| Inflation Protection Model Portfolio |

|

| Monthly Portfolio Review: May 2026Publication date: June 1, 2026 |

|

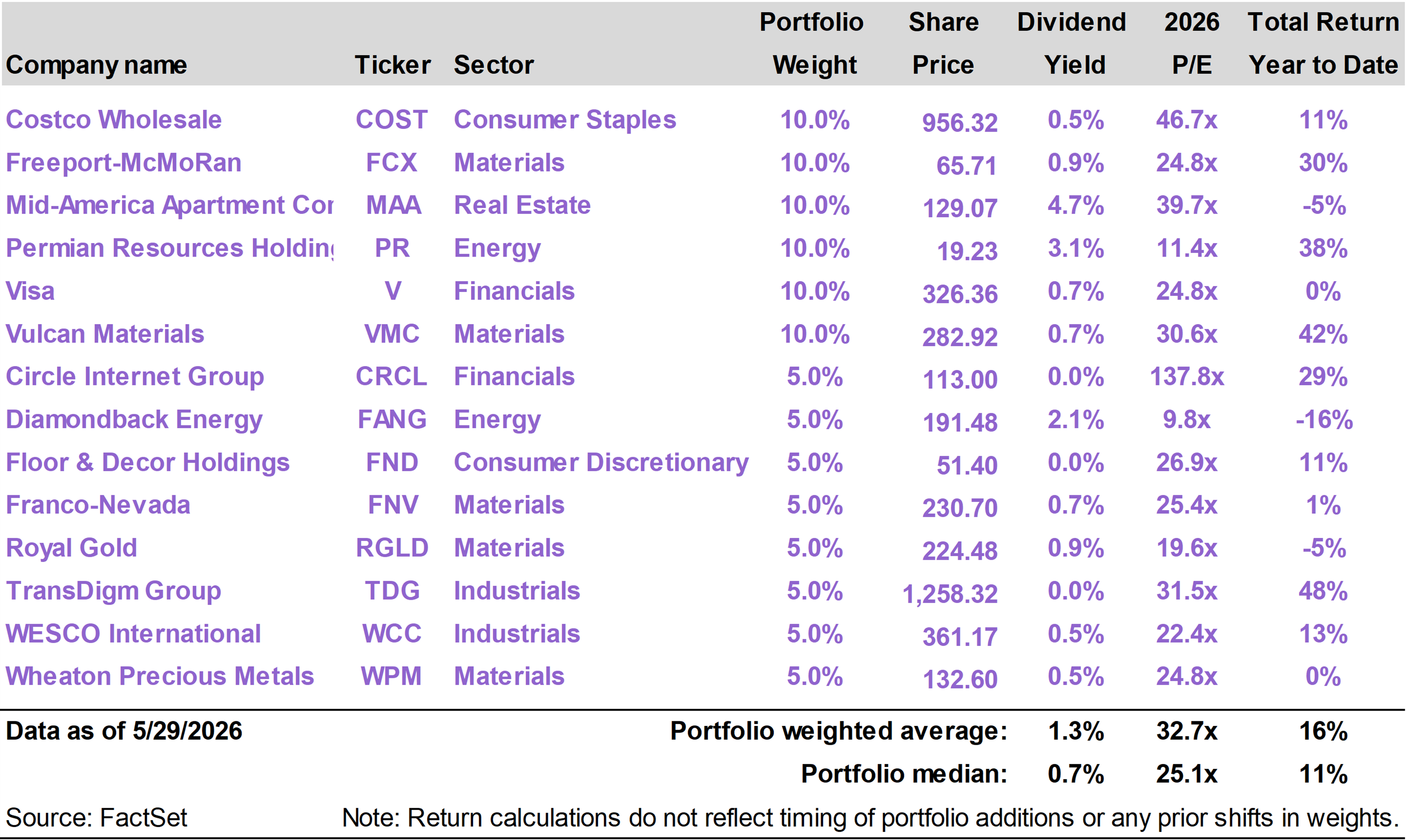

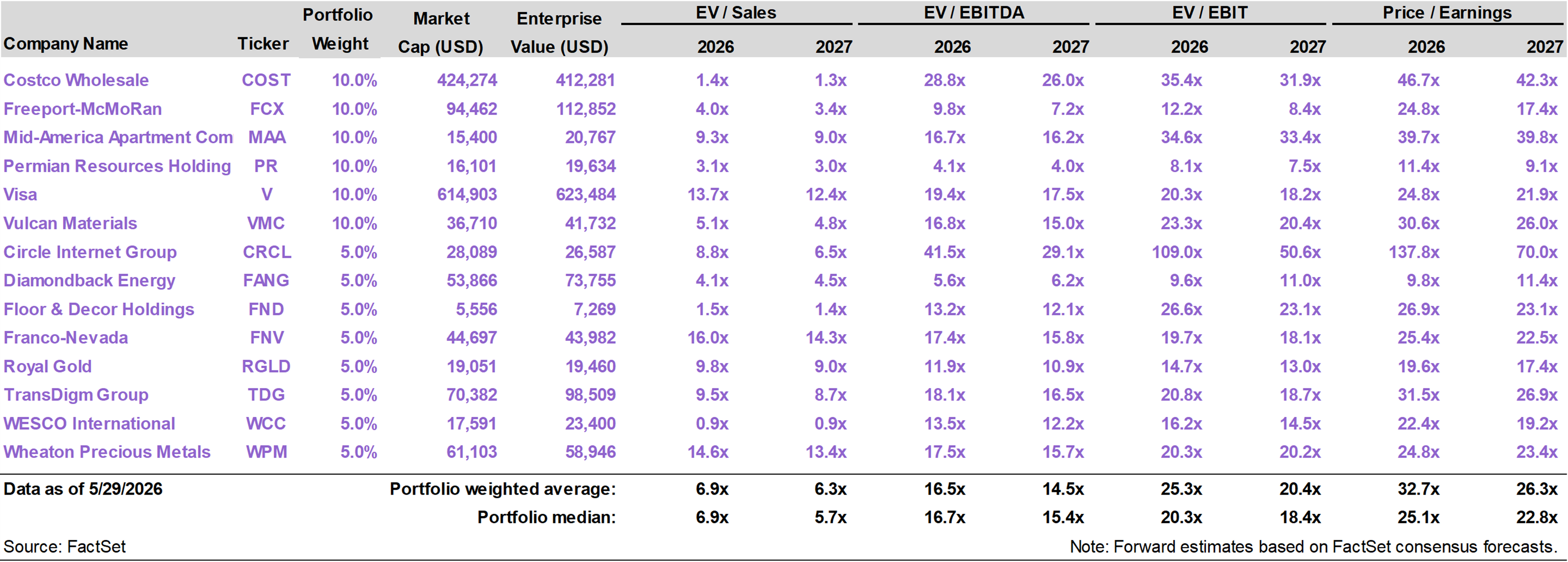

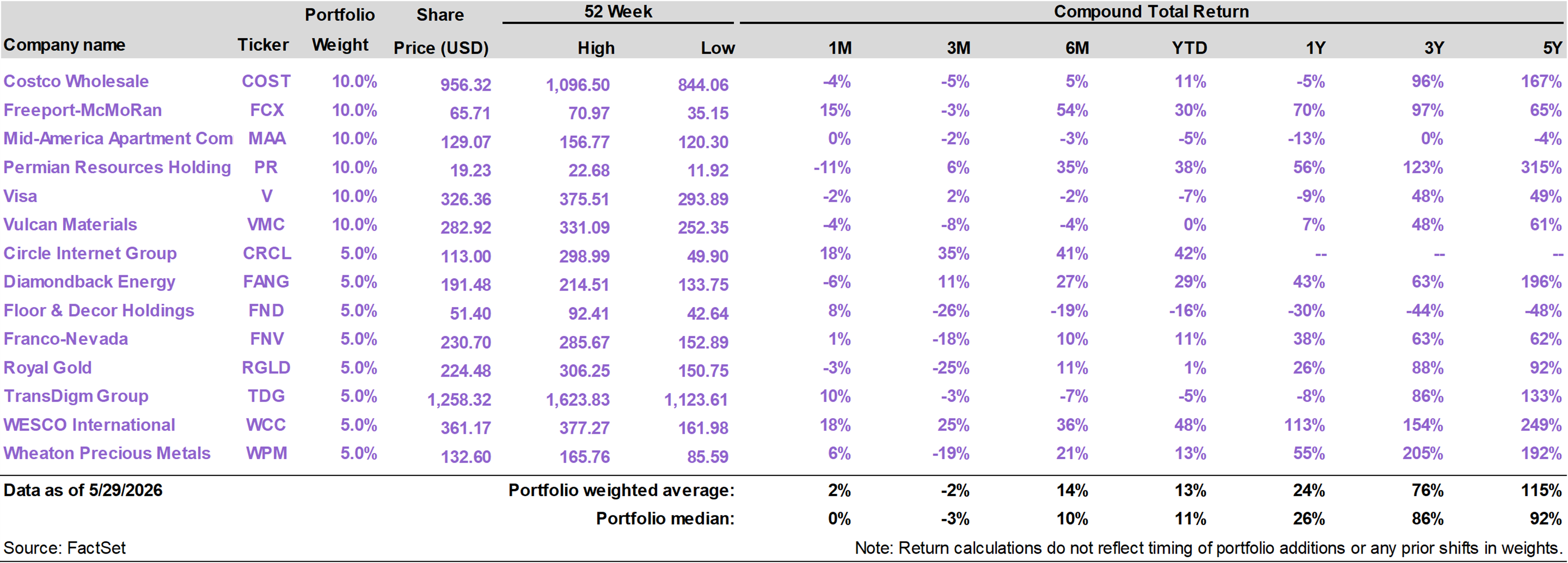

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

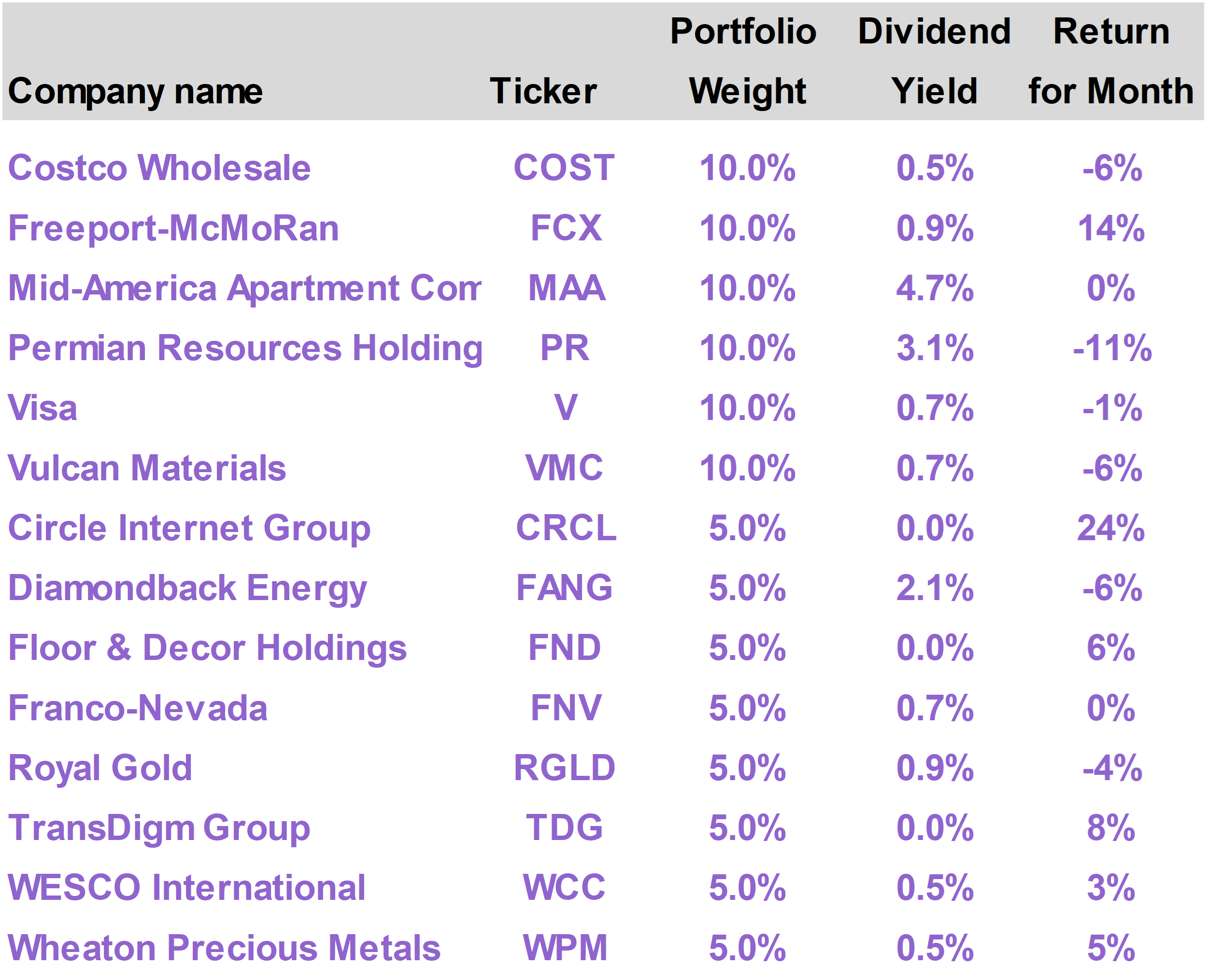

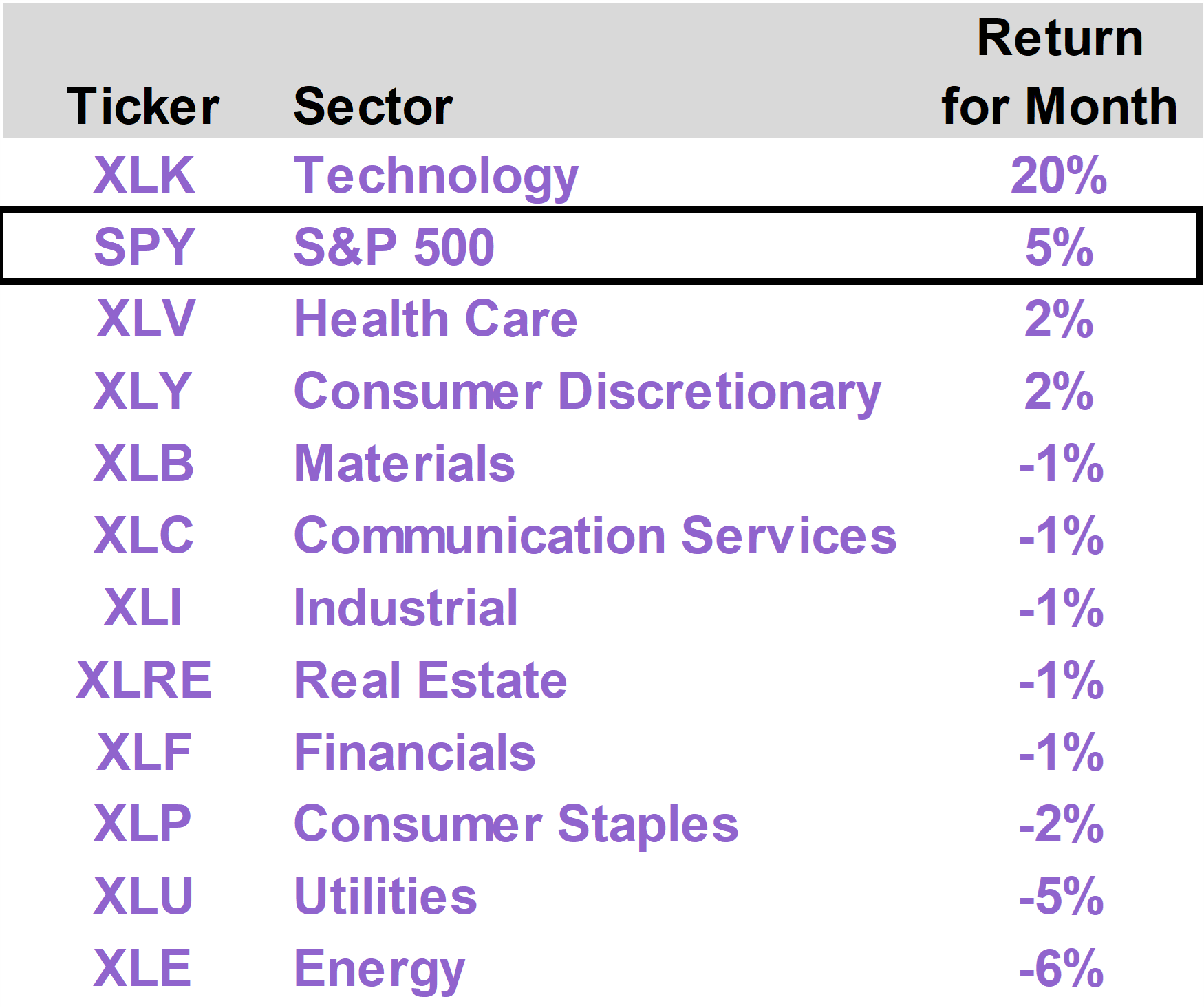

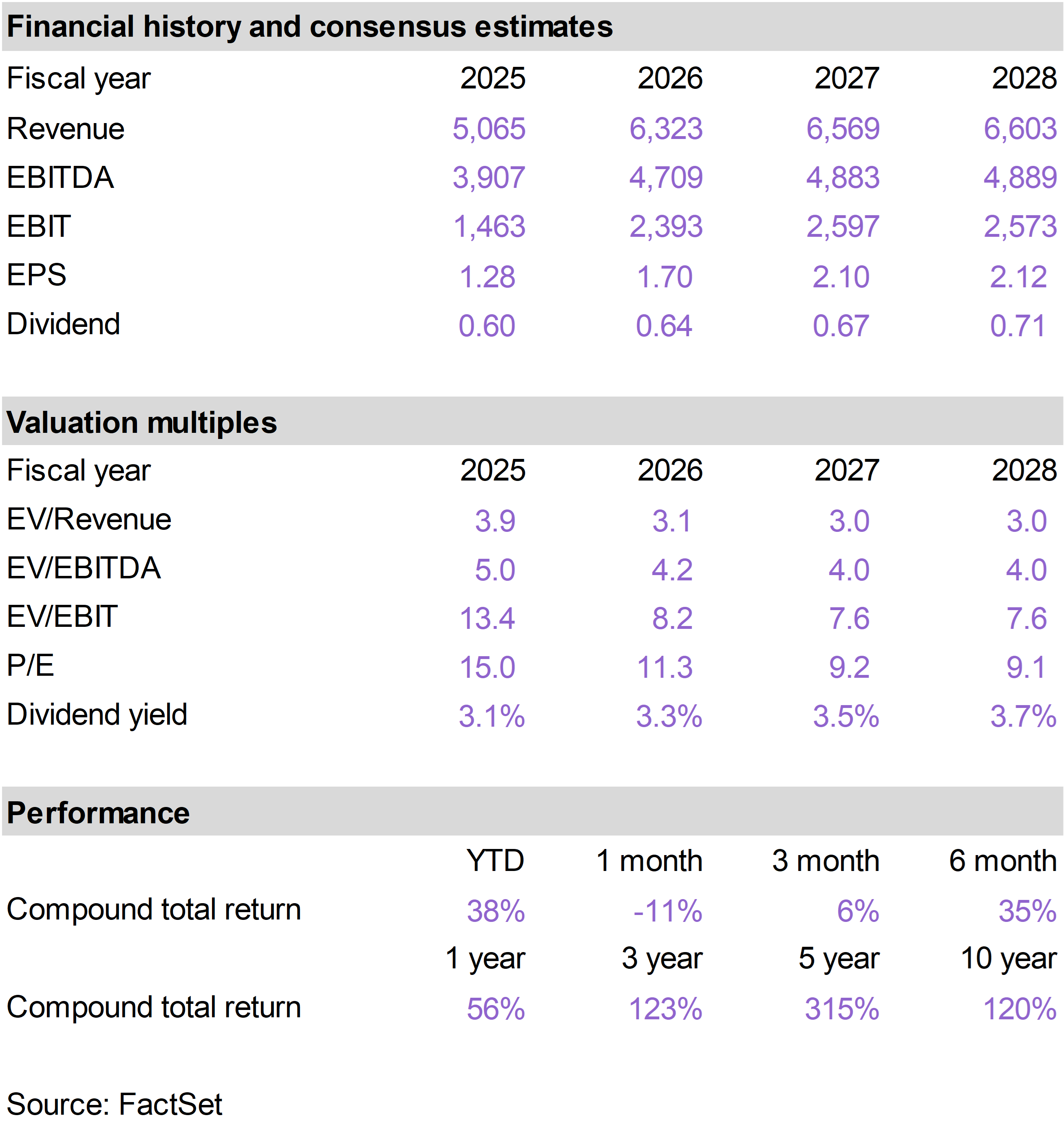

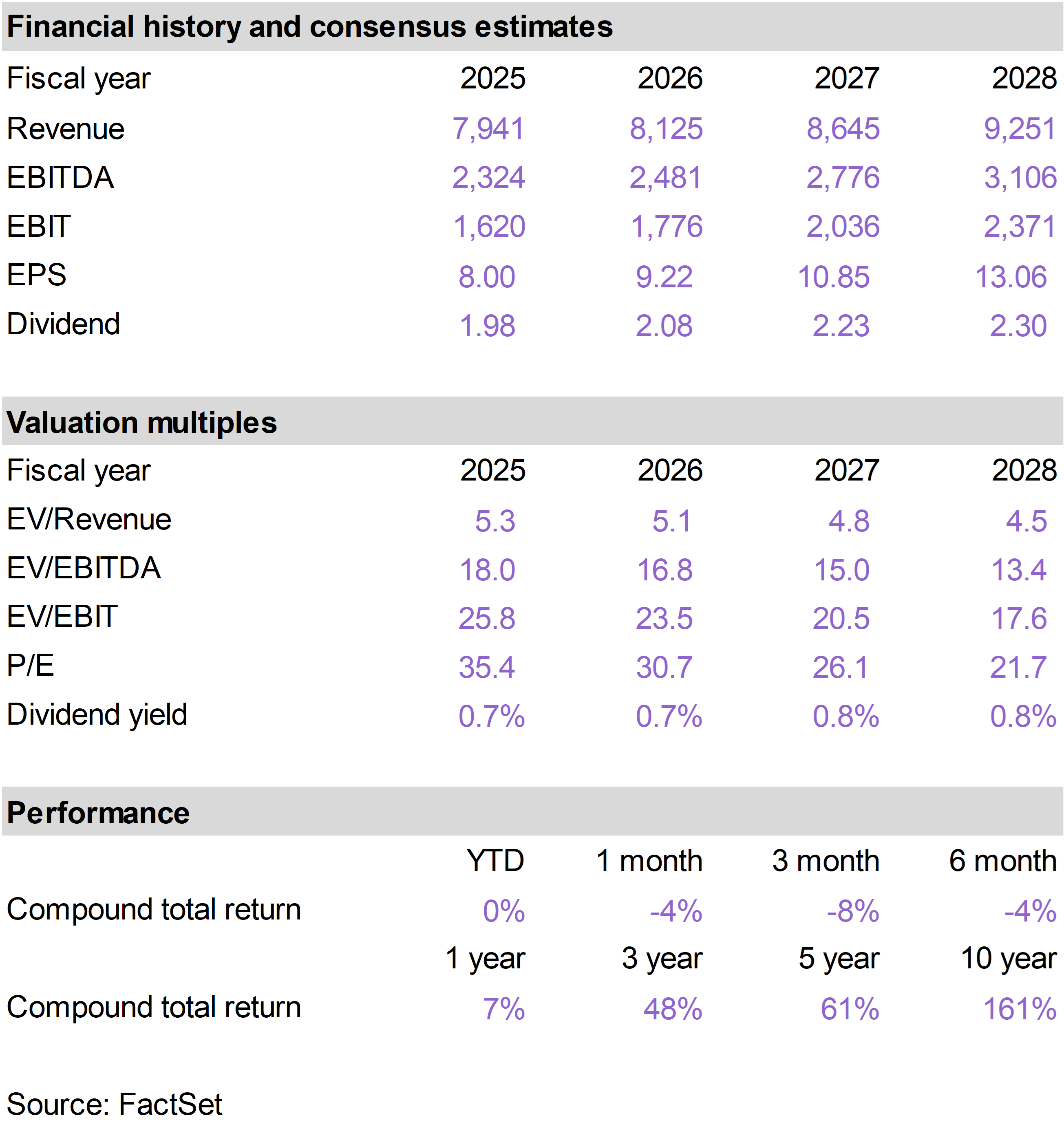

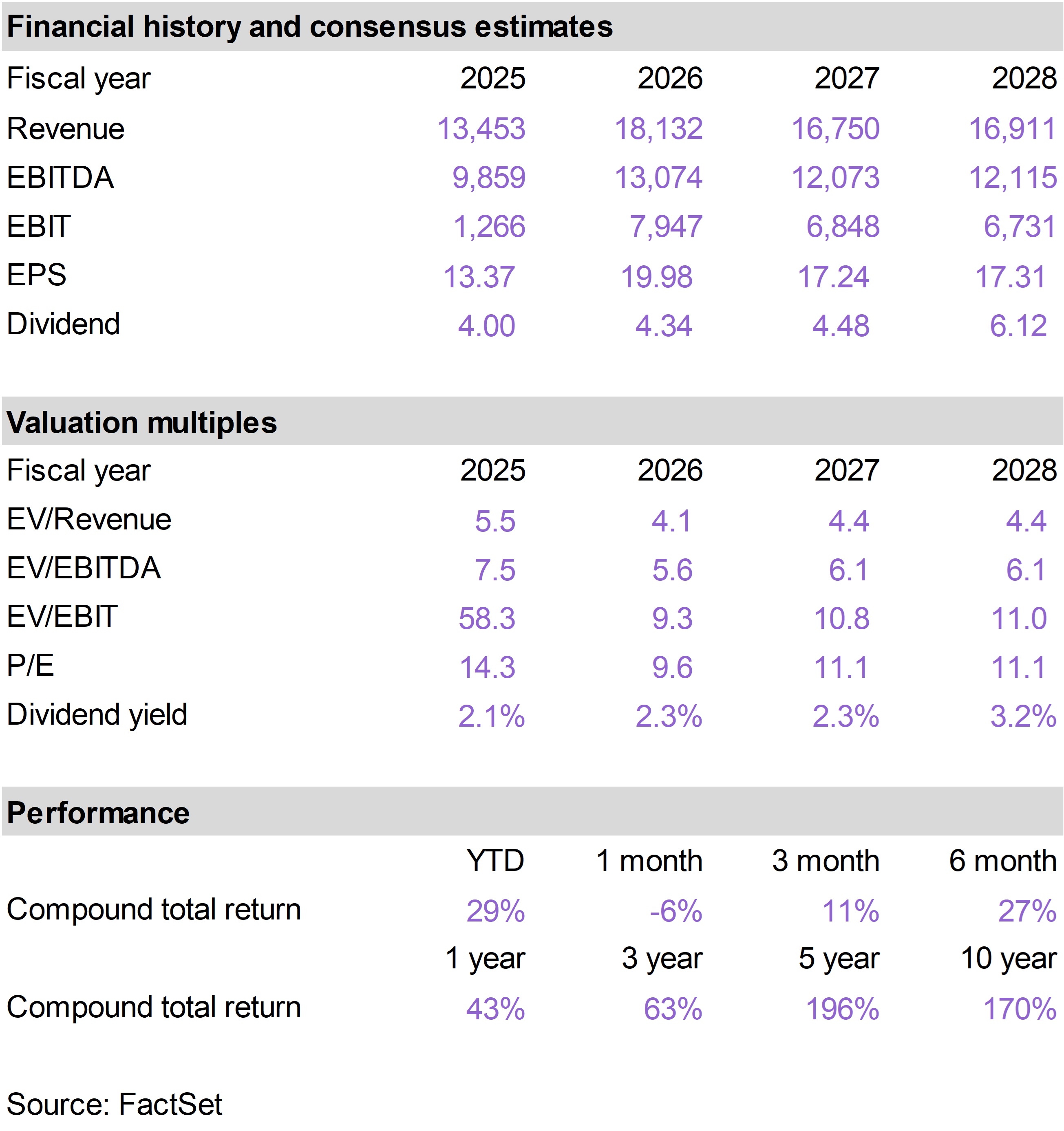

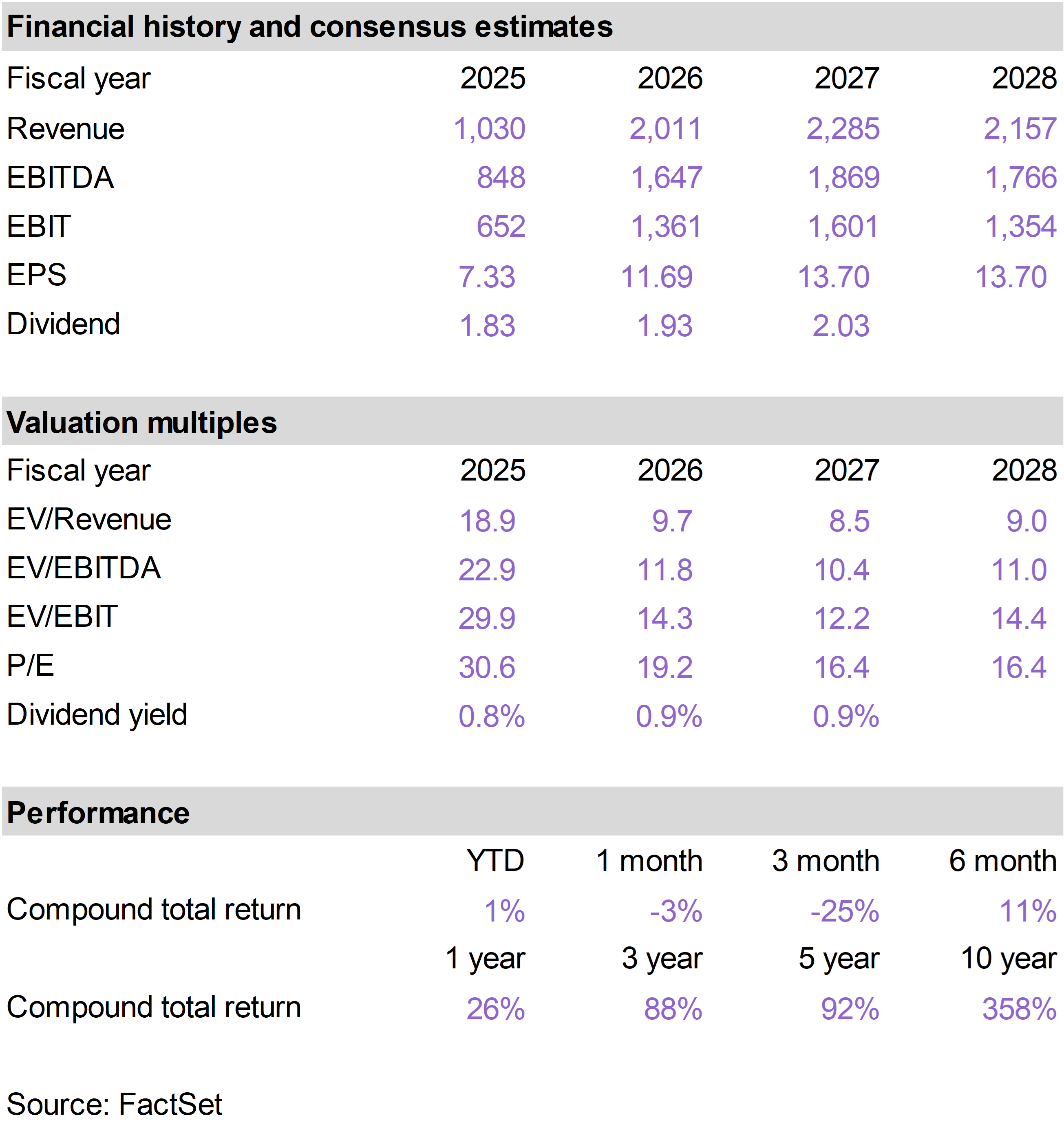

| | | Major stock indexes performed well in May, as several leading Technology stocks delivered exceptional earnings results. The S&P 500 advanced 5.3%, but the gains were not evenly distributed. The Tech sector returned 20%, while the majority of industry sectors actually had negative returns. With crude oil prices retreating below $95 per barrel by the end of the month, Energy was the worst performing sector. The Inflation Protection portfolio generated a 0.9% return. On a year to date basis, the portfolio has returned 15.5%, versus 11.3% for the S&P 500. Circle (CRCL) led portfolio performance with a 24% gain as the CLARITY Act progresses through Congress and on the heels of a strong earnings report. Oil and gas producers Permian Resources (PR) and Diamondback Energy (FANG) declined despite solid execution, reflecting lower crude prices. Our holdings across the portfolio continue to exercise strong pricing power based on supply constraints and dominant market positions.

|

|

| | | The Inflation Protection portfolio returned 0.9% in May, versus the S&P 500 Index return of 5.3%. On a year to date basis through the end of the month, the portfolio has generated a total return of 15.5%, versus the 11.3% return of the S&P 500.

The portfolio’s top performing stocks this month were Circle Internet Group (CRCL), which returned 24%; Freeport-McMoRan (FCX), which returned 14%; and TransDigm (TDG), which returned 8%.

The largest portfolio detractors were Permian Resources (PR), which returned -11%; Diamondback Energy (FANG), which returned -6%; and Vulcan Materials (VMC), which returned -6%. |

|

|

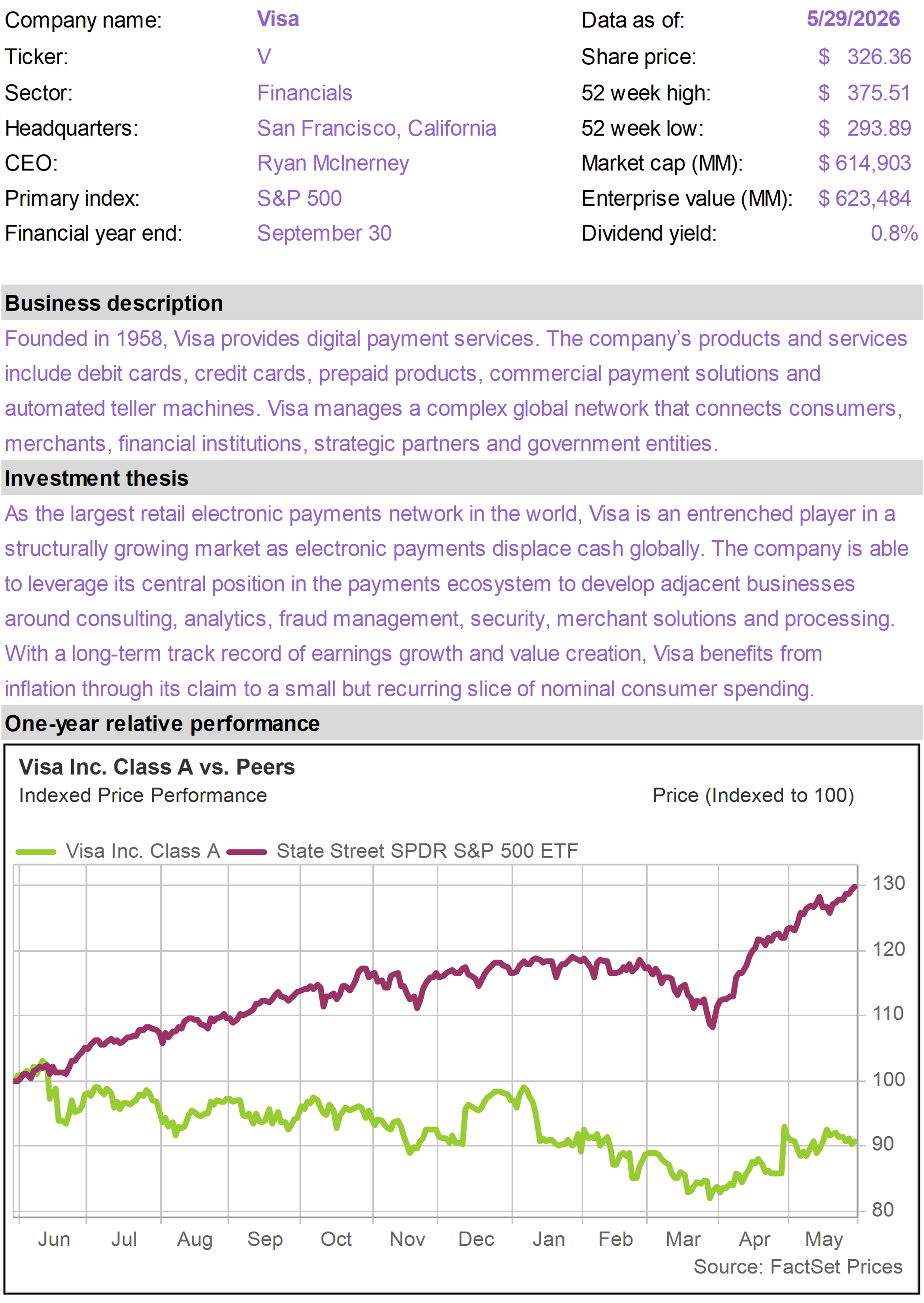

Tech dominates again

Investors in Technology stocks were once again the big winners in May. For the second straight month, the Tech holdings of the S&P 500 Index generated a 20% total return.

Tech, which now represents just under 39% of the entire index, effectively accounted for more than 100% of the total gain of the index this month.

All other sectors generated either marginally positive or negative performance. In fact, despite the strong overall performance of the index, most industry sectors (8 out of 11) actually delivered a negative result. |

|

|

|

Tech performance was extremely strong, but it was driven by a small group of stocks. Notably, among large-cap tech stocks with greater than 0.5% representation in the S&P 500, Micron (MU) returned of 88%, Advanced Micro Devices (AMD) returned 46%, and Oracle (ORCL) returned 40%.

All three companies benefited from growing investor confidence in AI-related demand, especially in certain areas that may have been previously underestimated.

MU broke one trillion dollars in market cap as demand for High-Bandwidth Memory (HBM)—a critical component used alongside AI chips—continued to outpace expectations.

AMD surged after investors became increasingly optimistic that the company could capture a larger share of the rapidly expanding AI accelerator market.

ORCL surged on growing enthusiasm for its cloud infrastructure business, reversing doubts that have surfaced in recent months over the pace of its AI data center investments.

There were a number of other, somewhat smaller tech names that also performed extremely well as a result of surprisingly strong AI-related demand.

Dell Technologies (DELL), for example, gained sharply after reporting blowout results that highlighted accelerating demand for its AI-optimized servers. DELL was the single best performer in the index, returning 101% in May.

These companies illustrate how the AI boom is expanding beyond the most obvious beneficiaries and driving up earnings expectations for companies that occupy critical niches of the broader buildout.

In many of these cases, the market was caught off-guard by the sheer strength of demand, from memory and semiconductors to cloud computing and data center capacity.

Iran coming to a close?

Stock market returns in May were largely driven by company-specific earnings surprises, but the broader macro backdrop continued to improve with apparent progress toward a resolution in Iran.

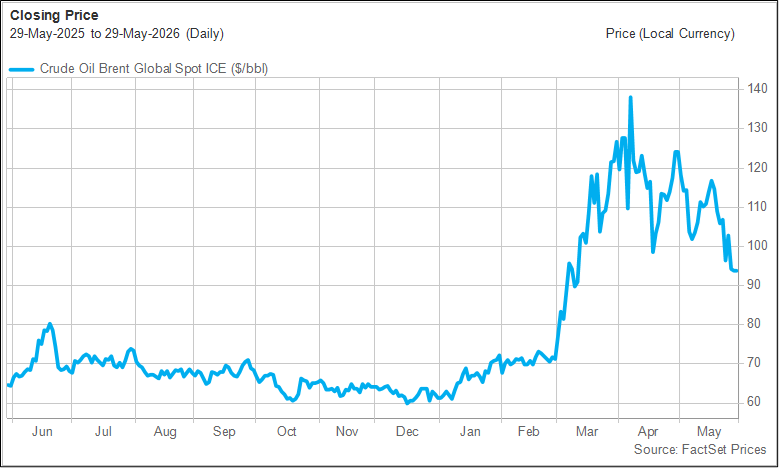

The ultimate barometer of progress in the Middle East is the price of crude oil. As markets sense an improved probability that the Strait of Hormuz will finally reopen and get back to normalized traffic levels, the price of oil drops.

Oil started the month over $120 per barrel and ended just below $95, the lowest level since mid-March. The decline followed a series of developments that suggested the conflict was moving toward de-escalation.

Over the course of the month, fears of a prolonged disruption in the Strait of Hormuz dissipated as reports emerged of backchannel negotiations between the United States and Iran and growing diplomatic efforts by Gulf states to broker a settlement.

As progress toward a ceasefire became increasingly apparent, the geopolitical risk premium embedded in oil prices began to fade. By the end of the month, investors were increasingly pricing in a diplomatic resolution, helping drive crude oil below $95 per barrel. |

|

|

|

Brent Crude Oil($/barrel - Last 12 Months) |

|

|

Energy stocks were the worst performing sector in May, declining 6%. The decline reflects lower oil prices and likely some unwind of hedge positions in the sector that investors established over the course of the conflict.

While the normalization of the situation in the Persian Gulf has taken longer than most investors would have liked, we remain optimistic that the Trump administration is committed to bringing the disruption to an end.

Rate volatility

Strong tech earnings ultimately led to a positive result for the stock market as a whole in May, but investor sentiment was negatively affected by bond market volatility.

Long-term bond yields spiked in the middle of the month, feeding concerns that higher interest rates could eventually weigh on economic growth and stock valuations.

The yield on the 30-Year Treasury bond broke through 5% in May, almost getting as high as 5.2% in the middle of the month, levels not seen in years. |

|

|

|

30-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

|

The primary catalyst was the sharp rise in oil prices towards the middle of the month as negotiations with Iran appeared to break down. Bond investors were also responding to the April Consumer Price Index (CPI) report, which showed inflation rising to 3.8%, its highest level in roughly three years.

The inflation report primarily reflected the direct impact of the spike in oil prices on gasoline prices and other energy expenses, which accounted for the vast majority of the increase.

As oil prices later receded, Treasury yields stabilized, removing an important headwind for equities.

The sharp decline in oil prices has also had an impact on perceptions on future rate cuts. The higher than expected inflation report fueled speculation that rather than continuing on the rate-cutting path, the Federal Reserve may even have to hike rates.

Following the pattern of the 30-Year, short-term interest rates rose slightly in the middle of the month before retreating.

One-Year Treasury yields still remain about a quarter-point higher than where they were before the war in Iran started.

With the Fed funds rate currently set within the 3.5% to 3.75% band, and One-Year Treasury yields just below 3.8%, the bond market is signaling that there is at least the potential for an additional rate hike in the next 12 months. |

|

|

|

One-Year Treasury Yields—Last 12 Months(Source: FactSet) |

|

|

A positive inflation surprise?

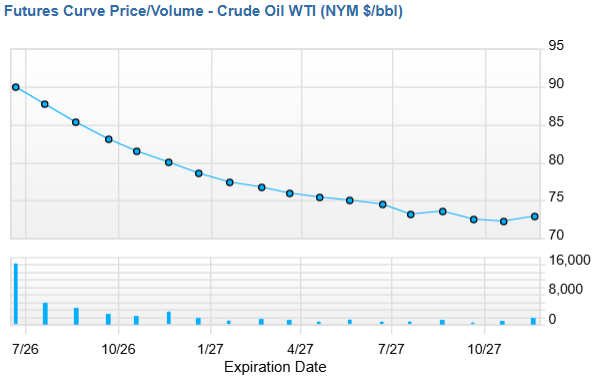

With oil prices still elevated relative to pre-war levels, and heavy spending on AI leading to some supply constraints (for example, in memory), the market remains focused on inflation risk.

While the mood toward inflation is currently cautious, there are reasons to be optimistic.

Futures markets price in significantly lower oil prices going forward, suggesting we are on a path toward lower energy costs. As spot oil prices come down, it is possible that forward pricing could come down even further. |

|

|

|

Crude Oil Futures Curve(Source: FactSet) |

|

|

From a more long-term perspective, the energy crisis we have experienced over the past several months is likely to produce a significant supply response.

Higher oil prices will encourage greater oil production and, over a multi-year period, the creation of new pipelines that bypass the Strait of Hormuz.

On the other hand, heavy spending on AI infrastructure is injecting demand into the economy for labor, commodities, and equipment. All of this is ultimately positive and pro-growth but likely contributes to short-term inflationary pressure.

But as Kevin Warsh begins his tenture as Fed Chair, we should not lose sight of one of his most important messages—that AI, as it gets deployed throughout the economy, has enormous potential to deliver increased productivity and thereby serve as a disinflationary force.

While the stock market has performed well on the back of strong earnings growth, rising inflation risk, manifesting as rising long-term interest rates, has been a headwind.

Any sign that inflation risk is receding over the course of the year could allow the new Warsh Fed to get back on the rate-cutting path. This in turn could serve as a meaningful source of support for the market, particularly sectors outside of technology that stand to benefit from relief on interest rates. |

|

| | |

The top performing stocks in the Inflation Protection portfolio this month were Circle Internet Group (CRCL), which returned 24%; Freeport-McMoRan (FCX), which returned 14%; and TransDigm (TDG), which returned 8%.

The worst performing stocks in the portfolio in May were Permian Resources (PR), which returned -11%; Diamondback Energy (FANG), which returned -6%; and Vulcan Materials (VMC), which returned -6%. |

|

| |

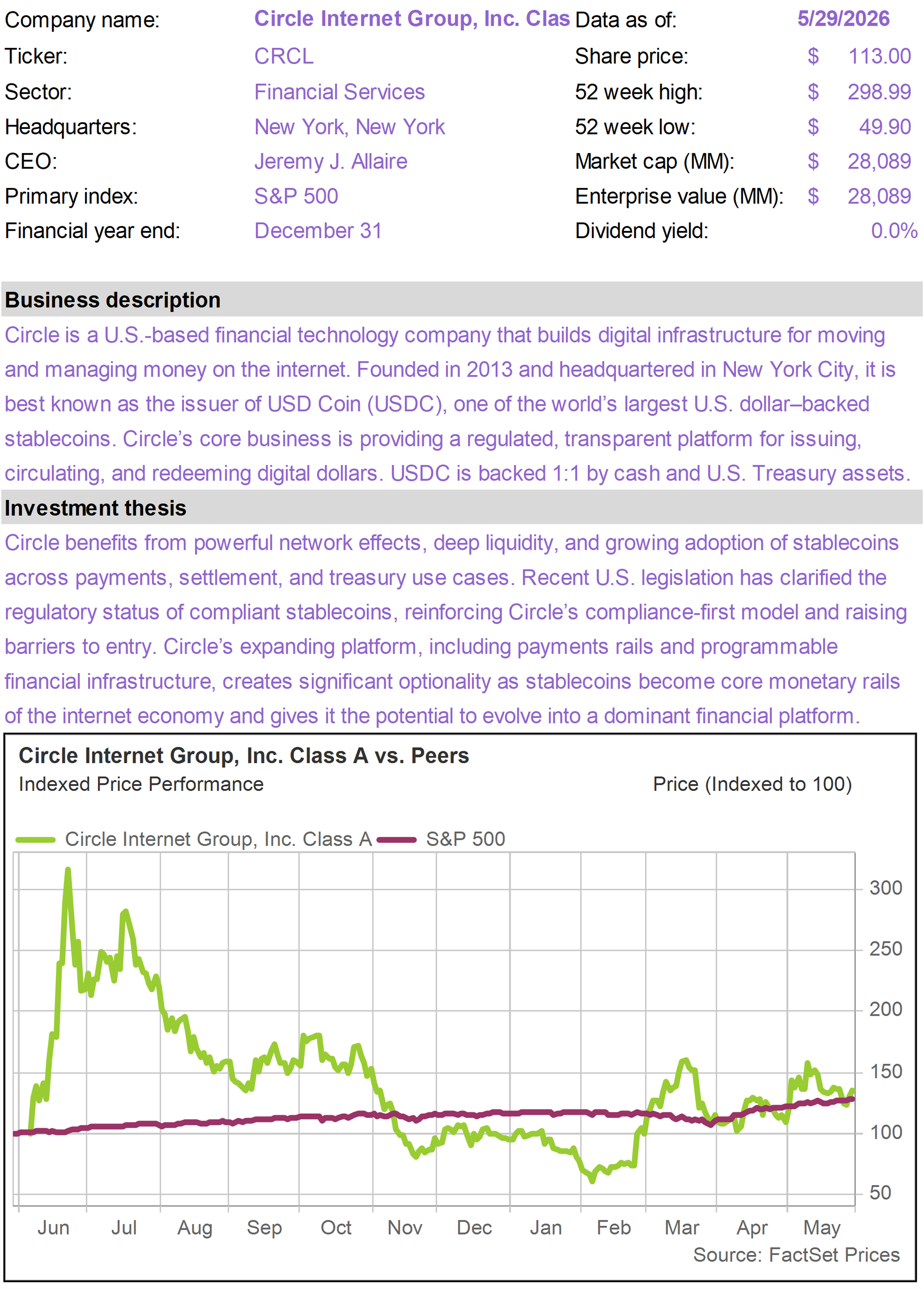

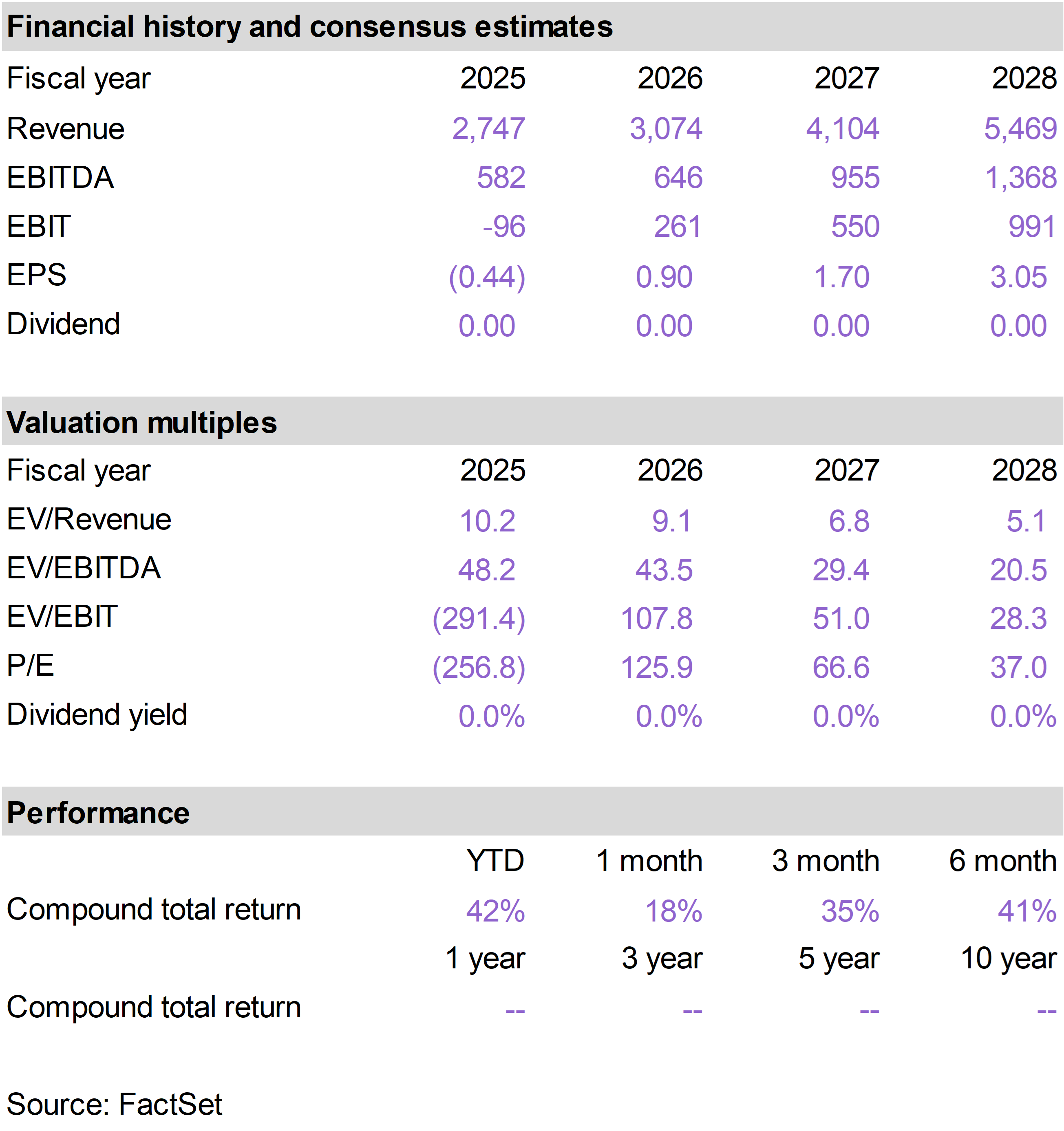

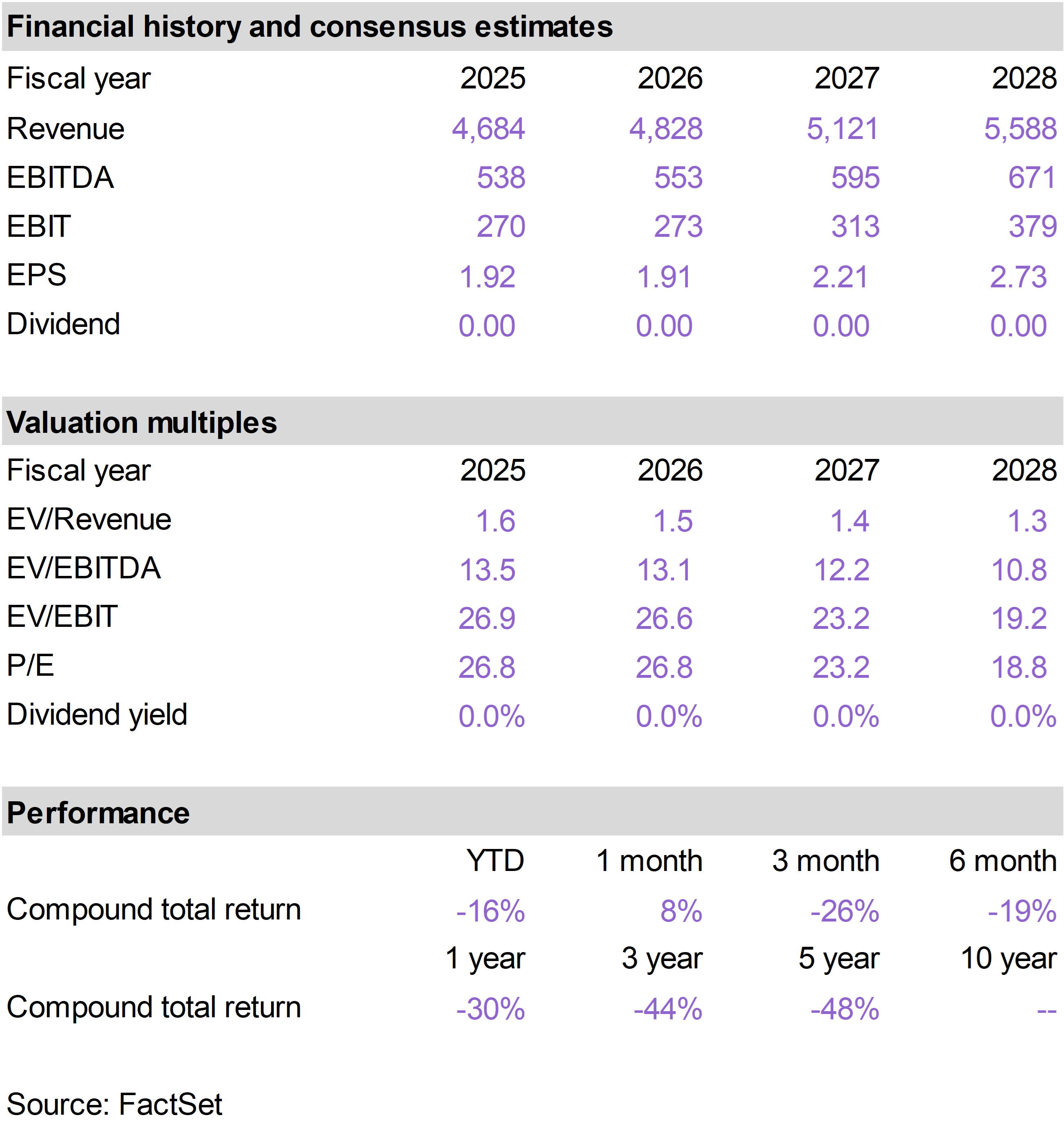

Shares of CRCL performed well in May due to a combination of favorable regulatory developments and a strong earnings report.

On the regulatory front, the CLARITY Act moved closer to becoming law after advancing through the Senate Banking Committee with bipartisan support. Investors increasingly view the legislation as a potential turning point for the digital asset industry.

In particular, investors took comfort that the dispute over stablecoin yield will be resolved in an acceptable manner. Under the anticipated compromise, holders of CRCL’s USDC stablecoin will be able to earn rewards that are similar to interest payments on bank savings accounts.

The company's first quarter earnings report also helped boost sentiment. CRCL exceeded earnings expectations and demonstrated that demand for USDC remained resilient despite weakness in broader crypto markets.

Management also highlighted several new growth initiatives. CRCL announced the successful $222 million presale of its ARC token, implying a network valuation of roughly $3 billion, while also highlighting progress on new payment, settlement, and transaction services built on its blockchain platform.

We view CRCL as one of the most innovative and well-positioned players in digital finance, targeting enormous long-term addressable markets. As stablecoins, tokenized assets, blockchain payments, and AI-driven commerce gain adoption, CRCL stands to benefit from multiple growth drivers. |

|

| |

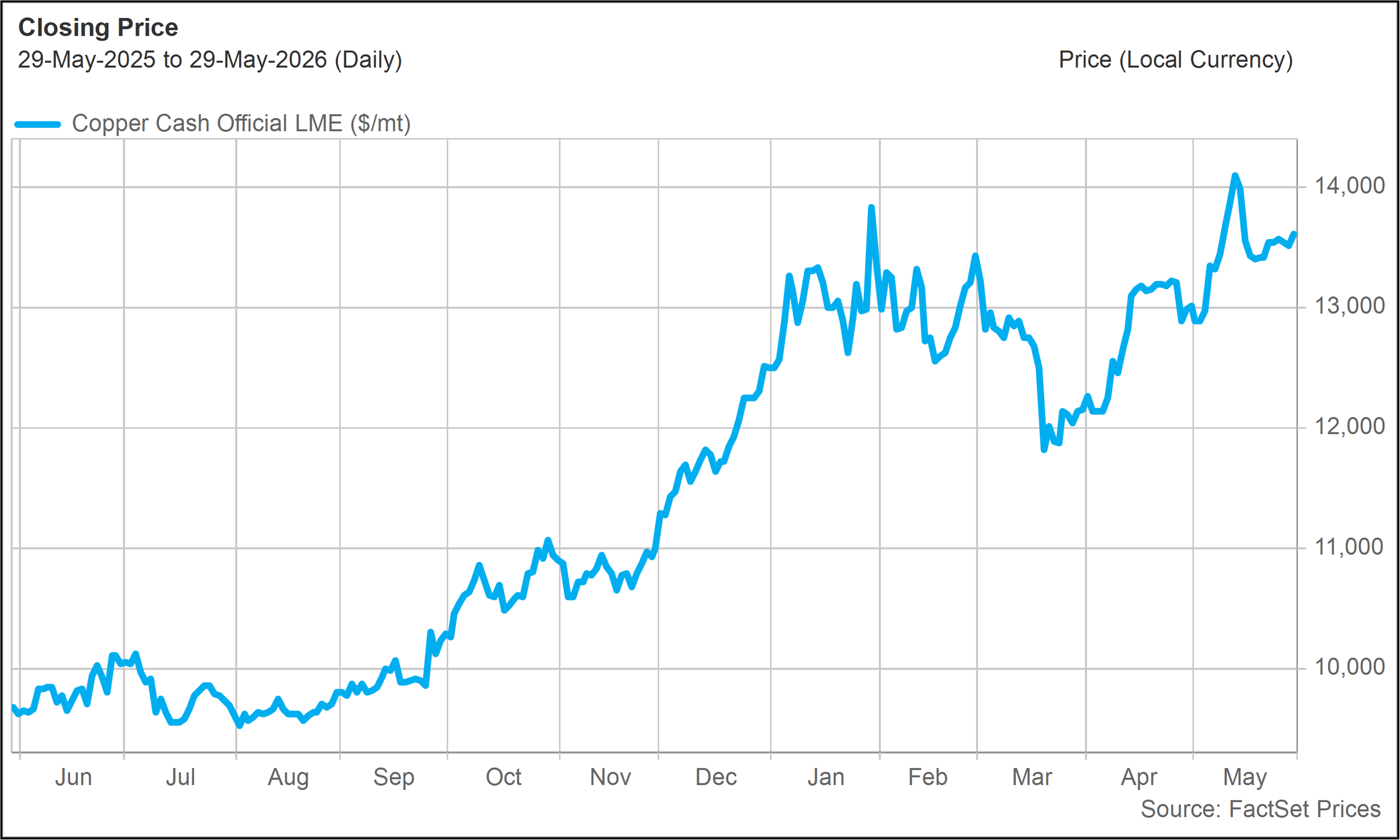

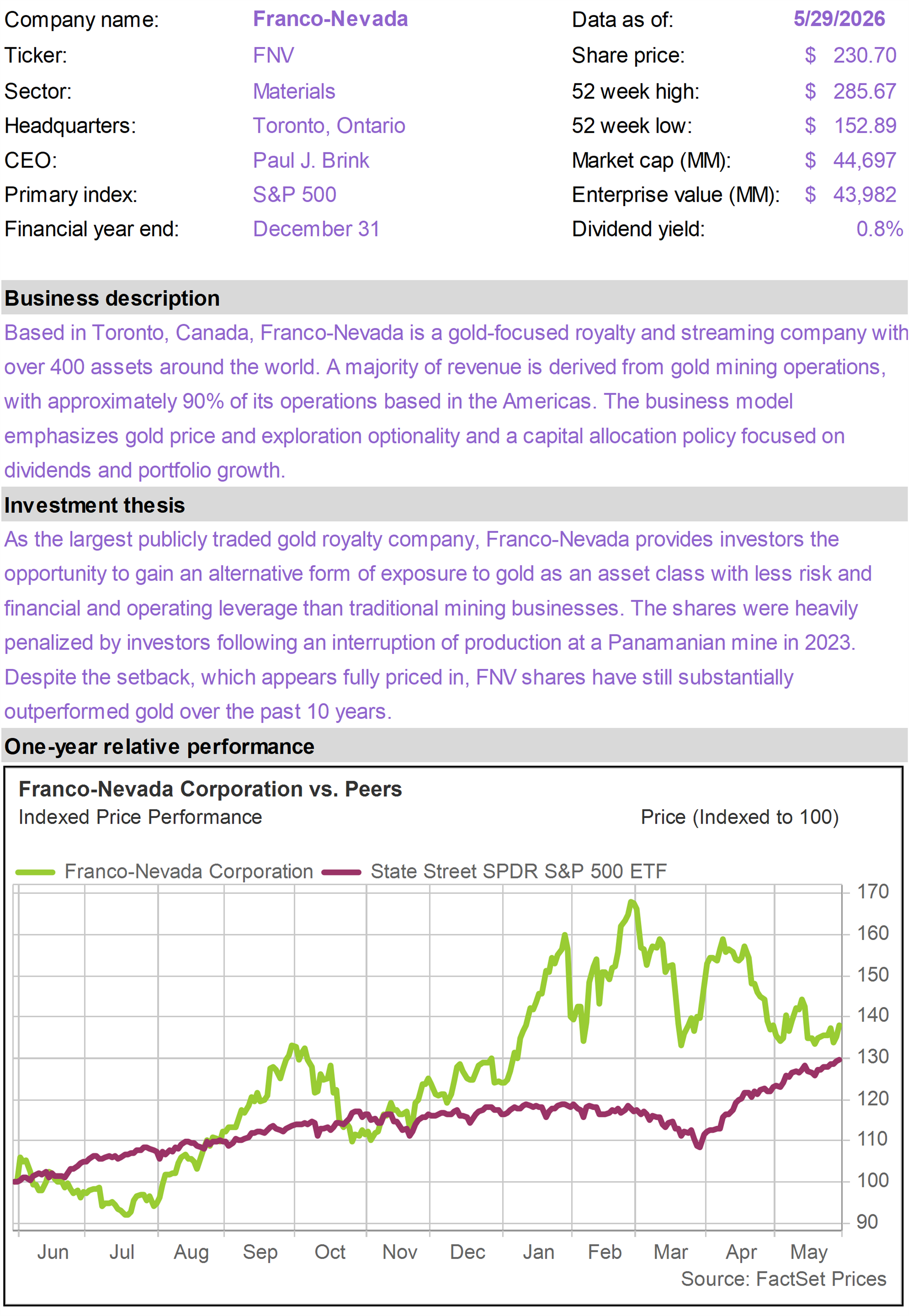

FCX continues to benefit from rising copper prices as one of the premier copper mining platforms accessible to public market investors.

Copper is directly relevant to several of the most powerful investment themes in the market today. The metal is essential for electrification, power transmission, data centers, electric vehicles, and the broader buildout of AI infrastructure.

As global electricity demand continues to rise, future copper supply will struggle to keep pace, especially given extremely long lead times on mining operations (often more than a decade). |

|

|

|

Copper - $/Metric Ton(Last 12 Months) |

|

|

FCX owns some of the world's most valuable copper assets, including the massive Grasberg mine in Indonesia.

With few large-scale copper projects scheduled to come online in the coming years, copper prices may continue to rise, creating an even more favorable environment for established producers like FCX. |

|

| |

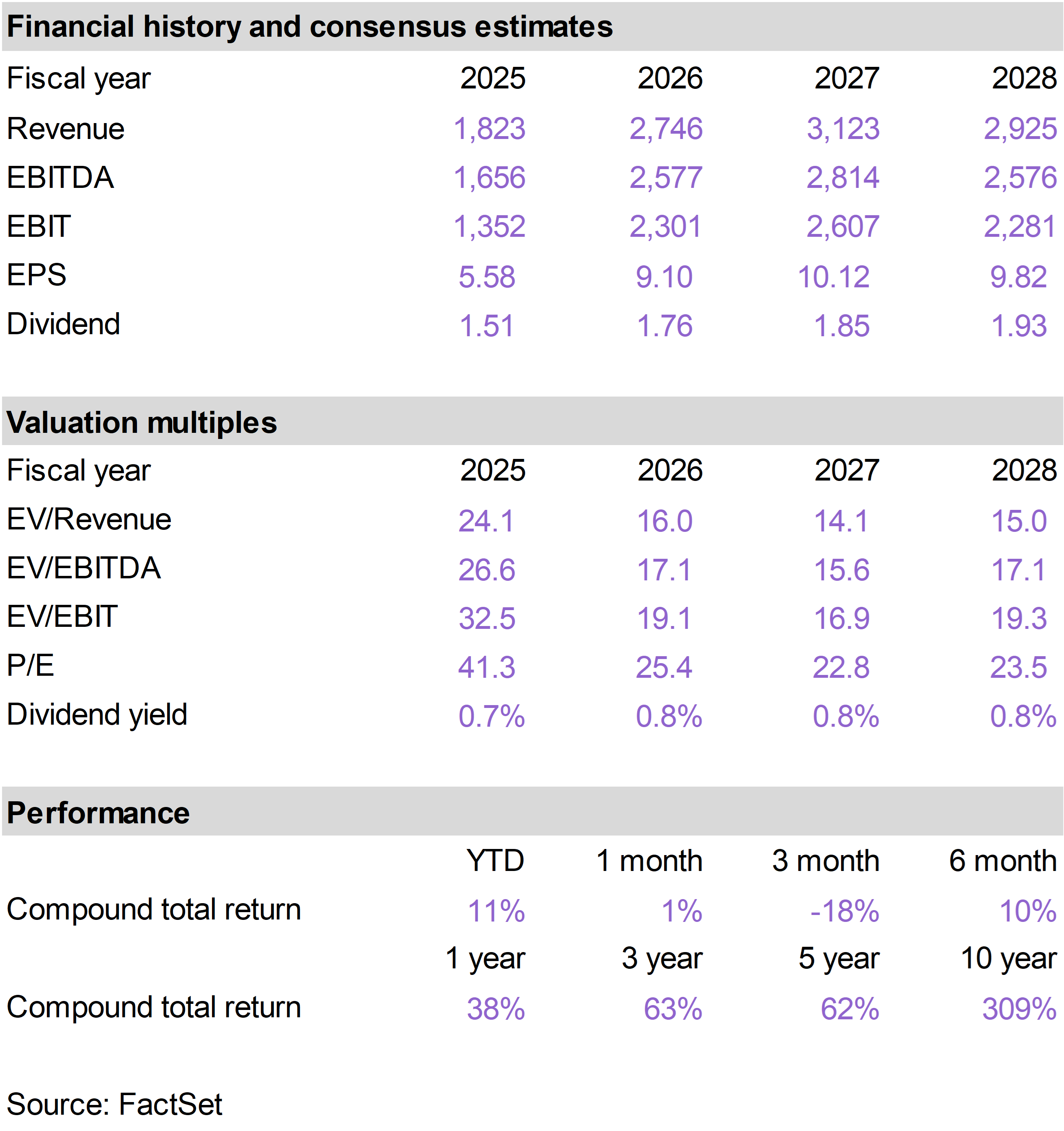

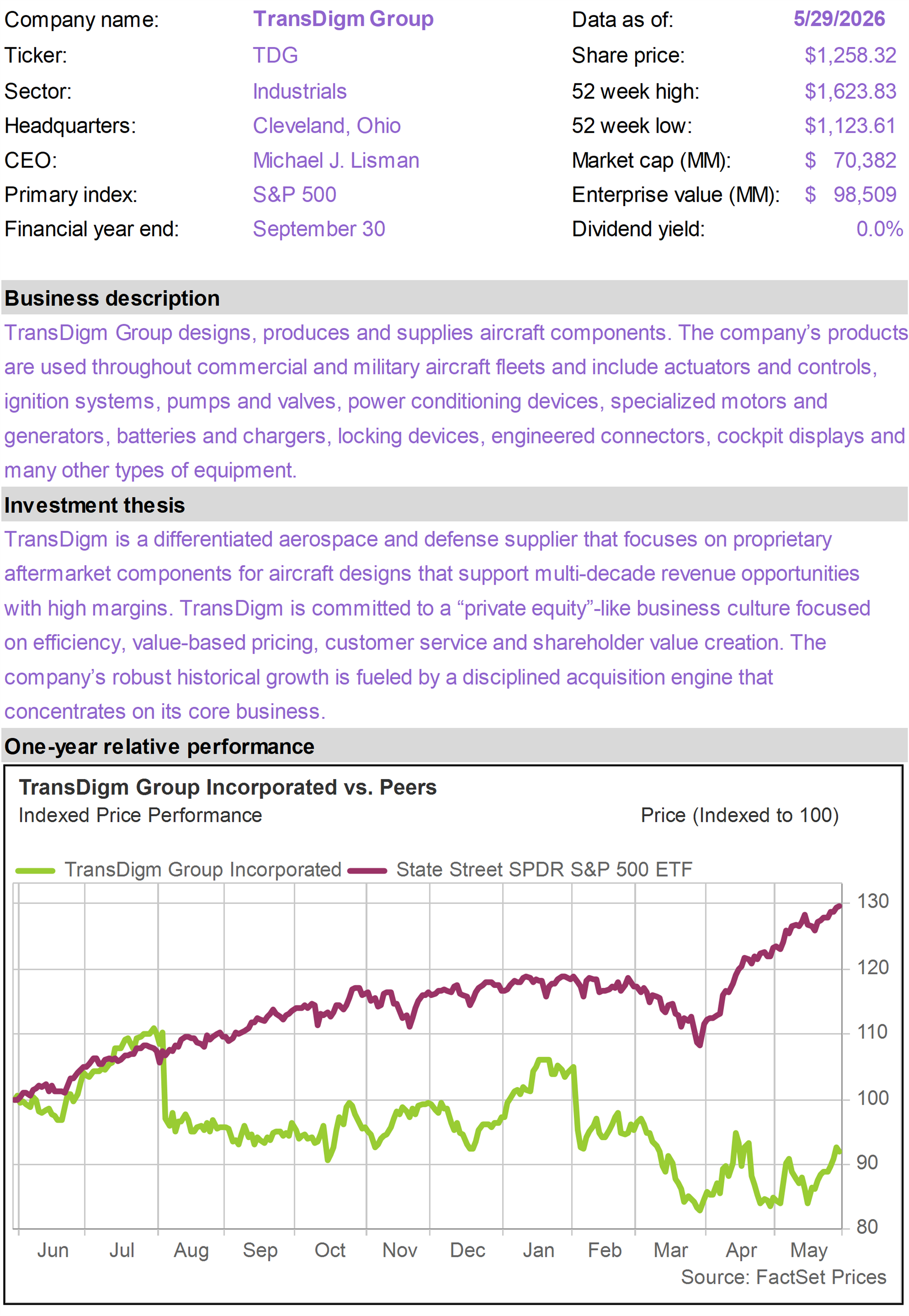

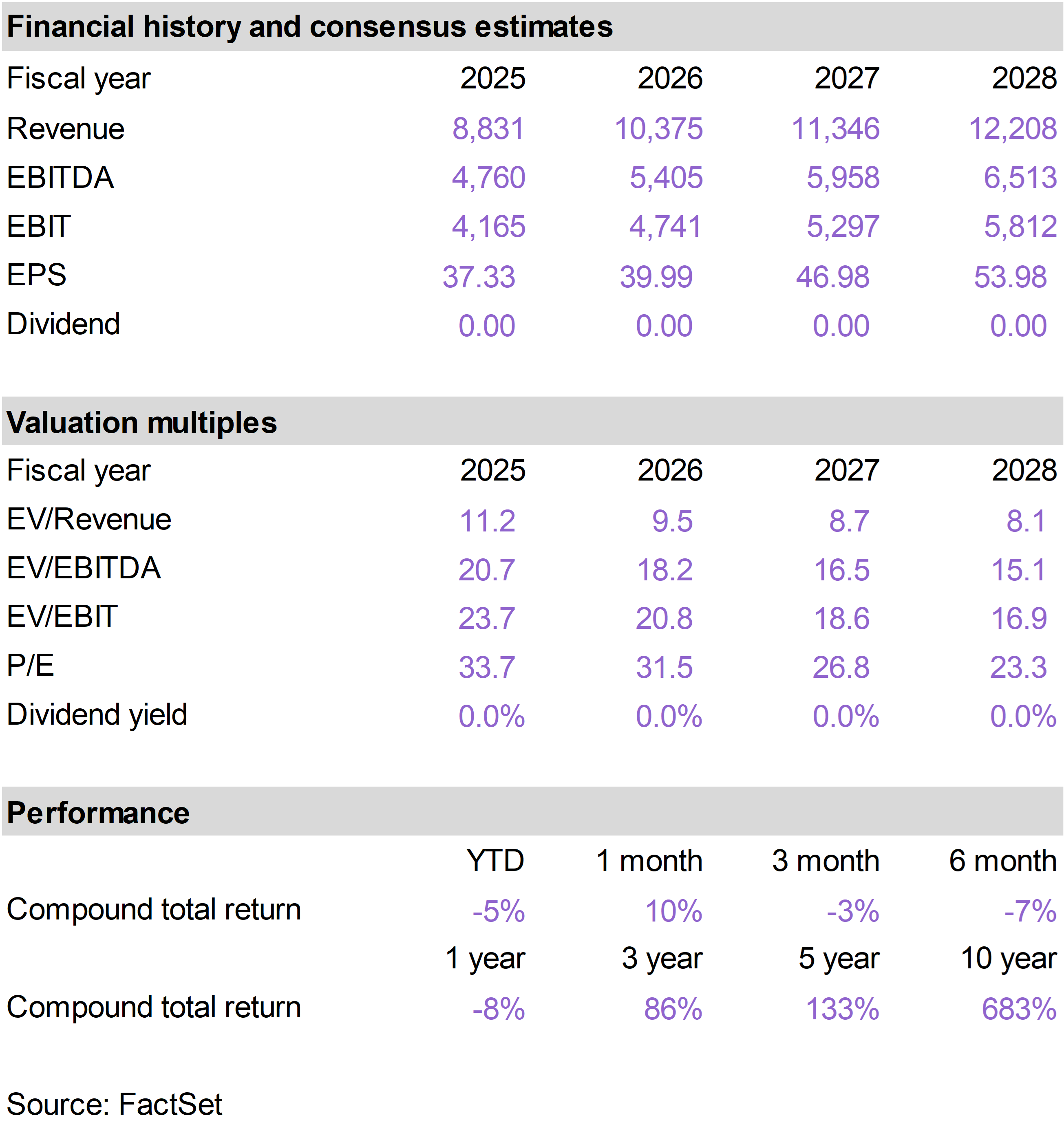

TDG shares advanced after a strong first quarter earnings report that demonstrated broad-based strength across the business.

Commercial aftermarket revenue accelerated to 14% organic growth, while both the defense and commercial segments also delivered double-digit growth. Management responded by raising guidance across all three end markets.

Perhaps most encouraging was the resurgence in the company's highly profitable aftermarket business. Commercial air travel remains strong, airline maintenance spending continues to recover, and distributors reported robust demand for replacement parts.

Because aftermarket revenue carries substantially higher margins than original equipment sales, accelerating aftermarket growth has an outsized impact on profitability.

We continue to view TDG as one of the highest quality businesses in the aerospace sector.

The company owns thousands of proprietary components that are critical to aircraft operation but represent only a small fraction of an airline's overall operating costs. This creates significant pricing power and allows TDG to generate exceptional margins and free cash flow.

Importantly, management continues to deploy that cash flow into acquisitions that expand the company's portfolio of proprietary aerospace products. Over time, this acquisition strategy has created a powerful flywheel of revenue growth, pricing power, and margin expansion that has consistently generated attractive returns for shareholders. |

|

| |

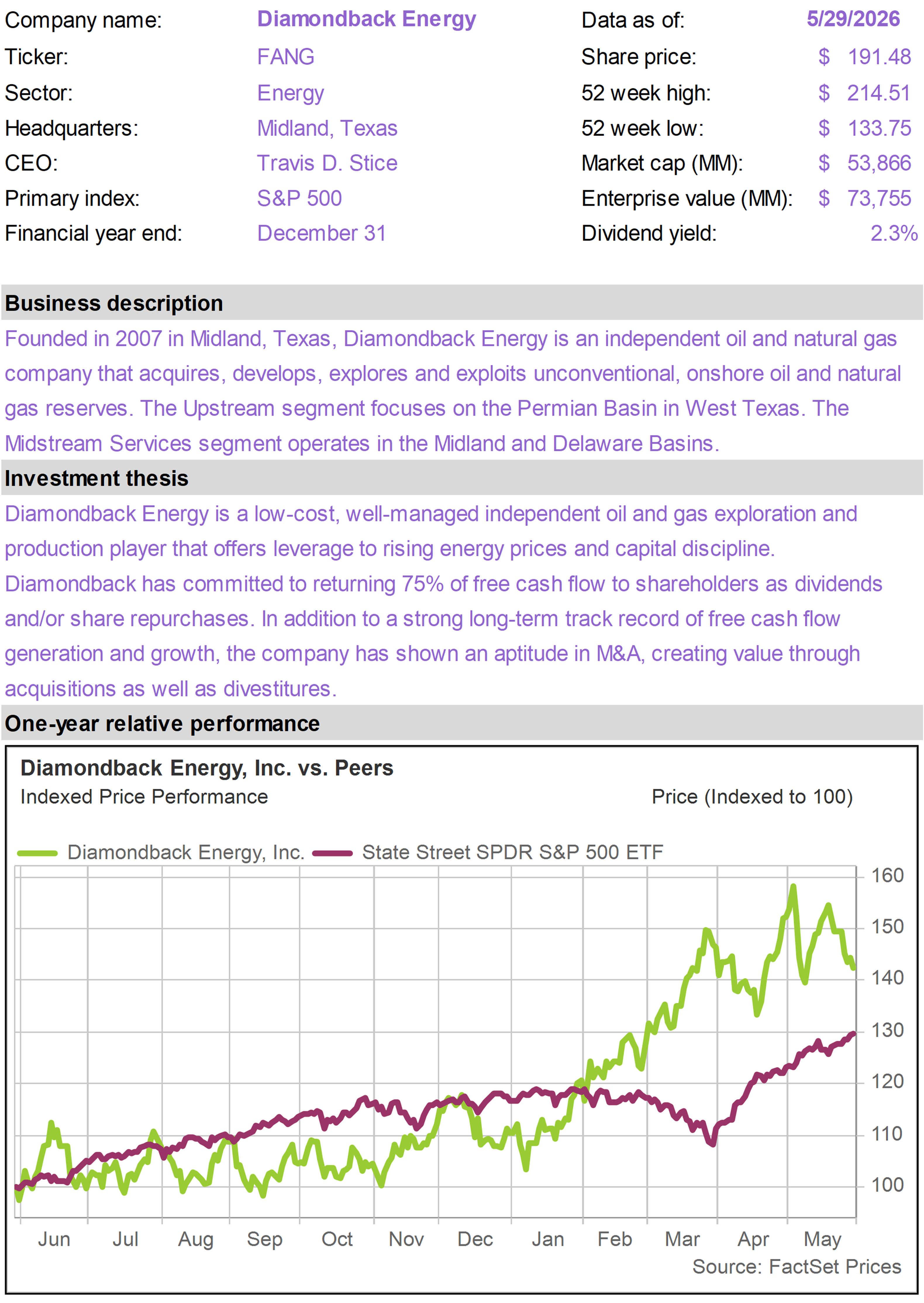

Both PR and FANG retreated this month as oil prices declined and the energy sector lagged, following an extended period of outperformance.

While oil prices are inherently volatile, we continue to view both companies as compelling long-term beneficiaries of U.S. energy dominance, supported by attractive assets, strong balance sheets, and significant free cash flow generation.

PR reported a strong first quarter in May, increasing its full-year oil production outlook while maintaining spending discipline. Management highlighted continued improvements in drilling efficiency and indicated that the company has the flexibility to grow production further if market conditions remain favorable.

PR continues to generate substantial cash flow while maintaining a strong balance sheet and preserving flexibility for future acquisitions.

FANG also delivered impressive results. Management expressed confidence in the company's ability to grow production in the current environment of higher oil prices, while keeping costs under control, a reflection of its high-quality acreage and operational scale.

The company continues to generate significant free cash flow, rapidly reduce debt, and build financial flexibility. We were also encouraged by management's willingness to adapt its capital allocation strategy, emphasizing long-term value creation over rigid shareholder return formulas.

In our view, both companies remain exceptionally well positioned. They own attractive assets, generate significant cash flow, and have management teams that have demonstrated an ability to allocate capital effectively through both strong and weak commodity environments. |

|

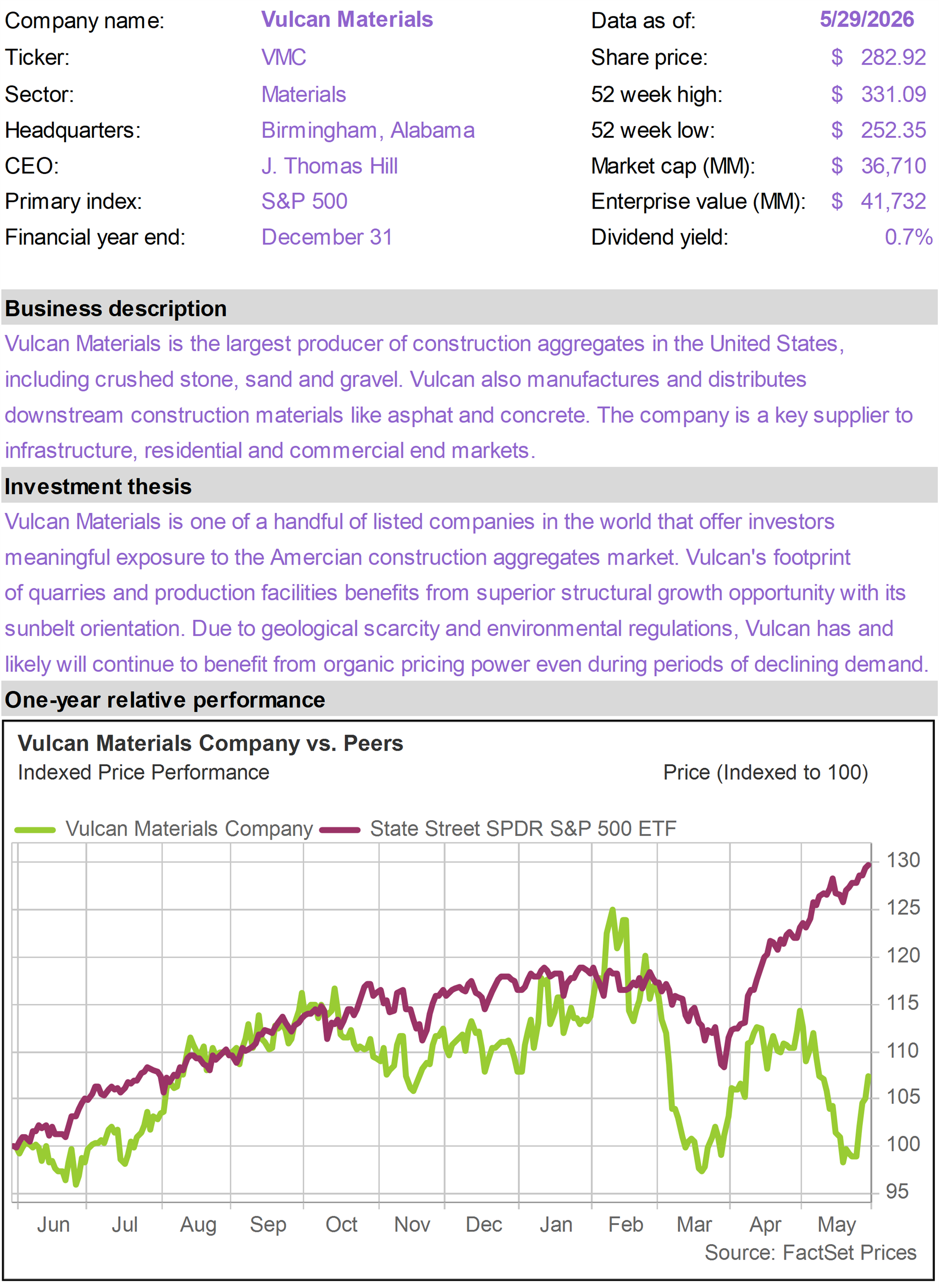

| |

Shares of VMC declined this month despite the company delivering another strong earnings report at the very end of April. First quarter results exceeded expectations, driven by higher shipment volumes, continued pricing strength, and margin expansion across the business.

The stock's weakness appears to have been driven less by company-specific issues and more by investor concerns that the spike in oil prices during the month could pressure profitability going forward.

Fuel and energy represent important input costs for quarry operations, transportation, asphalt production, and concrete manufacturing. As oil prices surged following tensions in the Middle East, some investors worried that higher energy costs could weigh on margins.

We believe those concerns may be overstated. Management noted that energy-related surcharges are already in place in portions of the business, while pricing discussions with customers began earlier than usual to address rising fuel costs. As a result, the company continues to expect margin improvement over the remainder of the year.

Higher fuel costs have the potential to pressure margins in the short-term but also reinforce local pricing power. The all-in cost of acquiring stone from competitors at more distant quarries becomes increasingly prohibitive for customers as shipping costs rise.

Management also indicated that demand tied to data center construction is beginning to have a measurable impact on results, an important trend to watch.

VMC generates substantial free cash flow, which it is now returning to shareholders through an accelerated share repurchase program. While the stock pulled back during the month, we continue to view VMC as a long-term beneficiary of America's ongoing investment in infrastructure, power, and AI-related construction. |

|

| | | |

| | |

| | |

| | | |

|

| | |

|

| | Mid-America Apartment (MAA) |

|

|

|

| | |

|

| | |

|

| | |

|

| | Circle Internet Group (CRCL) |

|

|

|

| | Diamondback Energy (FANG) |

|

|

|

| | Floor & Decor Holdings (FND) |

|

|

|

| | |

|

| | |

|

| | |

|

| | WESCO International (WCC) |

|

|

|

| | Wheaton Precious Metals (WPM) |

|

|

|

| | The 76research Inflation Protection Model Portfolio emphasizes business models that benefit from inflationary pressure. Holdings are typically selected from industries based on supply constrained real assets, including commodity and energy businesses, or companies that otherwise demonstrate superior pricing power. Drawing from an investable universe of expected inflation beneficiaries, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

|