As Jensen elaborates, software is fundamentally a tool that AI will use, not replace or reinvent. He goes onto describe a scenario where AI agents make use of existing software, perhaps even more heavily than it is currently used.

Selectivity matters

Many of the stocks that investors are dumping in response to the disruption threat embodied by the Claude plugins have proprietary data sets and other strategic assets that cannot be easily replicated.

It is in many cases an extreme oversimplification to think AI can perform complex, data-intensive tasks for which expensive software was previously required. Just as it was an extreme oversimplification to think DeepSeek could do for millions of dollars what American companies were spending billions on.

That said… AI absolutely is a disruptive technology.

The technology sector as a whole may ultimately do well as a result of AI, but within the sector, there will be a substantial separation between winners and losers.

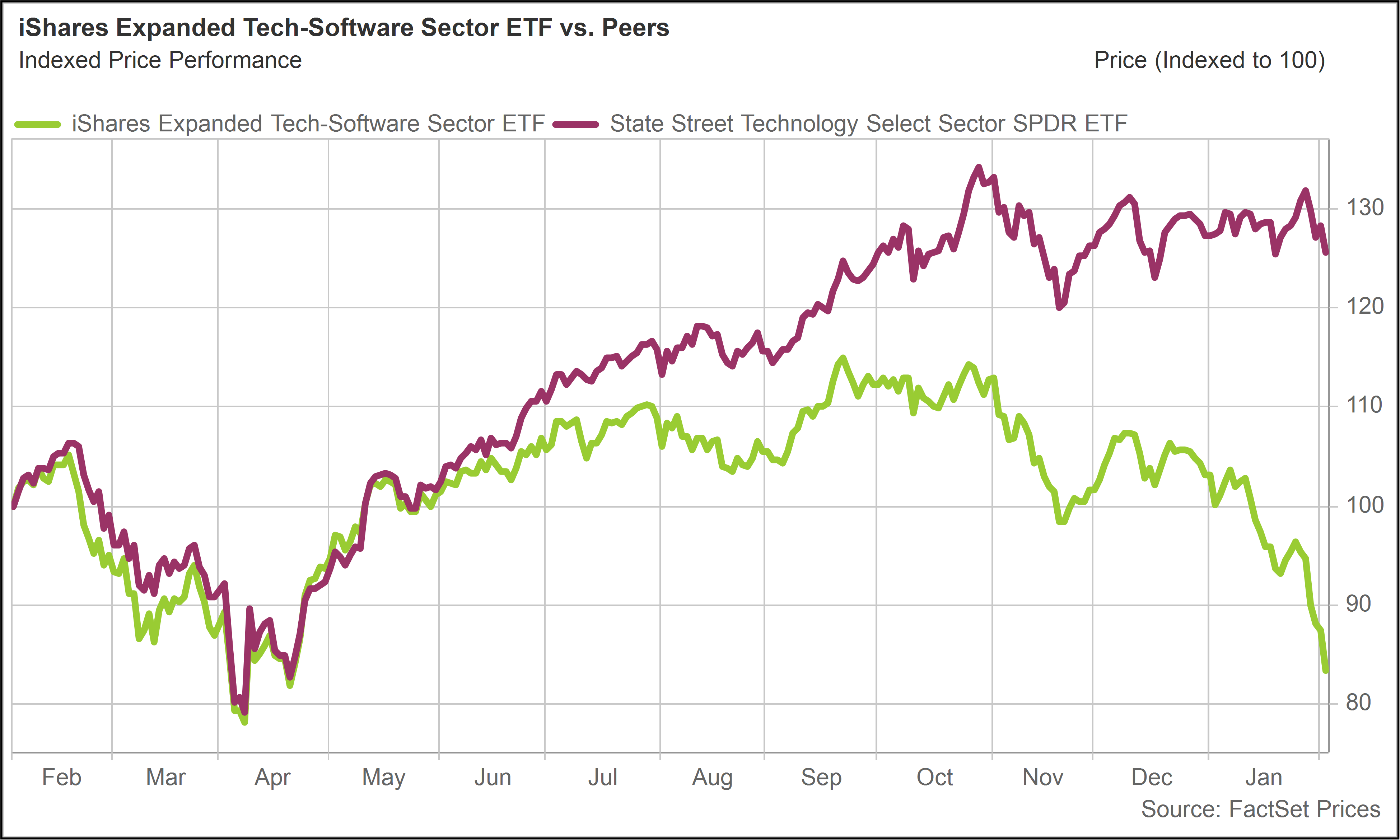

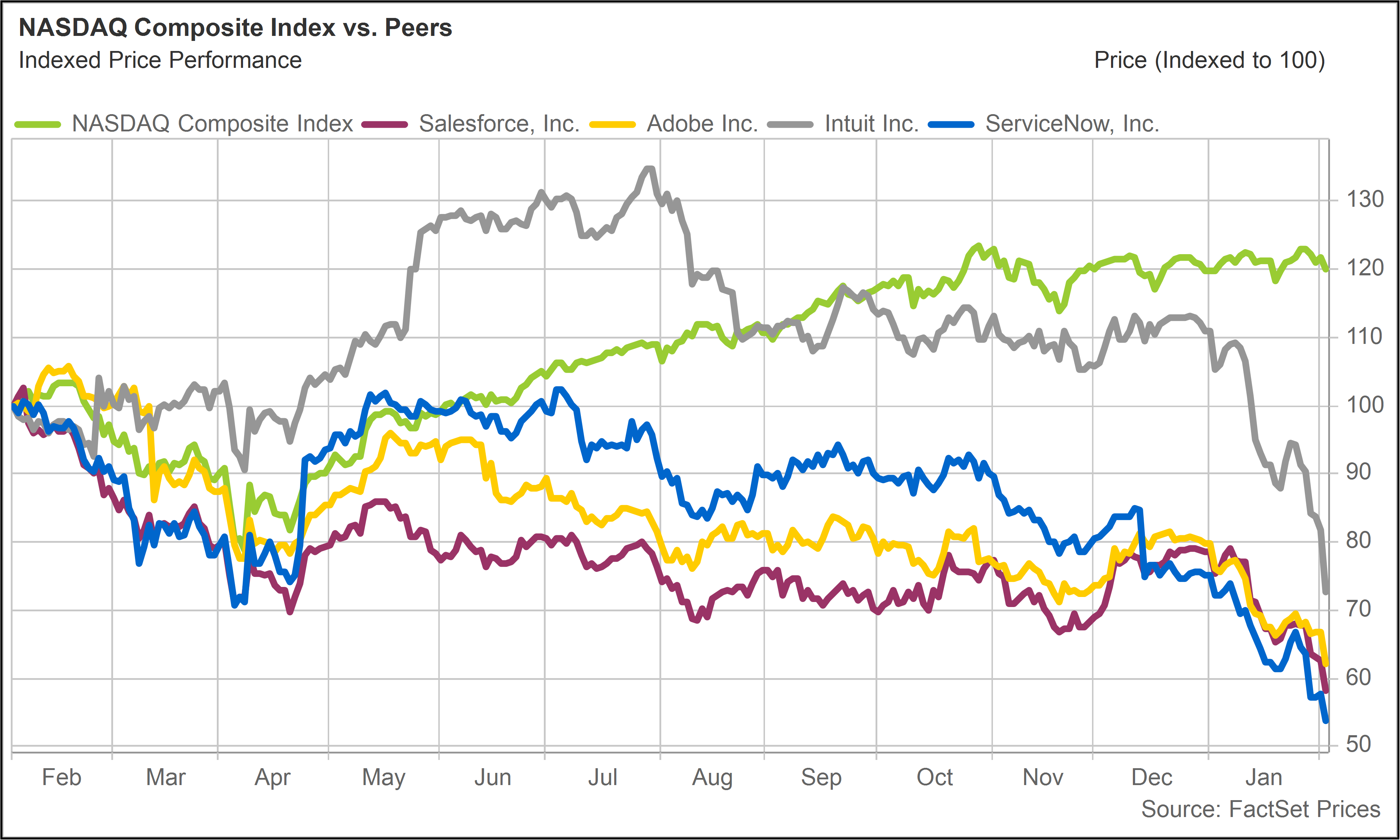

The large-cap software names mentioned above that have significantly underperformed in recent months may in some cases be undervalued now. But their long-term earnings growth may also be genuinely impaired.

In our Model Portfolios, especially our more technology and growth-oriented American Resilience portfolio, our top priority is to choose stocks that we believe stand to benefit from long-term developments in AI (and certainly not get injured by them).

This is because we view AI as probably the most impactful driver of technological, economic and social change of our lifetimes. (We discuss our approach to AI in more depth in our Guide to Investing in the Age of AI.)

While the goal is clear, the answers are not always obvious, as many tech investors over the last six months have discovered. Within the American Resilience portfolio, for example, we recently chose to exit a software stock that we concluded did have too much vulnerability to AI disruption.

It pays to be alert to these risks. That particular stock has since declined some 13% since its removal from the portfolio in mid-January.

AI will inevitably get cheaper, more powerful and more pervasive. Within and outside our tech investments, we are constantly stress testing our ideas to make sure this inevitability is an asset rather than a liability.

Investing beyond tech

While AI is a product of the tech sector, its impact is felt across all sectors of the economy, directly or indirectly. Given uncertainties around which particular tech stocks will prevail and which will suffer, many investors are now prioritizing other areas.

We are just over a month into the new year, but a key observation so far is that stocks in certain more traditional industries are in many cases performing quite well. AI is driving productivity and economic growth, benefiting these companies.

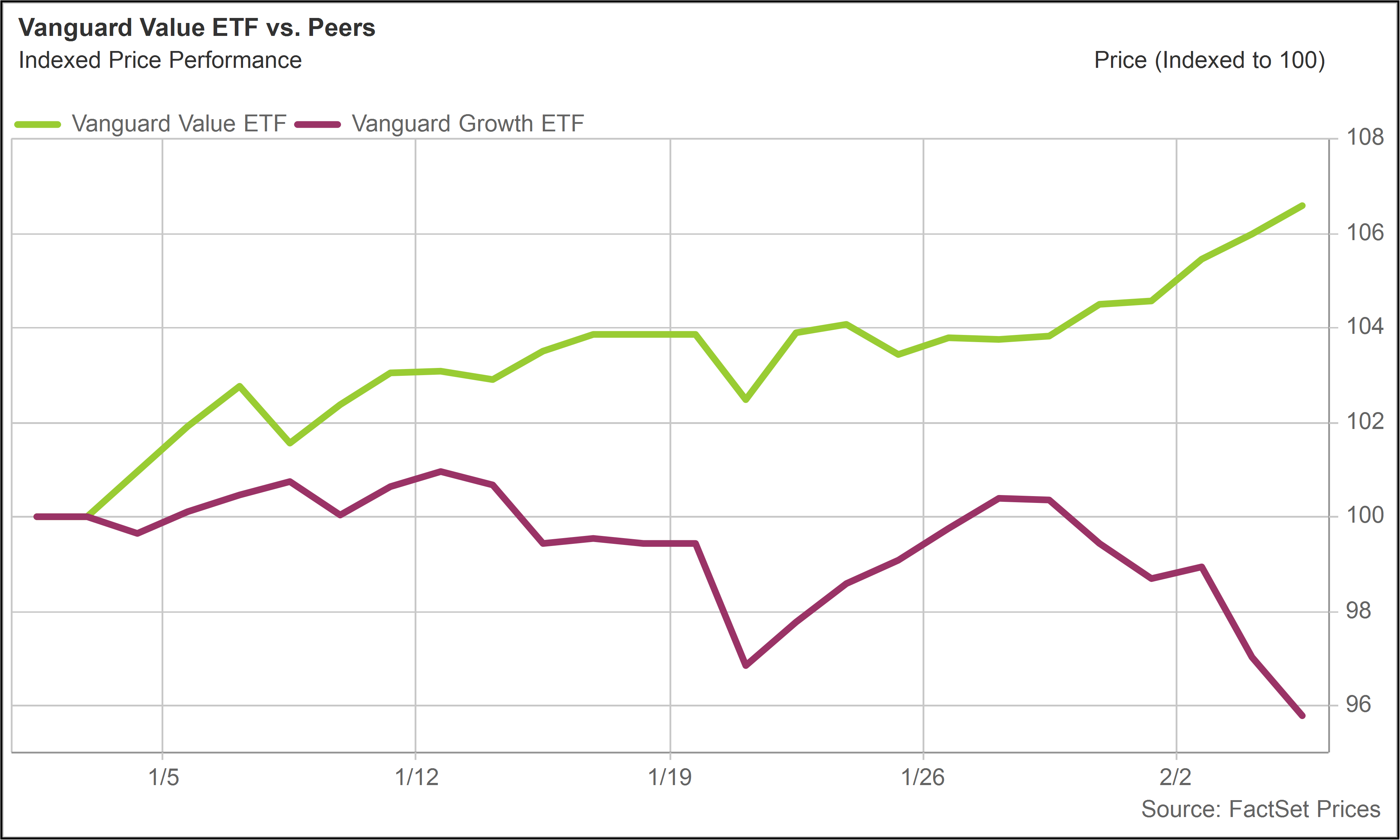

The Vanguard Value ETF (VTV), which tracks the large-cap value index, is in fact outperforming the Vanguard Growth ETF (VUG) by more than 10% on a year to date basis.

This is by historical standards a large dispersion as well as a trend reversal. The last decade has belonged to growth. Over the last ten years, VUG (420% total return) has substantially outperformed VTV (240% total return).