Yet NVDA is growing much faster than the index. Based on consensus forecasts, earnings per share are expected to rise 36% in 2027 and another 16% in 2028.

This far exceeds market expectations for S&P 500 earnings growth in the same time frame (approximately 10% to 15% per year).

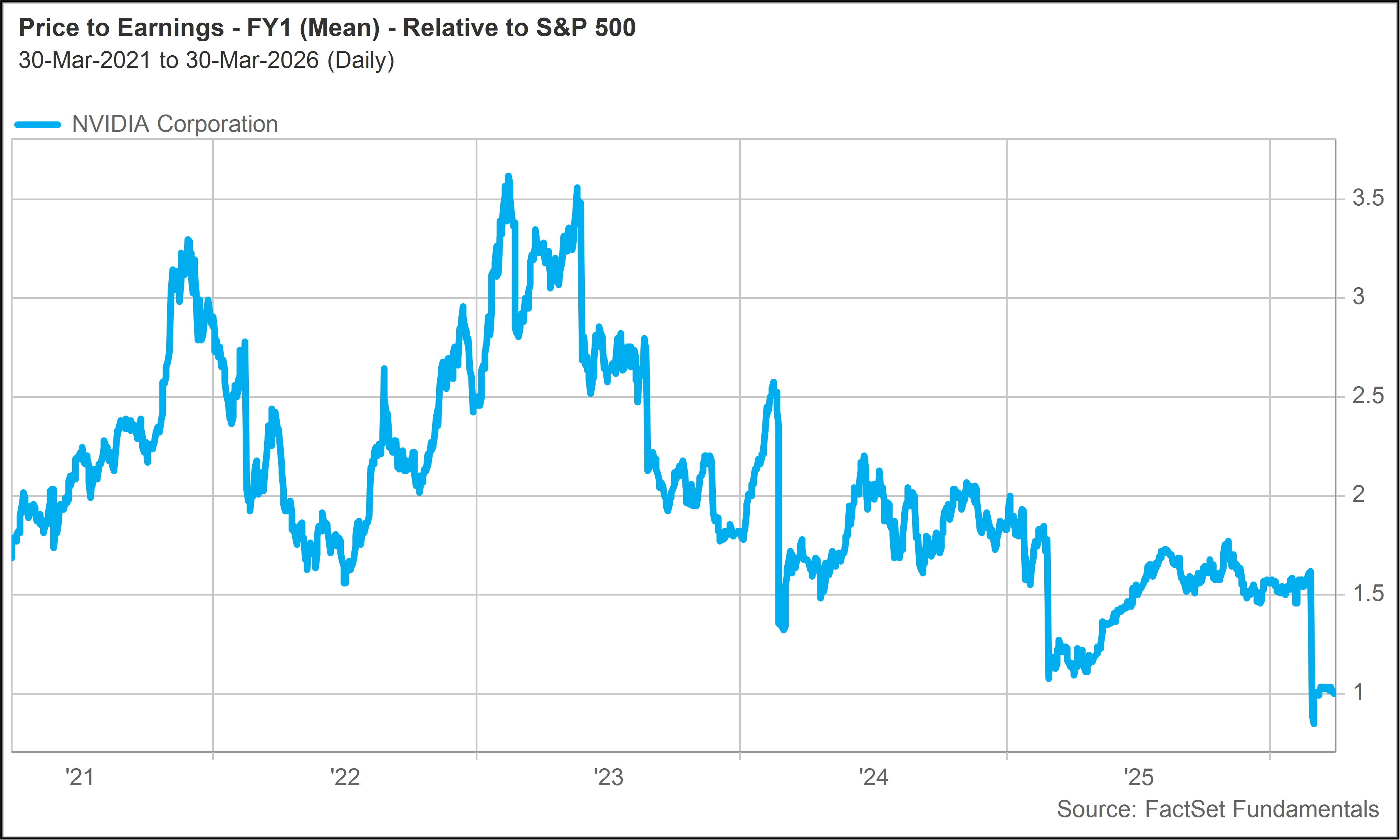

NVDA’s lack of a premium earnings multiple implies real skepticism toward the company’s long-term ability to grow. We find this skepticism unwarranted.

The “hyperscalers” within the MAG7 (including MSFT, GOOGL and AMZN) are aggressively investing in their AI buildouts, which has many investors concerned. This is not a direct concern for investors in NVDA, which has minimal capital spending requirements and continues to generate high levels of free cash flow.

What is a concern is that NVDA is a top supplier of hardware to these hyperscalers, which are its main customers. If their pace of investment proves to be unsustainable, or if they are able to transition away from NVDA hardware to competing products, NVDA revenue could suffer.

It is hard to argue the market has entirely “given up” on the NVDA growth story. NVDA remains the most valuable company in the world, with a $4 trillion market cap. But at current prices, we think the market is too aggressively handicapping NVDA’s long-term growth potential.

Despite the skeptics, the world remains hungry for AI. When CEO Jensen Huang spoke a few weeks ago at the company’s annual GTC conference, he referenced a trillion dollars of revenue visibility through 2027, which suggests consensus earnings forecasts may in fact be conservative.

Custom silicon and alternative chips are being developed, but NVDA’s advantage extends beyond hardware. Its CUDA ecosystem, developer tools, and integrated software stack create high switching costs and make NVDA extremely difficult to replace.

From a longer term perspective, NVDA is the innovation leader in AI. The business has transitioned away from merely being a supplier of chips to becoming an end-to-end provider of “AI factories.”

NVDA sits at the epicenter of the AI revolution, which is still in the early stages. We expect NVDA’s high rates of growth to continue for many years ahead.

Even if the market continues to value NVDA as cautiously as it does now, the share price will likely rise as earnings rise. And if the historical growth premium returns to NVDA, the upside could be much greater.

META

META also now offers what we would describe as “cheap growth.”

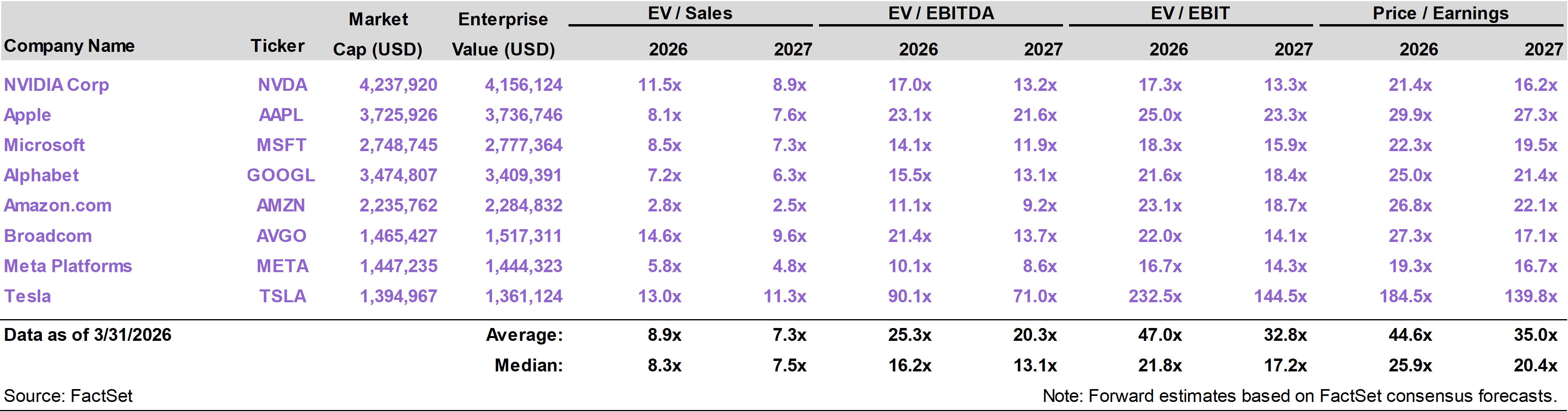

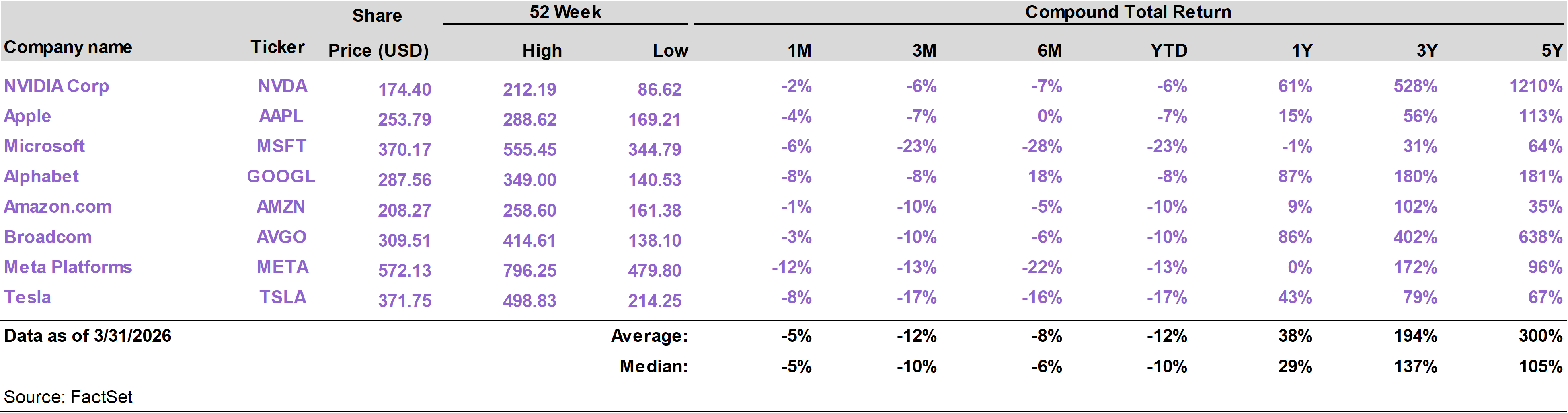

META trades at 19x current year earnings, slightly below the broader market multiple (20x) and the lowest in the group. Yet META is expected to grow earnings at a mid to high teens rate over the next two years, with potential acceleration later on as AI investments pay off.

Unlike NVDA, where the debate centers on the durability of demand, META’s recent weakness reflects concerns around spending and margin pressure.

META is not technically a hyperscaler in that the company does not directly host cloud computing for third parties. But the company is still investing heavily in AI infrastructure—data centers, compute, and model development—which has weighed on near-term profitability.

What makes META compelling is that AI is already working in the business today. Improved recommendation systems, ad targeting, and engagement are driving measurable gains in advertising efficiency.

In other words, META is not just investing in AI—it is actively monetizing it.

META controls its own distribution through Facebook, Instagram, and WhatsApp—platforms with billions of users. That gives it a direct channel to deploy AI at scale and capture the economic benefits internally.

In a market concerned about the cost of AI, META stands out as a company where the returns are already visible. As spending normalizes and efficiency gains compound, we expect that to become more apparent in the financials and for investor confidence in META to return.

Similar to NVDA, if META merely holds a low earnings multiple while earnings grow, this is sufficient for good performance. The opportunity for multiple expansion represents an extra source of potential upside.