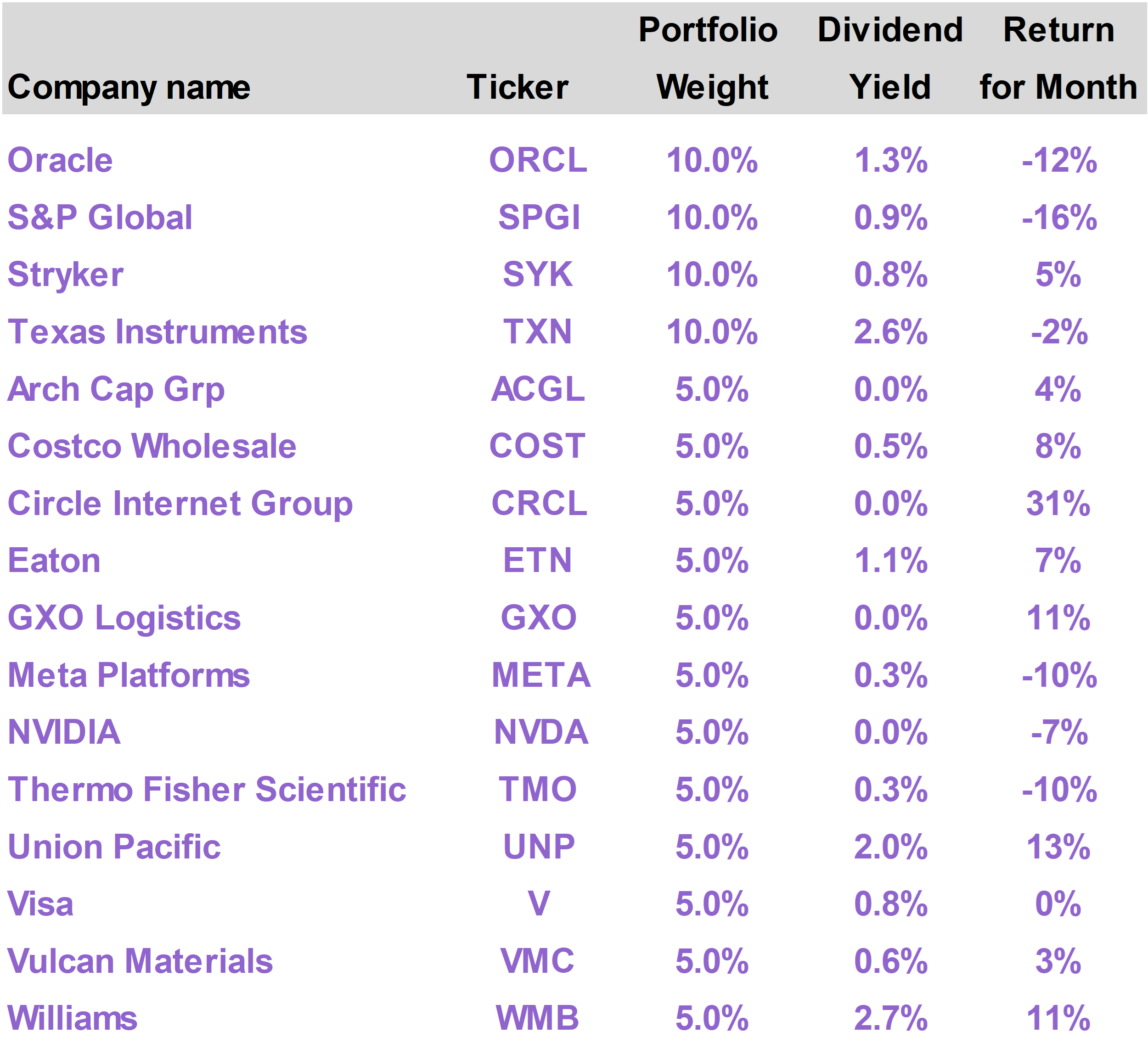

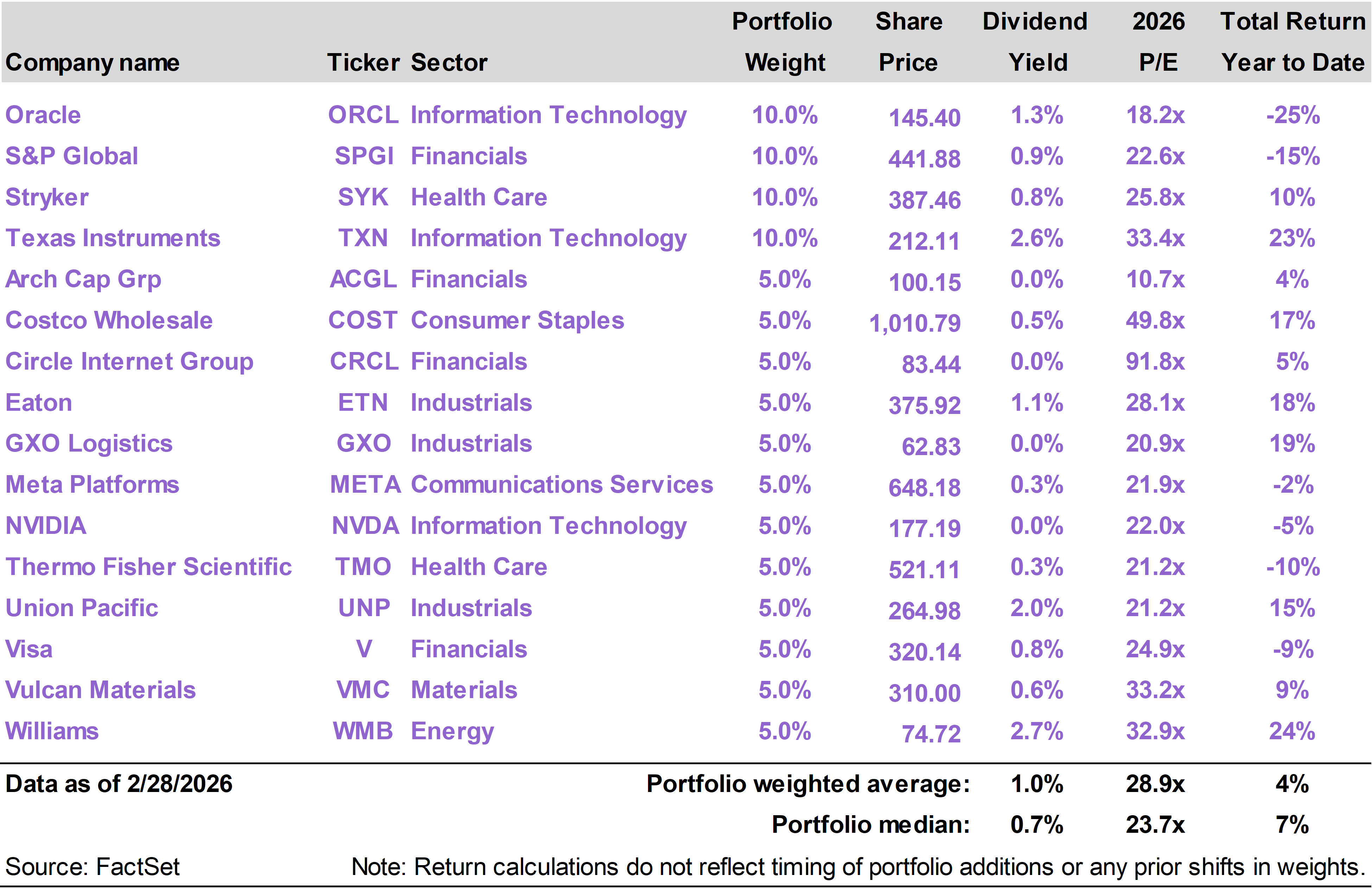

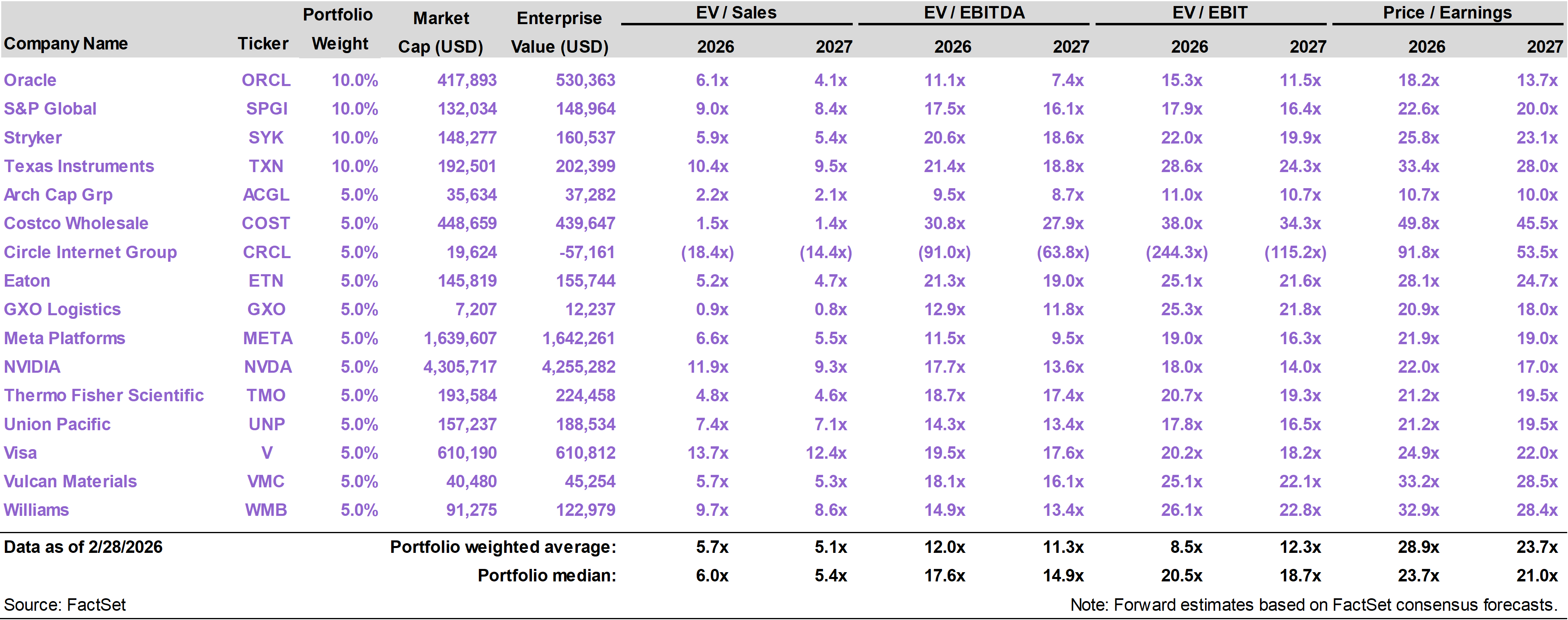

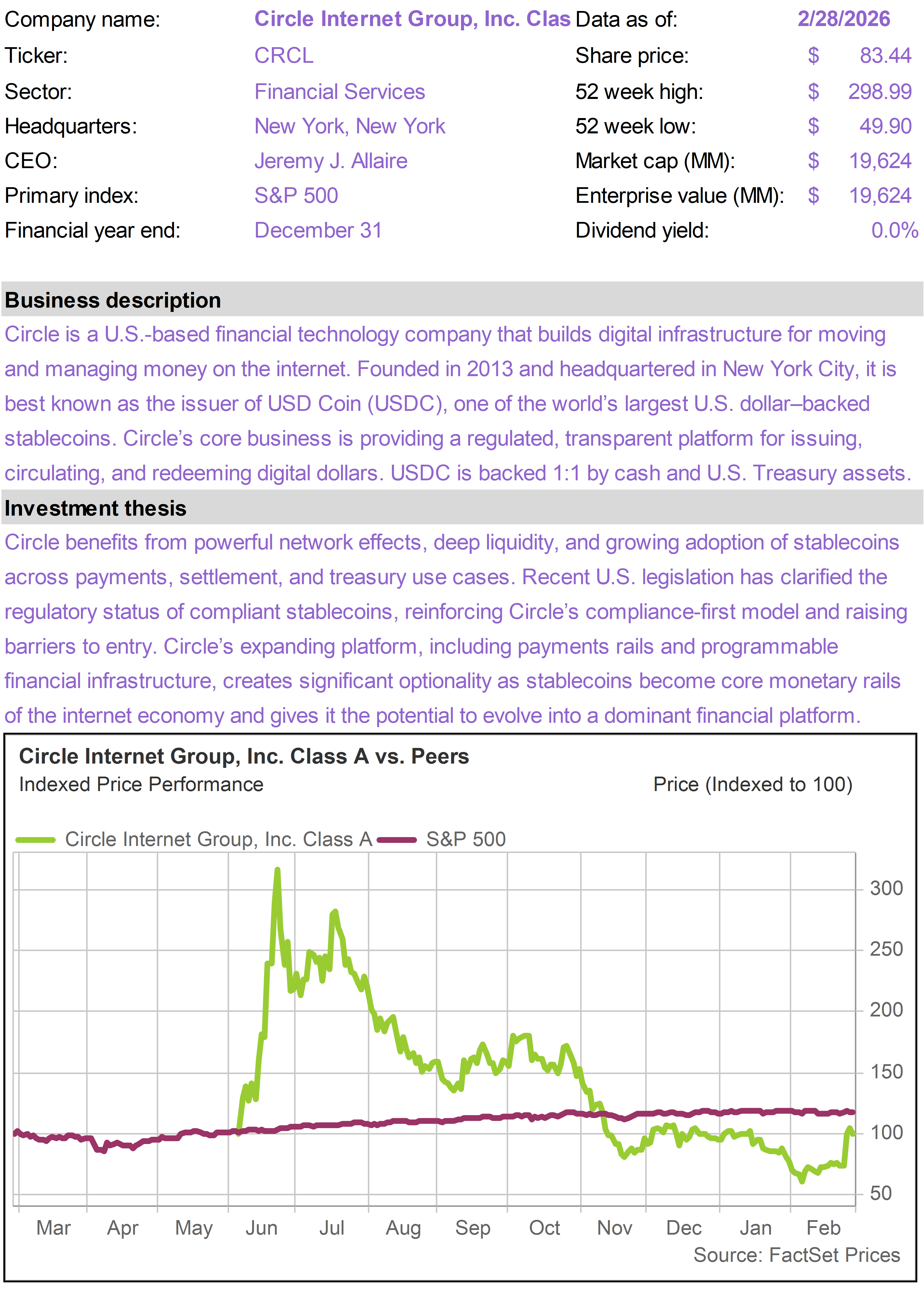

Shares of CRCL soared after the company reported fourth quarter earnings results that solidified the long-term business case.

As we explained in our initial discussion of the CRCL opportunity (Capitalizing on the Tech Downturn) as well as our post-earnings follow-up (Tech and Crypto Snap Back), we believe CRCL should not have been included in the harsh software-led sell-off.

Market sentiment can move a stock up or down, but ultimately fundamentals tend to prevail. When CRCL reported fourth quarter results on February 25, attention shifted away from sweeping sector narratives and toward the company’s substantial operational progress.

Notwithstanding the difficult environment for crypto, stablecoins continue to attract capital and gain adoption. CRCL stands to benefit from AI as more transactions, payments, and financial services move online and become automated, increasing demand for trusted, regulated digital dollars.

UNP shares performed well in February on the heels of a solid earnings report in late January. Management reaffirmed expectations for mid-single-digit EPS growth in 2026, driven less by macro tailwinds and more by productivity gains, pricing discipline, and cost control.

Earnings growth is expected to accelerate further in 2027 as longer-term strategic initiatives begin to bear fruit.

UNP also likely benefited from investor aversion to AI disruption risk. Railroads are hard-asset, network-based businesses with high barriers to entry. They own physical infrastructure, rights-of-way, and irreplaceable logistics corridors.

If anything, AI and automation should over time enhance scheduling, routing, fuel efficiency, and safety, rather than threaten the core franchise. In a market concerned about digital disruption, UNP’s tangible assets and pricing power provide a stabilizing contrast.

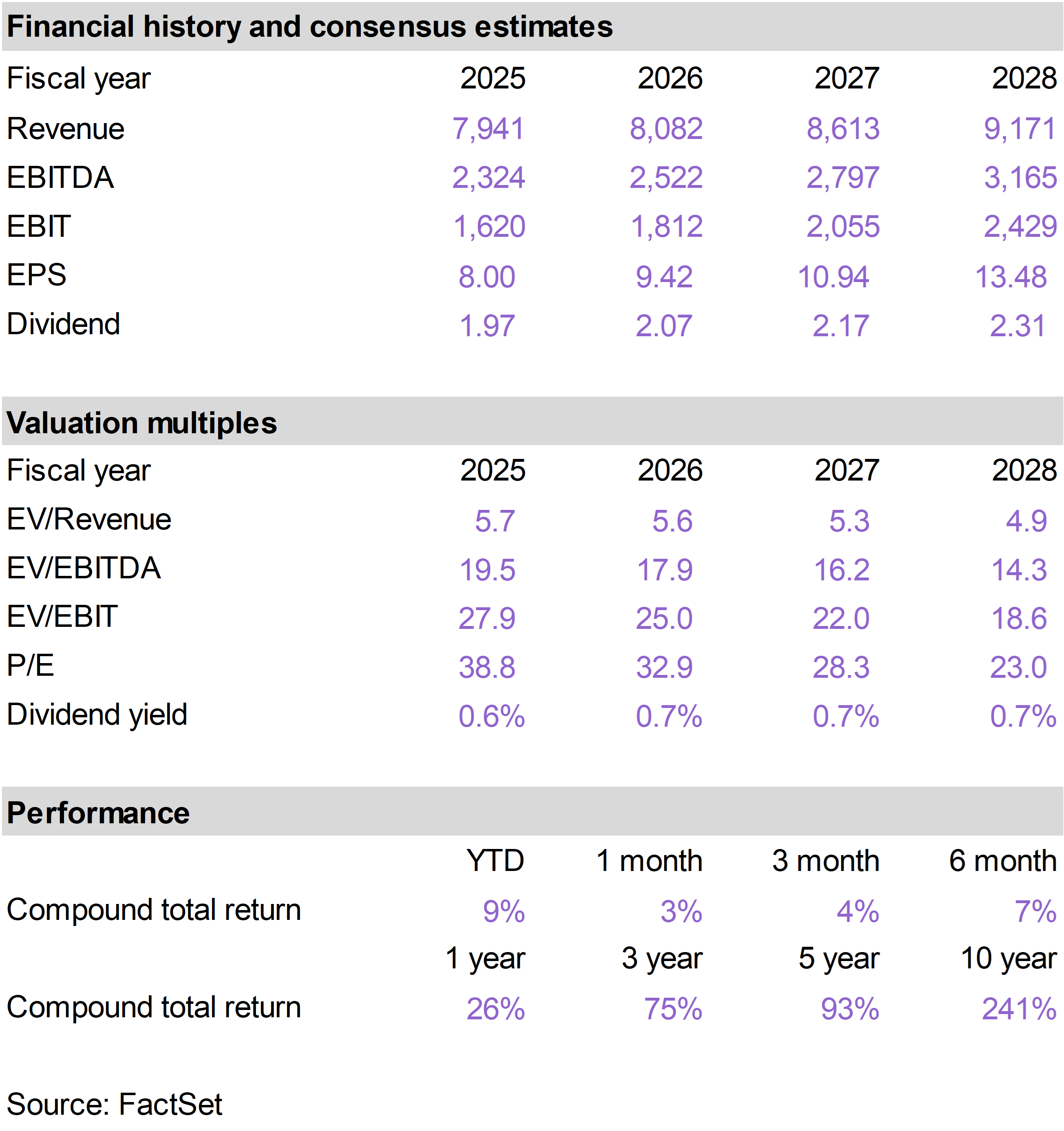

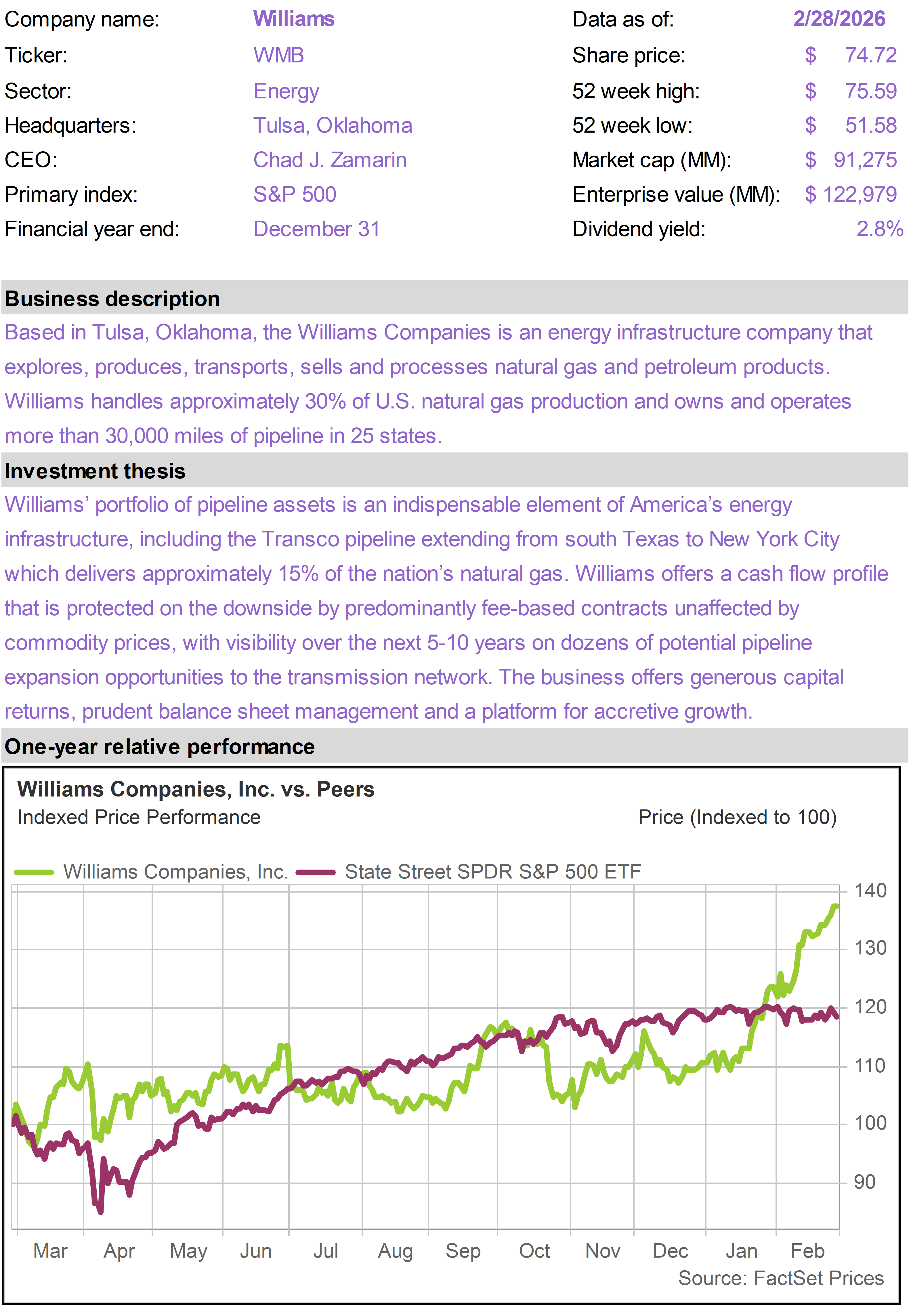

Like UNP, WMB owns indispensable and irreplaceable industrial infrastructure as the largest natural gas pipeline operator in the United States. Shares of WMB benefited in February from a solid fourth quarter earnings report and a successful investor day event.

Management reinforced confidence in the company’s long-term growth framework, highlighting durable demand across its natural gas transmission and processing footprint and a strong backlog of expansion projects.

The business continues to generate steady cash flow, supported by largely fee-based contracts and strong operating performance. Management’s outlook calls for continued earnings growth driven by disciplined capital allocation, incremental project roll-ins, and modest margin expansion.

With improving fundamentals, a constructive multi-year demand outlook tied to power generation and LNG exports, and a strong balance sheet, investors appear increasingly confident in WMB’s ability to compound value through the cycle.

SPGI was among a number of information services providers that participated in the AI disruption-related weakness this month. However, the company’s core businesses remain solid.

The Ratings segment continues to benefit from healthy debt issuance, including refinancing activity and financing tied to AI infrastructure buildouts. The Indices segment is also delivering double-digit growth, driven by rising assets linked to S&P benchmarks and strong derivatives trading activity.

Looking ahead, tokenization and the expansion of private markets could further strengthen SPGI’s position. As more assets move into digital formats and investors rely on AI-driven analysis, demand for trusted benchmarks, credit ratings, and high-quality financial data should persist.

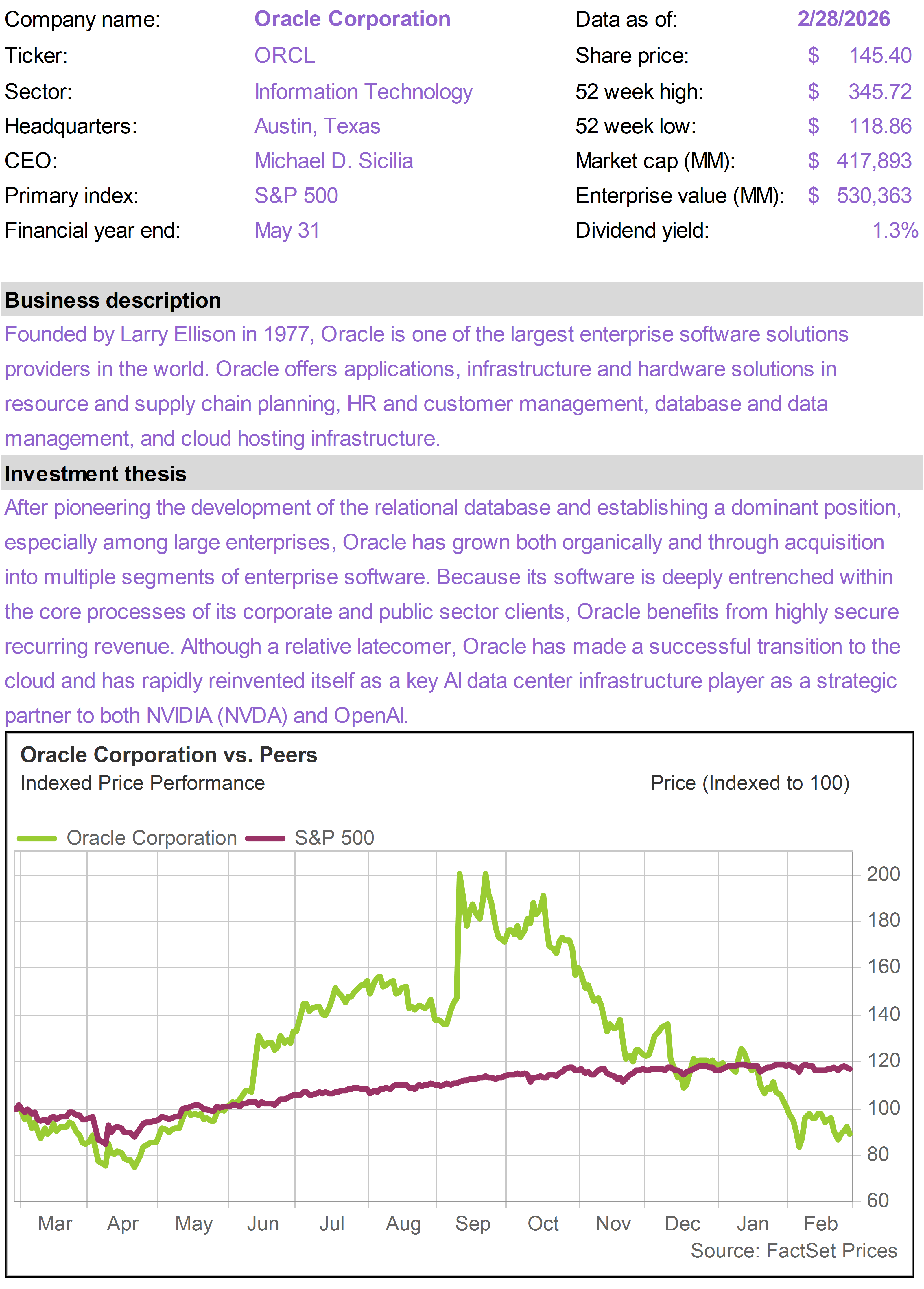

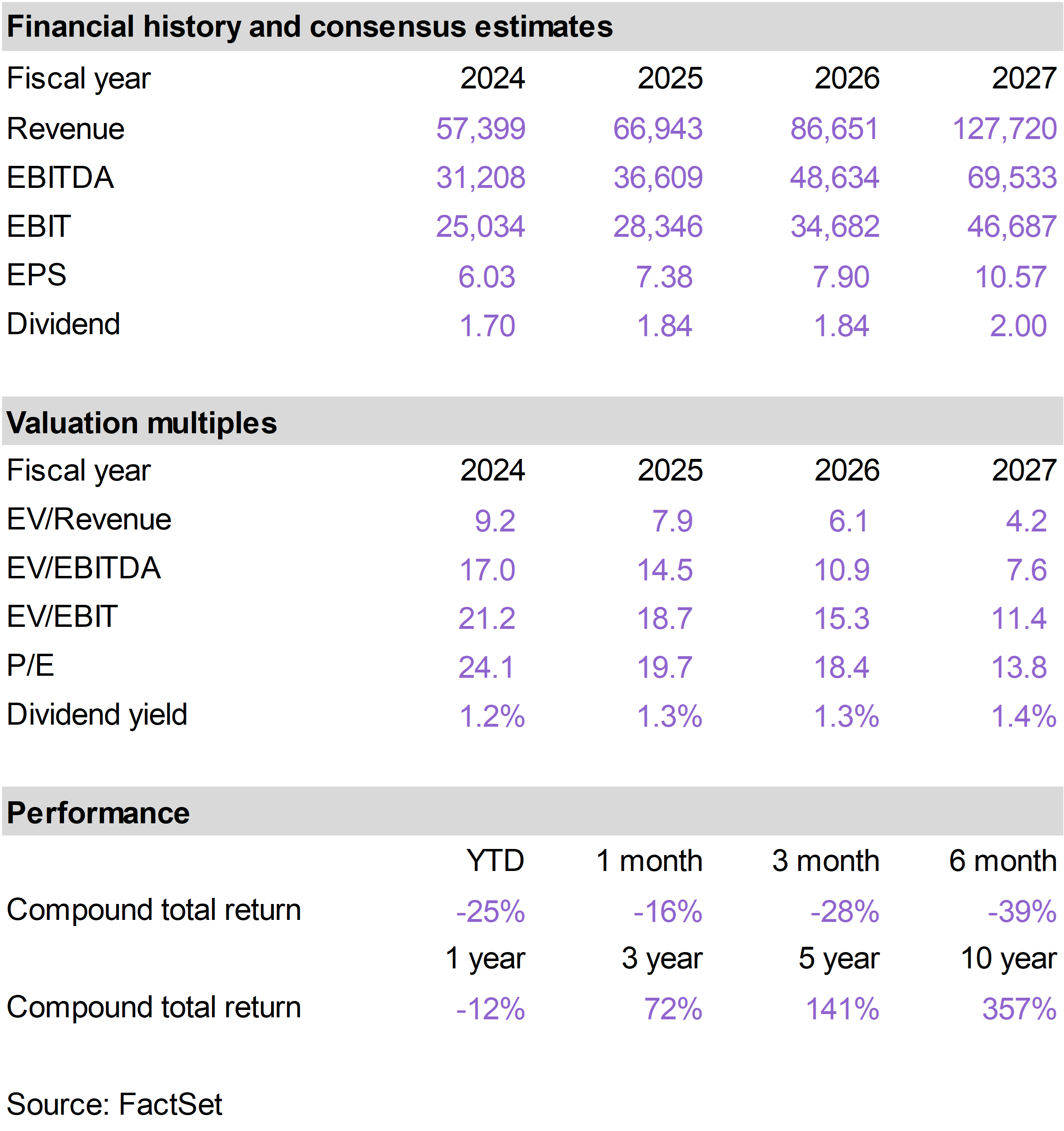

ORCL remained under pressure as investors shy away from its aggressive AI infrastructure strategy. While sentiment has become negative, its core database business remains deeply embedded in mission-critical systems. AI adoption should increase demand for its secure, high-performance data infrastructure.

ORCL’s growth strategy carries some well-flagged risks, but from a valuation perspective, it is now trading at less than 14 times consensus earnings forecasts for fiscal year 2027. We view the stock’s risk-reward profile as highly favorable.

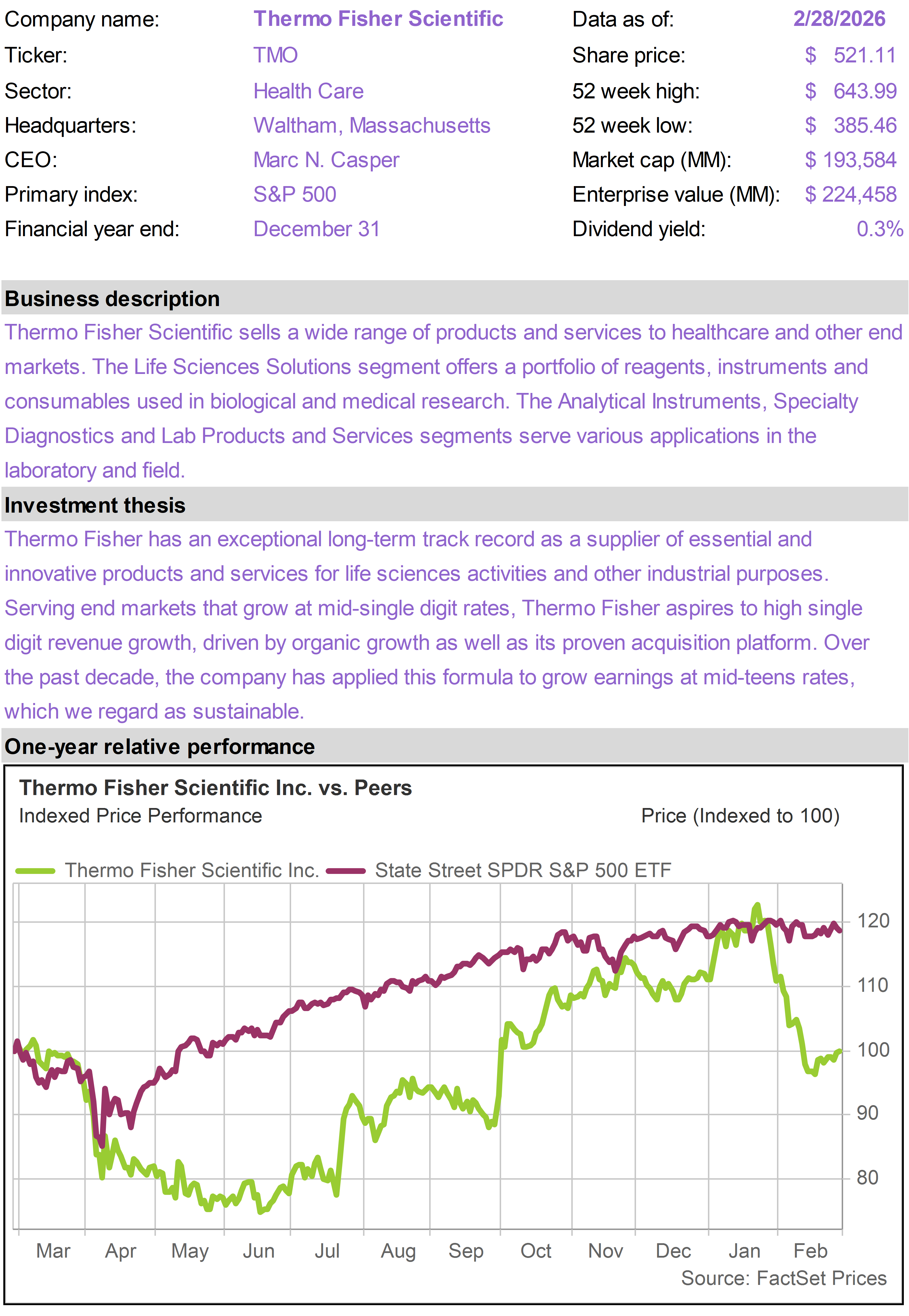

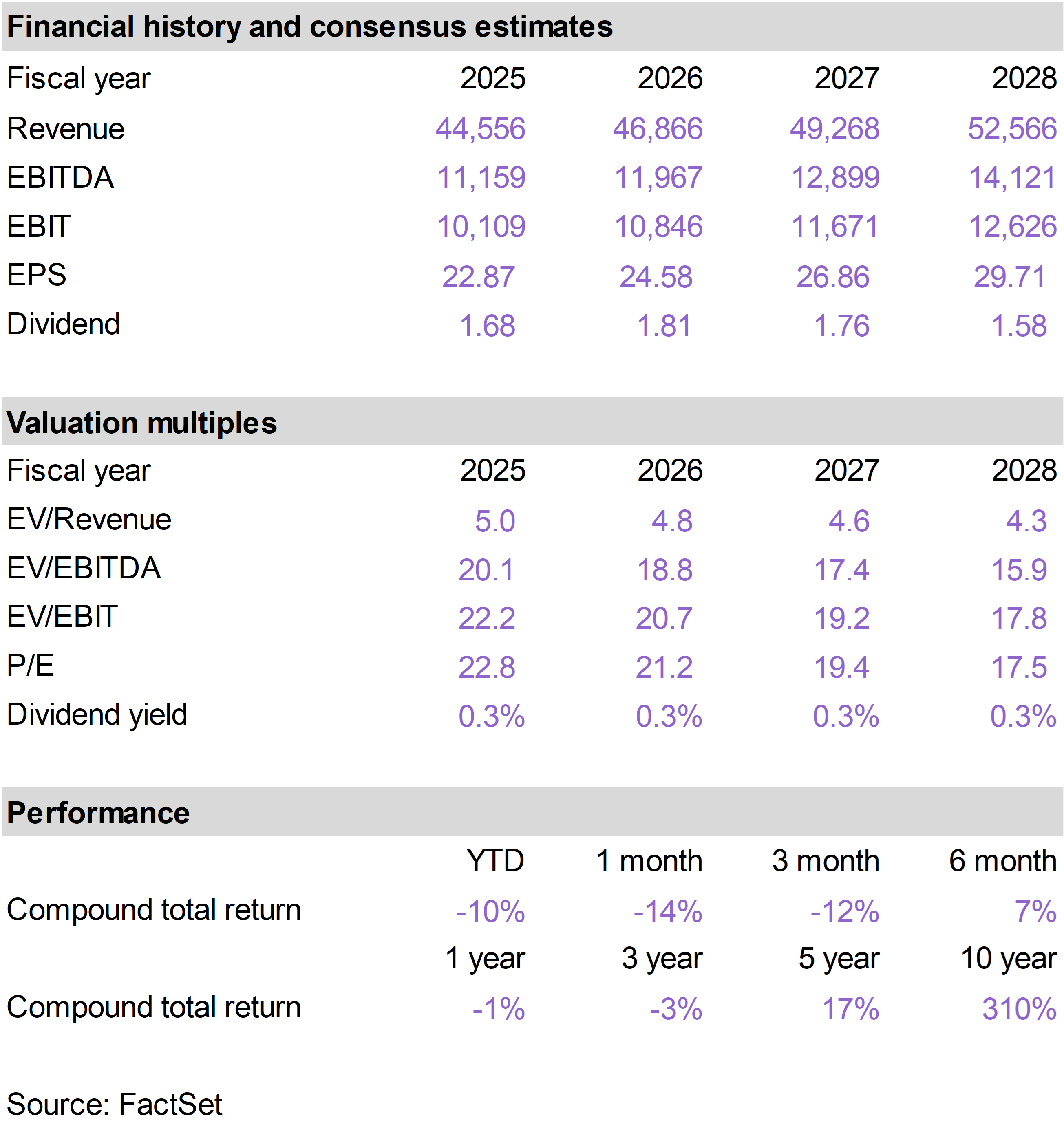

Shares of TMO declined in February following several months of strong outperformance. Investors appeared to focus on conservative 2026 guidance, which calls for organic revenue growth at the lower end of the 3–4% range and 6–8% adjusted EPS growth, along with a softer first quarter due to tougher comps.

That said, the outlook still implies margin expansion and accelerating growth through the year. In addition, there are early signs of improving biotech funding and better momentum in academic and government channels, which could support a demand rebound as 2026 progresses.