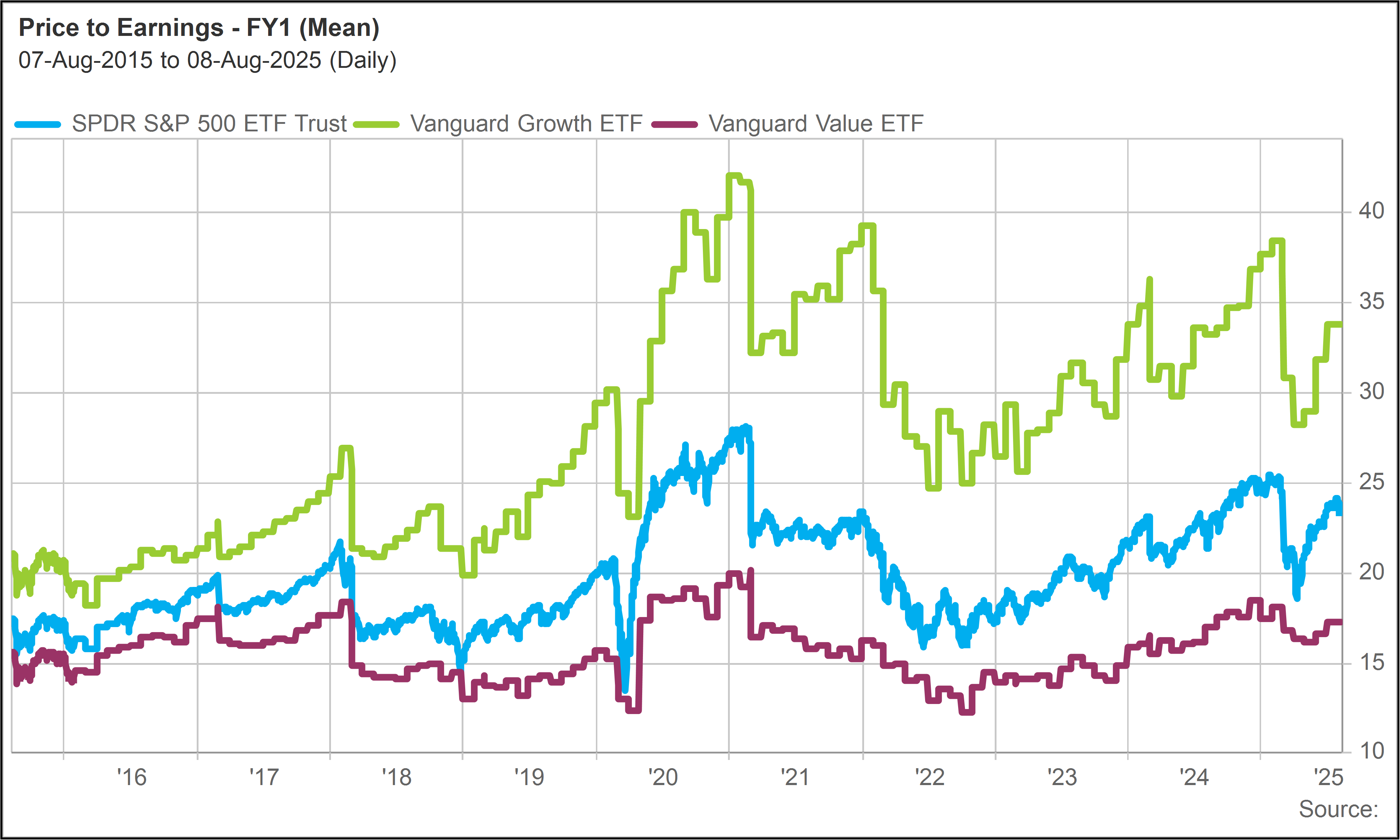

Growth stock earnings multiples have advanced sharply from April levels, but, at 30 to 35 times, are in the middle of the range they have occupied for about the past five years.

It is true that growth stock earnings multiples have expanded since the first half of the past decade, when they were more like 20 to 30 times. But in retrospect, those multiples woefully understated the growth potential of the companies they applied to at the time.

Meanwhile, the forward earnings multiple of the value component of the S&P 500, at around 15 to 20 times, is completely in line with levels that have prevailed over the past decade.

The multiple on the overall index is slightly higher, driven primarily by the growth component.

Shifting monetary policy

In addition to tariff impacts, investors have been concerned about labor market weakness and pressures on the consumer. A disappointing jobs report led Trump to replace the economist who runs the Bureau of Labor Statistics, a move that has naturally stirred controversy.

While the economy overall seems stable and healthy, a closer look reveals what could be described as two parallel economies.

We see a tech-driven high-end economy that is benefiting from the AI boom and wealth effects. This portion of the economy is what tends to be disproportionately captured by the stock market.

Then there is the low-tech economy (housing, autos, consumer spending) that is being held back by high interest rates.

To the extent we see labor market weakness in the private sector, this appears to be taking place in the low-tech economy.

While companies like Meta (META) drop pay packages worth hundreds of millions on AI superstars, working class Americans, whose savings were eviscerated by the post-Covid inflation wave, are struggling with high rates on mortgages, auto loans and credit card balances.

To the extent this labor market weakness persists, this will allow the pendulum to shift more in the direction of easier monetary policy and rate cuts. The high-tech names that dominate the S&P 500 may not need a rate cut, but they will benefit from it.

Selecitivity is key

Investors should always be worried about valuation but need to maintain broader perspective. Yes, stocks have moved up sharply since April, but the S&P 500 is only up about 9% since the start of the year—a healthy rise but not an extreme move.

The stock market as a whole was clearly too cheap in April. The opportunity to buy the dip in the S&P or the NASDAQ has passed.

While valuations are not currently extreme, they are definitely fuller, so it makes sense in the current environment to be more careful in terms of where one picks one’s spots.

We continue to be encouraged by many positive factors.

AI represents an innovation wave that is following its own trajectory, largely independent of macroeconomic forces. Growth in AI is led by tech juggernauts with exceptional balance sheets and cash flow that are making long-term investments in the future.

Not all tech stocks will necessarily benefit from AI, however.

Shares of graphics software giant Adobe (ADBE), for example, are down nearly 25% year to date. With AI models producing incredible graphics for free or at very low cost, investors have grown concerned that ADBE will be disrupted by AI rather than benefit from it.

AI has the potential to drive productivity higher, which will likely be good for the economy and stock market as a whole, but there will be some casualties along the way among legacy business models, which need to be avoided.

Meanwhile, as reasonable trade deals get done and favorable inflation data flows through, tariff-related risks are subsiding.

And then there is the prospect of rate cuts, which may be needed to support job growth in the low-tech portion of the economy—and possibly even the high-tech portion, as AI replaces engineers and computer programmers.

Staying the course

After a period of sharp gains, there is a natural psychological instinct to “lock in profits.” Behavioral economists call this the disposition effect.

While we discourage long-term investors from attempting to time the stock market as a general matter, we see the recent upside as validation of an attractive economic backdrop, rather than an indicator of risk.

Within our Model Portfolios, we remain cognizant of somewhat elevated valuations but remain focused on the solid long-term fundamentals that underpin these investments—and in many cases are only looking stronger.