The surge in e-commerce with the onset of the pandemic led to massive global demand for warehouse capacity. PLD performed extremely well through early 2022 as warehouse rents surged.

The industry invested heavily in new space, however, and e-commerce demand soon moderated as Covid restrictions disappeared. This led to a sharp rebalancing of supply/demand conditions.

After several years of excess capacity absorption, the logistics space is now once again getting much tighter. In its mid-October third quarter earnings report, PLD reported record leasing activity and nudged up forward guidance.

Industrial real estate operates with long cycles. Just as it took several years to absorb the aggressive buildouts of the Covid-era, we are now looking at a multi-year period of tightening supply and rising rents.

Development pipelines have slowed meaningfully due to higher interest rates and construction costs, while demand has continued to rise steadily.

As a result, market vacancy is drifting lower again, and lease roll-ups are trending well above expiring rents. For PLD, whose portfolio is heavily weighted toward key logistics corridors and modern distribution facilities, this translates into strong pricing power, high occupancy, and steady internal cash flow growth.

There is now an additional growth driver as well… data centers.

PLD is of course primarily a logistics player, but it is now participating in the data center build-out because it already controls millions of square feet of strategically located real estate that data center developers need.

Modern data centers require large parcels close to cities, access to utility-scale power, and dense fiber connectivity—the exact locations where PLD has spent decades assembling and entitling logistics land.

Rather than becoming a data center operator, PLD is leveraging its existing land bank and warehouse footprint to offer “powered shells” and development sites to hyperscale cloud providers. This allows PLD to capture higher rents and multi-decade lease terms with minimal incremental risk.

PLD is early in this opportunity to convert warehouses and vacant land into “higher and better use” data centers, but investors are increasingly focused on it. Some analysts are already calculating the potential value creation from this additional growth driver, which was largely ignored twelve months ago, as approximately 10% to 15% of the current share price.

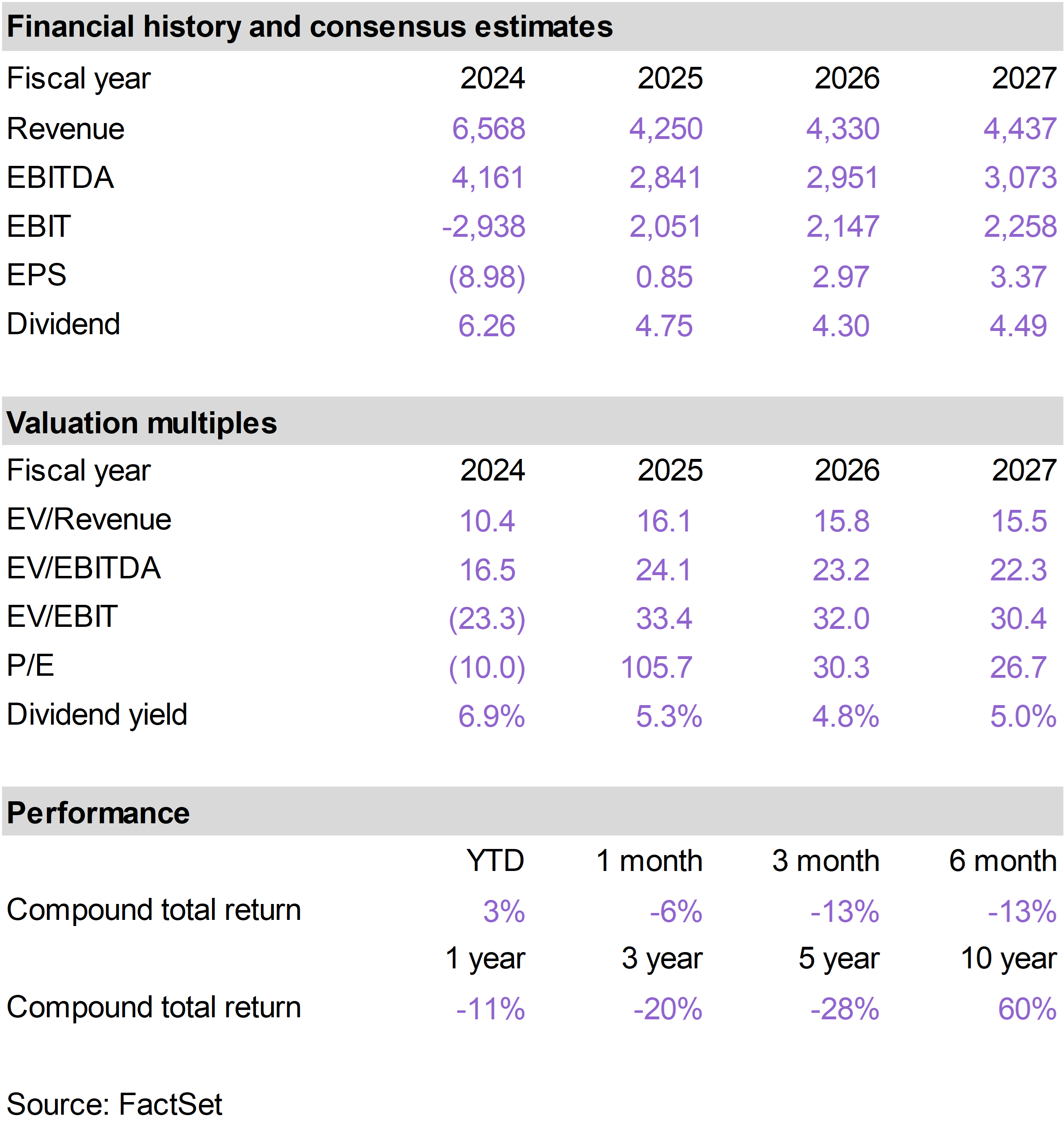

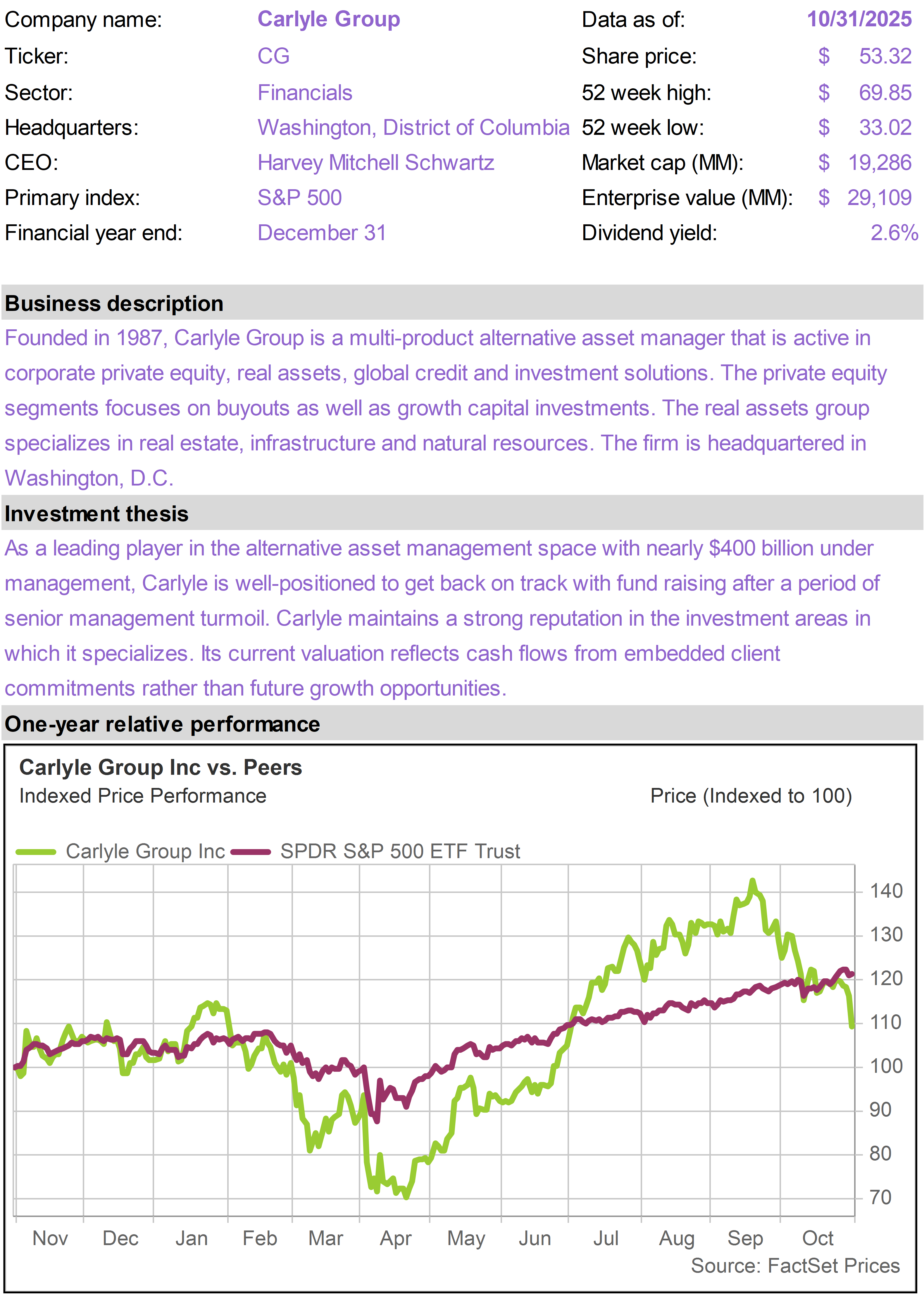

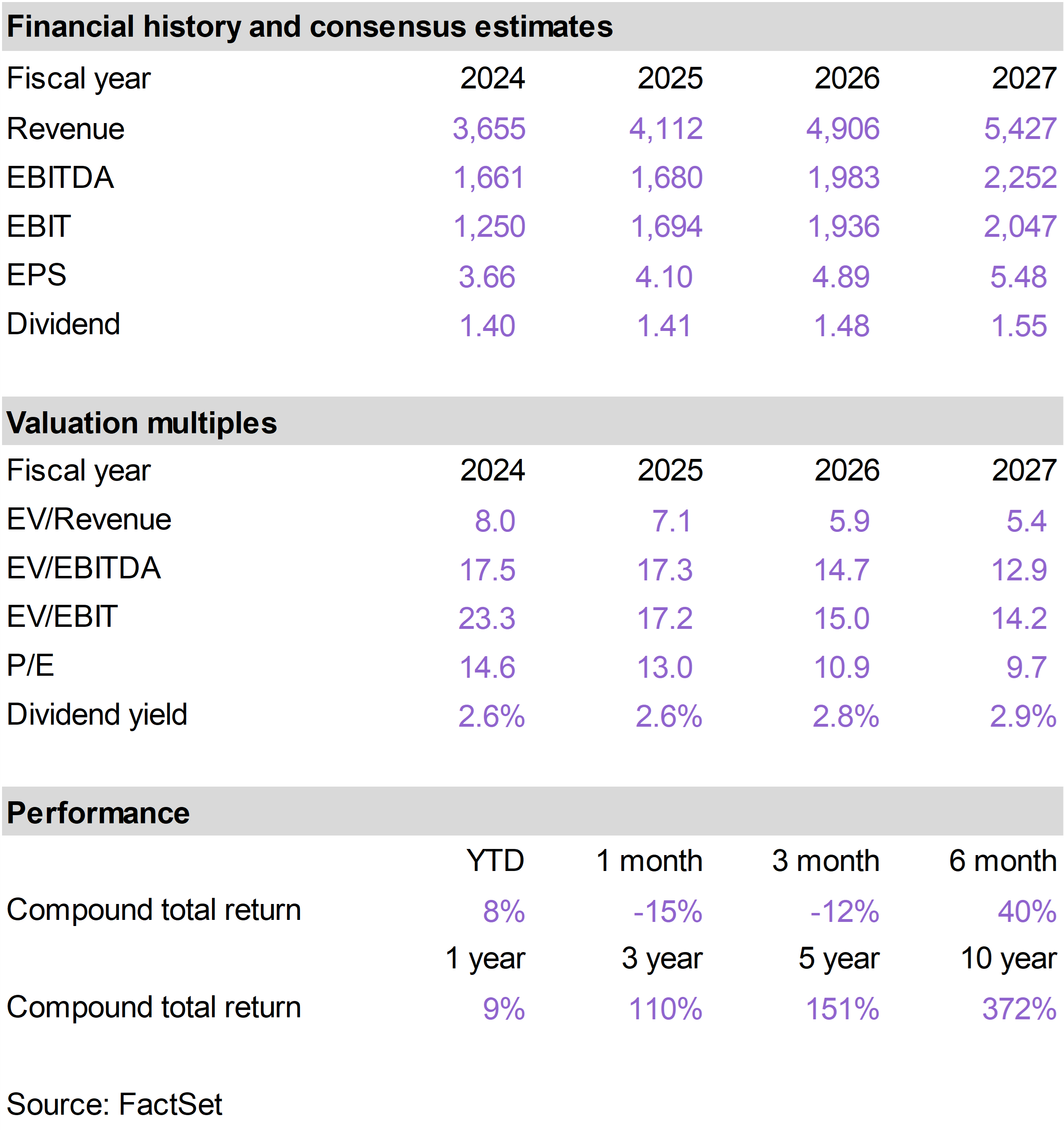

Cockroach phobia

The portfolio’s alternative asset managers—BX and CG—sold off sharply in October after having reached or approached all-time highs in mid-September.

While the firms demonstrated strong asset gathering and earnings growth when they reported third quarter earnings, investors in financial stocks appear to have been rattled by emerging risks in private credit.

Investors have been specifically focused on comments made by JPMorgan Chase CEO Jamie Dimon, who in mid-October reacted to the bankruptcy of subprime auto lender Tricolor Holdings by observing that “when you see one cockroach, there are probably more.”

We view the sell-off in BX and CG as excessive, given the breadth and positive momentum of their businesses and the unique challenges of the subprime auto market.

These are strong franchises benefiting from durable trends in the financial services industry; we see investor skittishness around these names as an opportunity.

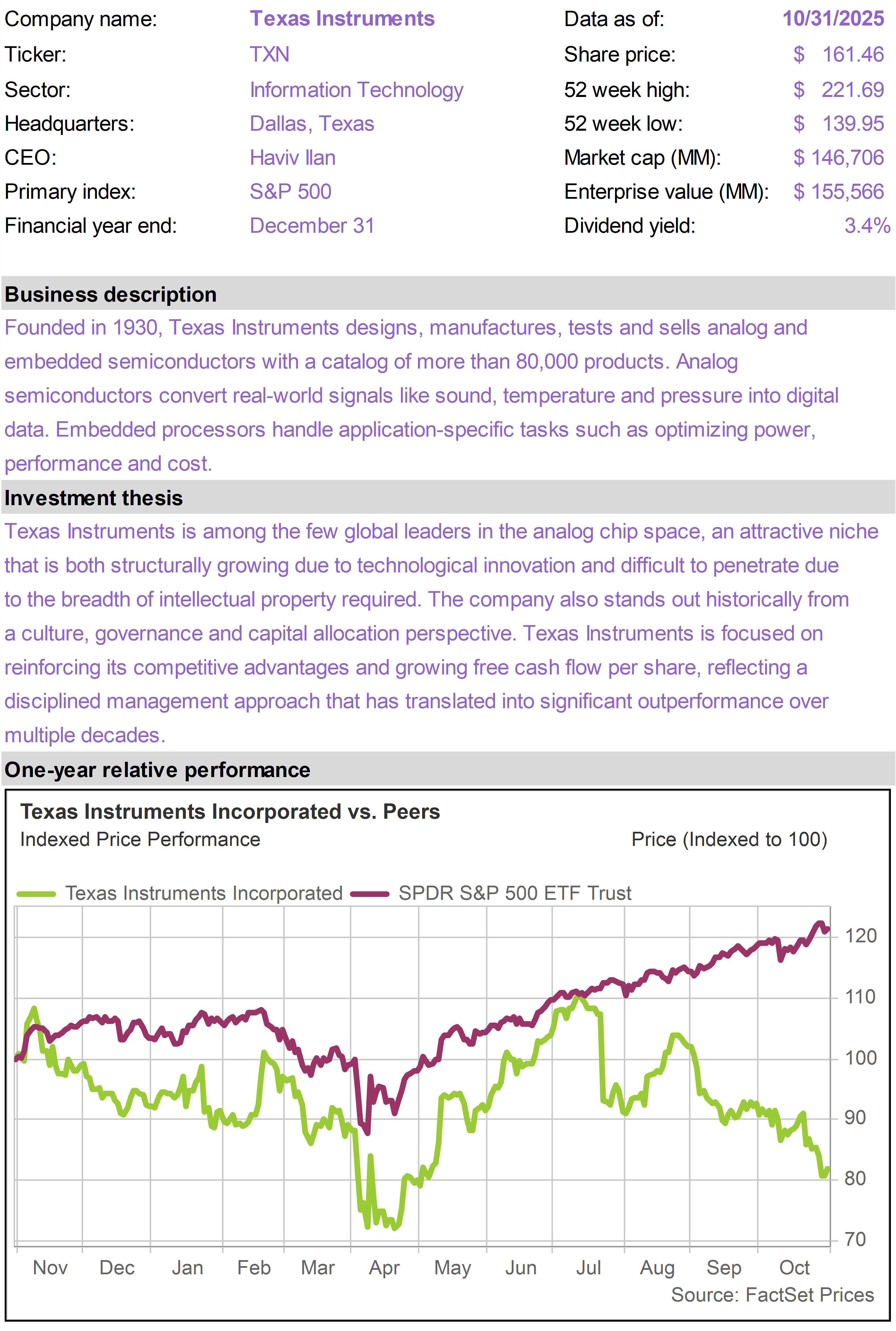

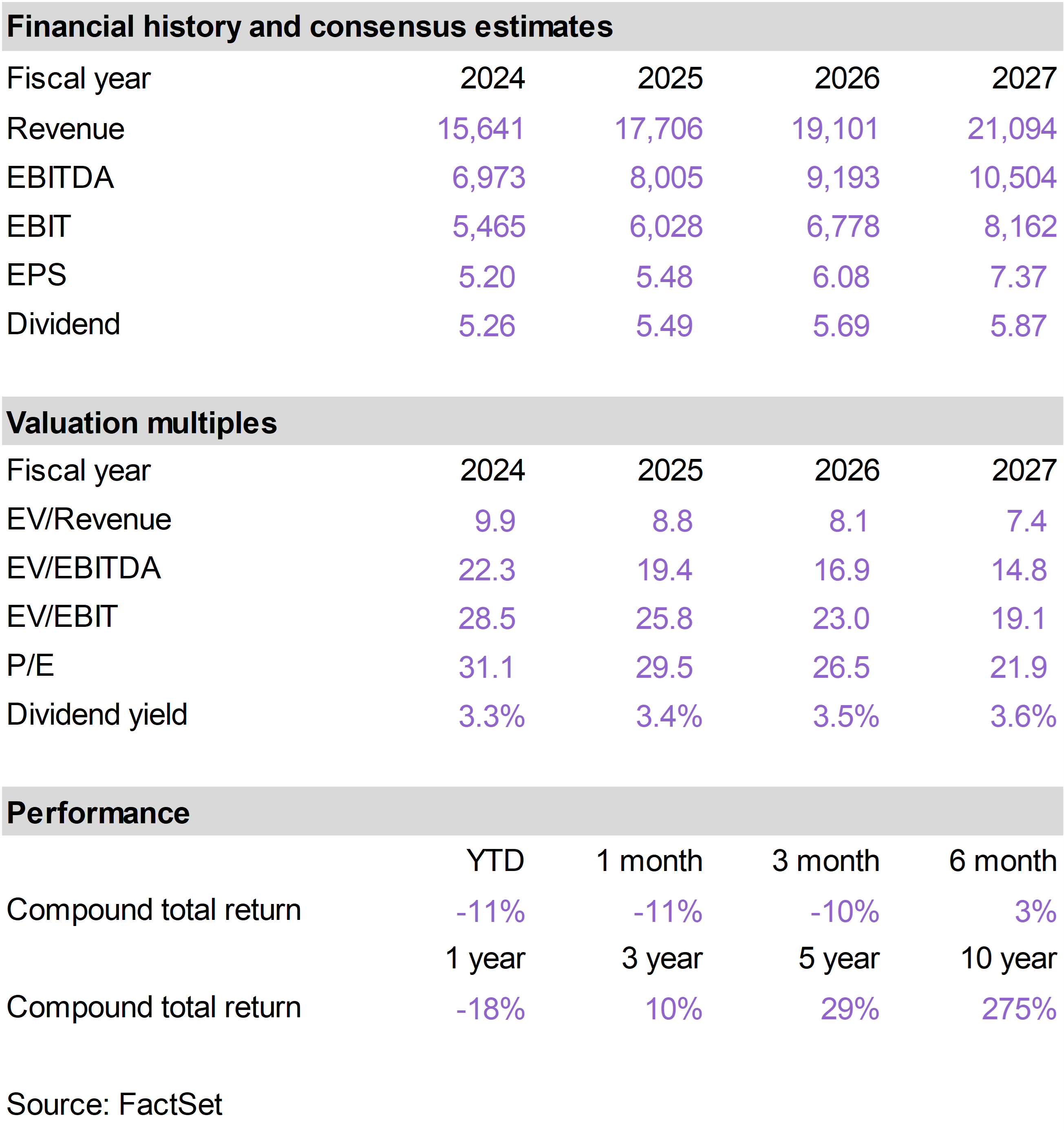

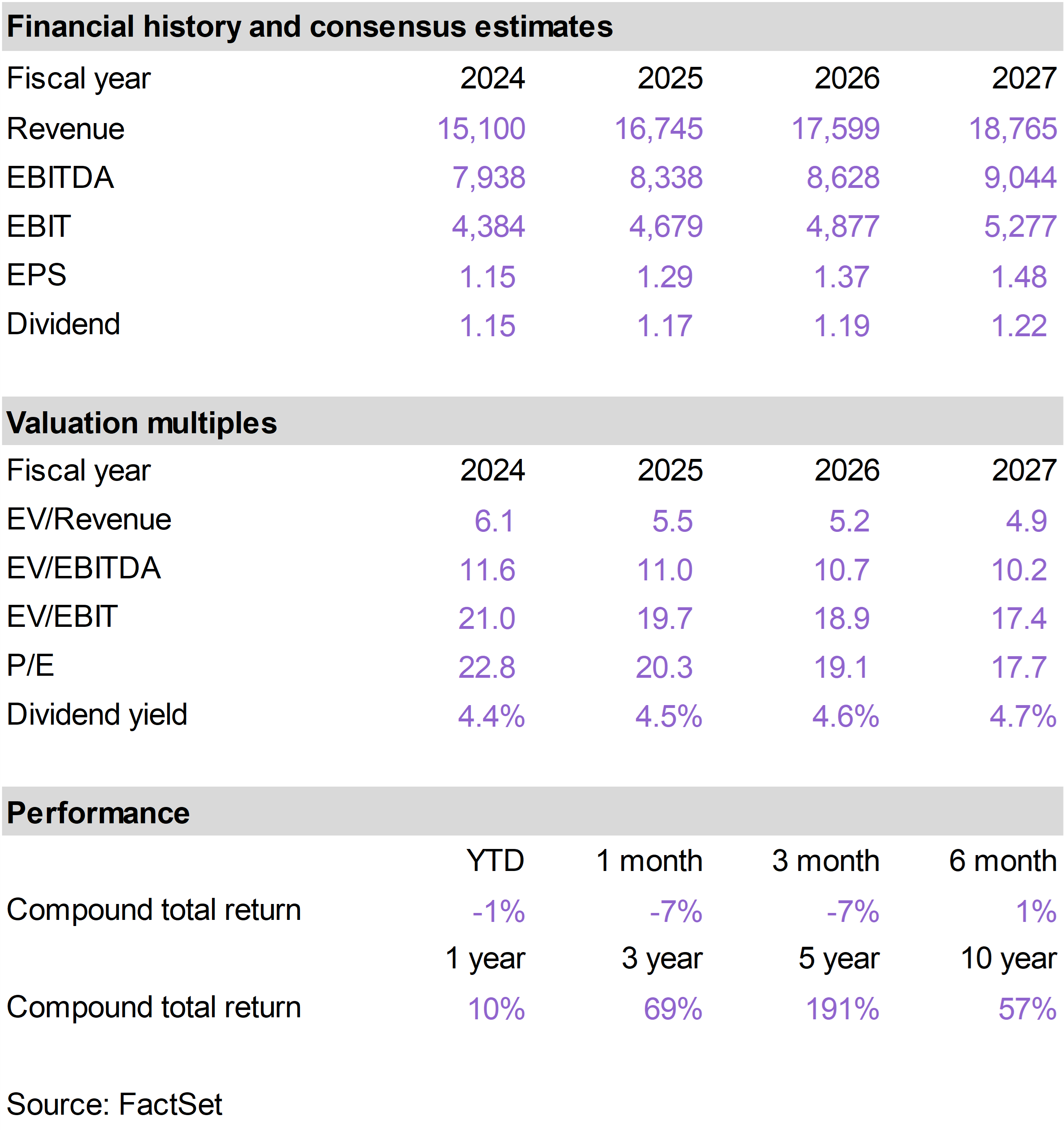

Undervalued AI beneficiary

The market’s view of TXN is similarly too pessimistic, in our view—placing too much emphasis on short-term challenges as opposed to compelling long-term opportunities.

TXN shares declined following its third-quarter earnings report. While results largely met expectations, management guided to softer demand in the industrial end market for the upcoming quarter.

In a market where many technology companies are reporting accelerating growth tied to AI adoption, TXN’s slower cyclical recovery has tested investor patience. The near-term backdrop remains mixed, but the long-term strategic position is still highly attractive.

TXN is a market-leading supplier of analog and embedded processing chips that are essential for powering and controlling real-world systems. These are critical to data centers, robotics, factory automation, electric vehicles, and autonomous driving—all of which are long-duration AI-driven growth trends.

TXN has the world’s most advanced and efficient analog chip fabs located within U.S. borders. This positions it to be the low-cost, high-reliability supplier of choice to manufacturers in these growth areas.

As the industrial cycle stabilizes, TXN remains well-placed to expand margins and move closer to its long-term free cash flow targets. For investors seeking long-term exposure to AI without paying premium valuations, TXN offers a compelling setup at current levels.

As the company’s major fab expansion cycle winds down, capital expenditures are poised to decline meaningfully. At the same time, revenues are expected to grow steadily as industrial and auto demand stabilize. Together, these dynamics support analyst forecasts that call for free cash flow to nearly triple over the next two years.

Looking further ahead, AI-intensive markets—data centers, robotics, factory automation, EVs, and autonomous systems—will represent an increasingly large share of TXN’s business mix. As this transition unfolds, TXN’s long-term growth profile should improve, with structurally higher margins and more durable long-term demand.

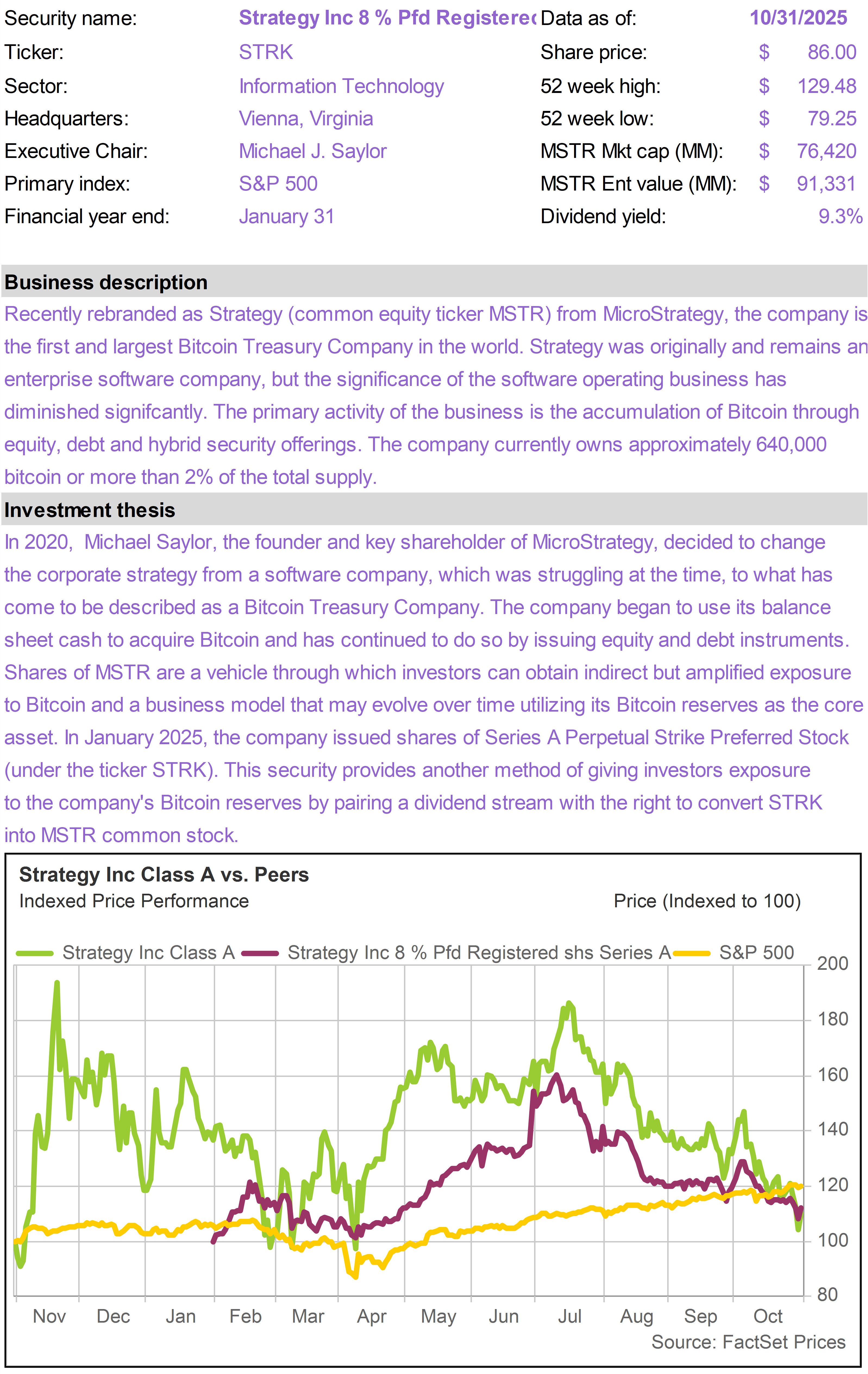

STRK dividend tax treatment

In last month’s report, we added Strategy 8% Perpetual Pref (STRK) to the portfolio to take advantage of weakness in the share price. STRK now offers an effective yield of approximately 9%.

Since adding STRK to the portfolio, we learned of an interesting wrinkle to how the IRS will classify the $2 per quarter dividend distributions that STRK pays out. Because these will largely be funded by the sale of MSTR stock, the dividends, according to statements made by the parent company Strategy, will be regarded as “return of capital.”

This tax treatment is expected to persist for as long as ten years.

In taxable accounts, this means investors will not have to pay taxes on the dividends they receive. What happens is the cost basis in their investment in the security is effectively reduced, so if a shareholder were to sell the security later on for a gain, the taxable capital gain would be higher.

For income-seeking investors, this determination of the tax treatment of Strategy’s preferred stock dividends is very attractive.

In addition to the ~9% dividend yield, STRK investors get the benefit of the permanent convertibility of STRK into MSTR common stock. In a scenario where Bitcoin appreciates substantially, the value of the conversion option could increase substantially as well.