Regulatory tailwind

Recent U.S. legislation materially improves Circle’s competitive positioning by turning its long-standing compliance posture into a structural advantage.

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), now law, establishes a federal framework for payment stablecoins. It requires 1:1 reserve backing with high-quality liquid assets, frequent public disclosures, and ongoing regulatory supervision—while explicitly clarifying that compliant payment stablecoins are not securities.

For Circle, this largely codifies how USDC already operates. In effect, regulation is no longer a hurdle Circle must clear; it is a moat that raises the bar for competitors who built under looser standards.

Crucially, GENIUS enables banks, payment processors, and enterprises to use stablecoins within a clear legal perimeter. That expands USDC’s addressable market beyond crypto-native activity into payments, treasury management, settlement, and tokenized finance.

The Digital Asset Market Clarity Act, while not yet fully enacted, complements this shift by defining regulatory jurisdiction and market structure for digital assets more broadly. The law reduces the risk that stablecoins become entangled in securities or commodities enforcement regimes, reducing long-term policy uncertainty and supporting institutional adoption.

Taken together, these two laws reward the model Circle has already built: transparent reserves, regulatory engagement, and neutral financial infrastructure.

Sizing the stablecoin opportunity

Stablecoins are best thought of as “internet-native money.” They combine the stability of fiat currency with the speed, programmability, and global reach of blockchains.

Today, global stablecoin supply is roughly $300 billion, having grown at a rapid pace over the last five years. The future long-term growth opportunity is vast. Stablecoins have the potential to become the dominant mode of digital transactions.

Stablecoins represent a fully digital approach to moving, storing, and exchanging money. Most stablecoin usage today is still concentrated in crypto-related activity like trading and on-chain settlement.

The real long-term opportunity, however, is the upgrade of the traditional financial system to tokenized cash, which is similar in many ways to the upgrade from physical mail to e-mail over the past several decades.

Management contends that stablecoins function as a new form of digital M1. This refers to the portion of the money supply (totaling some $19 trillion at year-end 2025 in the U.S. alone) that sits in checking and savings accounts or as physical cash in a wallet or safe.

Stablecoins enable cash to move at internet speed. As adoption broadens, growth is driven not just by supply, but by velocity. The same dollar can settle many transactions in a short period, magnifying utility.

If even a modest percentage of global dollar settlement migrates on-chain, the addressable market for stablecoins expands into the trillions, not hundreds of billions.

It is worth noting as well that the money supply itself is not static but is constantly growing. Over the past 20 years, overall money supply has grown approximately 6% per year in the United States. So, over the long term, stablecoins have the potential to take a growing share of a consistently growing pie.

Circle’s competitive advantages

Circle’s benefits from numerous competitive advantages which intersect to strengthen its positioning within this rapidly growing sector.

(1) Trust and regulatory credibility

USDC is fully reserved, transparent, and issued within an increasingly clear regulatory framework. This matters enormously as stablecoins move beyond retail crypto traders into businesses, funds, and regulated institutions. Trust is hard to regain once lost—and Circle has spent more than a decade prioritizing credibility, often at the expense of faster growth.

(2) Liquidity

USDC is deeply embedded across exchanges, decentralized finance protocols, payment systems, and blockchains. Liquidity begets liquidity: developers build where liquidity already exists; users migrate to where transactions are cheapest and fastest.

As Allaire noted on the recent earnings call, Circle’s moat comes from its “core liquidity infrastructure, global minting and redemption capabilities, and broad distribution across ecosystems.”

(3) Market-neutral infrastructure

Unlike exchanges, wallets, or trading firms, Circle positions itself as market-neutral plumbing. This makes it a trusted counterparty for firms that do not want to build on a competitor’s technology stack.

(4) Technology depth

Circle is not just an issuer; it is a builder of financial infrastructure software. Its cross-chain transfer technology, payments rails, and programmable money tooling allow developers to treat USDC as a native application layer rather than a static token.

Additional growth avenues

Circle’s most compelling long-term upside potentially lies beyond reserve income.

As USDC migrates into real-world payments—B2B settlement, remittances, marketplace payouts—Circle can capture transaction-based fees while reinforcing the base network. Unlike card networks, stablecoin payments settle instantly, globally, and at low cost. That is attractive for use cases where speed and predictability matter more than consumer credit.

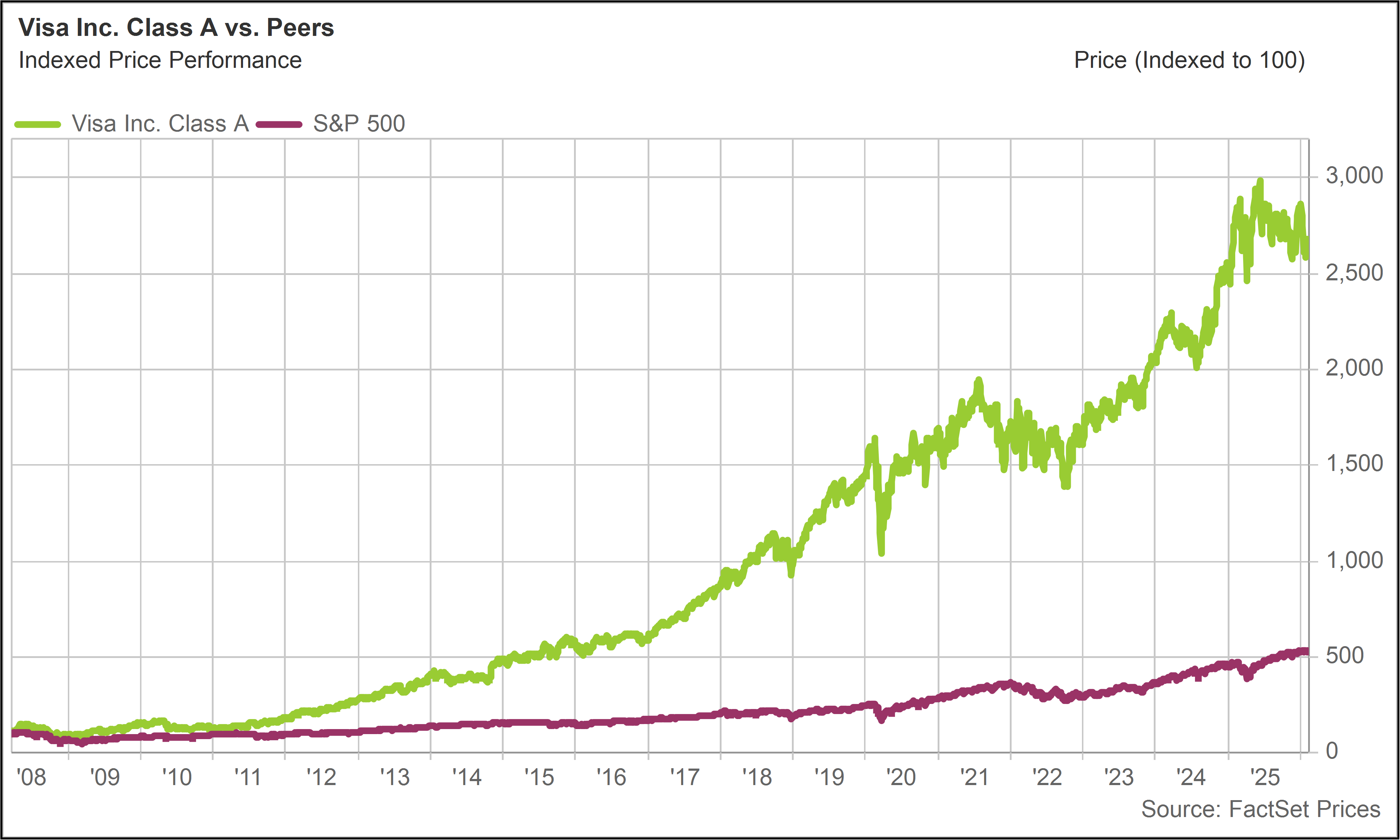

Circle’s strategy also extends into traditional payment rails through partnerships with Visa (V) and other payment processors.

Visa has integrated USDC settlement capabilities, enabling select partners to settle obligations directly in stablecoins rather than through legacy banking rails. This allows payments to clear faster, operate 24/7, and reduce reliance on correspondent banks, particularly for cross-border transactions.

Circle’s Arc initiative is particularly important to long-term optionality. Arc is designed as a blockchain-based financial infrastructure layer optimized for regulated digital money.

Rather than competing with general-purpose blockchains, Arc aims to offer enterprise-grade performance, compliance hooks, and programmability that is specifically tailored to payments, treasury, and financial contracts.

Management has described Arc as part of a broader “internet financial system,” where money, contracts, and settlement logic live natively in software. If successful, Arc could become a high-margin platform layer enabling tokenized cash instruments, programmable settlement, and AI agent-driven financial workflows.

The company is currently exploring the creation of an Arc token to facilitate this business. Arc is early, but if adoption takes hold, it expands Circle’s role from issuer to operating system for digital money.

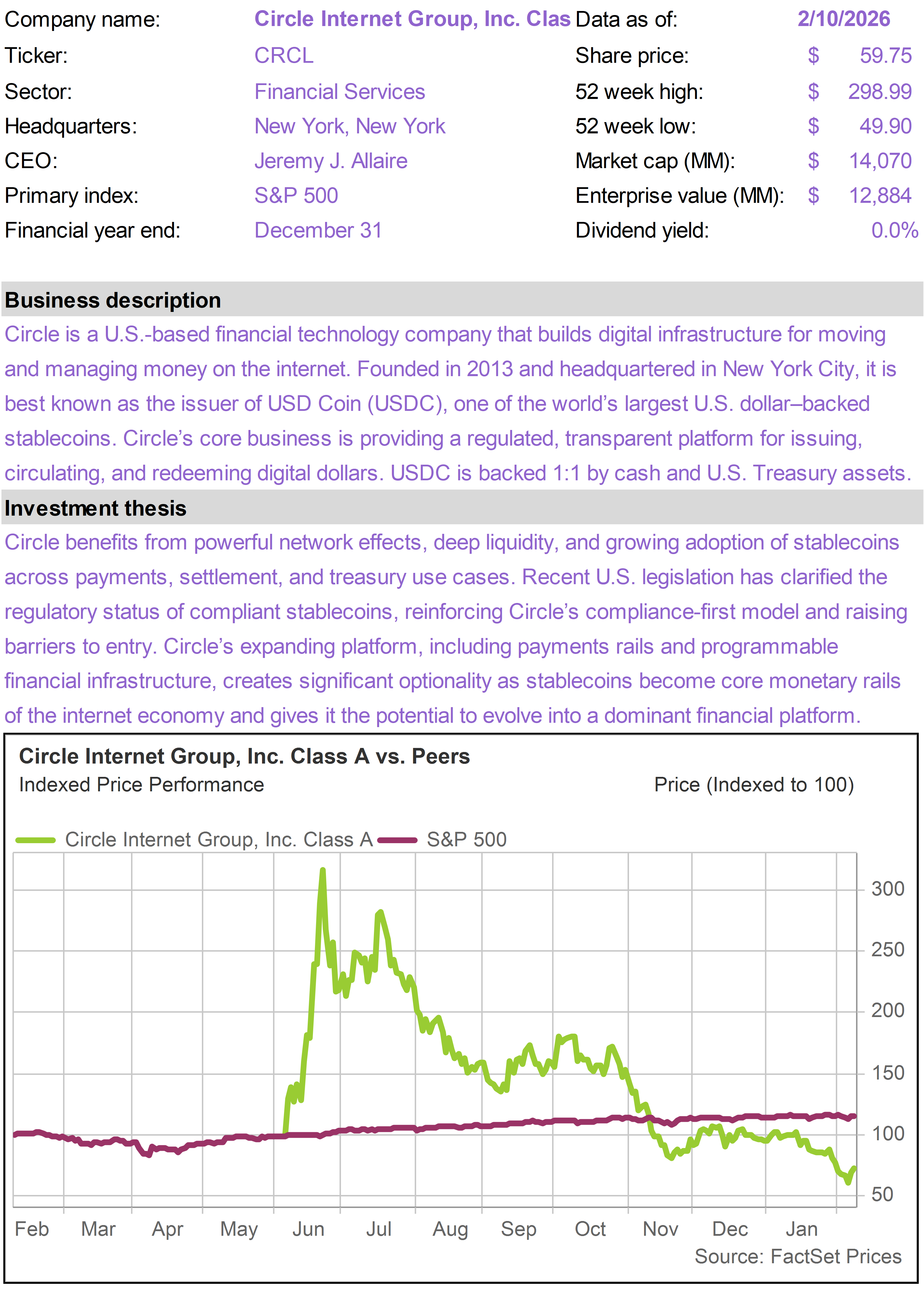

Company background

Circle was founded in 2013 by Jeremy Allaire, a repeat entrepreneur with deep roots in internet infrastructure and payments. Unlike many crypto founders, Allaire has consistently framed Circle’s mission in decade-long time horizons, not speculative cycles.

For years, Circle invested heavily in compliance, policy engagement, and global regulatory alignment—often while competitors optimized for speed or yield. That patience is now paying off as regulation shifts from existential risk to structural tailwind.

Allaire has described Circle as “still early-stage relative to the scale of what we’re building,” emphasizing that the company’s goal is to upgrade the entire global financial system, not simply issue a popular token.

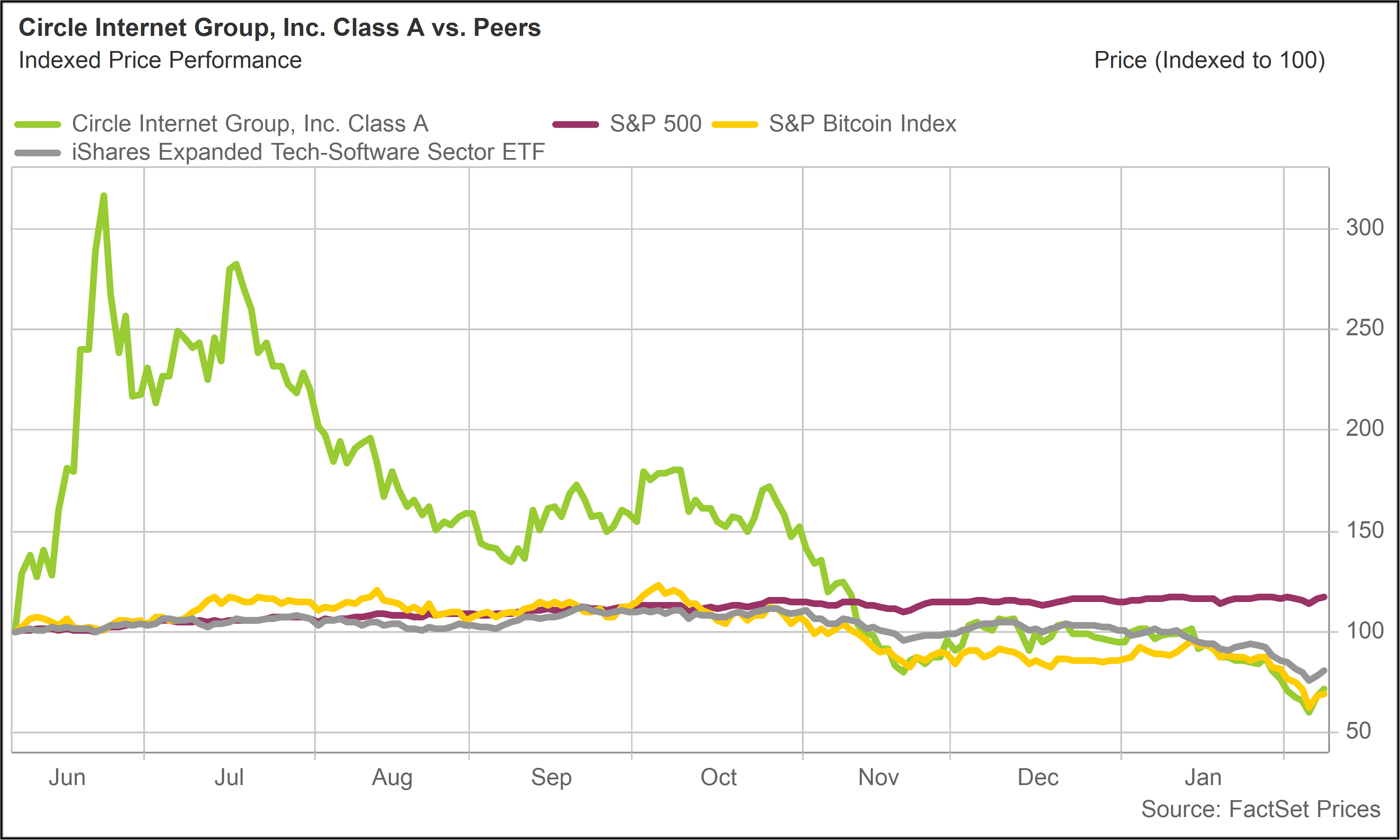

Post-IPO sell-off as opportunity

The June 5, 2025 IPO of CRCL was highly successful and coincided with strong momentum in crypto and technology. The shares were originally issued at $31 and closed at $83 on the first day of trading.

Over the next few weeks, CRCL would get as high as $299 in intra-day trading before settling into the $120 to $150 range for most of August, September and October.

Circumstances began to change drastically, however, starting at the end of October. CRCL shares came under pressure as the stock got caught up in two major (and intersecting) market trends.

First, there was the crypto sell-off. Bitcoin and other crypto assets peaked in late summer and early fall 2025. On October 10, crypto prices fell sharply as heavy leverage unwound across the system.

While broader macro uncertainty set the stage, the decline was amplified by market dynamics on major exchanges, particularly Binance, the world’s largest crypto exchange. When prices began to slip, automated liquidations kicked in, accelerating the move and creating a self-reinforcing cycle of forced selling.

Bitcoin and other digital assets have been extremely weak ever since, bringing down fintech stocks like CRCL as crypto sentiment has deteriorated.

There was also the software sell-off, which we wrote about last week (Software as a Sell-Off: Another AI Overreaction?). Since October, but especially in January and February 2026, software application stocks have traded poorly as investors have begun to view many of these companies (rightly or wrongly) as AI victims rather than beneficiaries.