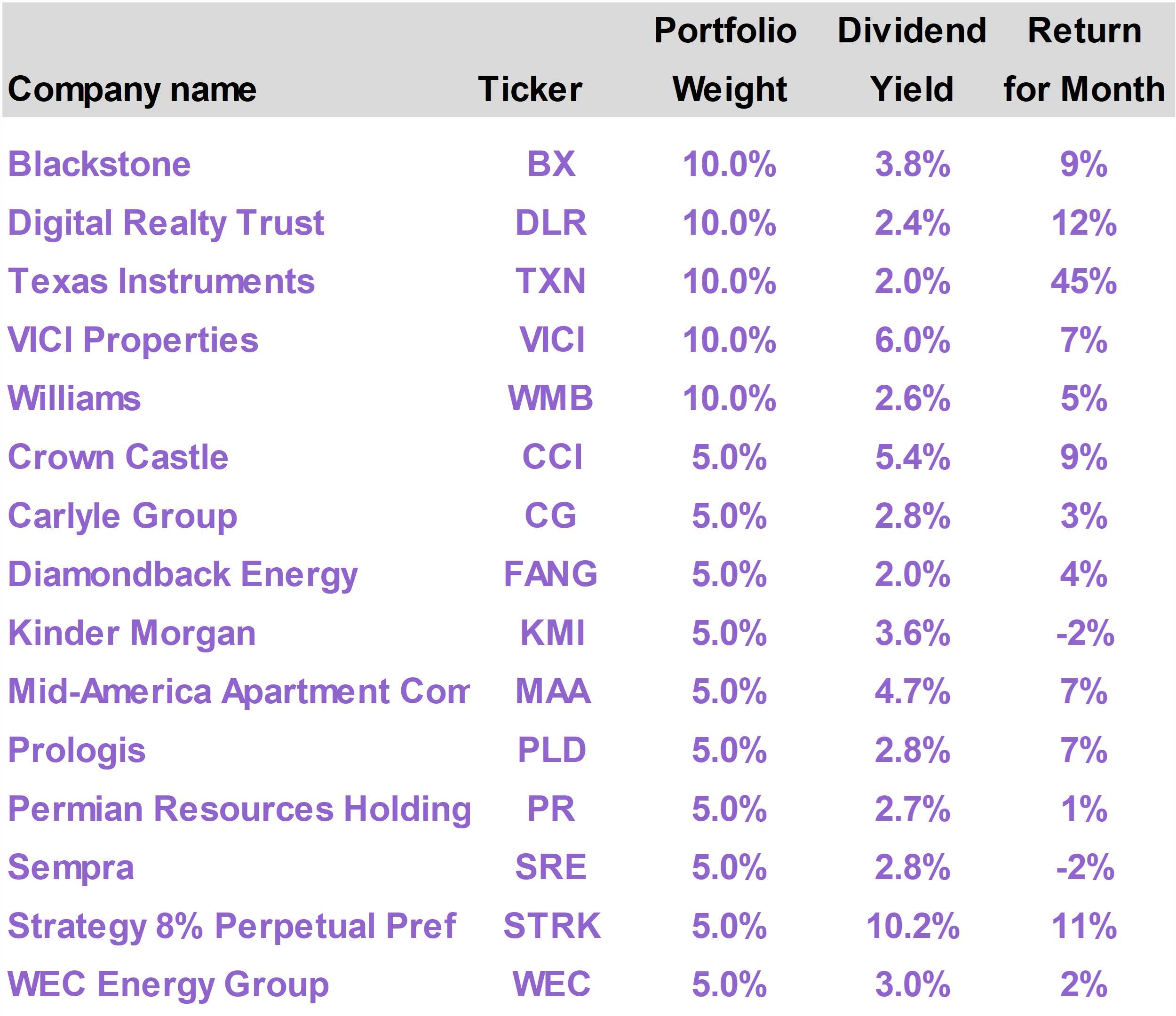

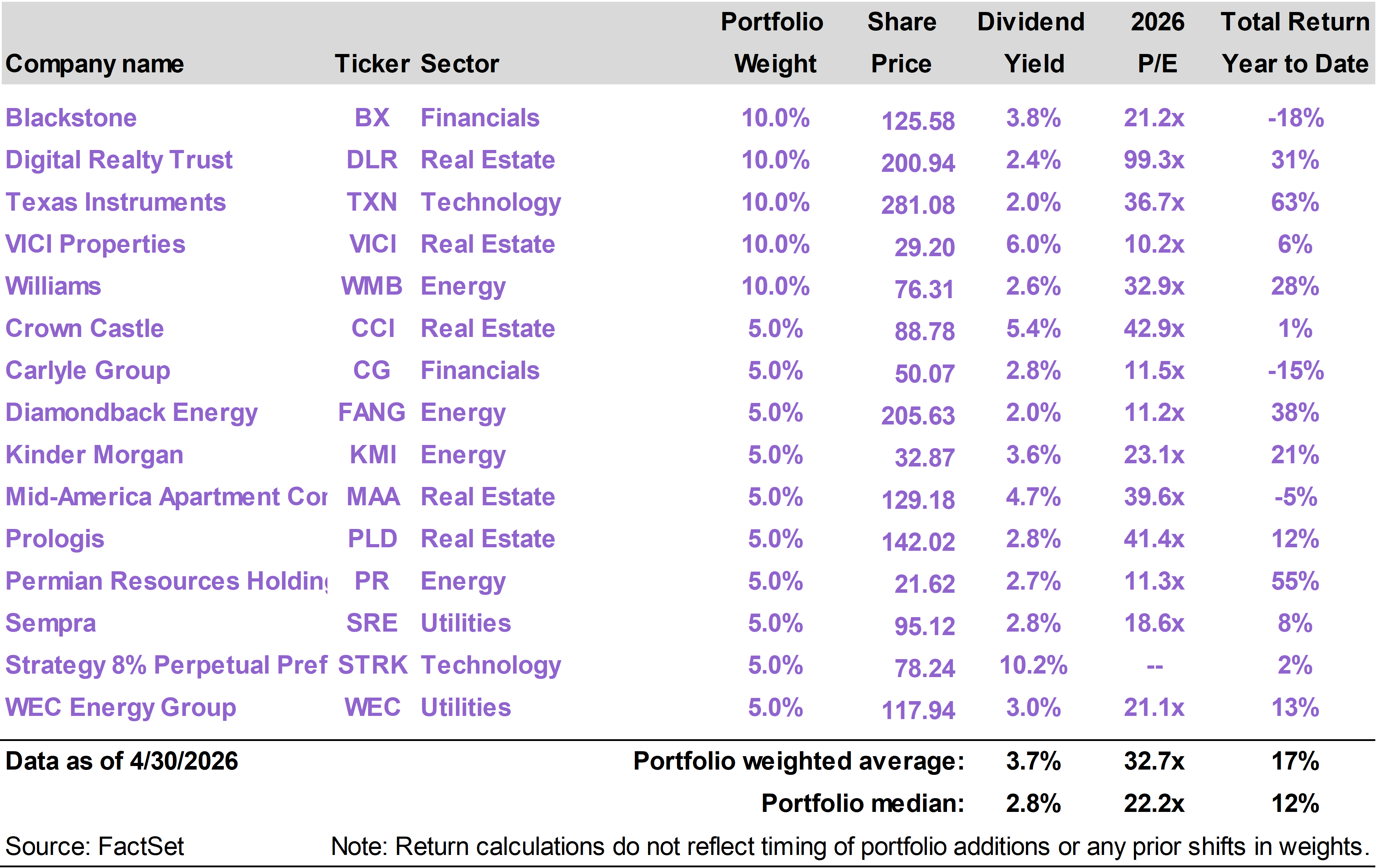

The Income Builder portfolio generated a total return of 9.8% in April, versus the S&P 500 Index return of 10.5%. On a year to date basis through the end of the month, the portfolio has returned 17.0%, substantially outpacing the 5.7% return of the S&P 500.

The top performing positions in the portfolio in April were Texas Instruments (TXN), which returned 45%; Digital Realty Trust (DLR), which returned 12%; and Strategy 8% Perpetual Preferred (STRK), which returned 11%.

The worst performing positions in the portfolio this month were Kinder Morgan (KMI), which returned -2%; Sempra (SRE), which returned -2%; and WEC Energy Group, which returned 2%. |

|

|

Stocks come back

We concluded last month’s portfolio review with the view that investors would ultimately be rewarded for pushing through the March volatility—and that the sell-off had created an opportunity to build positions at more attractive levels.

That view was quickly validated. Stocks rallied sharply in April as the U.S. demonstrated progress in Iran, even as the situation in the Strait of Hormuz remained unresolved.

Oil prices stayed elevated, but markets began to look through the disruption, increasingly focused on the likelihood that the worst-case outcomes would be avoided.

At the same time, strong economic data and a solid earnings season helped shift attention back to the fundamentals underpinning the market.

Tech leads the way

The rebound was led decisively by technology.

The S&P 500 rose 10.5% in April, while the tech-heavy NASDAQ Composite surged 15.3%. Beneath the surface, the leadership was even more concentrated, with the Technology sector advancing roughly 20% for the month.

Investor sentiment pivoted quickly—from concern over energy disruptions to renewed enthusiasm around corporate earnings, particularly those tied to AI spending.

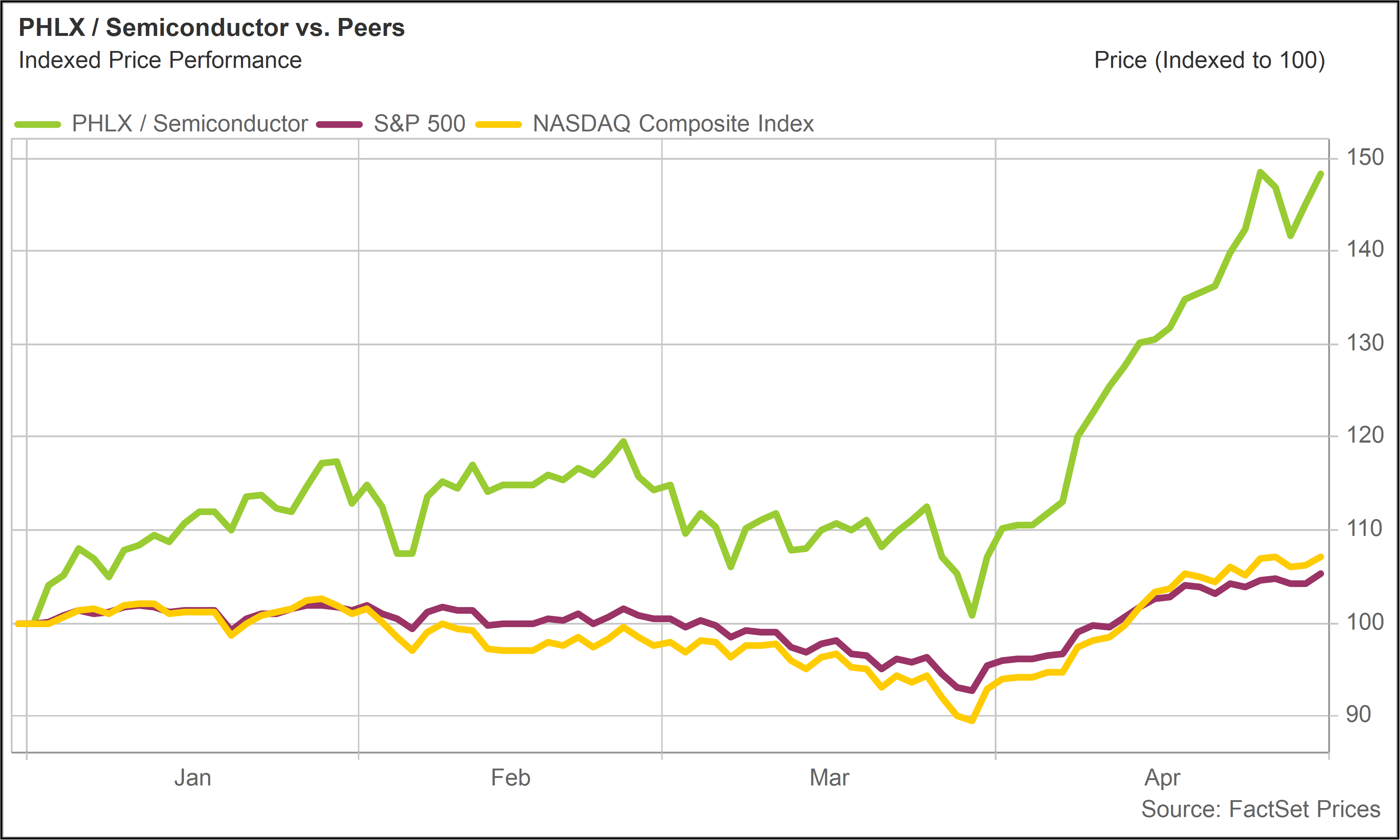

Semiconductors were a clear standout. The PHLX Semiconductor Index (SOX) climbed 38% in April, as a wave of strong first quarter results and optimistic outlooks drove the group higher.

The move capped an already powerful start to the year, with the index now up nearly 50%—far outpacing the broader market. |

|

|

|

SOX vs. S&P 500, NASDAQ(Total Return - Year to Date) |

|

|

Insatiable demand

Semiconductors are benefiting from a surge in demand for AI compute that continues to exceed expectations.

What once looked like a speculative buildout is now translating into real, measurable revenue growth across nearly every company tied to the ecosystem.

AI data centers sit at the center of this shift. They rely on a wide range of chips to generate the massive volumes of “tokens”—the fundamental units of AI output—that businesses and consumers increasingly rely on.

Not long ago, investors questioned whether AI had the makings of a bubble. As hyperscalers poured capital into infrastructure, there were real concerns about who would ultimately consume the output and whether meaningful use cases would materialize.

Those questions are now being answered.

Companies like Alphabet (GOOGL), Microsoft (MSFT), and Amazon (AMZN) are reporting AI-related growth in the 30%–60% range, providing clear evidence that demand is not only real, but accelerating.

The nature of that demand is also evolving.

In the early stages, most AI compute was dedicated to training models—feeding them vast datasets so they could learn patterns and improve performance. Increasingly, however, demand is shifting toward inference, where those models are deployed to solve real-world problems at scale.

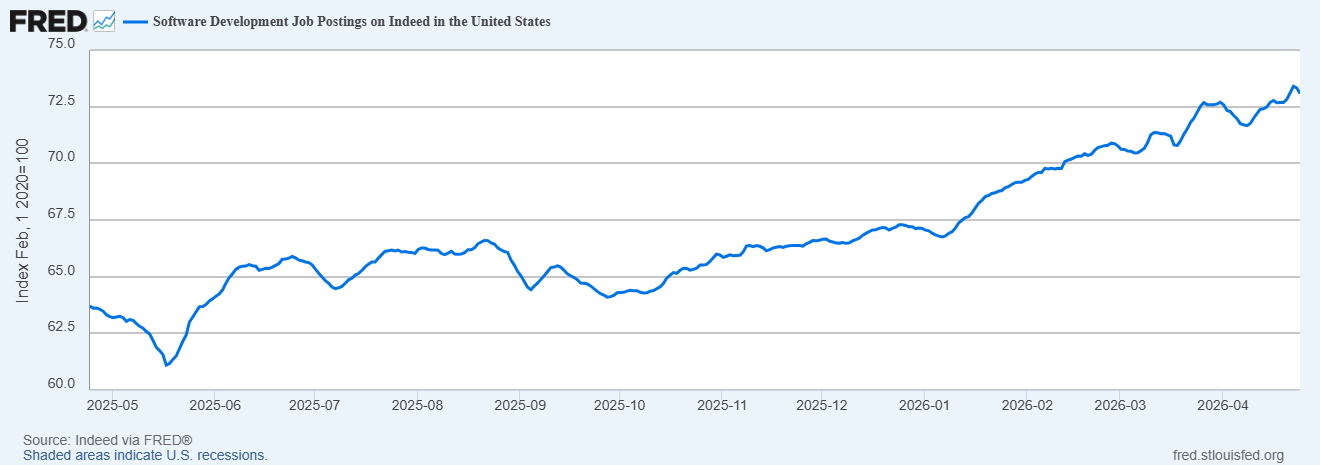

One of the most important drivers has been AI-assisted coding. Software development is being transformed, with engineers now leveraging AI tools to write and refine code—unlocking significant productivity gains.

That shift is beginning to ripple across the broader economy.

Enterprises are investing heavily in AI services because they are seeing tangible returns, using these tools to amplify the output of their workforce. Despite persistent concerns about job displacement, initial jobless claims recently fell to multi-decade lows—suggesting that the near-term impact of AI may be more additive than disruptive.

At a more granular level, demand for software talent remains strong. Job postings for developers continue to grow even as AI automates portions of the work, reinforcing the idea that productivity-enhancing technologies can expand, rather than contract, opportunity. |

|

|

|

Software Development Job Postings(Last 12 Months) |

|

|

An AI-powered economy

Technology stocks dominated performance in April, to the point that the sector was the primary driver of gains in the broader market. But strength was not limited to tech alone.

As markets increasingly looked through Iran-related risks, several other sectors also moved higher. Part of this reflected a reversal of March’s risk aversion, but it was also supported by improving earnings trends across the economy.

Across industries, companies with exposure to AI—whether through adoption, infrastructure, or productivity gains—tended to outperform their peers. What began as a technology story is increasingly becoming an economy-wide driver of growth. |

|

|

|

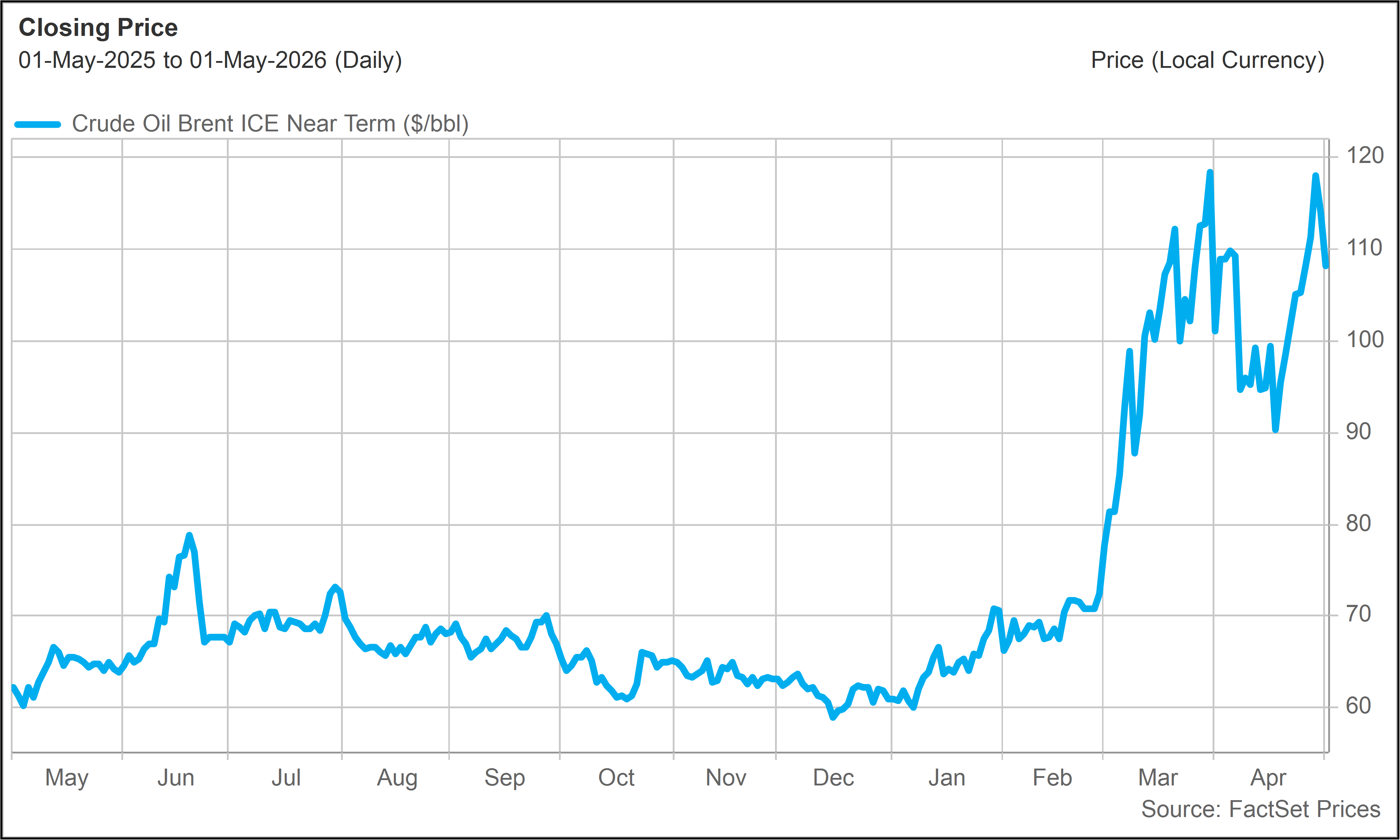

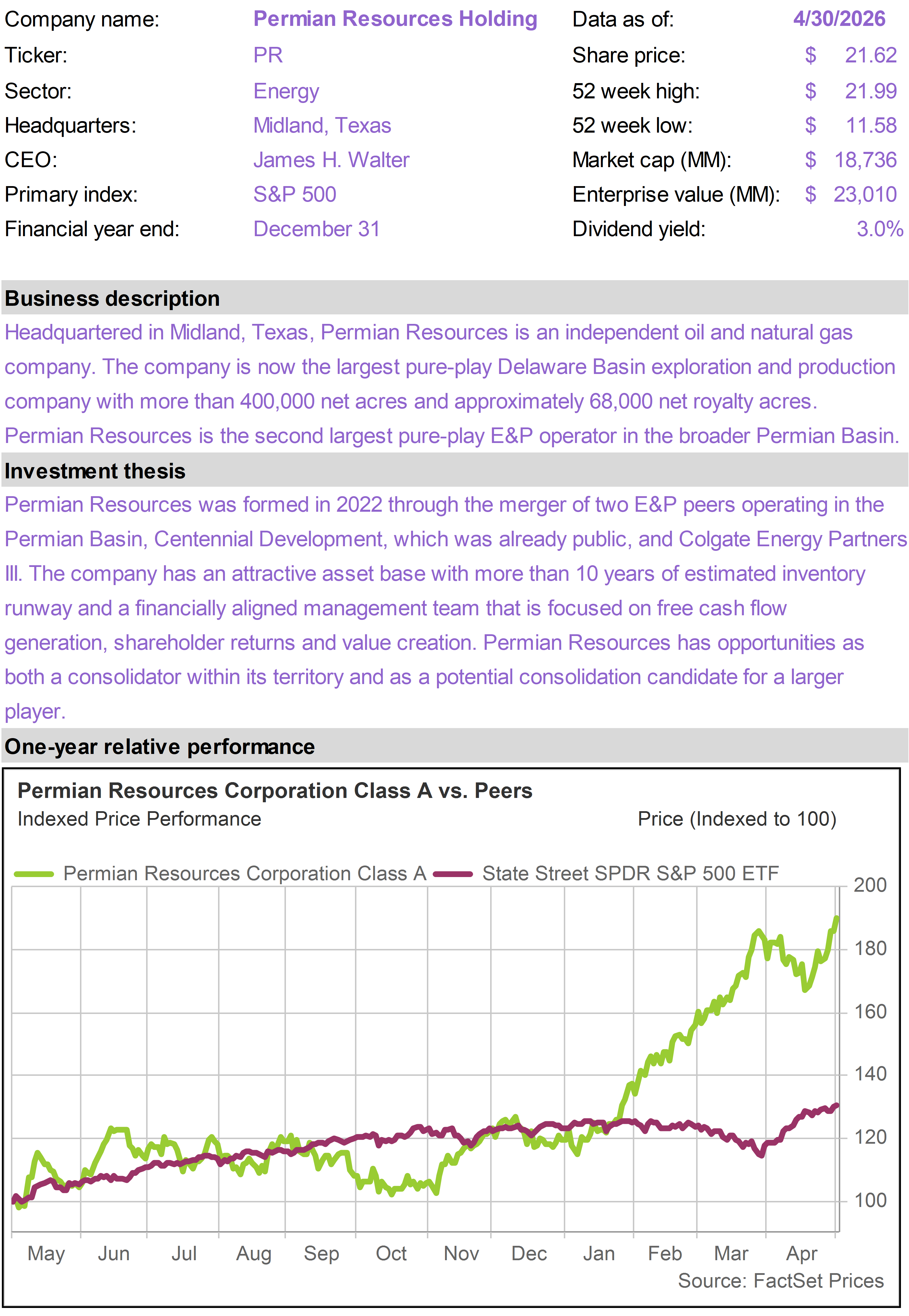

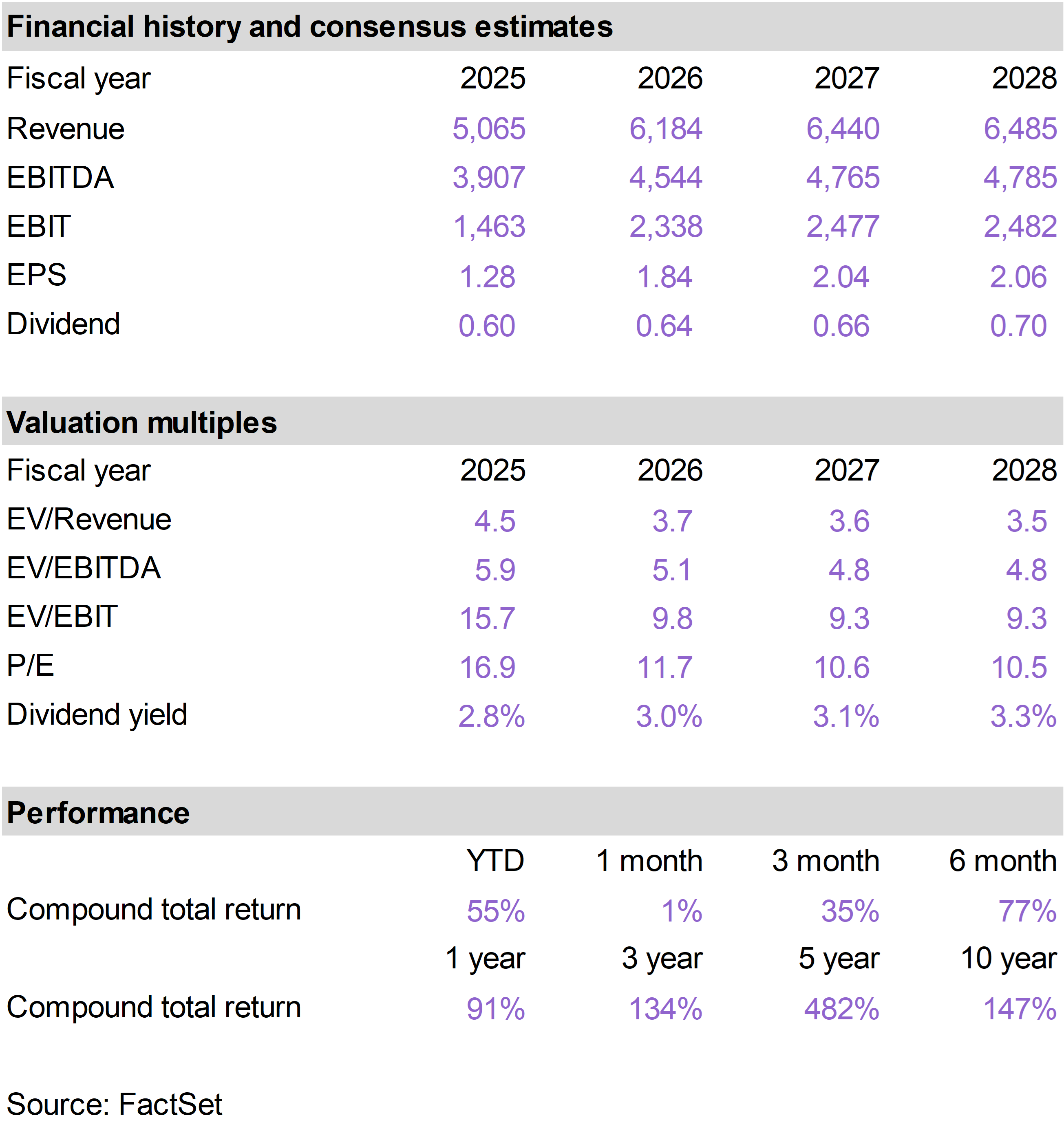

Energy holds

After leading the market in March with a 10% gain, the Energy sector lagged in April. The sector was the only one to post a negative return, declining roughly 3%.

The pullback came as investor perceptions of the Iran crisis improved. While oil prices remained elevated—at times exceeding $120 per barrel amid supply disruptions—markets became less focused on worst-case scenarios involving prolonged shortages or sustained price spikes.

Even so, energy equities held up relatively well given the move in sentiment.

Looking ahead, we expect oil markets to gradually normalize as supply from the Persian Gulf recovers, though that process may take time. Historically, supply shocks tend to catalyze new investment and capacity expansion, often leading to structural shifts in the market.

Recent developments reinforce that dynamic. The UAE’s decision to exit OPEC, as we recently discussed (Did Trump Break OPEC?), raises the possibility of further fragmentation within the cartel. Venezuela could be next.

Despite near-term volatility, the outlook for many energy companies remains constructive. Global inventories have been drawn down, and governments are likely to use any pullback in prices to rebuild reserves.

At the same time, we expect increased investment in energy infrastructure—both in the United States and globally—as policymakers prioritize resilience and supply security.

From a portfolio perspective, recent months have underscored the value of energy exposure as a geopolitical hedge.

Sentiment toward the sector was subdued entering 2026, but the Iran conflict has served as a reminder of its strategic importance. With spot prices still elevated, producers are likely to benefit from a period of strong cash flow generation in the near term. |

|

|

|

Brent Crude Oil($/barrel - Last 12 Months) |

|

|

A divided Fed

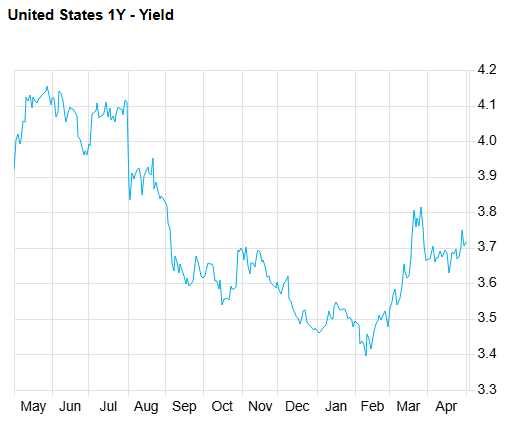

April also brought increased focus on the future leadership of the Federal Reserve.

Following the apparent resolution of the investigation into Jerome Powell, the path now appears clearer for Kevin Warsh to assume the role of Chair after his confirmation process moves forward.

For now, however, Powell has stated that he has no immediate intention of stepping down from the Board of Governors—a stance that departs from typical precedent and adds uncertainty to the policy outlook.

At the same time, divisions within the Fed are becoming more visible.

A number of policymakers have signaled reluctance to move toward further rate cuts, pitting themselves against Warsh, Stephen Miran, and others who have argued that easier policy is needed to support investment, particularly as the economy enters what could be an AI-driven productivity cycle.

Markets began to reflect this tension in April. Both short- and long-term interest rates drifted higher, as expectations for near-term rate cuts diminished.

Elevated oil prices, combined with resilient economic data—including the stronger-than-expected jobs report—reinforced the view that the Fed may be less inclined to ease policy in the near term. |

|

|

|

1-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

|

|

10-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

|

But with Warsh likely to assume the Chair role in mid-May, and with oil markets expected to normalize in the months ahead—easing inflation pressures—we could begin to see a gradual decline in interest rates, which would provide a supportive backdrop for equities.

Back on track

The Iran “excursion,” as Trump described it, is beginning to fade from the forefront as investor attention shifts back to the AI growth narrative.

While some investors remain uneasy about the valuation implications of aggressive capital spending by the hyperscalers, the impact of that spending—now widely expected to exceed $1 trillion by 2027—is increasingly visible across the economy.

Those investments are flowing through the system, benefiting downstream technology segments like semiconductors and extending into a broad range of industries tied to the buildout of AI infrastructure.

There are still crosscurrents. Kevin Warsh may face resistance within the Fed, and policy uncertainty remains a factor.

But with the Iran crisis receding, energy markets likely to stabilize, and AI beginning to deliver tangible economic gains, the broader picture is becoming clearer.

The stock market is moving back onto a stronger foundation. |

|

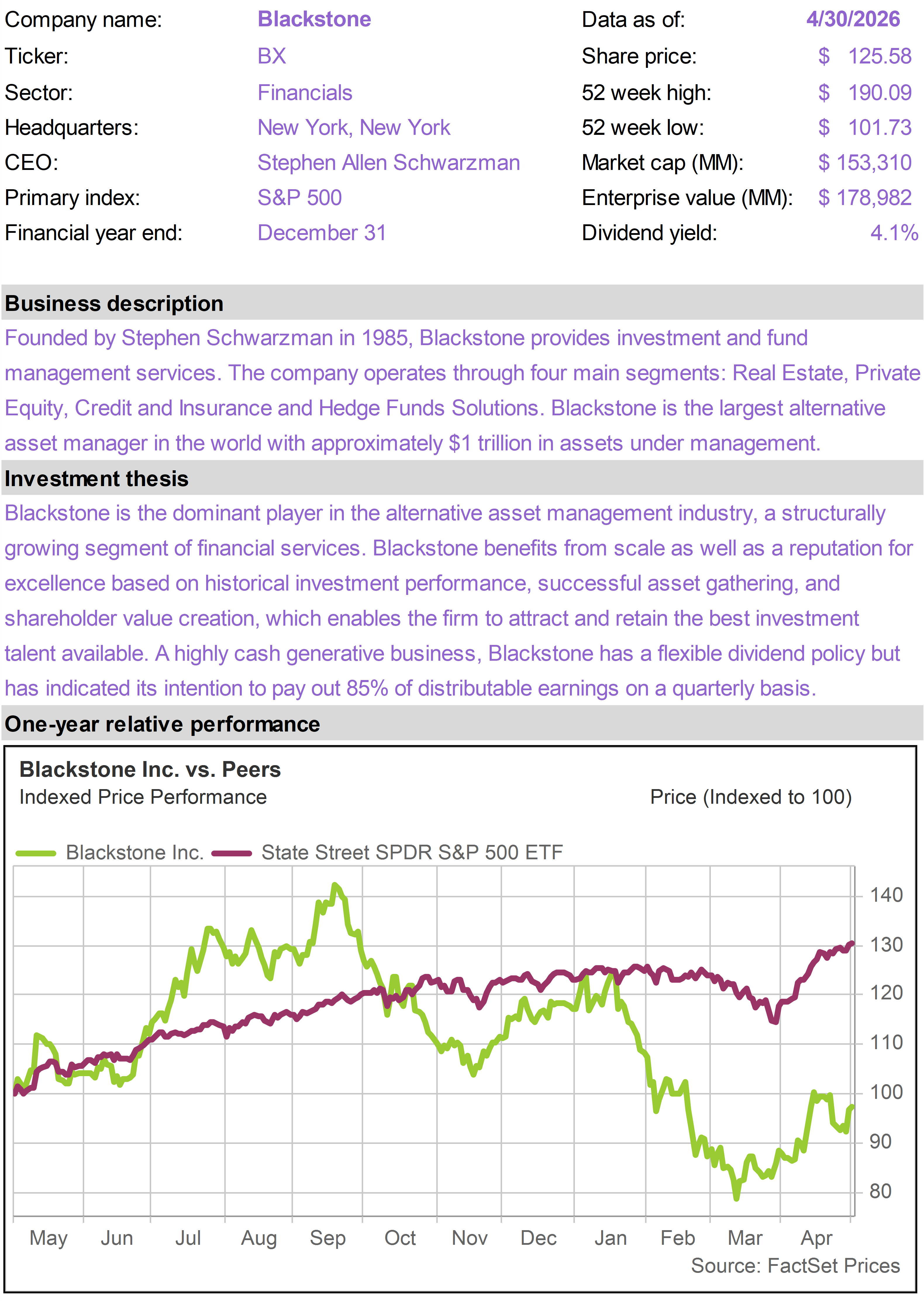

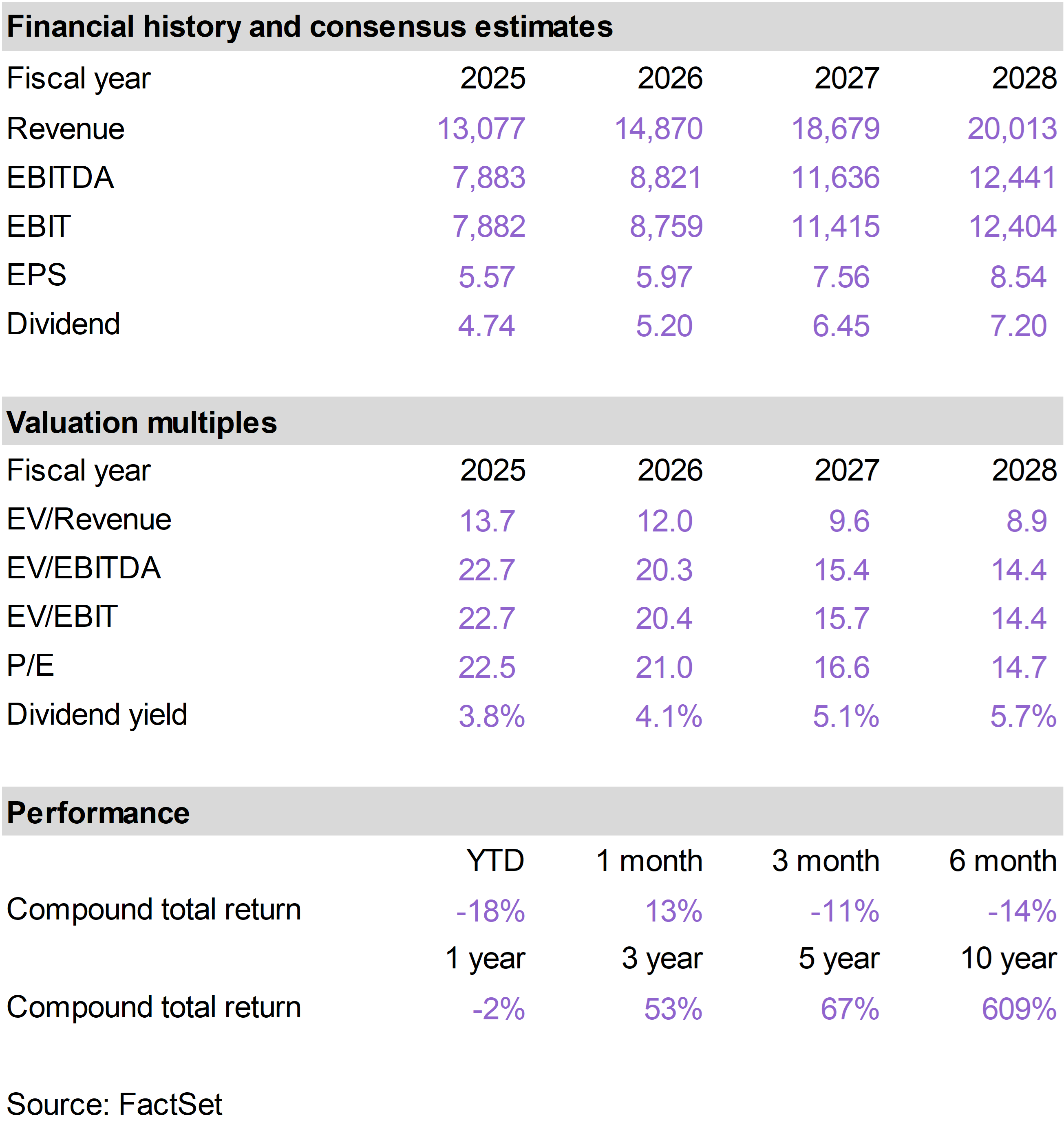

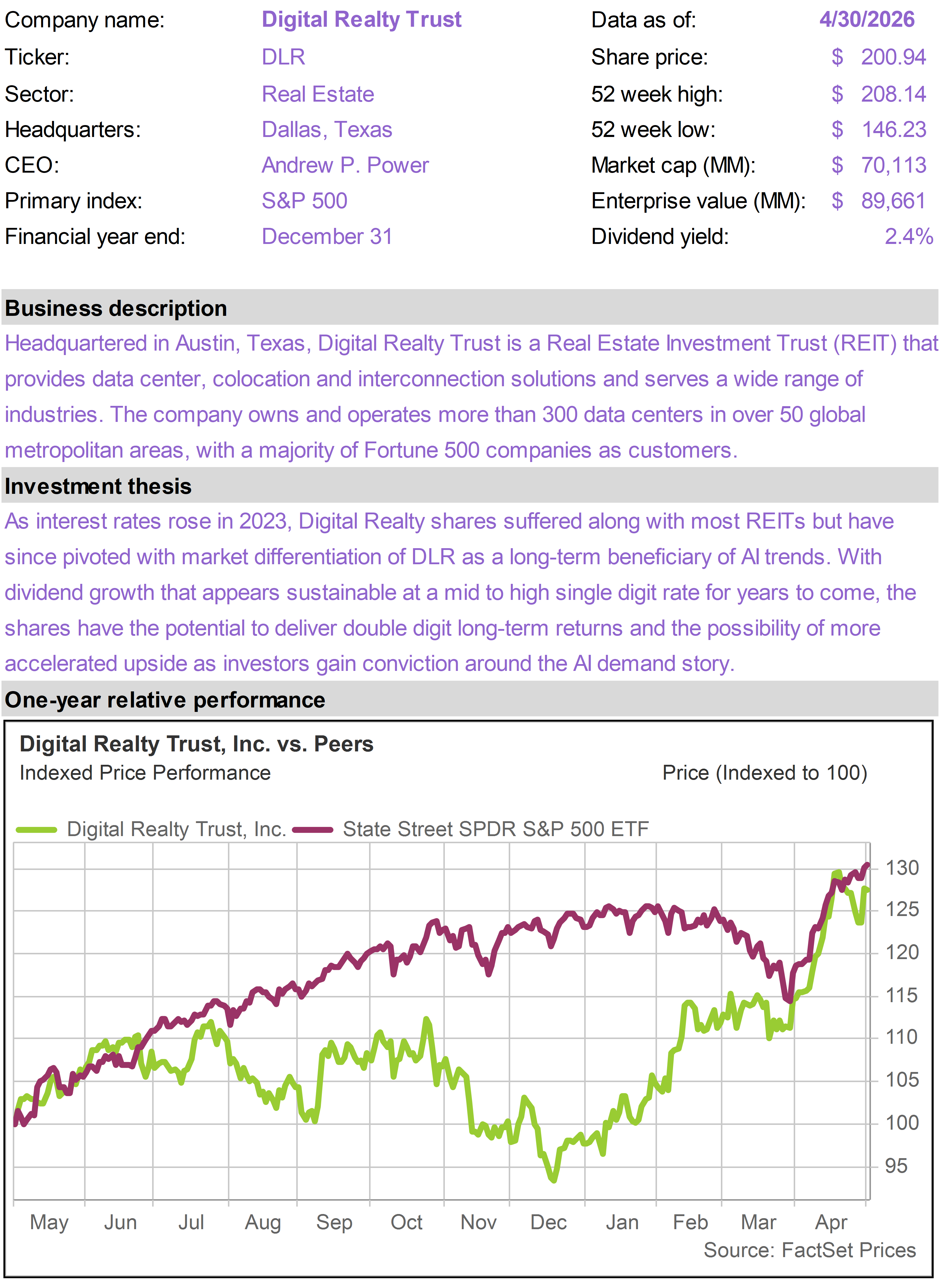

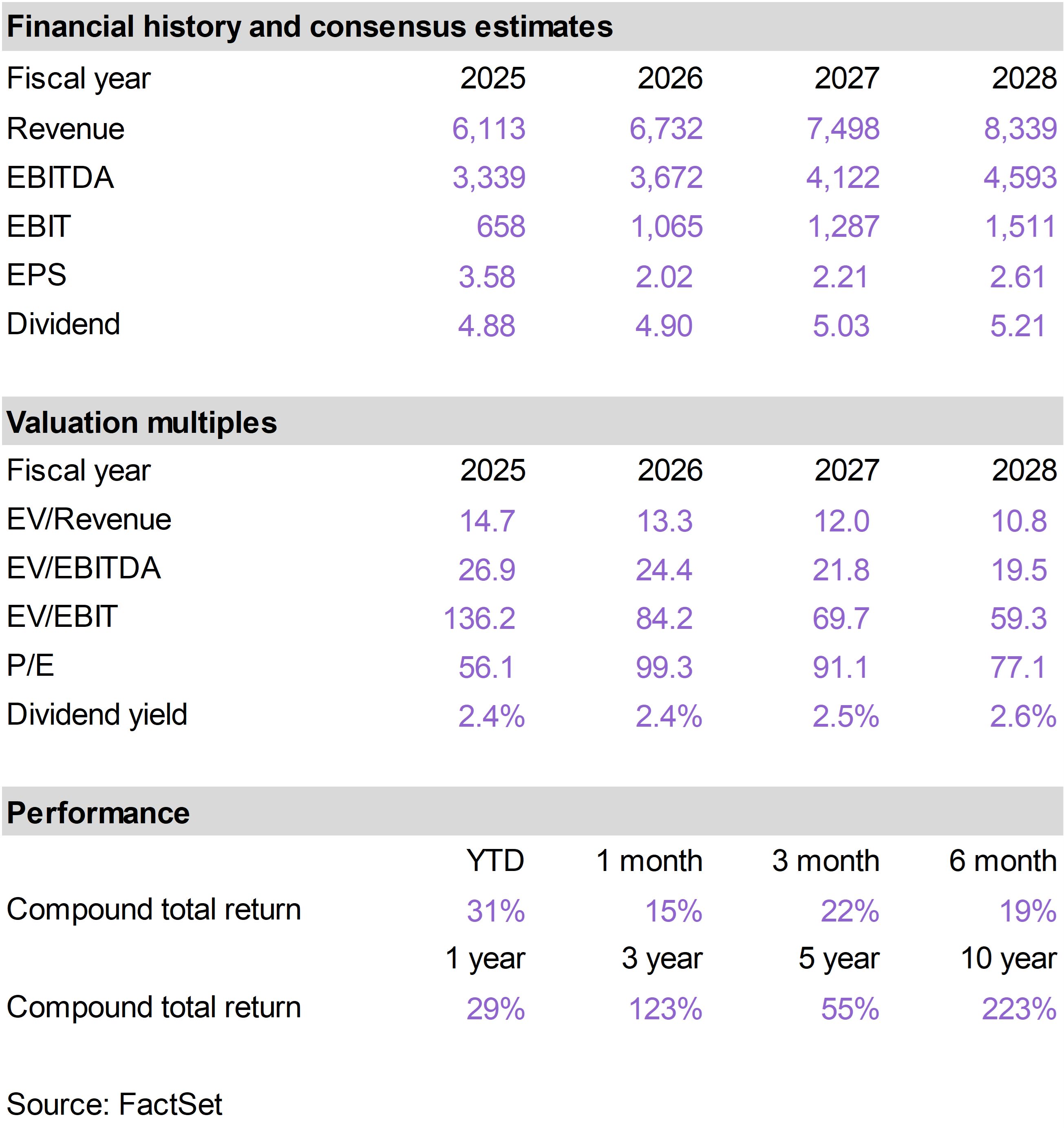

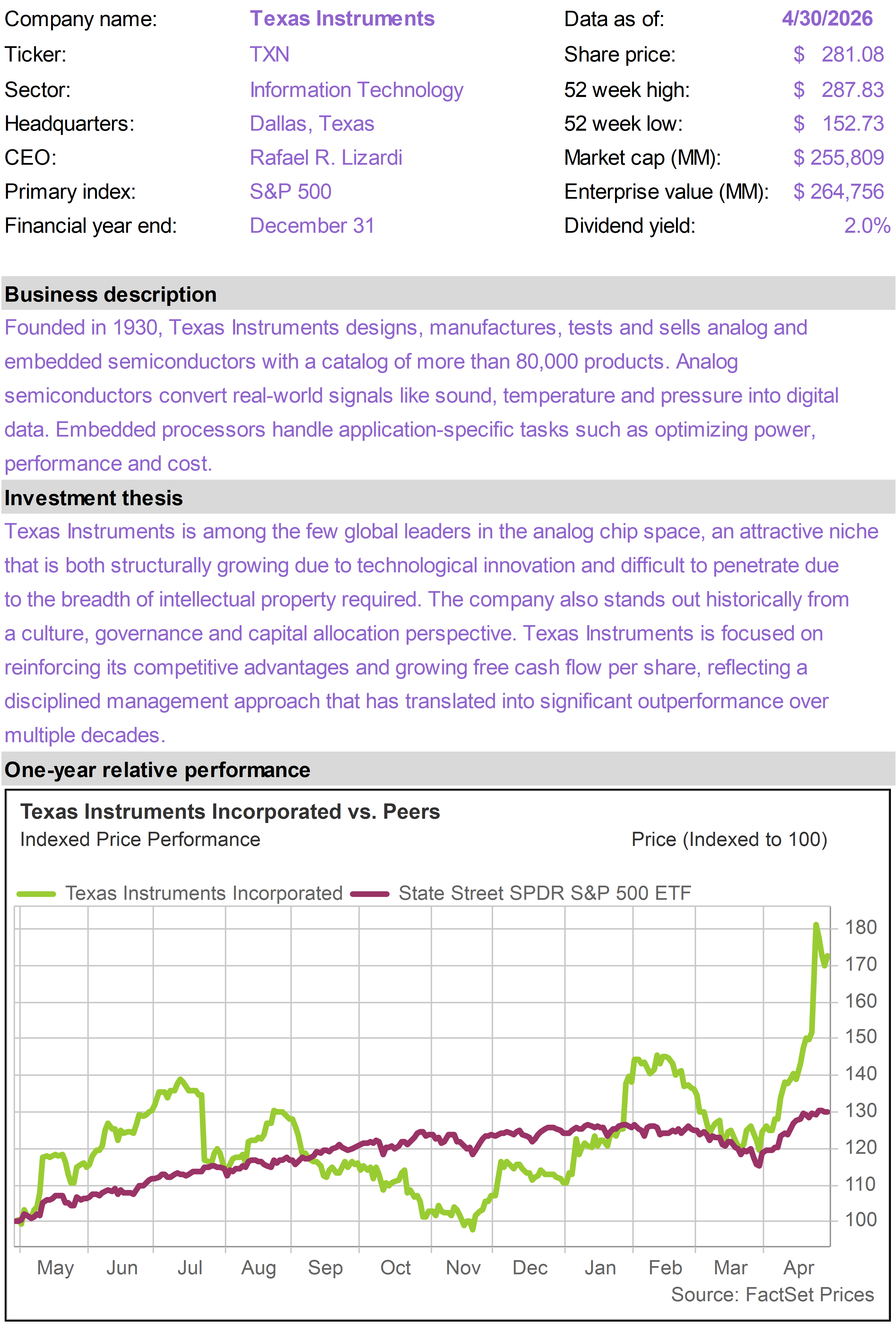

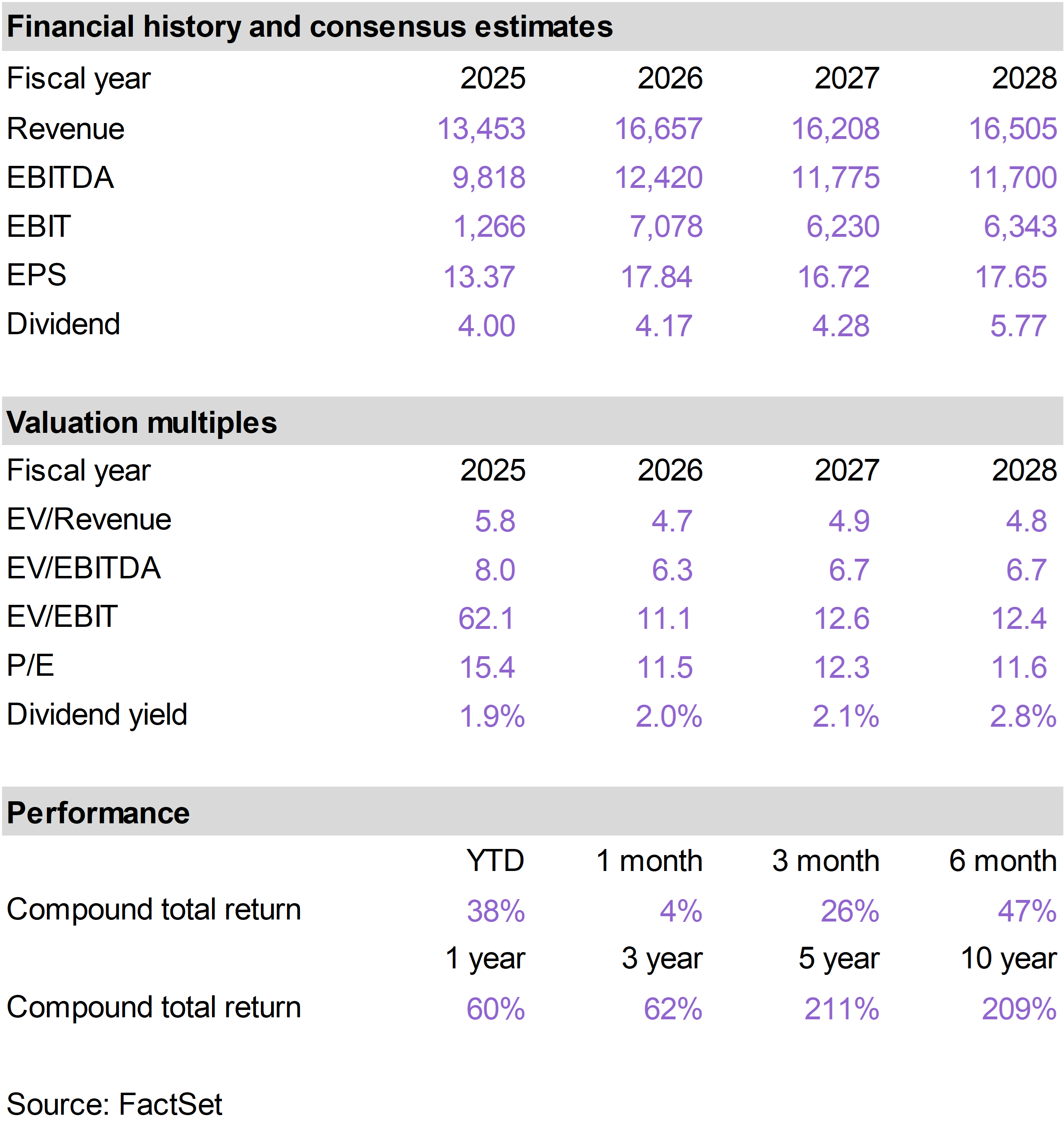

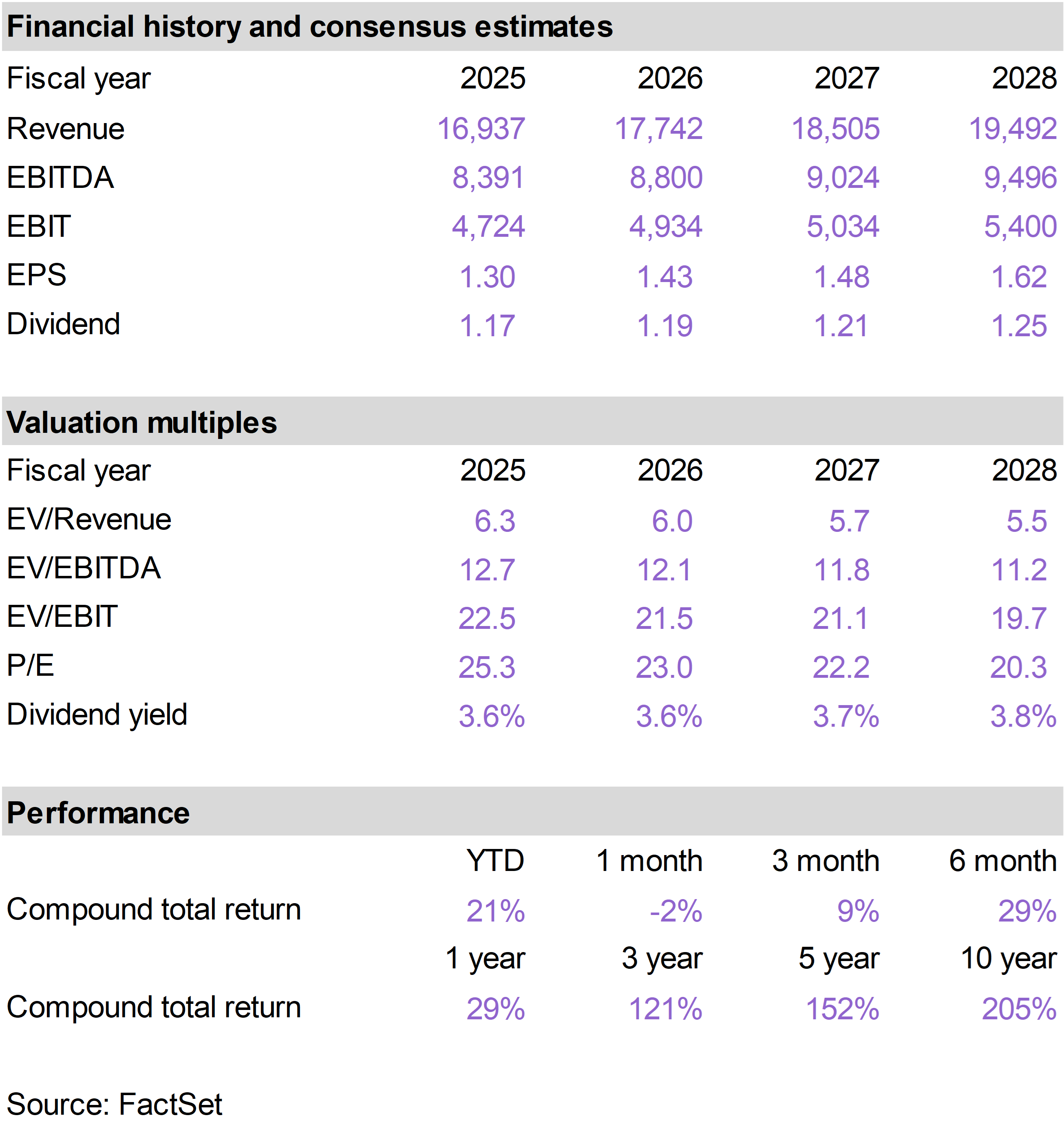

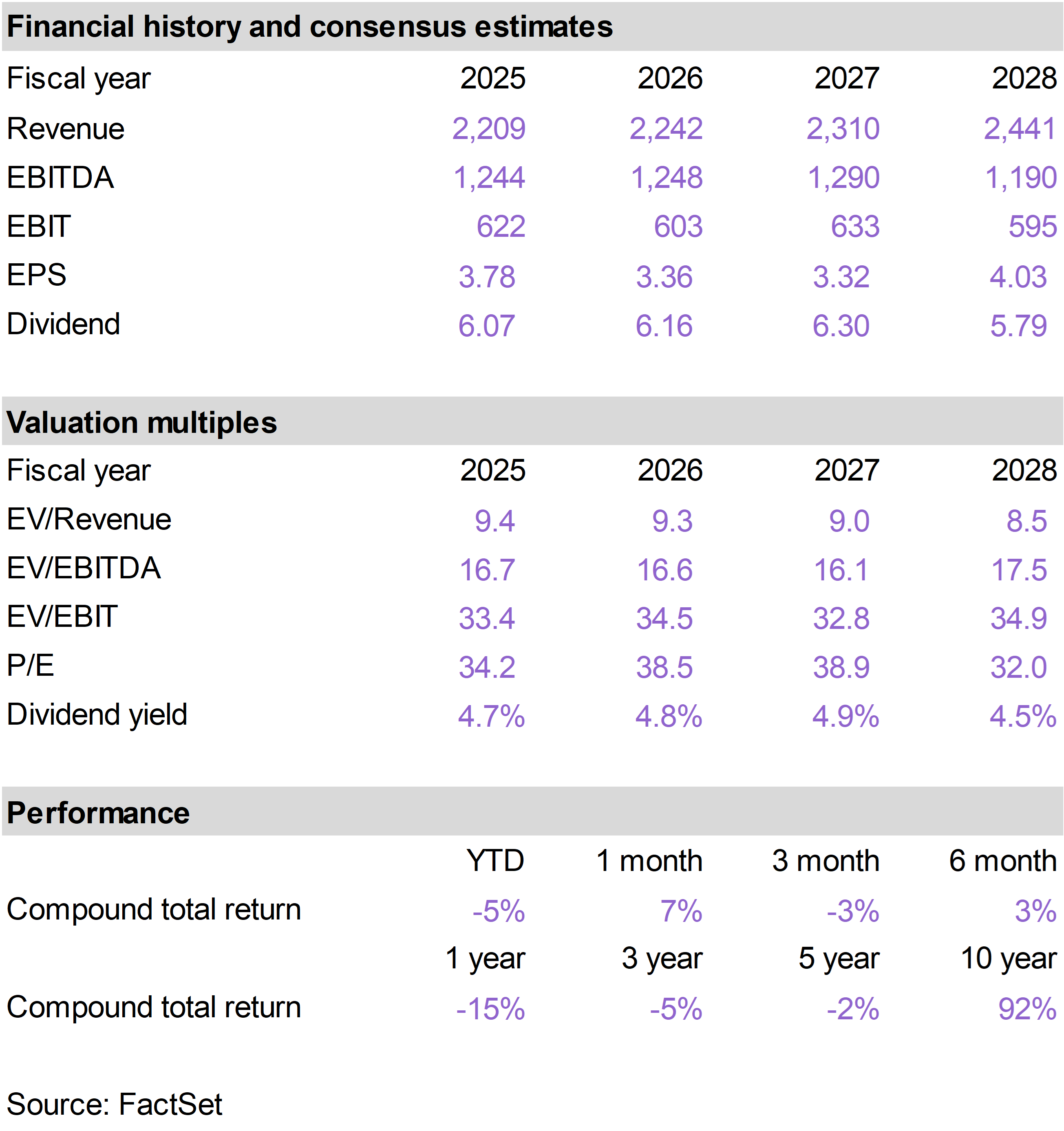

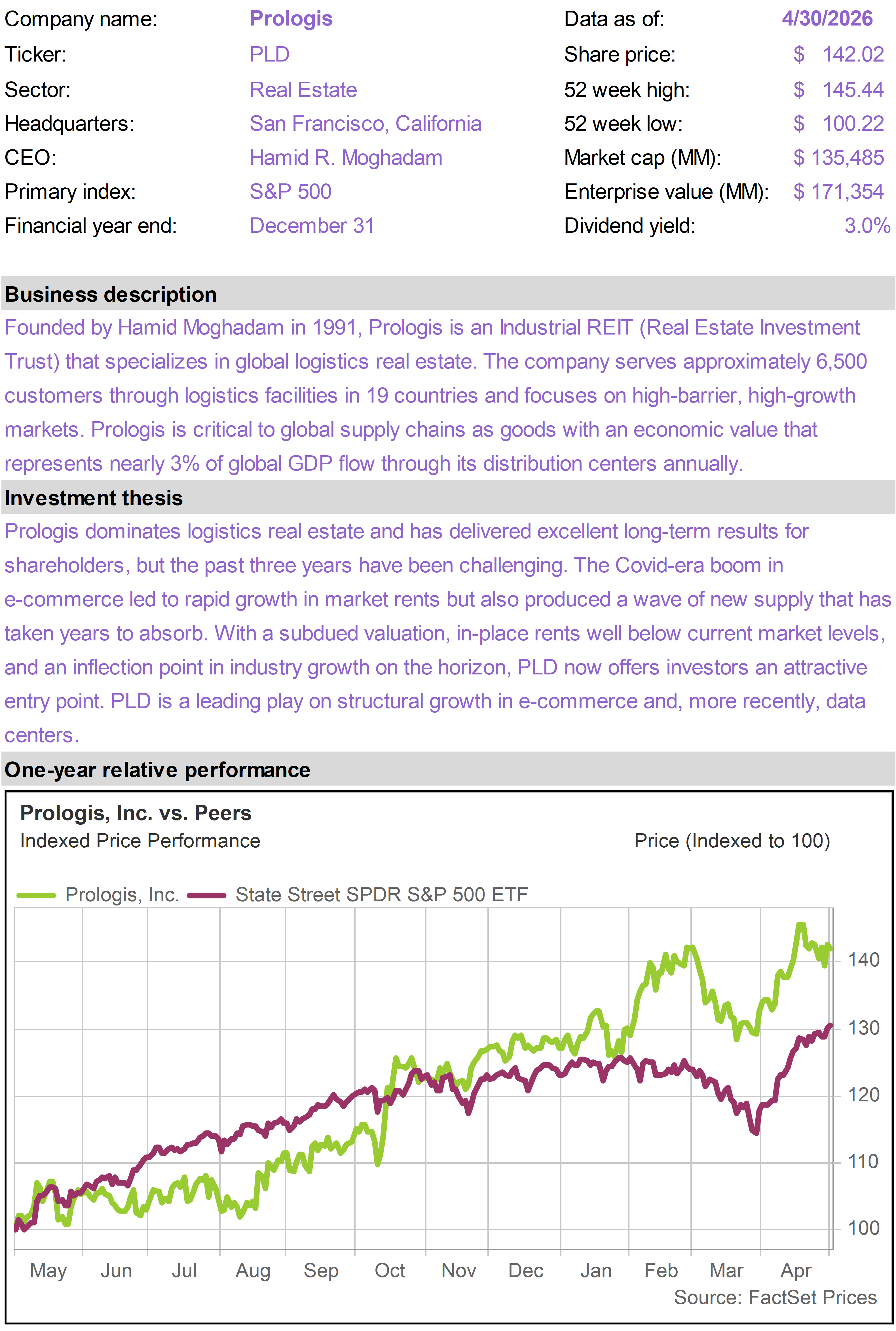

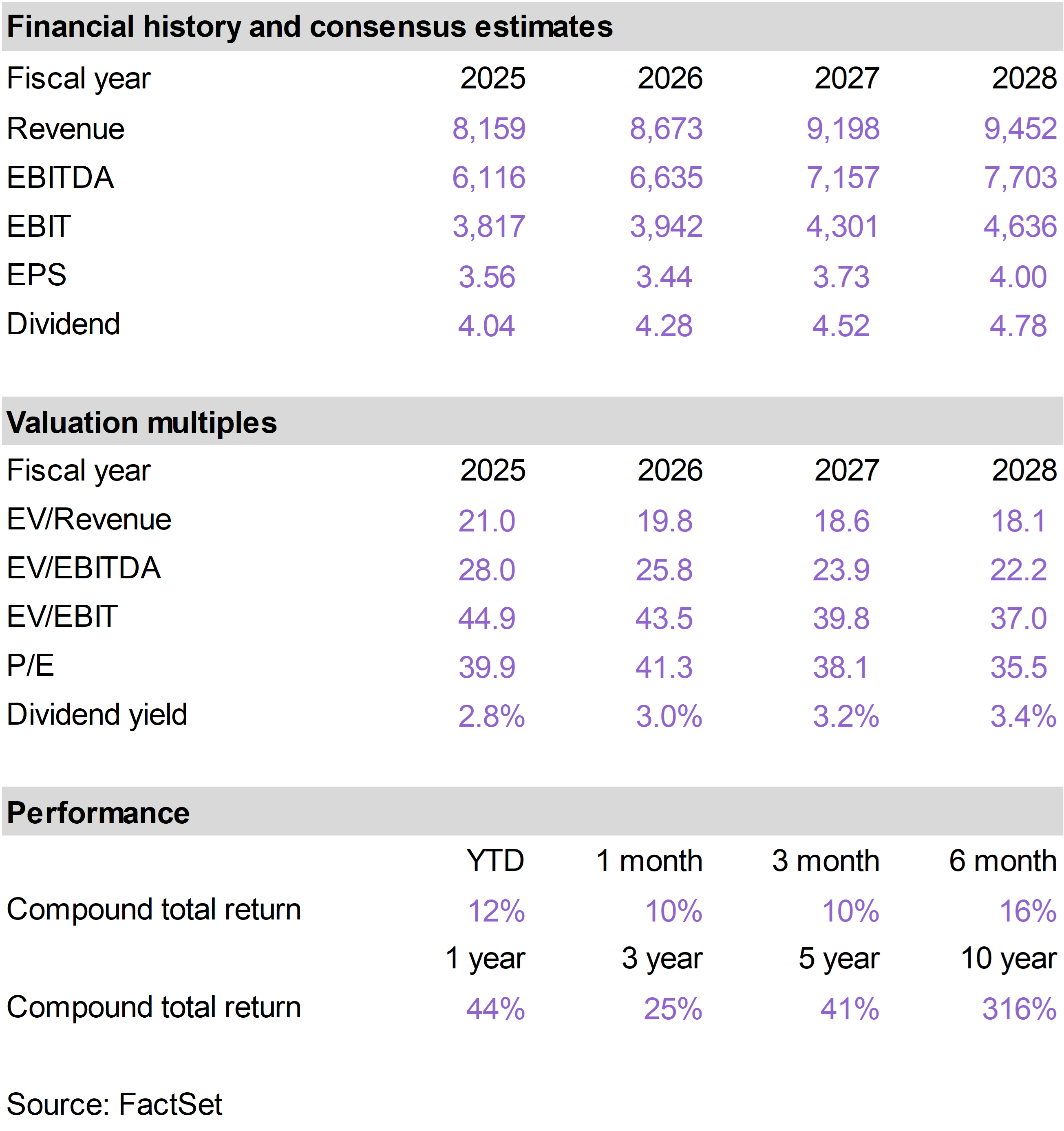

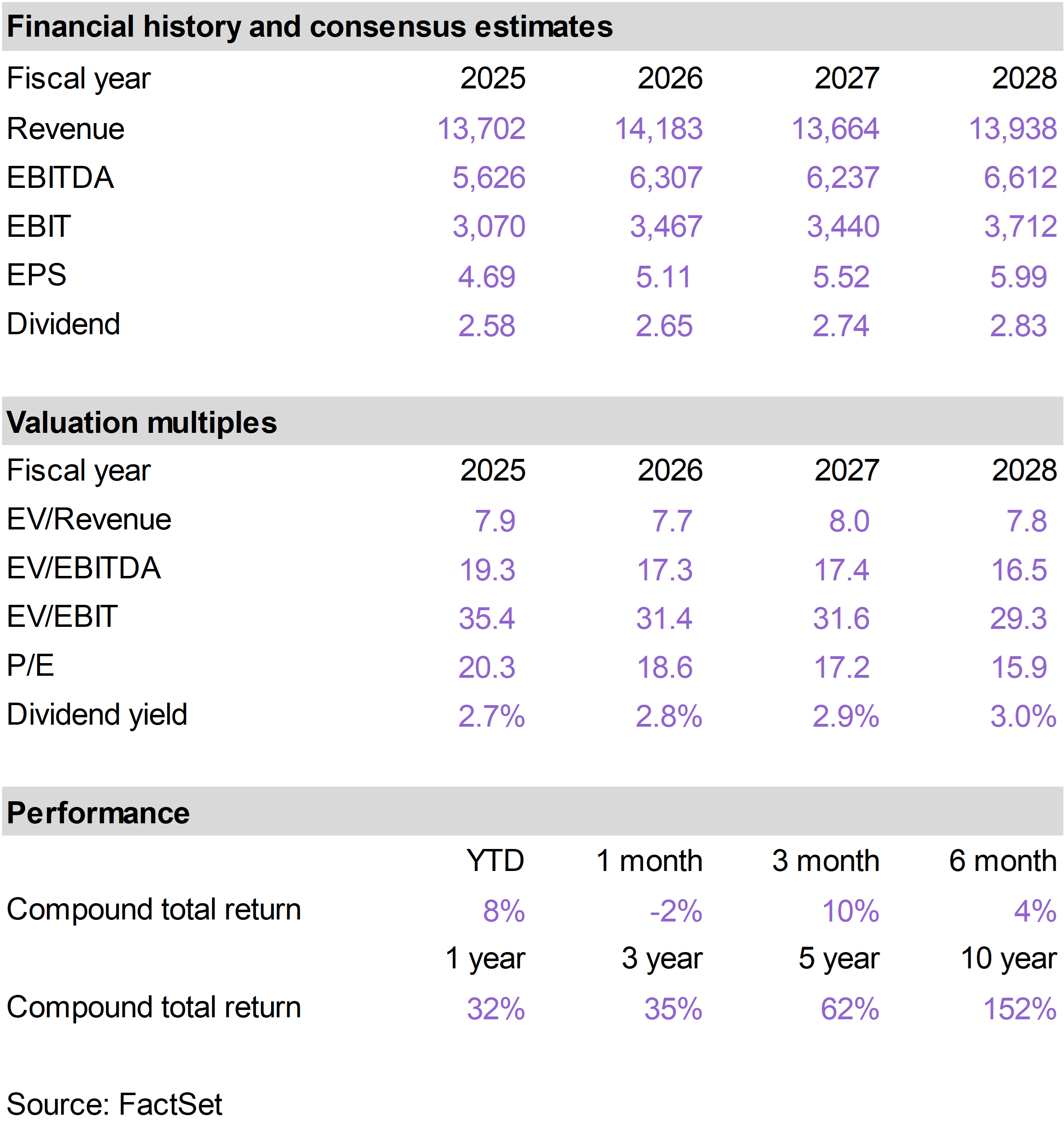

| | | The top performing positions within the portfolio in April were Texas Instruments (TXN), which returned 45%; Digital Realty Trust (DLR), which returned 12%; and Strategy 8% Perpetual Preferred (STRK), which returned 11%.

The worst performing positions were Kinder Morgan (KMI), which returned -2%; Sempra (SRE), which returned -2%; and WEC Energy Group (WEC), which returned 2%. |

|

| |

Shares of TXN surged in April following a strong first quarter earnings release that highlighted a powerful combination of cyclical recovery and structural growth.

The biggest driver was accelerating demand across industrial and data center markets. Industrial strength broadened across geographies and end markets, with activity still below prior peaks—suggesting further upside as the cycle continues to recover.

At the same time, the company is emerging as a key beneficiary of AI infrastructure spending. Data center revenue grew sharply—up roughly 25% sequentially and 90% year over year—driven by strong demand for power management chips used across AI systems.

This positions TXN as a critical, and often underappreciated, supplier to the AI buildout. Revenue, margins, and earnings all came in ahead of expectations, supported by higher volumes and improving factory utilization.

TXN is transitioning out of a heavy investment phase and into a period of rising free cash flow, with a greater share of revenue expected to convert into real cash earnings and shareholder returns.

Demand related to AI data centers is finally having a material impact on TXN’s financials, and the market is recognizing it. Over a longer time horizon, we also expect TXN to be viewed a major beneficiary of growth in robotics and “physical AI,” which rely heavily on analog chips. |

|

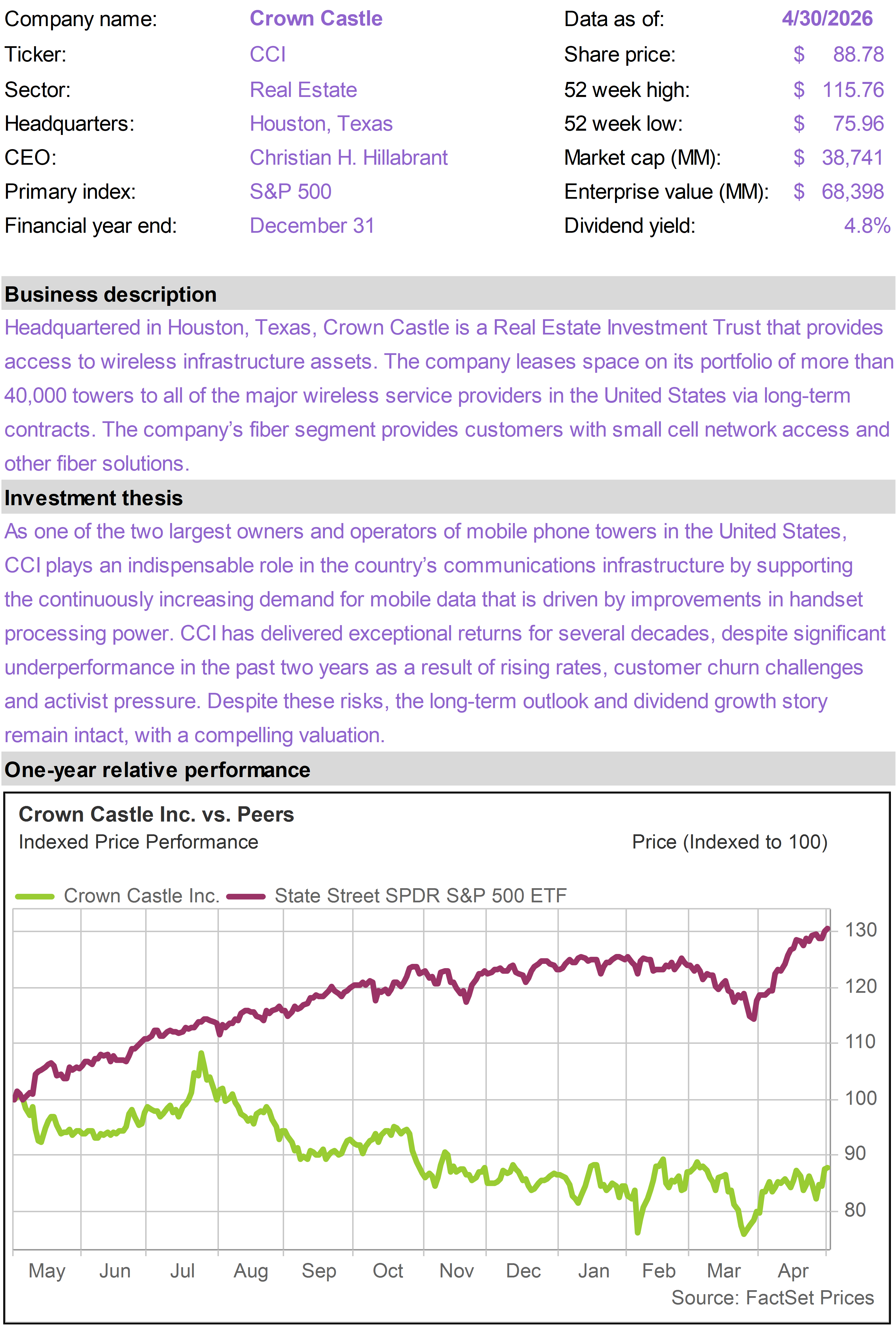

| | Shares of DLR outperformed after the company surpassed expectations for the first quarter and lifted guidance.

The strength in the quarter was driven by exceptionally strong leasing activity, with total signings reaching roughly $700 million, one of the largest quarters in the company’s history.

A significant portion of this demand is tied directly to AI, including a landmark 200 MW lease with a hyperscaler for AI inference workloads, highlighting the scale at which these deployments are now occurring.

Management emphasized that enterprise AI adoption is still in the early innings, with customers increasingly seeking larger capacity blocks as AI workloads move from experimentation into production. This is showing up in both colocation and large-scale leases across global markets.

Available supply remains constrained, favoring DLR’s established footprint of data centers around the world. Power availability, labor, and permitting challenges are limiting new capacity, creating a favorable pricing environment.

DLR raised its expectations for leasing spreads and is also accelerating development. Capacity under construction has increased to roughly 1.2 GW, with a multi-gigawatt pipeline behind it, positioning the company to capture sustained demand from both cloud and AI customers.

DLR sits at the physical center of the AI buildout. As demand for compute continues to surge, the infrastructure required to support it—data centers, power, and connectivity—is becoming just as critical as the chips themselves. |

|

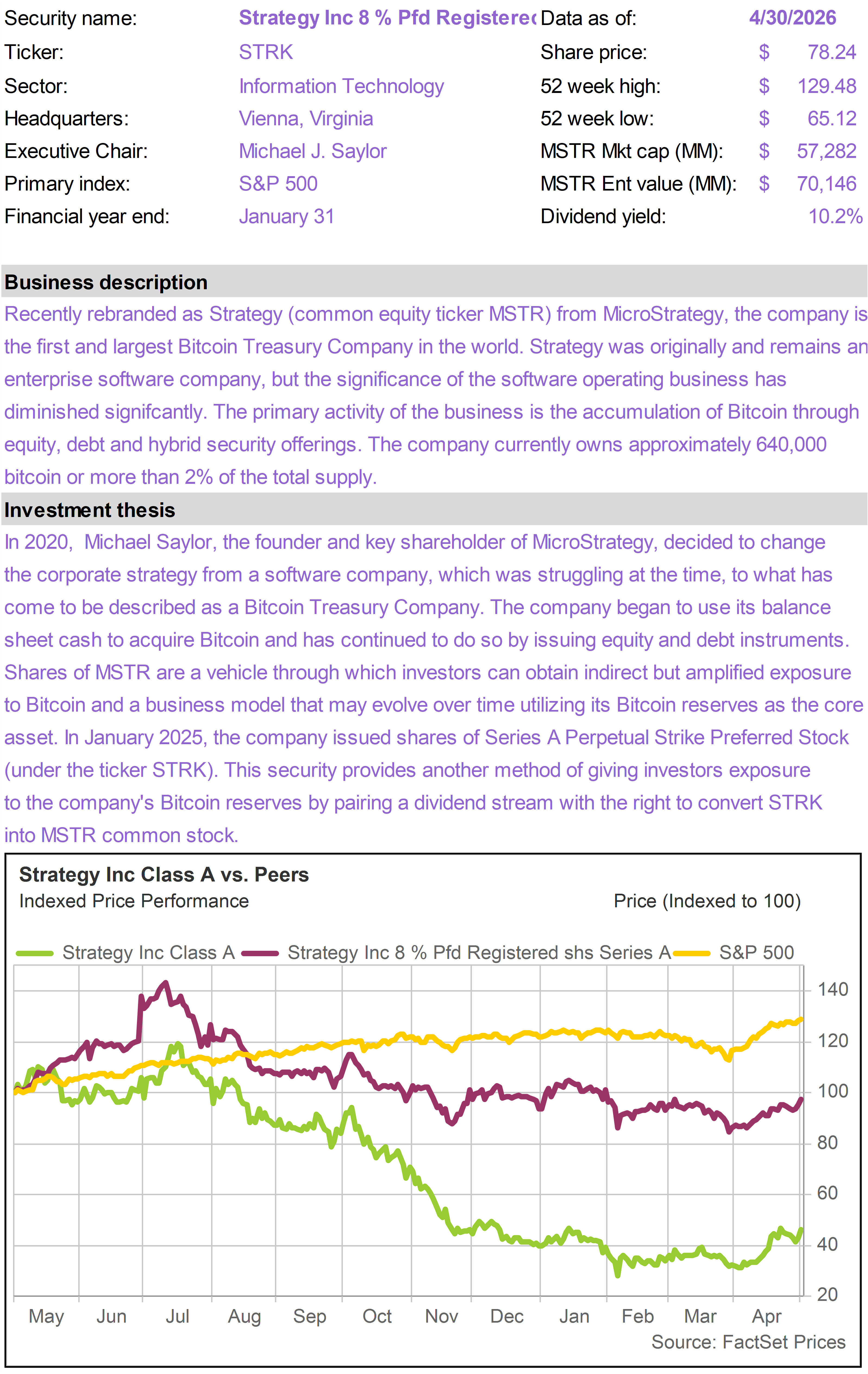

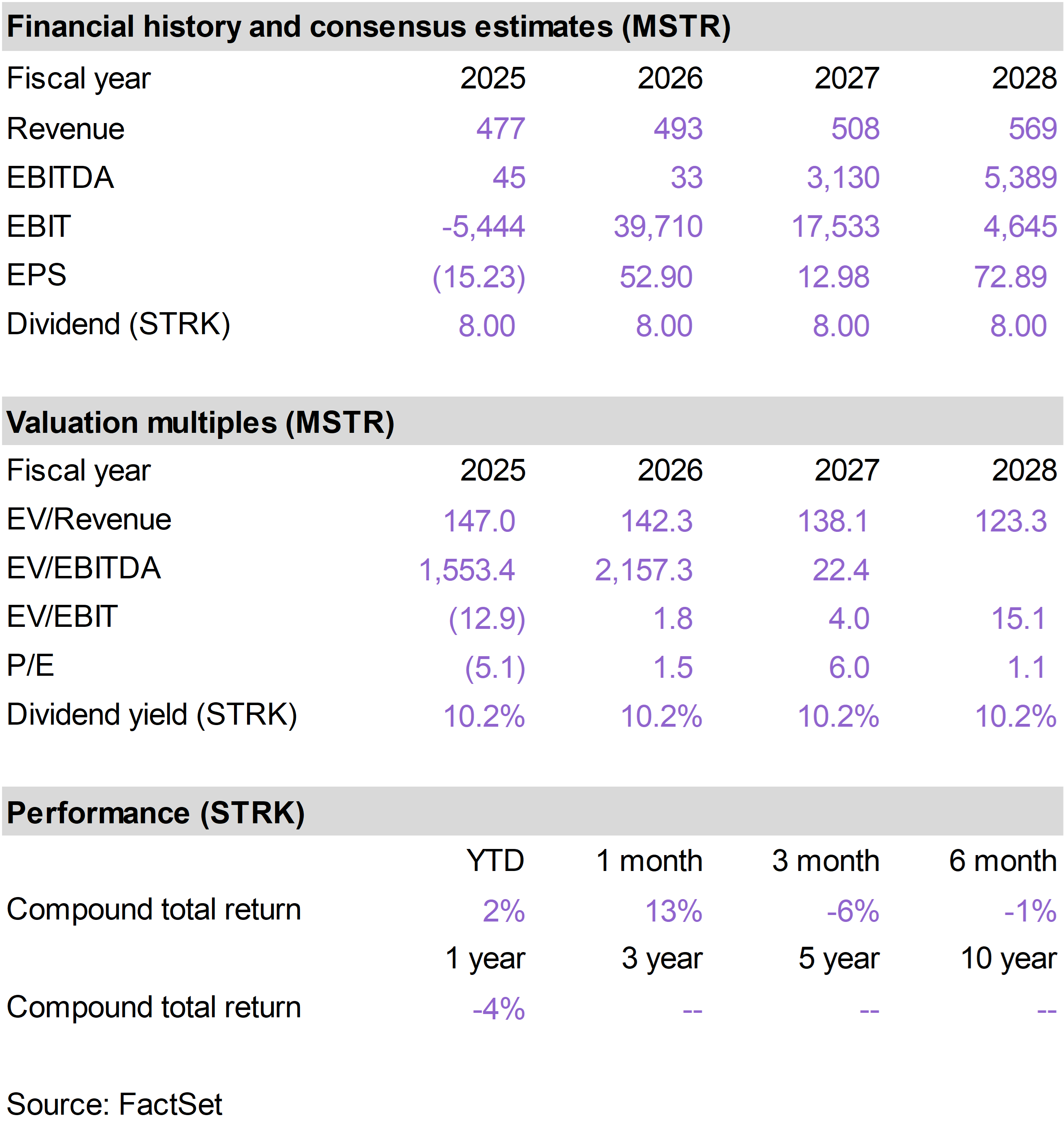

| | STRK performed well in April as Bitcoin pricing firmed and the MSTR share price advanced. Despite the improvement, STRK continues to offer investors a double-digit dividend yield, paired with long-term upside potential through the MSTR conversion feature.

For investors comfortable with Bitcoin volatility, we continue to like STRK, especially considering the substantial overcollateralization of its debt and preferred stock obligations.

Crypto as a whole has stabilized and nudged higher in recent months. Passage of the CLARITY Act, key legislation that will help mainstream financial institutions integrate blockchain technologies and products, now seems increasingly likely. This could provide further upside to Bitcoin, MSTR and, in turn, STRK. |

|

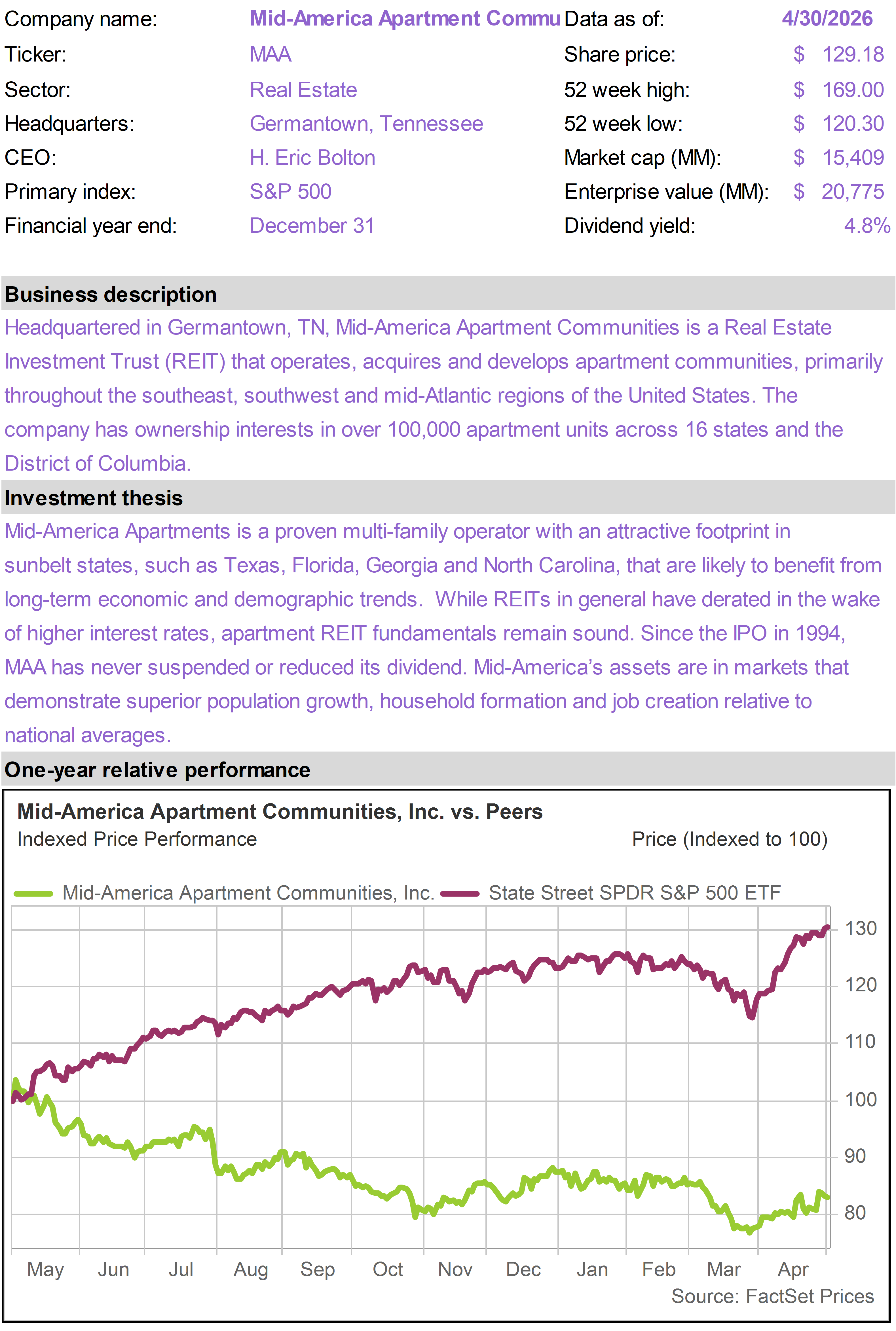

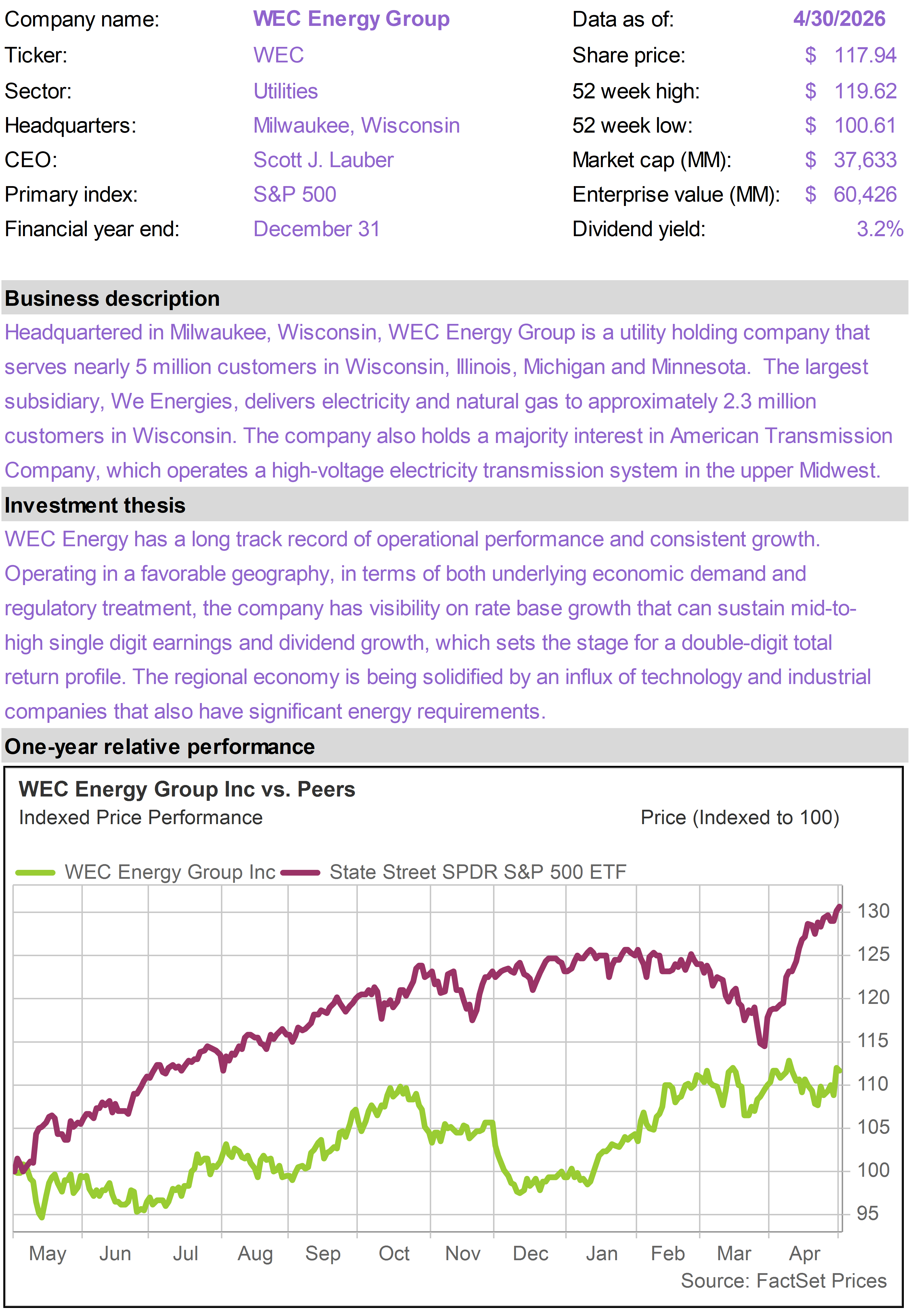

| | KMI, SRE and WEC underperformed in April, as investor interest migrated away from energy and utilities toward tech and other cyclical areas.

While these stocks lagged the sharp upside seen in other sectors, share prices were broadly unchanged over the course of the month. Contained portfolio losses helped the Income Builder keep pace with the broader market in April, despite significantly lower tech exposure. |

|

| | |

| | |

| | |

| | | |

|

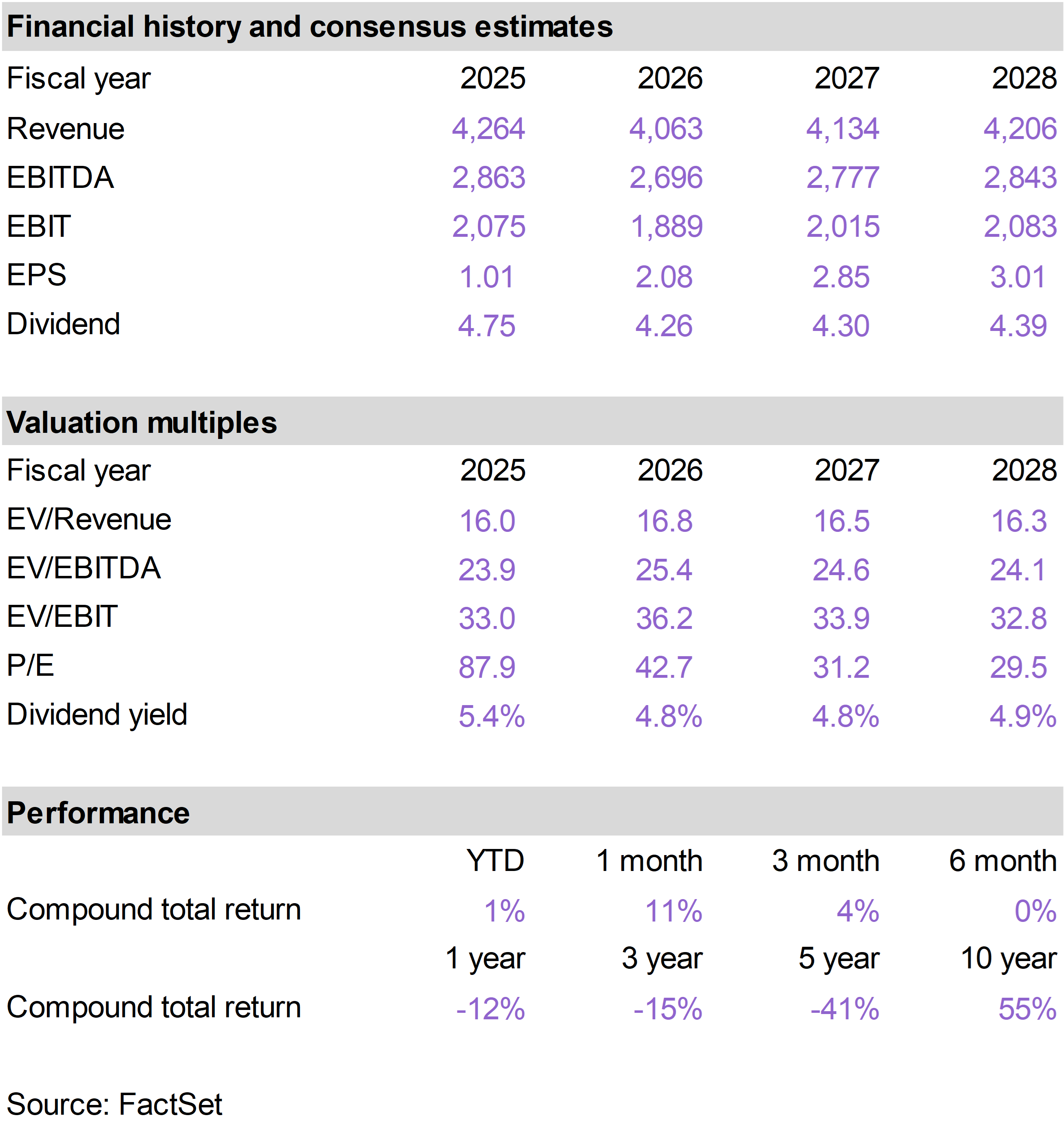

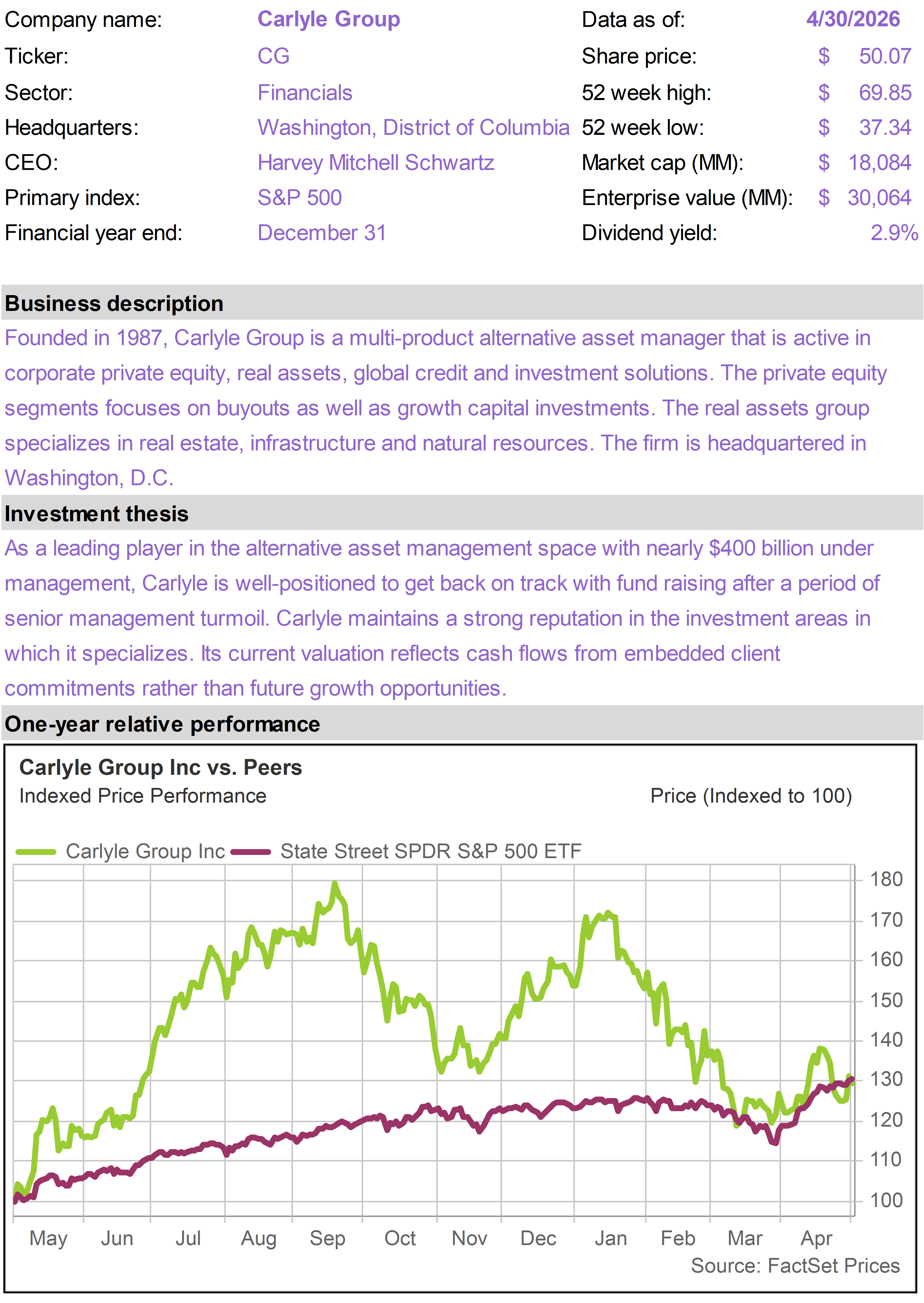

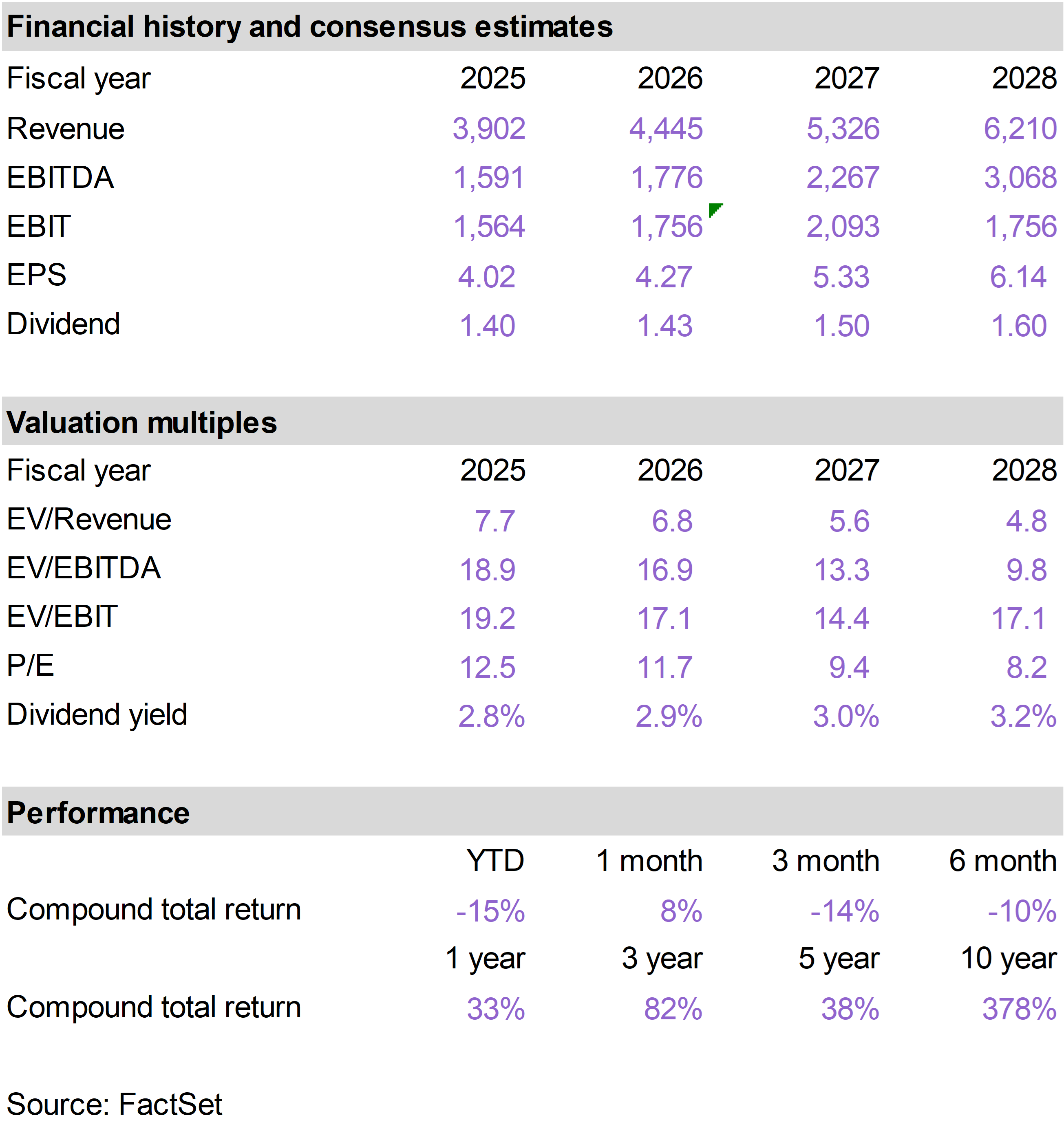

| | Digital Realty Trust (DLR) |

|

|

|

| | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Diamondback Energy (FANG) |

|

|

|

| | |

|

| | Mid-America Apartment (MAA) |

|

|

|

| | |

|

| | |

|

| | |

|

| | Strategy 8% Perpetual Pref (STRK) |

|

|

|

| | |

|

| | The 76research Income Builder Model Portfolio is intended for income-oriented investors and managed to generate an overall yield that is materially higher than broad equity indices. The portfolio includes stocks with above average dividend yields from a cross section of industries. While investments are screened for their income and income growth characteristics, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

|