Geopolitical instability. Macro uncertainty. The collapse of the international order. Risk-off.

As news broke over the weekend of a U.S. military operation in Venezuela, these were the words splashed across financial media.

President Trump’s decision to capture Nicolas Maduro through a high-stakes military operation was widely expected to rattle markets and send investors scrambling for cover.

That was the script. But a funny thing happened on the way to Monday’s open: stocks were heading higher.

Even with futures pointing decisively up before the opening bell, Bloomberg—perhaps the most widely read financial news source among institutional investors—described markets as “jittery.”

Then the market opened. And stocks kept going up.

The S&P 500 finished solidly in the green not just on Monday, but again on Tuesday, leaving many observers confused. One major news service suggested that investors have simply grown accustomed to “shrugging off” macro and geopolitical risks altogether.

That explanation misses the point.

What much of the financial commentary failed to recognize—as it often does—is that American assertiveness on the global stage is not a negative for markets. It is often a positive.

Markets do not fear change per se. They fear indecision, incompetence, and unmanaged risk. The investment world does not want chaos, but it also does not necessarily want the status quo either. It wants clarity, leadership, and progress.

Most of all, the investment world wants a strong America.

Many journalists and even Wall Street strategists seem to view Trump and his America First foreign policy as a dangerous wild card. But their biases and opinions ultimately do not matter.

What matters is what real people, with real money, choose to do. And on balance, they bought rather than sold.

Why Venezuela is important

For years, Venezuela represented a lingering source of geopolitical and economic ambiguity: a sanctioned petro-state sitting atop the world’s largest proven oil reserves.

This resource-rich country of 30 million people, just a few hours by plane from Florida, has for more than a quarter century been ruled by a regime that was not only hostile to the United States, but also deeply embedded with America’s most significant adversaries.

There is not a single overriding reason that fixing Venezuela is strategically important for the United States. Rather, it is a combination of factors that are collectively quite meaningful, from energy markets and migration to homeland security, geopolitics, and stability across the Americas.

Venezuela has been a festering problem for the United States for decades. With Maduro removed, his successor, Delcy Rodriguez, now faces intense economic and military pressure to govern in a manner acceptable to the American government.

That pressure will center on clear priorities: restoring American property expropriated by the Chavez and Maduro regimes, revitalizing Venezuela’s oil sector through reintegration with global energy markets, and laying the groundwork for sustainable economic recovery for the Venezuelan people.

Remarkably, if these outcomes hold, the Venezuela problem may have been largely resolved—without the loss of a single American life.

The world’s largest oil reserves

Venezuela holds roughly 300 billion barrels of proven crude oil reserves, the largest in the world, representing about 17% of the global total. They are mostly found in the Orinoco Belt, with its heavy and extra-heavy crude deposits.

Venezuelan oil output peaked in the late 1990s around 3.5 million barrels per day. Currently, Venezuela is only producing around 1 million barrels per day, which is roughly 1% of total global crude oil production. For perspective, the U.S. as a whole now produces about 13.5 million barrels per day.

The decline in Venezuela’s oil output was driven by mismanagement, chronic underinvestment in infrastructure, and the country’s isolation from global capital and oil industry partners.

With heavy involvement and investment by global oil majors, Venezuela could realistically increase its crude oil output by 50% to 100% over the next 5 to 10 years.

This would not dramatically alter the global supply/demand picture, but on the margin it would give the U.S. reliable access to additional crude oil in its own backyard, reducing dependence on other foreign suppliers.

Likely impact on U.S. oil imports

U.S. Gulf Coast refineries are among the only facilities in the world equipped to handle heavy sour crude like Venezuela’s. They were largely built for that purpose—back when Venezuela was a reliable energy partner and before relations collapsed following the election of anti-American socialist Hugo Chavez.

The U.S. is net importer of approximately 7 million barrels per day of crude oil. The majority of that comes from Canada, which is highly reliable (notwithstanding recent frictions with the Canadian government).

If relations with Venezuela normalize and Venezuelan crude output expands, Venezuelan crude can become a meaningful component of the relatively small slice of American crude oil consumption, approximately 15%, that is not currently satisfied by U.S. and Canadian production.

In other words, there is an opportunity here to make U.S. almost completely oil independent in the sense of only requiring imports from highly reliable sources close to the border (Canada and potentially now Venezuela).

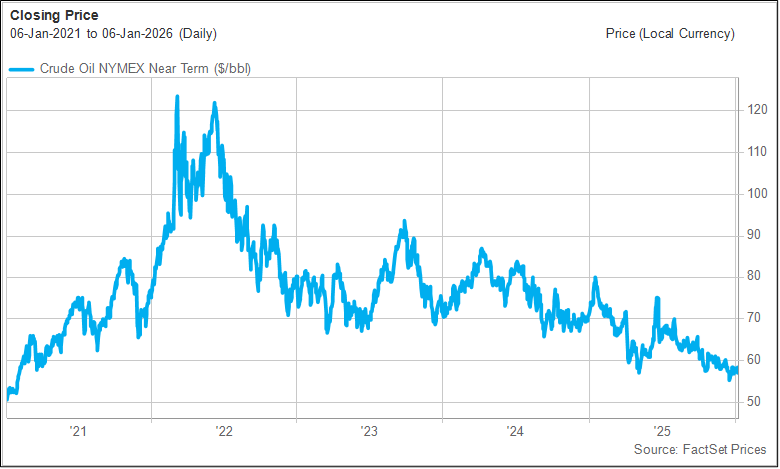

Gasoline ≠ oil

Gasoline is often conflated with oil, but the two are quite different. Oil is not consumed directly but has to be refined into usable fuels, like gasoline, diesel, and jet fuel.

The distinction has economic consequences.

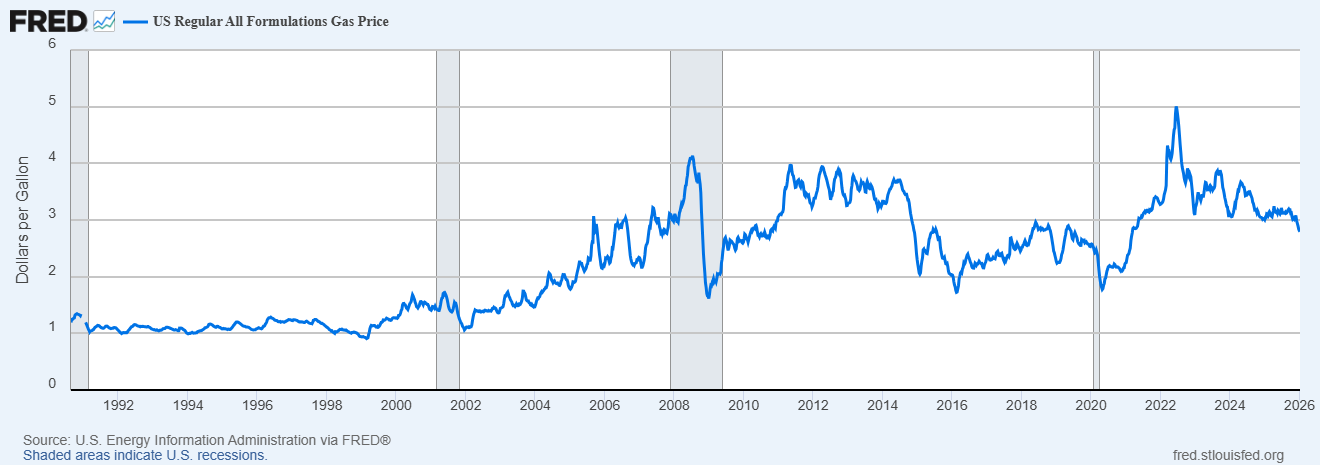

In the United States, the trajectory of gasoline prices can deviate significantly from the trajectory of global crude oil prices. This is mainly because U.S. refining capacity disproportionately requires heavier crude oil, like what is produced in Venezuela.

Prior to Chavez taking power in 1999, when Venezuela was producing nearly three times as much heavy crude as it does today, average retail gasoline prices were close to $1 for many years. Gasoline prices in the United States started to rise once the Chavez/Maduro era began.

Venezuelan oil may not be extremely important in the context of global supplies, but it is valuable to the United States in particular. The U.S. does not absolutely need Venezuelan oil but stands to benefit from its availability and abundance.