The China problem

Shares of NVDA traded down a few percentage points in after-market trading immediately after the earnings release. The share price has fluctuated around yesterday’s closing levels as of Thursday morning.

Investors and analysts appear mainly concerned about NVDA’s ability to do business in China, given U.S. government objections to sharing valuable technology with its main geopolitical rival.

Due to ongoing licensing reviews, NVDA conservatively excluded any revenue from China from its guidance for next quarter. The company did, however, indicate several billion dollars of potential revenue upside if the approvals come through.

The number two AI market in the world after the U.S., China is certainly an important market for NVDA—and one with high growth potential, which NVDA estimates in the 50% range.

On the call, Jensen Huang explained how he continues to make the case to the administration about “the importance of American companies to be able to address the Chinese market” in order to “lead and win the AI race.”

The big picture

We urge investors not to become too distracted by the ongoing political dynamic with China.

The administration appears to be working on a path forward that balances America’s interest in having the world standardize around U.S. technology without giving away sensitive intellectual property.

For long-term investors, what really matters is the scale and scope of the global AI infrastructure build-out and NVDA’s ability to maintain its enormous share of that spending.

China aside, NVDA once again demonstrated this quarter that it is the key player in a multi-trillion dollar investment wave.

Despite the China headwind, NVDA still surpassed estimates. Revenue grew by 56% on a year over year basis and 6% sequentially.

Many investors think of NVDA as a “chip” company. If you frame your understanding of the business this way, it may diminish your appreciation for the business’s long-term potential.

As Jensen Huang emphasized on the earnings call last night, NVDA is really an AI infrastructure company, integrating a wide range of chips and systems to help companies build and run AI data centers.

He estimated that if it costs about $50 billion to build a 1 gigawatt AI data center, NVDA typically collects about $35 billion. As he put it, “what you get for that is not a GPU.”

You are getting supercomputers that are powering an “AI factory.”

NVDA’s competitive edge

NVDA’s dominance in AI infrastructure stems from its early lead as a pioneer in graphics processing as well as the software ecosystem that has developed around it.

The software that runs NVDA hardware is known as Compute Unified Device Architecture (CUDA).

A proprietary programming model, CUDA has been around for some 15 years and is deeply entrenched with developers, enterprises and researchers.

With so much AI technology based on the CUDA platform, the system creates an extremely hard to penetrate competitive moat for NVDA equipment. Switching costs are very high.

Given that there is practically insatiable demand for AI compute capacity, competitors and even customers will nonetheless continue to work towards making chips that compete with NVDA Graphic Processing Units.

This is a threat that should be taken seriously. But NVDA will continue to innovate and evolve, following the same pattern of the other dominant technology platform companies.

Businesses like Microsoft (MSFT), Amazon (AMZN) and Meta Platforms (META) are now practically unrecognizable, in terms of their product offerings and revenue streams, relative to the companies they were a decade ago.

As we discussed in our latest AI thought piece (Surviving and Thriving in the AI Economy), we are still in the early days of the AI revolution.

NVDA is the undisputed technology leader in AI. Even investors who are concerned about NVDA losing GPU market share should have confidence in the company’s ability to grow in new directions over time, even if those paths are not totally visible right now.

How about valuation?

NVDA clearly has immense long-term potential, but it also sports a $4.4 trillion valuation. This single company’s market cap exceeds the total public company market caps of every nation in the world other than the the U.S., China and Japan.

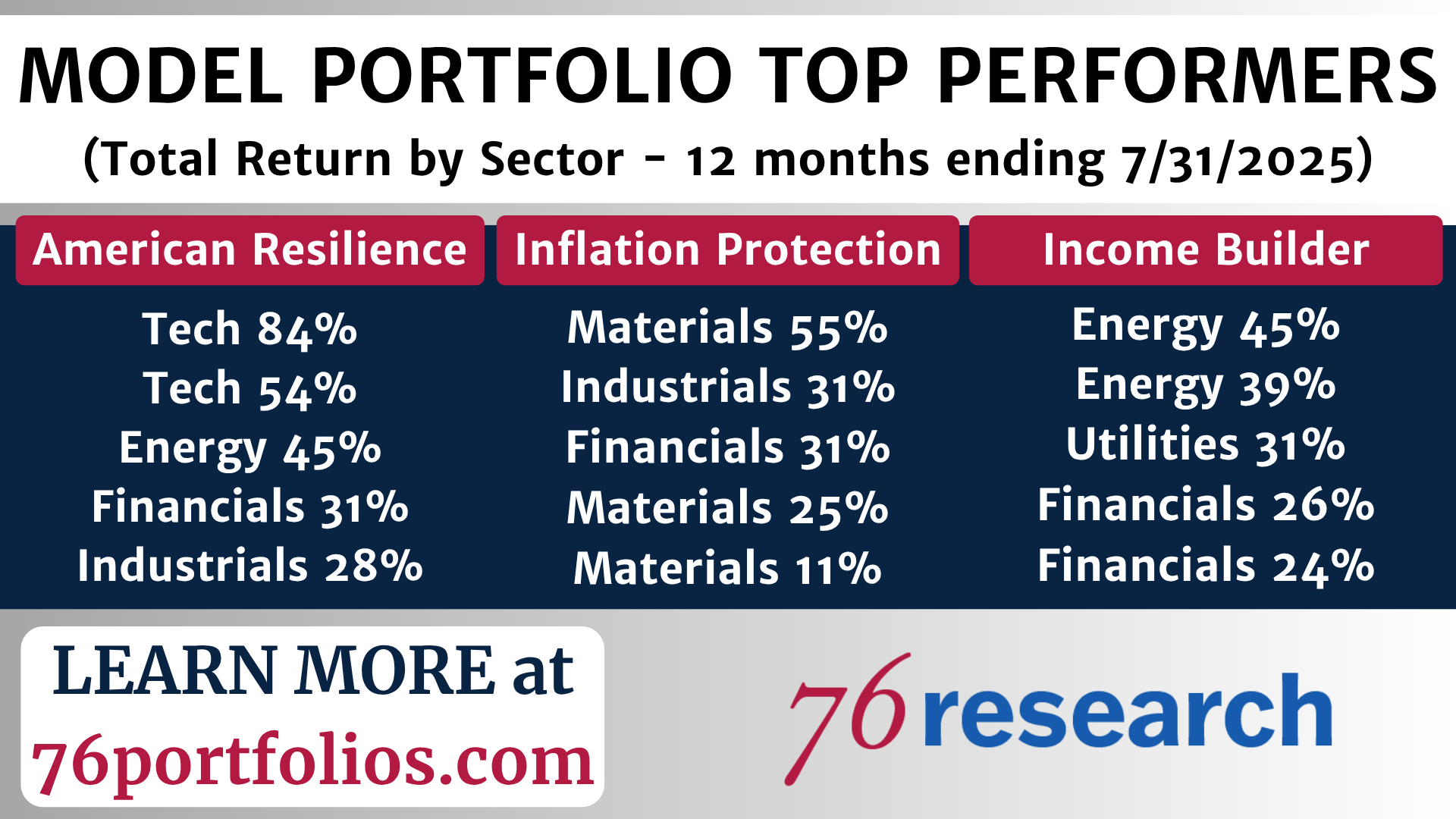

When we added NVDA to the American Resilience Model Portfolio on March 12, 2025 (NVIDIA: The Time Has Come), it was a moment of deep pessimism.

We had the emergence of the (misperceived) DeepSeek threat amidst developing concerns over tariffs that would only intensify in subsequent weeks.

We felt the valuation at that moment was extremely compelling. The shares have since recovered and established new highs, gaining more than 50% in less than six months, versus approximately 15% for the S&P 500.