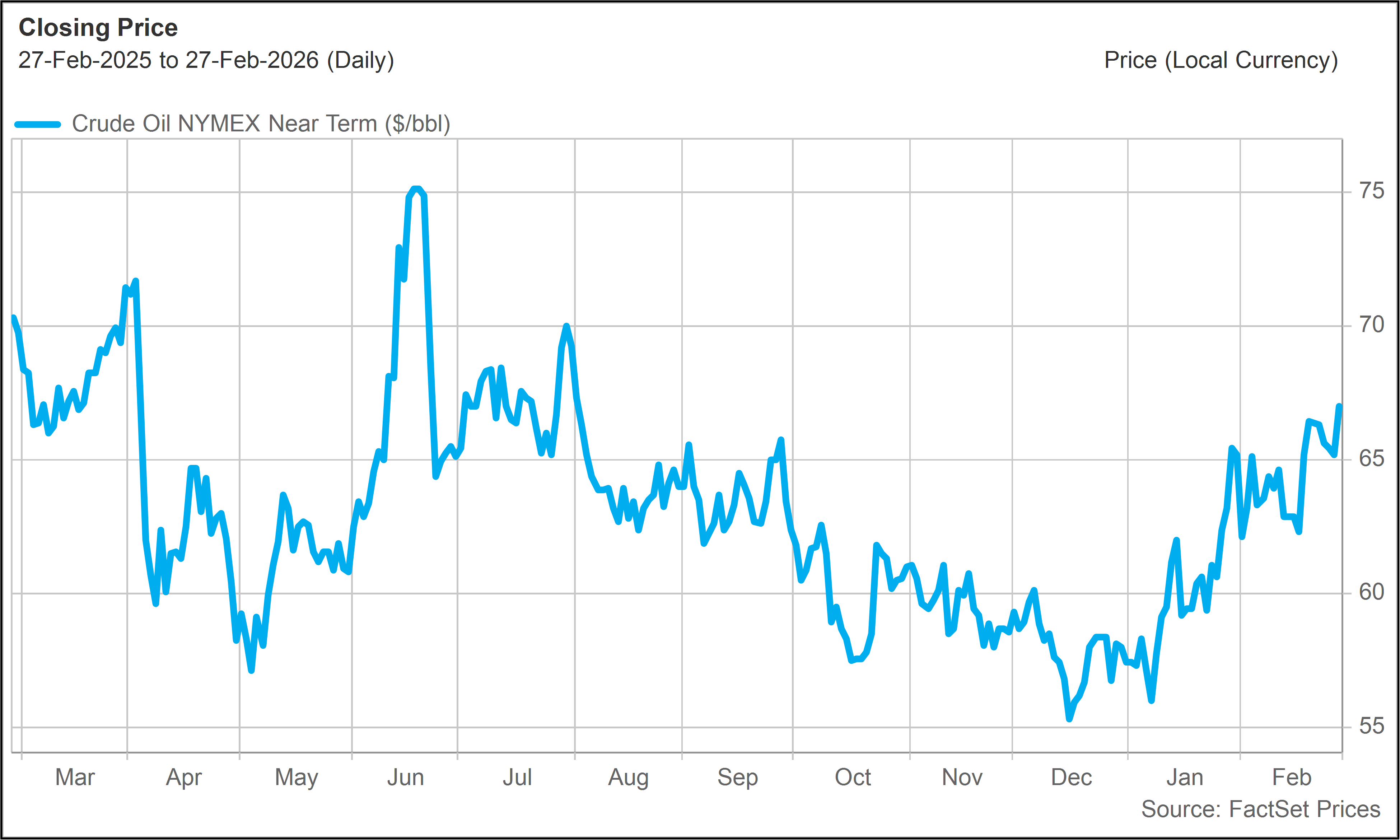

Shares of PR advanced on the heels of a strong earnings report and upward movement in oil prices. The company exited 2025 with record oil production and some of the lowest drilling and completion costs in its history, underscoring the strength of its Delaware Basin operations.

Free cash flow generation remains a key highlight. PR grew free cash flow by 18% in 2025, while reducing debt by more than $600 million. Management continues to emphasize a long-term focus on growing free cash flow per share through capital efficiency, disciplined spending, and opportunistic acquisitions.

Looking into 2026, the company expects roughly 5% oil production growth while keeping capital spending relatively steady. Combined with improved gas marketing, PR is positioned to generate durable cash flow even in a moderate commodity environment.

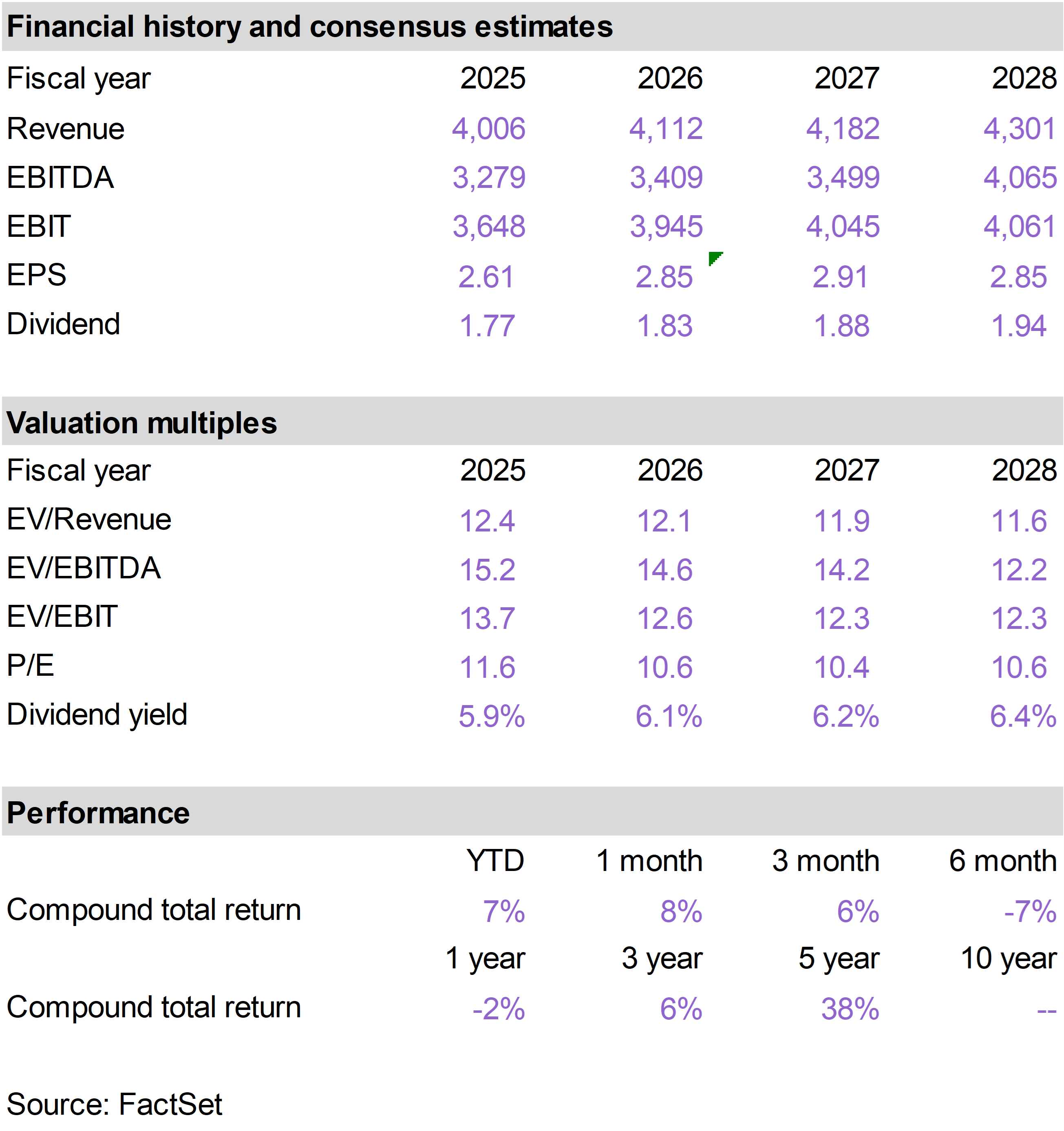

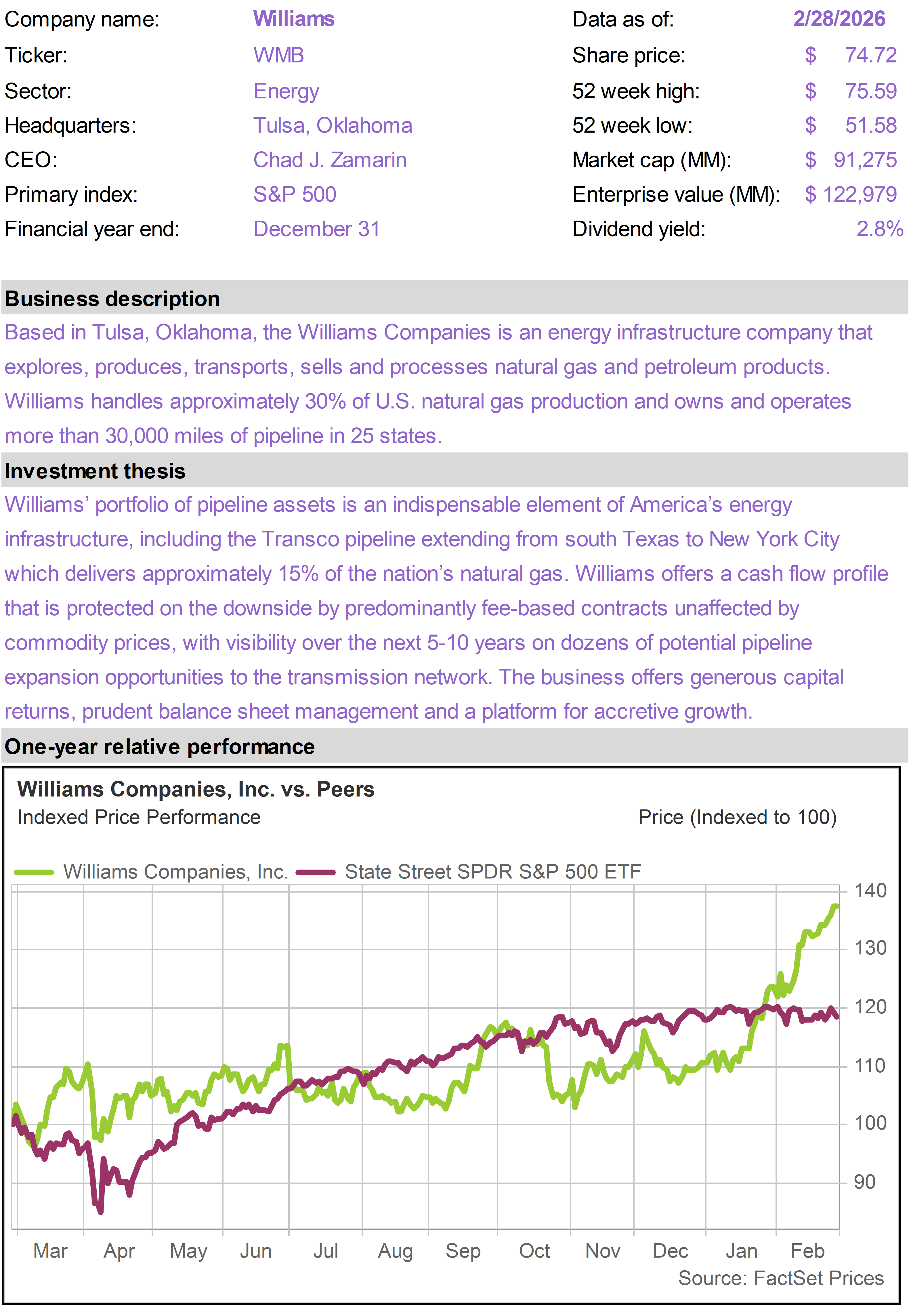

As the largest natural gas pipeline operator in the United States, WMB owns indispensable and irreplaceable industrial infrastructure. Shares of WMB benefited in February from a solid fourth quarter earnings report and a successful investor day event.

Management reinforced confidence in the company’s long-term growth framework, highlighting durable demand across its natural gas transmission and processing footprint and a strong backlog of expansion projects.

The business continues to generate steady cash flow, supported by largely fee-based contracts and strong operating performance. Management’s outlook calls for continued earnings growth driven by disciplined capital allocation, incremental project roll-ins, and modest margin expansion.

With improving fundamentals, a constructive multi-year demand outlook tied to power generation and LNG exports, and a strong balance sheet, investors appear increasingly confident in WMB’s ability to compound value through the cycle.

SRE performed well as investors favored utility stocks. The company offers meaningful leverage to strong infrastructure demand in Texas, where accelerating transmission and distribution investment is driving an attractive rate base growth outlook.

Management sees a clear path to achieving the high end of its long-term 7–9% earnings growth framework. The combination of visible capital investment, improving earnings alignment with rate base growth, and a predominantly regulated business mix provides investors with durable, lower-volatility growth.

Shares of alternative asset managers BX and CG declined, reflecting fears of private credit exposure. Investors grew concerned that a slower growth environment and tighter financial conditions could pressure portfolio companies, reduce deal activity, and lead to higher credit losses across private lending platforms.

There is also a secondary concern tied to software exposure. Over the past decade, private equity and private credit have allocated significant capital to software and asset-light technology businesses, attracted by their recurring revenue models and high margins.

As public software stocks have sold off amid AI disruption fears, investors have begun to question whether private-market valuations for these businesses may also come under pressure.

Both BX and CG operate diversified alternative asset management platforms with substantial fee-related earnings that are not directly tied to short-term mark-to-market movements. Much of their revenue comes from long-duration capital and management fees rather than purely transactional income.

Recent weakness, therefore, appears driven more by macro and sentiment concerns, including spillover from software, than by any deterioration in long-term fundamentals.

In February, CG hosted an investor day which focused attention on the long-term strengths of the business. Management outlined a clear three-year roadmap centered on scaling fee-related earnings, expanding margins, and driving durable organic growth across its platform.

The firm is targeting approximately 15% annual growth in fee-related earnings by 2028, alongside fee-related earnings margins of 50% or greater. Cumulative inflows are projected to exceed $200 billion between 2026 and 2028.

Notably, management emphasized the growing importance of wealth and insurance-related capital, including more than $40 billion expected from evergreen wealth vehicles that represent a structurally attractive and recurring source of fundraising.

The investor day reinforced our view that CG is evolving into a more diversified, margin-accretive alternative asset manager with stronger visibility into long-term fee growth.

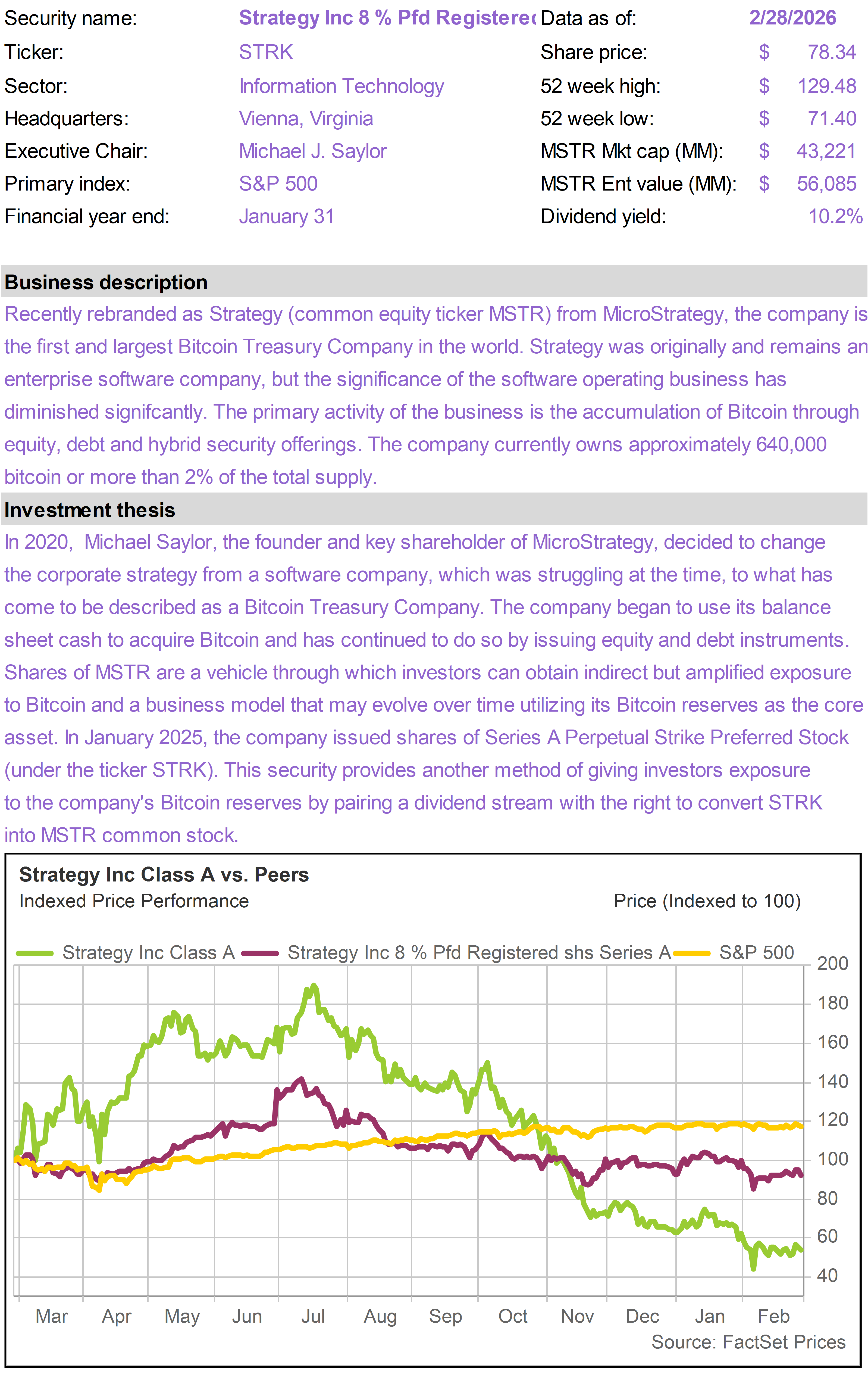

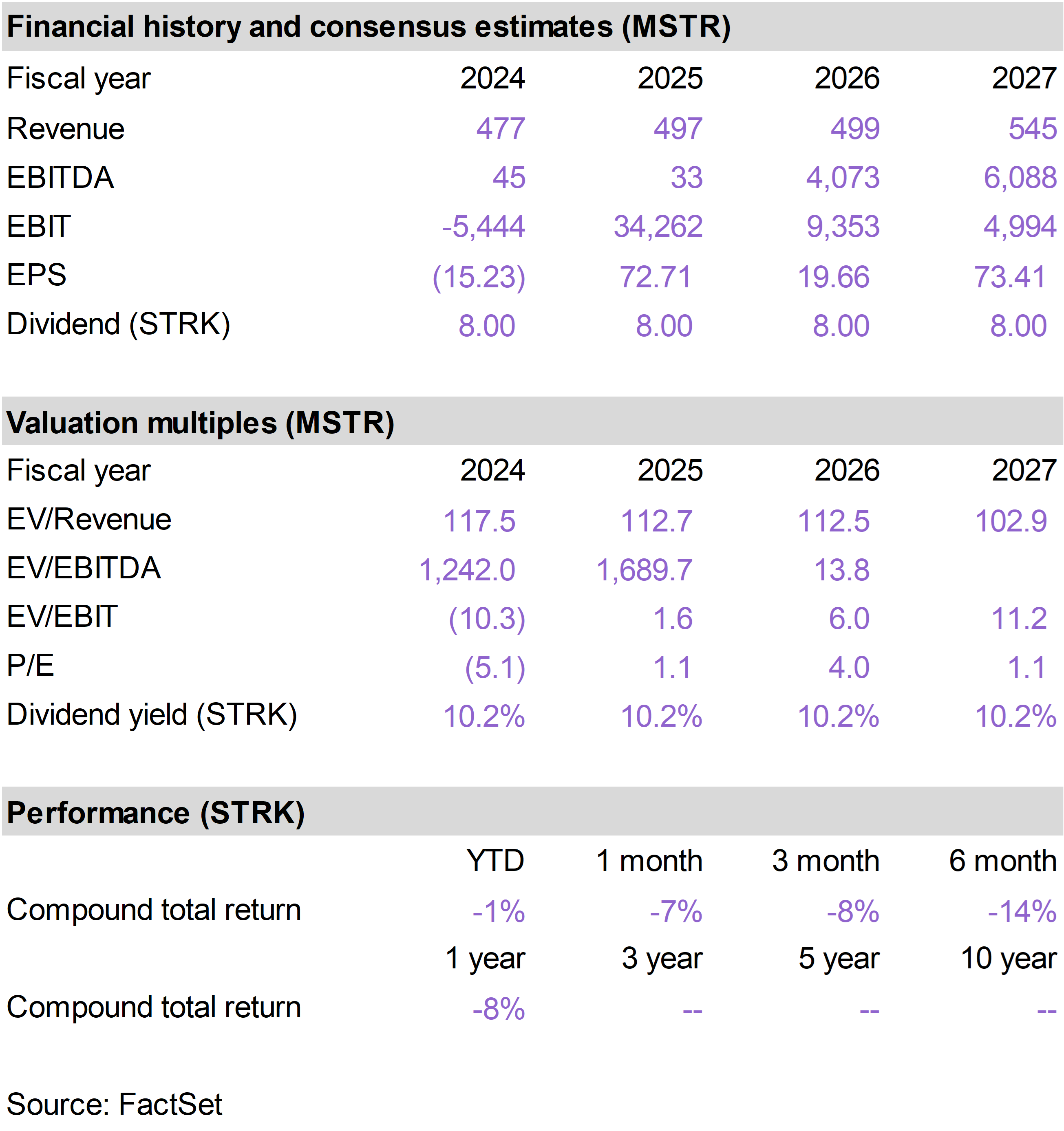

Shares of STRK declined with weakness in Bitcoin and soft crypto sentiment. We remain quite comfortable with Strategy’s ability to meet it dividend obligations to preferred shareholders, barring a catastrophic and sustained collapse in the value of Bitcoin.