Better late than never

What we find most interesting about the JPMorgan report on the debasement trade is not so much its observations but that the mainstream financial community found them so noteworthy. From the standpoint of investors in gold and Bitcoin, these insights are quite familiar and obvious.

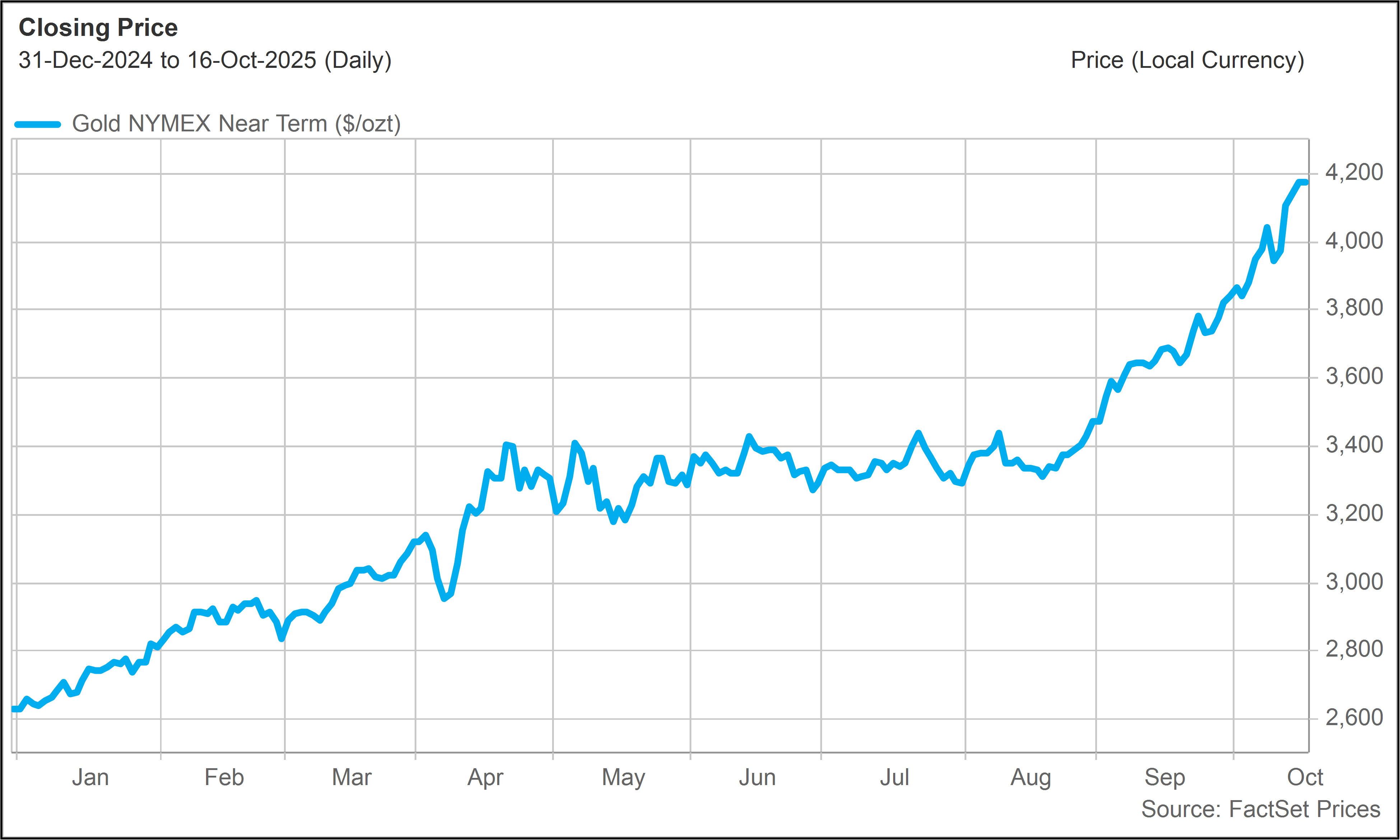

The JP Morgan note connects the debasement trade to a “combination of factors,” ranging from “elevated geopolitical and policy uncertainty, to uncertainty about the longer-term inflation backdrop, to concerns about ‘debt debasement’ due to persistently high government deficits across major economies, to concerns about Fed independence, to waning confidence in fiat currencies in certain emerging markets in particular, and to a broader diversification away from the US dollar.”

In other words, investors are now responding to all of the core macroeconomic themes we have been explaining to subscribers over the past two years, from our April 2024 note on gold (Gold Advances, Justifiably) to our September 2024 note on Bitcoin (Dollar-Proofing Your Portfolio).

How far will the debasement trade go?

Wall Street conventional wisdom is perhaps finally catching up. For those who may already be positioned to benefit from the monetary debasement theme, the key question is how much further can it go and what are the best ways to play it.

These are complicated questions, given that the debasement trade has multiple drivers. Below, we will provide our updated thinking on the key asset classes connected to the debasement trade: gold, crypto and stocks…

To continue reading The Great Debasement Theory, subscribe now to the 76report.

Use promo code DOLLAR and pay only $1 per month for the first two months.

Click HERE to begin!