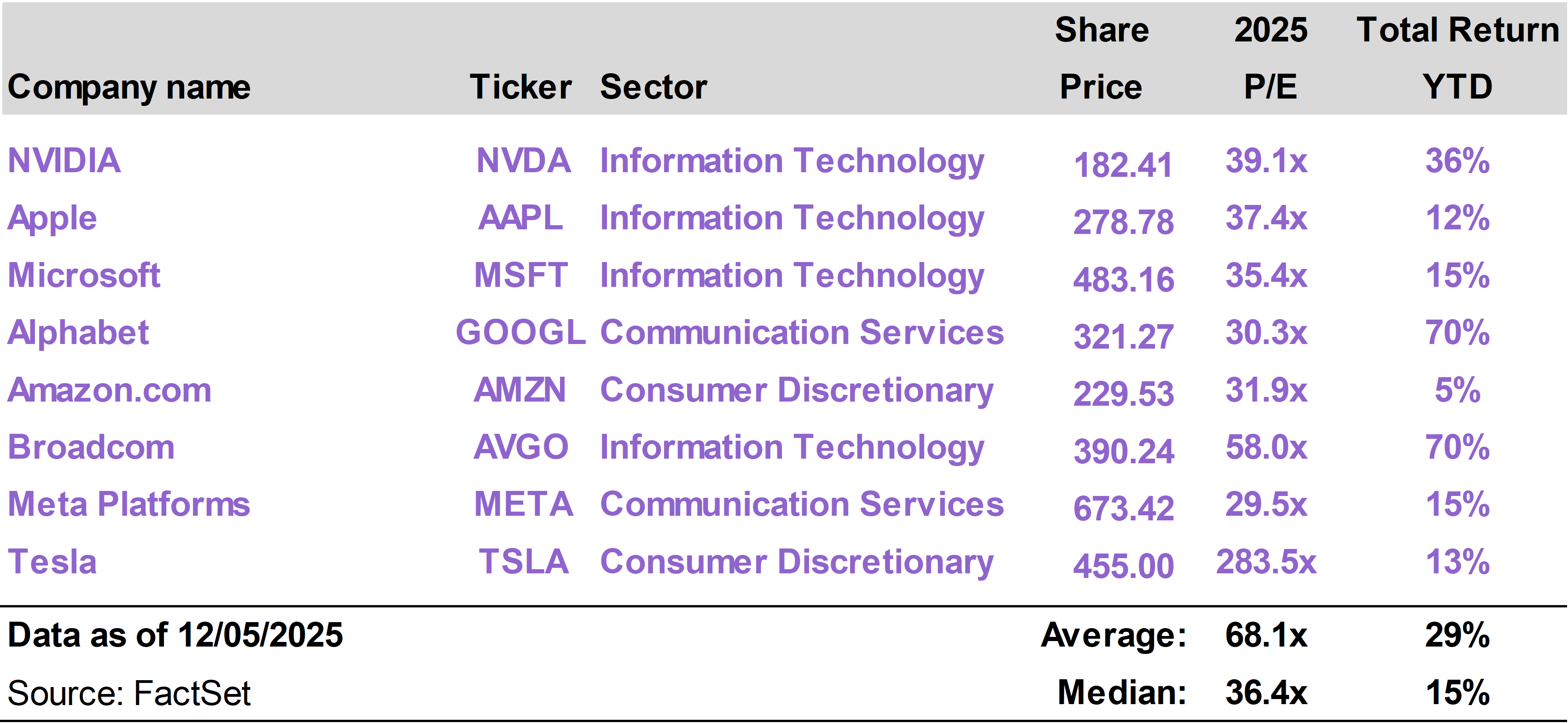

For starters, the Magnificent Seven (plus one) are important because they make up such a large chunk of the stock market. These eight stocks now represent almost 40% of the S&P 500. They are more than 50% of the Nasdaq-100.

But they are also crucial to understand because of their relevance to the economy. What they all have in common is a deep connection to the one structural trend that is reshaping everything—AI.

Just a few years ago, NVDA was a secondary player in the semiconductor space. Having emerged as the key hardware provider enabling the AI revolution, it now leads the Magnificent Seven as the most valuable company in the world.

All of these companies have extremely valuable legacy franchises that preceded the large-scale commercialization of AI. Yet they are all strategically adapting to an inevitable future in which AI is the dominant technological force.

Even a stock like TSLA, which many investors may view as a car maker, is inherently an AI play. The most important thing about Tesla vehicles is not that they are electric but that they are on their way toward becoming completely self-driving.

TSLA’s biggest long-term business opportunity may not even be cars. It could be humanoid robots, as Elon Musk has described. (See The Robots Are Coming: Positioning for the Next Leg of AI, recently published in the 76report.)

Why investors need to follow these stocks

The top reason investors should track these stocks is that, in all likelihood, they already own them.

The vast majority of investors have some (if not most) of their allocation to the stock market through index funds or funds that resemble major indexes like the S&P 500, the Nasdaq Composite, or the MSCI World.

It has been estimated that nearly one-third of stock market ownership is linked to passive or quasi-passive index approaches. Taking into account the large direct ownership of stocks by company founders and insiders, retail exposure to index strategies may be even higher.

To be clear, we support this sort of index exposure as a foundation for almost any investment strategy. The stock market, as a whole, delivers over time. Index exposure is low-cost, tax-efficient, and diversified.

Should they be owned?

Through index and related strategies, many investors have ended up with very large allocations to the Mag 7. Indexing has become, quite unintentionally, a mechanism for investing in these AI leaders.

Concerns about valuation and market concentration are valid, but we do believe it makes a lot of sense to have long-term, essentially permanent exposure to the Mag 7.

These companies have several unique qualities versus the rest of the stock market universe, justifying their place at the top of many investment portfolios.

In different ways, these businesses have carved out dominant positions across the digital economy, backing them with competitive moats that are hard to erode.

They are also, for the most part, immensely profitable. This means they have an unrivaled ability to reinvest their cash flows into innovation.

It also means they can take risks other companies cannot. They can operate with a long-term vision that is often absent within the typical public company.

Because technology changes so rapidly, these companies are not what they were five years ago. And they are not today what they will be in five years.

They are in a constant state of evolution that creates new upside opportunities for them. This helps explain their substantial outperformance over the years and separation from the rest of the pack.

The extent to which these stocks have in fact outperformed over the past ten years needs to be emphasized.

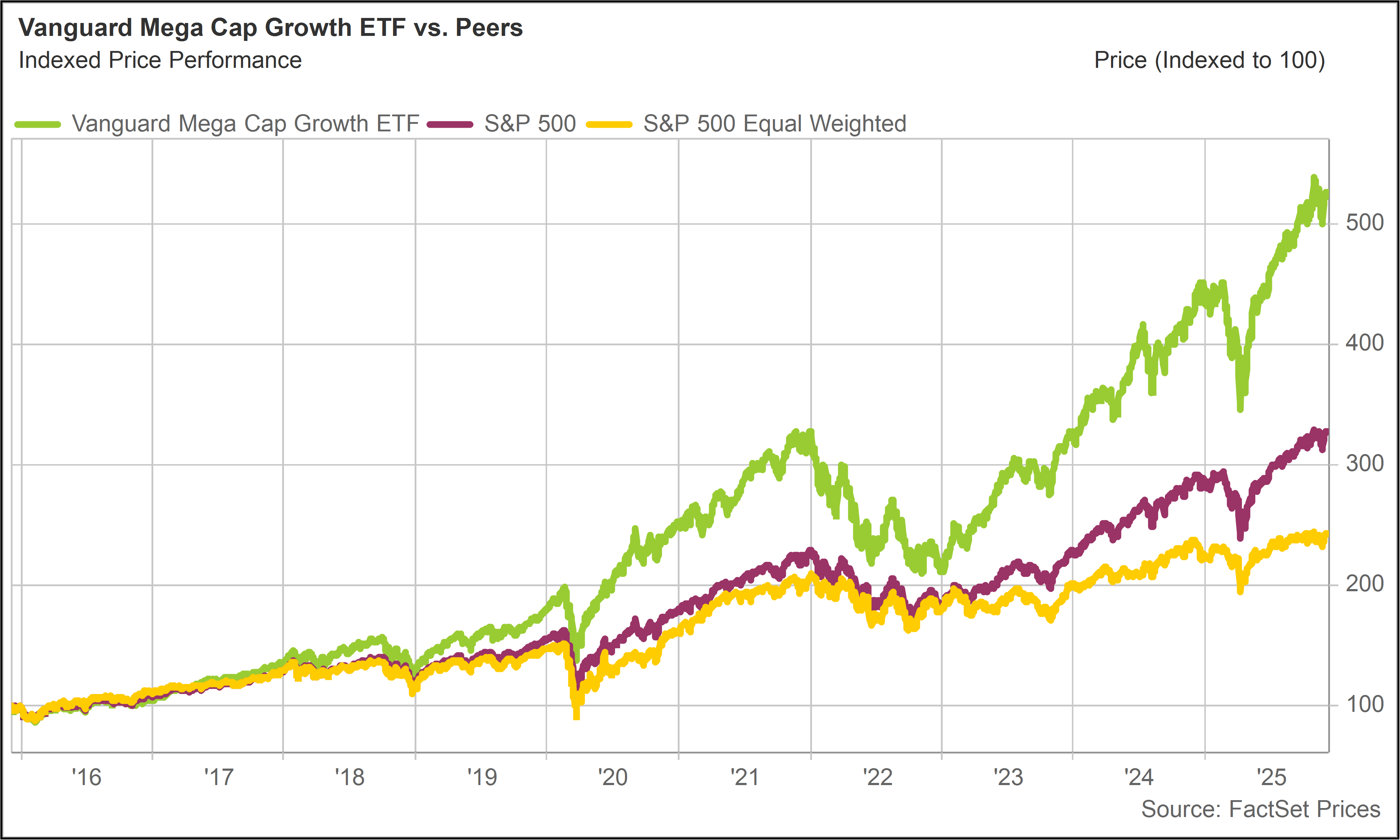

One of the most efficient ways investors can both track and access the Mag 7 is through the Vanguard Mega Cap Growth ETF (MGK).

MGK is a highly liquid (over $30 billion in assets) passive ETF that provides exposure to the largest market cap growth stocks. The Mag 7 (plus AVGO) now represent approximately two-thirds of the total value of MGK.

Powered by its high exposure to these names, MGK has returned over 400% over the past 10 years, versus just over 200% for the S&P 500 (which also has had high Mag 7 exposure).

For perspective, the S&P 500 Equal Weight Index (limited contribution from Mag 7) has returned less than 150% in this time frame.

As always, past performance is no guarantee of future success, but over the past ten years, having exposure to the Mag 7 has been a clear difference maker.