|

| Inflation Protection Model Portfolio |

|

| Monthly Portfolio Review: August 2025Publication date: September 2, 2025 |

|

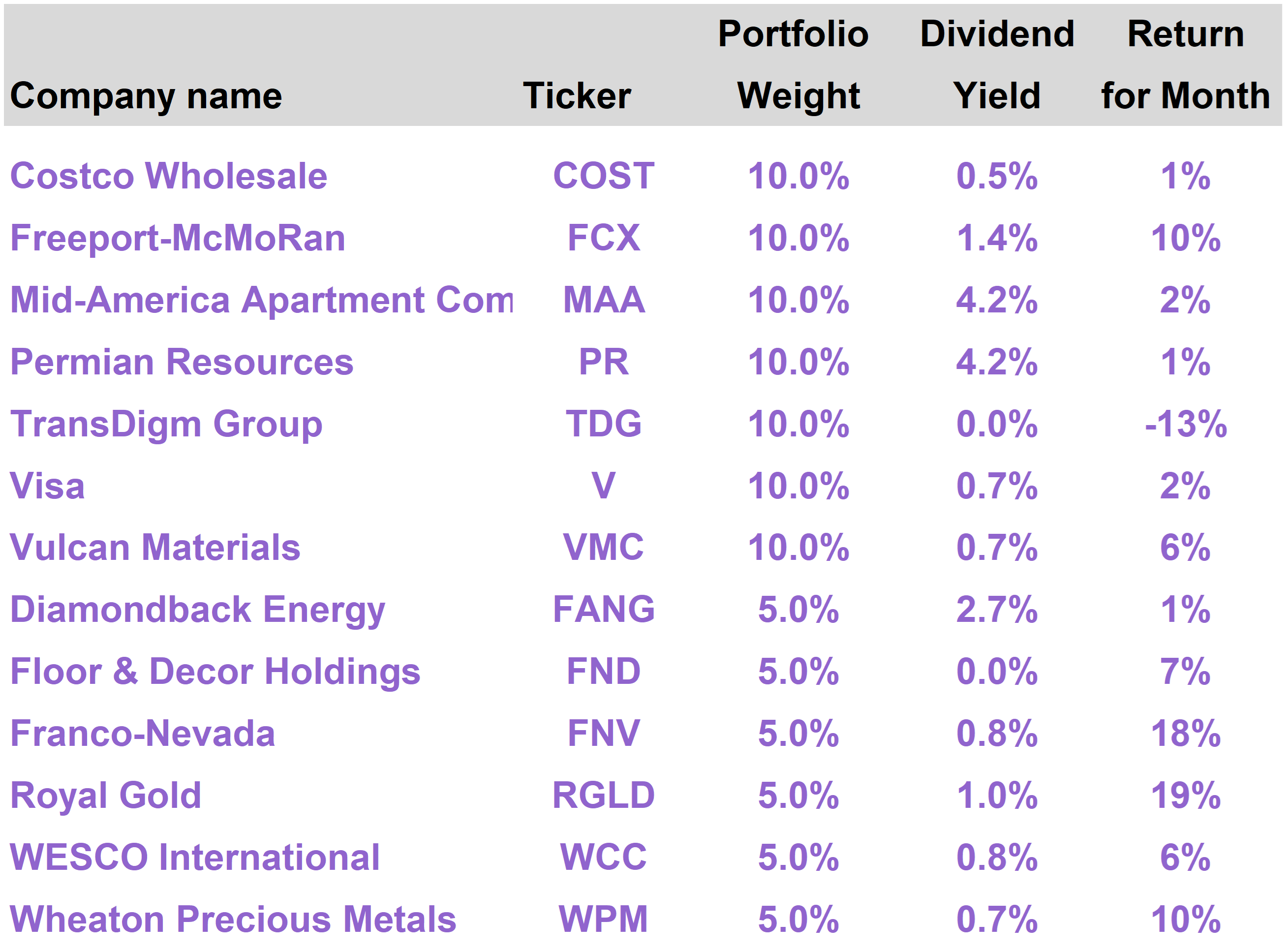

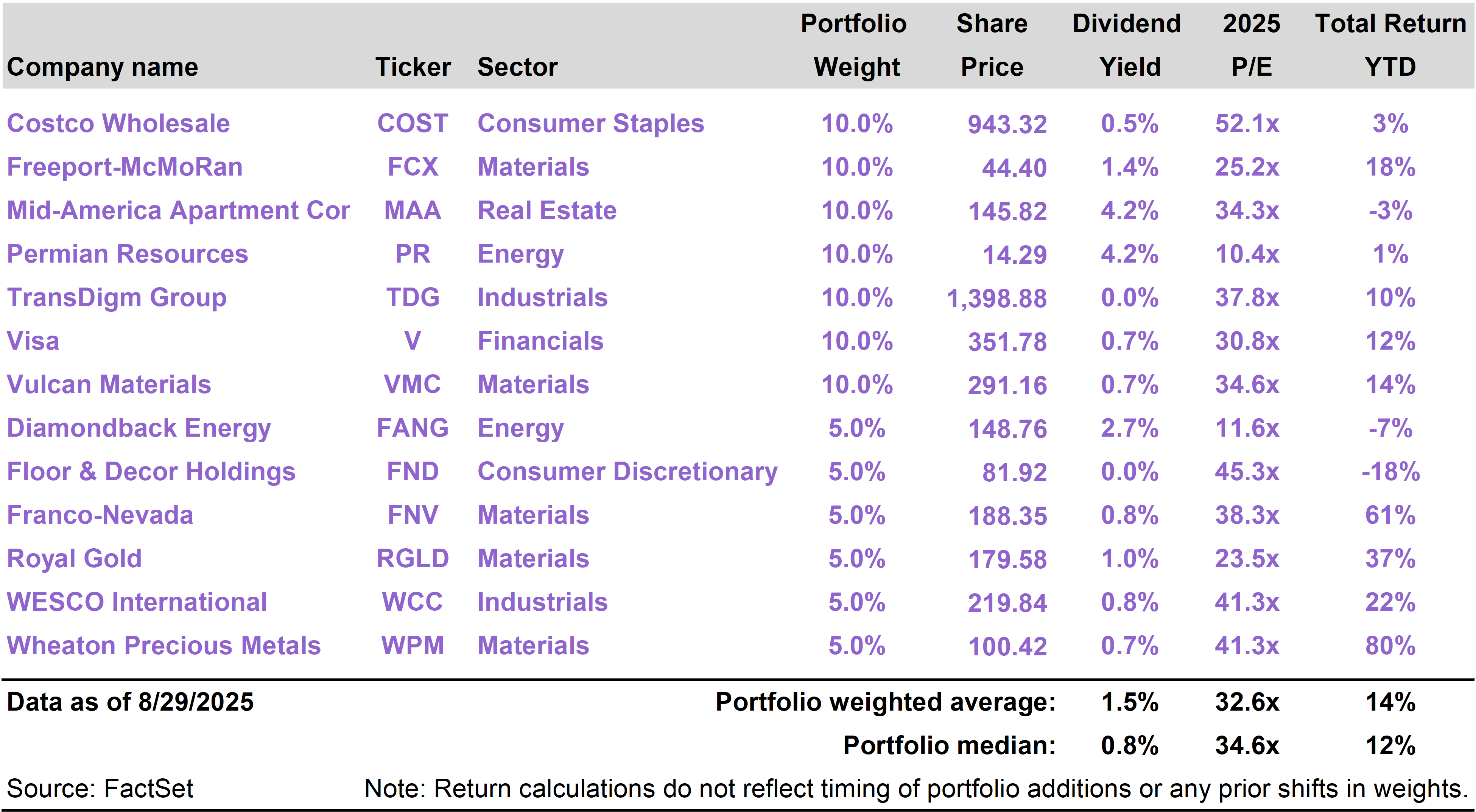

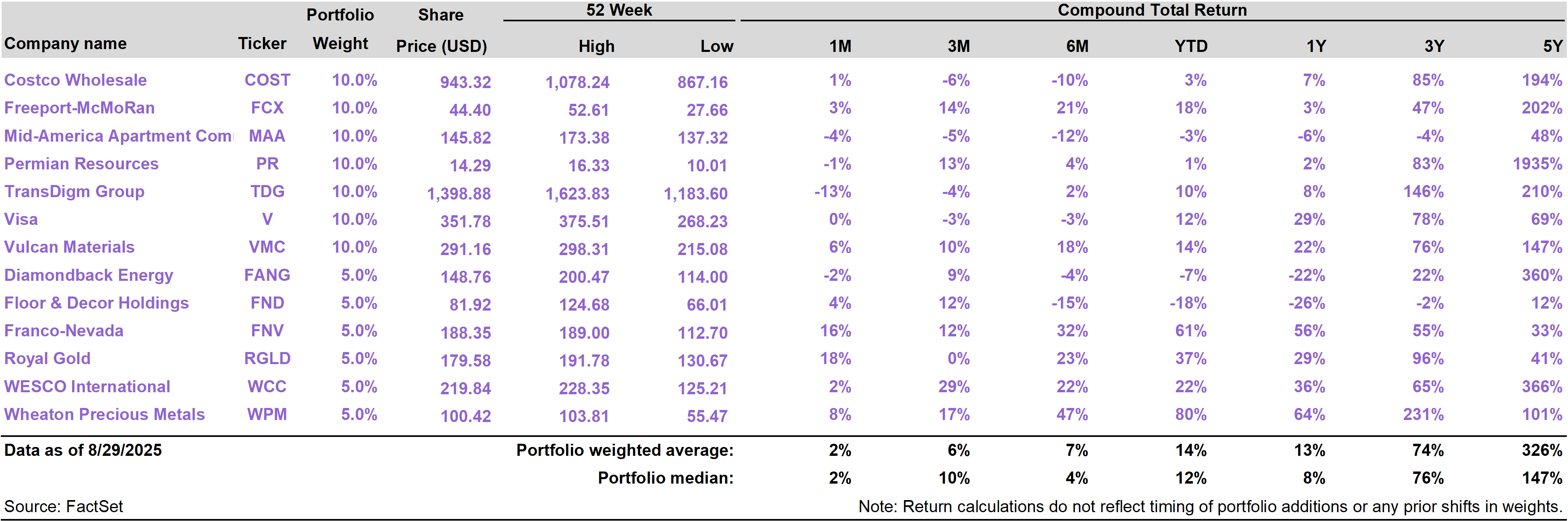

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | Stocks moved higher in August with tech stocks taking a back seat to other sectors. Jerome Powell delivered a positive surprise at Jackson Hole by opening the door to future rate cuts in response to labor market uncertainty. The Inflation Protection delivered a total return of 4% in August, well ahead of the S&P 500 Index. The portfolio was led by its gold-related names, which delivered returns between 10% and 19% during the month. One position in the portfolio produced a loss; TransDigm (TDG) shares were punished for a slight earnings miss. Gold advanced 5.5% in August in response to perceptions of easier monetary policy going forward. Continued pressure by the Trump administration on the Fed should help drive upside for gold and inflation-sensitive assets.

|

|

| | | The Inflation Protection portfolio returned 4.0% in August, versus a total return of 2.0% for the S&P 500 Index. On a year to date basis through the end of August, the portfolio has generated a total return of 11.7%, versus a 10.8% return for the S&P 500.

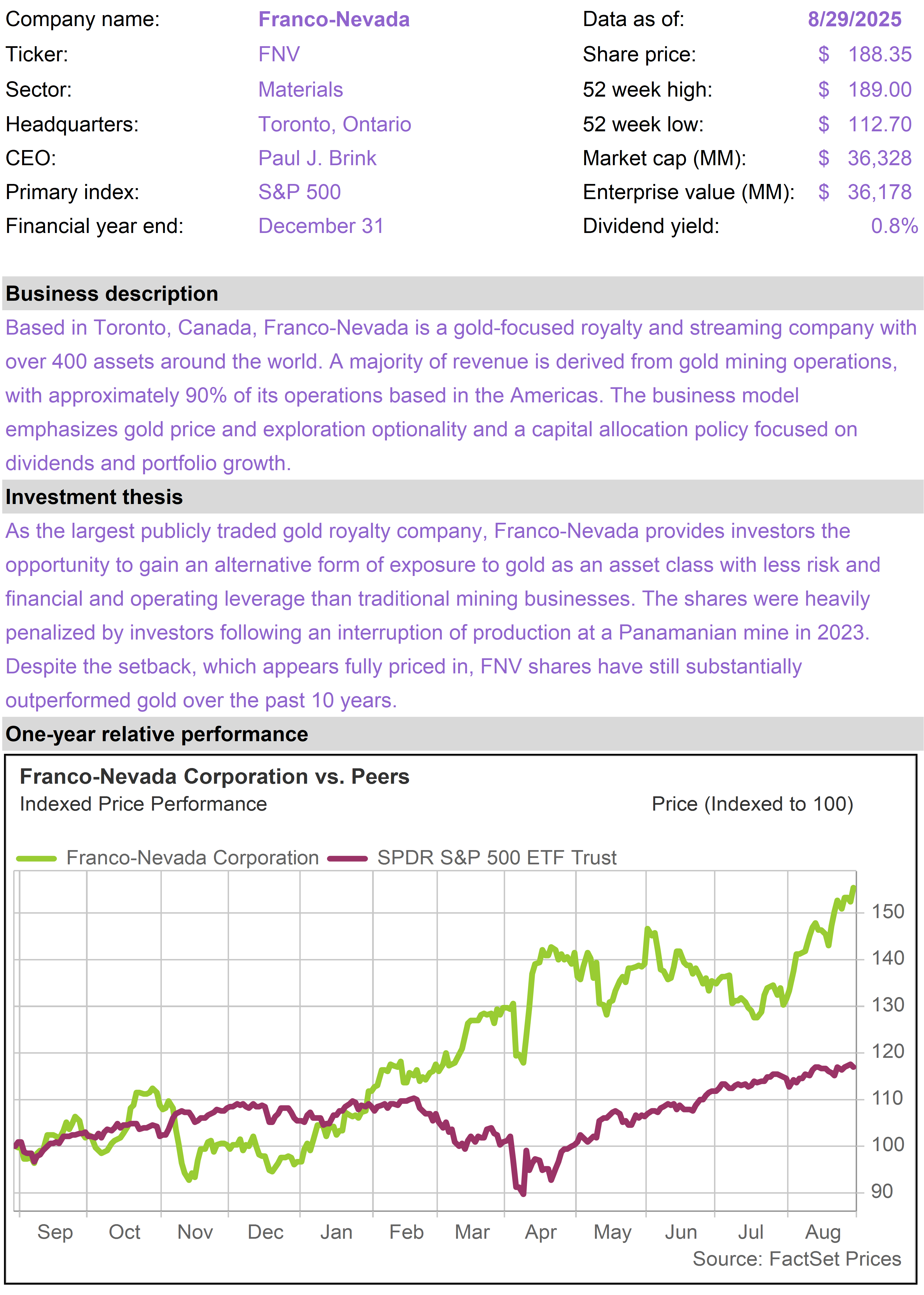

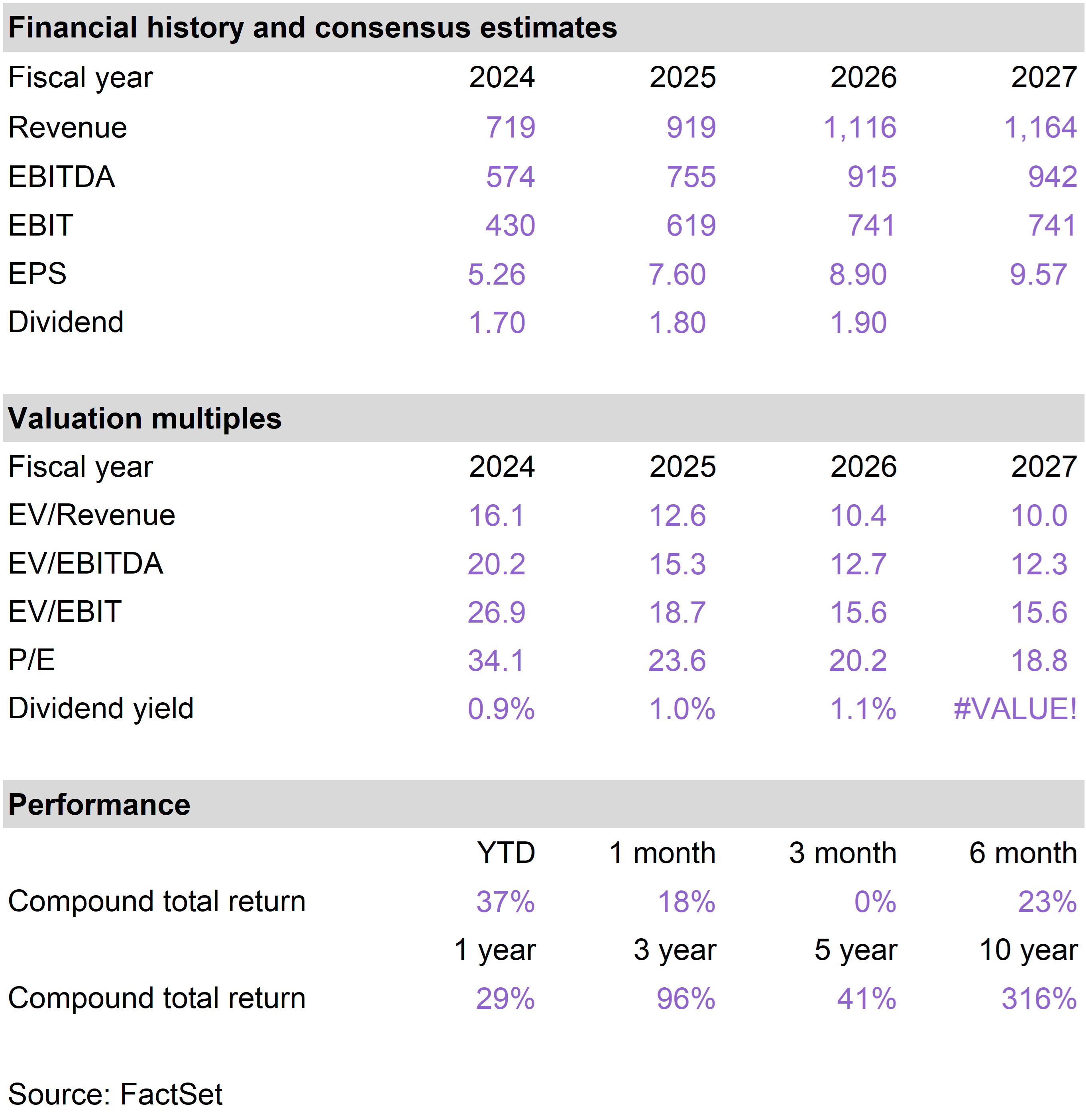

The portfolio’s top performing stocks this month were Royal Gold (RGLD), which returned 19%; Franco-Nevada (FNV), which returned 18%; Freeport-McMoRan (FCX), which returned 10%; and Wheaton Precious Metals (WPM), which returned 10%.

The only position that delivered a negative return was TransDigm Group (TDG), which declined 13%. |

|

| Stocks Move Higher

Investors in the stock market saw continued success this month, with the S&P 500 Index breaking 6,500 for the first time on August 28, the second to last trading day of the month. |

|

|

| S&P 500 and NASDAQ CompositeTotal Return (12/31/24 - 8/29/25) |

|

| Market momentum in August was mainly driven by optimism over falling interest rates, paired with confidence in an economy that is generally healthy, despite some pockets of concern.

Interestingly, stocks performed well this month even though sentiment towards the AI theme wobbled. Tech stocks actually underperformed as other sectors priced in the more favorable interest rate outlook.

The major macro development in August was the Federal Reserve symposium in Jackson Hole, Wyoming. As we discussed in Powell Finally Leans Towards Rate Cuts, stocks surged in the immediate aftermath of Jerome Powell’s highly anticipated speech on August 22.

Whether or not it had anything to do with months of browbeating by President Trump to start cutting interest rates, Powell finally acknowledged that the pendulum should start to swing in the direction of easier monetary policy.

Powell’s key message was that labor market conditions are looking increasingly fragile.

In light of the Fed’s dual mandate of maximizing employment while keeping prices stable, he made the point that more consideration would likely have to be given to supporting employment through lower interest rates going forward.

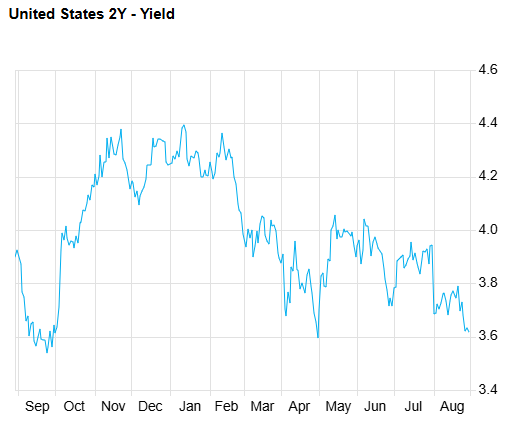

In addition to strong upward movement in stocks, we saw an immediate positive reaction in bonds.

By the end of August, yields on 2-Year Treasuries were about 0.3%, or 30 basis points, lower than where they were at the start of the month. This suggests that the market has priced in at least one incremental 25 basis point cut in the Fed funds rate over the next two years. |

|

|

| 2-Year Treasury Yields(Last 12 Months) |

|

| Yields on 10-Year Treasuries did not decline relative to where they started the month but ended the month around 4.2%. This is close to the lowest levels they have reached since Trump was elected. |

|

|

| 10-Year Treasury Yields(Last 12 Months) |

|

| Growth and lower rates

The sweet spot for stocks is low interest rates paired with a healthy growing economy.

Low interest rates—and, more generally, easy monetary policy—help the stock market for a number of reasons.

When rates are lower, fixed income alternatives (money market funds, bonds, etc.) are less attractive. This increases demand for stocks.

At the same time, easier monetary policy means there is more liquidity in the financial system—basically more money sloshing around. This extra liquidity has a tendency to find its way into the stock market along with other assets.

A prime example is the strong market rally from mid-2020 through year-end 2021, when the Fed brought rates close to zero in response to the pandemic. In the 18 month period between 6/30/2020 and 12/31/2021, the S&P 500 returned approximately 57%.

Low interest rates and easy monetary policy, however, do not typically coincide with strong economic growth. The main purpose of low interest rates is to stimulate economic growth and ward off recession.

While lower interest rates are good for stocks, a weak economy is definitely not.

With the exception of extremely defensive or counter-cyclical businesses, the vast majority of businesses benefit from growing consumer spending and business investment and high levels of economic confidence.

At the moment, there are no serious indications of recession.

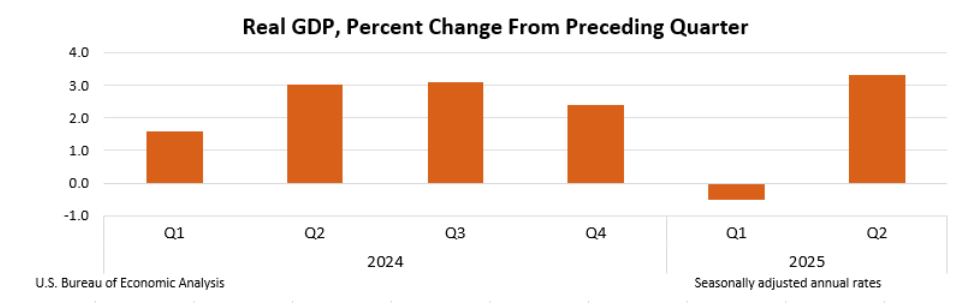

On August 28, the Bureau of Economic Analysis (BEA) released its “second estimate” of second quarter economic growth. The BEA substantially increased its real (i.e., inflation-adjusted) GDP estimate, from 3.0% to 3.3%. |

|

|

| Why lower rates?

With the economy performing well, corporate earnings strong, stock indices at all-time highs and inflation still coming in above the targeted 2% level, it is natural to question why we should be moving in the direction of lower interest rates.

The answer, in our view, is that we are increasingly moving towards a two-tiered economy, as we addressed in Surviving (and Thriving) in the AI Economy, our recent thought piece on AI.

Now more than ever, the stock market is not the economy.

Take NVIDIA (NVDA), the most valuable stock in the world. It has a $4.2 trillion market cap, which represents some 8% of the S&P 500 Index. Yet the company only has 36,000 employees.

For perspective, there are approximately 160 million people who are actively employed in the United States. NVDA may be 8% of the most important stock market index, but it only employs about 0.02% of the U.S. population.

Technologies related to AI will drive productivity gains and create tremendous wealth for asset owners, but these same productivity gains have may come at the expense of ordinary wage earners.

Knowledge workers seeking a paycheck will be going head to head with supercomputers in the cloud that are becoming smarter and faster every day.

AI may create problems for us (and/or our children) as we aim to stay relevant as contributors to a rapidly changing economy. For us as investors, however, it may usher in a very positive set of circumstances.

AI has the potential to drive both strong profit growth and easier monetary policy, which may be needed to support faltering labor markets.

Powell himself did not have a clear explanation as to what is behind the labor market uncertainty that he talked about at Jackson Hole. It may be that the AI productivity story is just getting started.

AI wobbles in August

While AI has the potential to drive vast changes in the economy and society in the years and decades ahead, AI as an investment theme will not necessarily follow a straight and smooth path forward.

AI is an evolving technology. There will be winners and losers. There will be setbacks and surprises along the way.

Investors experienced shifting sentiment towards AI in August, as high growth expectations were weighed against high valuations in many cases. When the stakes are high, negative data points that emerge can quickly lead to selling pressure. |

|

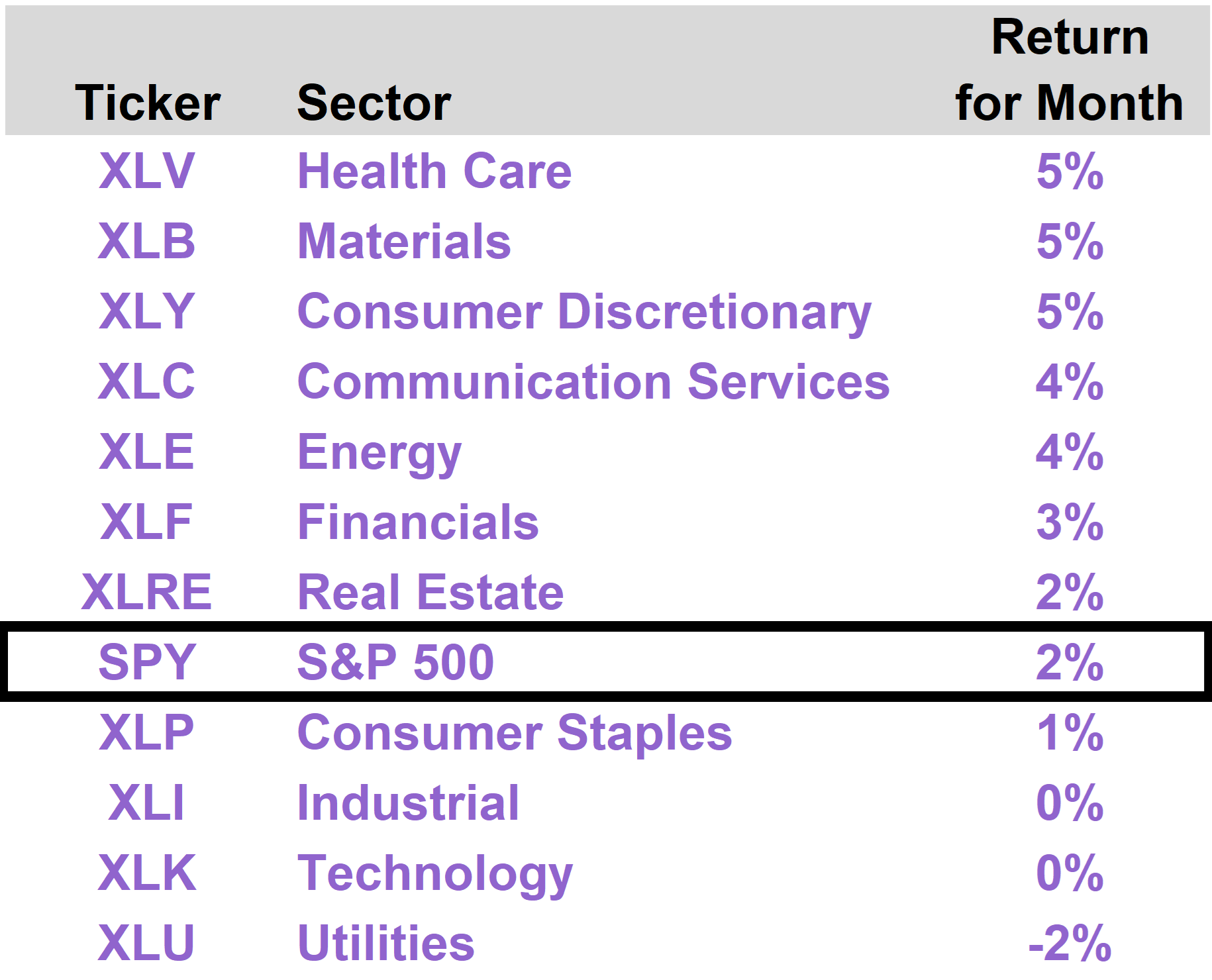

| Despite the 2% rise in the S&P 500, Technology sector stocks were actually flat in August, reflecting pressure on some AI-related names.

Shares of AI-bellwether NVDA were down marginally in August (approximately 2%) after the company reported second quarter earnings. While the earnings report was strong overall, investors are worried about the outlook for China (see NVIDIA Reports: The AI Race Is On).

There were some other high-profile AI stocks that disappointed investors in August.

Marvell Technology (MRVL) is a player in AI technology infrastructure. MRVL posted strong growth but offered forward guidance that was below expectations. MRVL shares declined more than 20% in August.

Shares of Dell Technologies (DELL) fell 8% in August. DELL has become a major provider of servers and storage systems to AI data centers. DELL lifted revenue guidance but noted significant margin pressure as it competes for business within its niche.

We regard AI as a powerful and enduring investment theme, but August volatility highlights the fact that not all AI plays will succeed, which underscores the need for careful stock picking.

While Tech and AI have occupied the limelight for much of the past two years, the improved outlook for rate cuts in August allowed some other sectors to shine.

Health Care, Materials and Consumer Discretionary each advanced 5% in August.

The Utility sector declined 2% in August, but this should be seen in the context of relinquishing strong gains from the prior month. Utility stocks were the top performing sector in July and advanced 5%. |

|

|

| | An independent central bank?

Powell’s Jackson Hole pivot towards lower rates came as the administration has pursued the removal of Fed Governor Lisa Cook, based on allegations of mortgage fraud.

Cook appears to have applied for and obtained simultaneous mortgages on different homes that she indicated would be her primary residence. Mortgages on primary residences are easier to obtain and typically involve lower interest rates.

There are interesting and complicated legal questions surrounding Trump’s authority to fire Cook “for cause.” But what is perhaps more important is the position that Jerome Powell now finds himself in.

If Powell fails to support what could be determined to be Trump’s legitimate right to remove a Fed Governor, Powell himself may have committed a serious offense.

Gold tends to respond well whenever politicians make their way closer to the money printer.

As the Trump administration continues to apply pressure to the Fed, gold is starting to recover some of its strong momentum from earlier in the year.

Gold ended the month of August at just under $3,450 per ounce, very close to its highest level ever. Gold advanced 5.5% in August.

Meanwhile, gold mining stocks, which are often more responsive to shifting sentiment towards gold, saw large upside in August. The VanEck Gold Miners ETF (GDX), a widely owned gold mining fund, advanced more than 20% in August. |

|

|

| Gold and Gold Mining ETF(Total Return - Last 12 Months) |

|

| The Trump administration is now overtly challenging the very idea of Fed independence. In a recent interview, in which Lisa Cook’s firing was raised, Vice President JD Vance was forthright on this topic. |

|

| | I thought that the people controlled this country through their elected representatives, including the President of the United States. I don’t think we allow bureaucrats to sit from on high and make decisions about monetary policy and interest rates without any input from the people that were elected to serve. - JD Vance (8/28/2025) |

|

| | The Federal Reserve, of course, has never been a truly independent body. It is a creation of Congress, and the President chooses its leadership. There are many safeguards in place, however, that inoculate the Fed from direct day-to-day political interference.

While Jerome Powell is now already leaning in the direction of rate cuts, his successor in the first half of next year (if not sooner) is clearly going to be someone who aligns with the Trump administration on interest rates.

Easier monetary policy represents a tailwind for almost all asset classes, from stocks to gold to crypto. If we start to see convincing evidence of AI-related weakness in hiring, this sets the stage for much easier monetary policy going forward, even if inflation remains somewhat elevated. |

|

| | | The top performing stocks in the Inflation Protection portfolio this month were Royal Gold (RGLD), which returned 19%; Franco-Nevada (FNV), which returned 18%; Freeport-McMoRan (FCX), which returned 10%; and Wheaton Precious Metals (WPM), which returned 10%.

The only position that delivered a negative result this month was TransDigm Group (TDG), which declined 13%. |

|

| After a very strong start to the year, the portfolio’s trio of gold streaming plays, RGLD, WPM and FNV, lost some ground when the gold price leveled off in the mid-April through July time frame.

With the gold price having advanced 5.5% in August, as Powell pivoted towards rate cuts and Trump kept the pressure on the Fed, investor sentiment towards gold-related stocks has markedly improved.

Gold is now up more than 30% year to date. RGLD, WPM and FNV each provide levered exposure to the gold price and are each exceeding gold’s return. |

|

|

| Gold vs. RGLD, WPM, FNV(Total Return - Last 12 Months) |

|

| RGLD’s strong return this month was also driven by its strong second quarter earnings performance as the company generated record-setting cash flow.

Powell’s shifting stance and other developments at the Fed appear to be reigniting interest in gold as an asset class, potentially setting the stage for another leg up. We would not be surprised to see our gold streaming names outperform gold in that context.

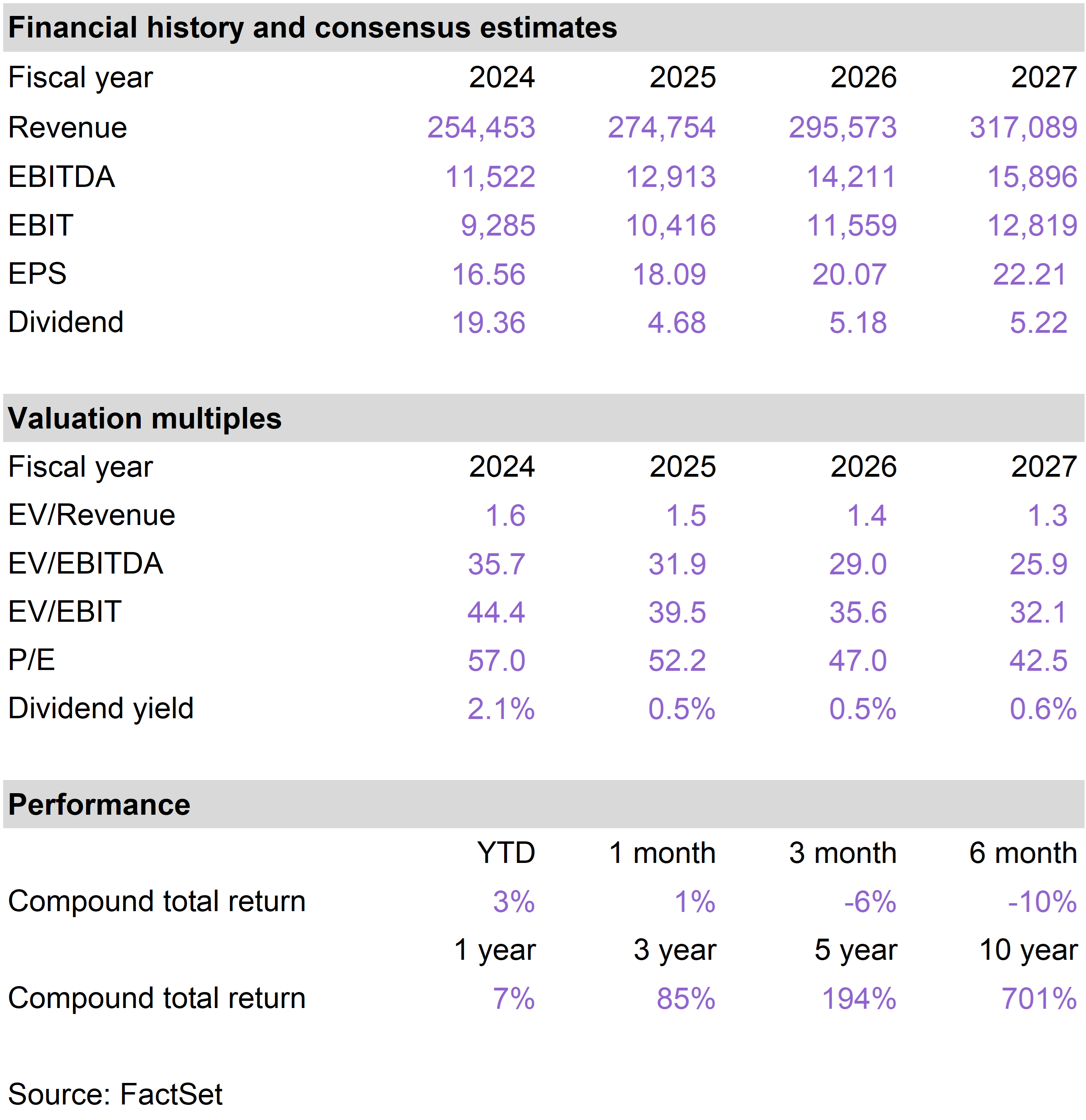

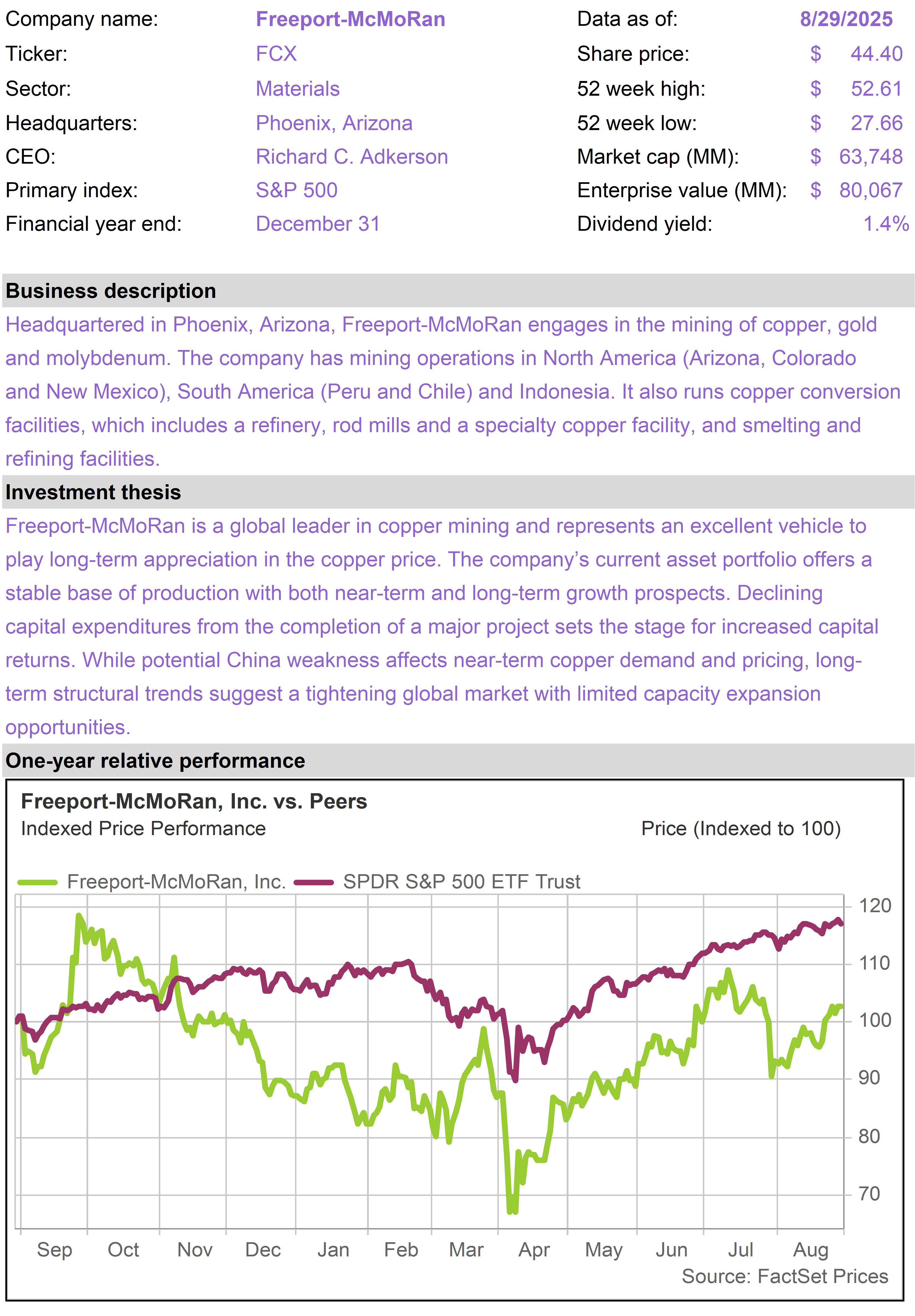

Thanks to repeated changes to Trump’s copper tariff policy, FCX has had a turbulent year. But FCX performed well in August as investors digested the removal of the proposed 50% tariff on imported copper.

As a major domestic producer, FCX stood to benefit from the proposed tariff scheme, which created a premium for U.S.-produced copper over foreign copper. This premium was visible in the higher copper prices that prevailed on exchanges in New York versus London.

With the end of July clarification that tariffs will only be applied to semi-finished copper products and copper derivatives, copper prices plunged in New York and immediately converged with global prices. |

|

|

| Copper - New York vs. London(Total Return - Last 12 Months) |

|

| FCX stood to benefit as a U.S. producer, but the decision was in our view the correct one.

American firms will now continue to have unimpeded access to global copper supplies. This is especially important given the critical role of copper as an input into nearly every electrical product or system.

FCX has copper mines outside the U.S. as well and in that sense benefits from the elimination of the tariff.

With the tariff distraction removed, investors now appear to be focusing their attention on the core value proposition of FCX as a leading global copper producer with an impressive operational track record and top quality assets.

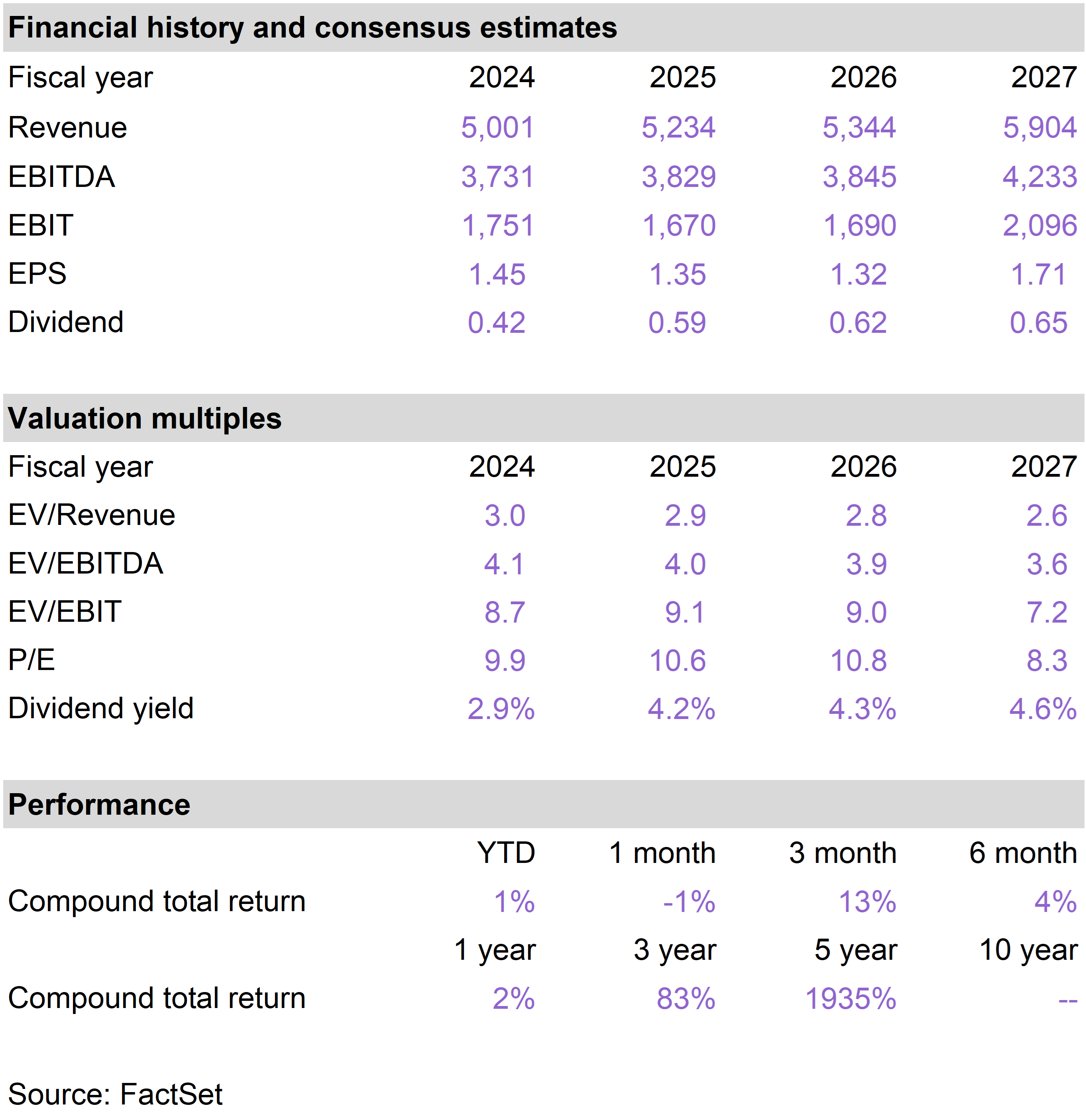

TDG is a leading aerospace equipment manufacturer with strong pricing power from its dominant position in aftermarket parts, where competition is minimal. Shares of TDG were punished after the company reported earnings in August and slightly missed.

Management remains optimistic that demand will normalize later this year in the commercial segment, where it experienced the shortfall.

Investors in TDG should be aware that the company will be paying a one-time special dividend of $90 per share on September 12. This equates to an approximately 6.4% divided yield.

The ex-date for this dividend is September 2, so only current TDG shareholders will be eligible to receive it. The share price of TDG will adjust downward in the coming week to reflect payment of this sizable dividend.

TDG has a long track record of paying special dividends. The company stands out for its thoughtful management of its balance sheet, including its value-accretive approach to strategic acquisitions of smaller industry players. |

|

| | |

| | |

| | |

| | | |

|

| | |

|

| | Mid-America Apartment (MAA) |

|

|

|

| |

|

| | |

|

| | |

|

| | |

|

| | Diamondback Energy (FANG) |

|

|

|

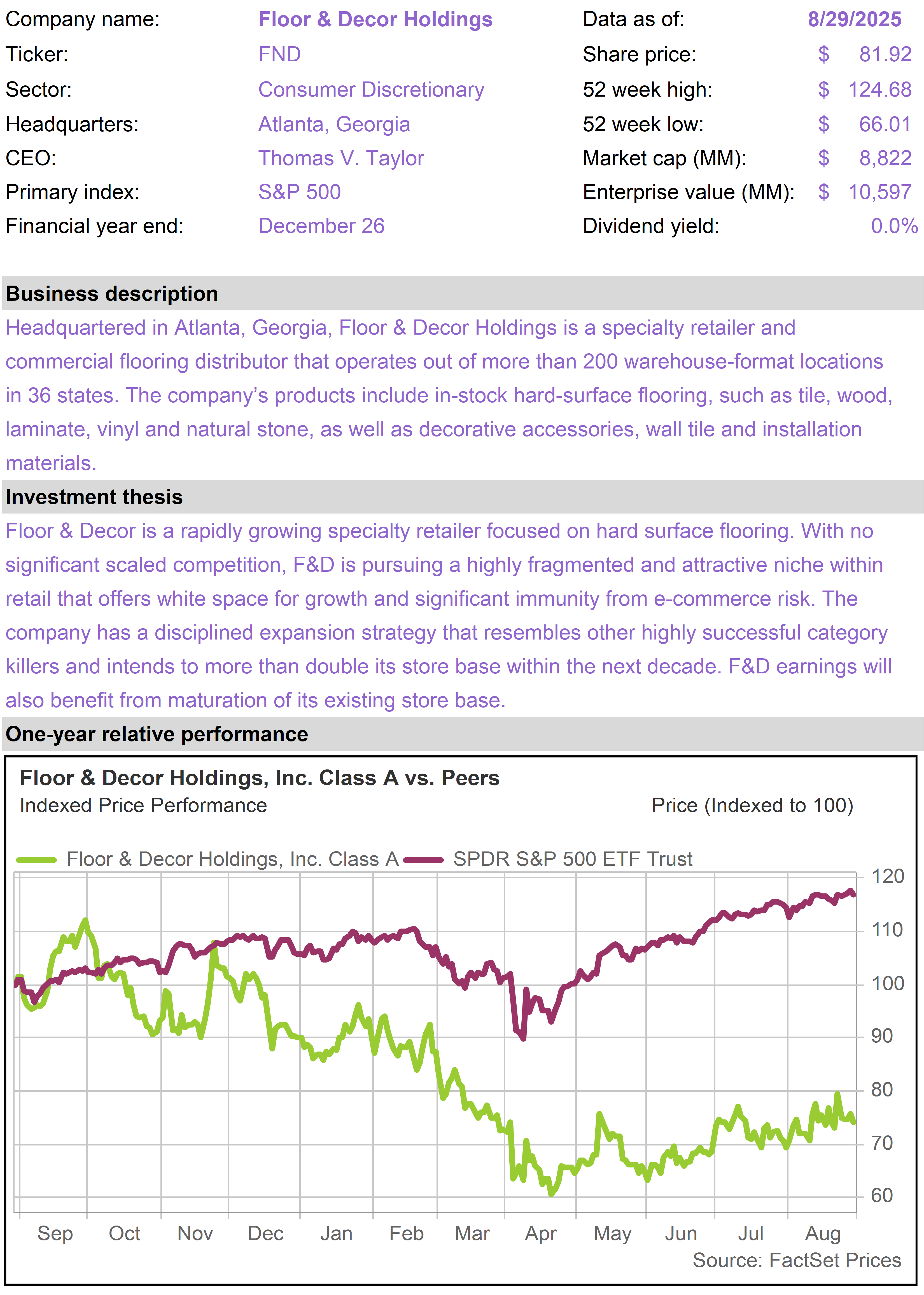

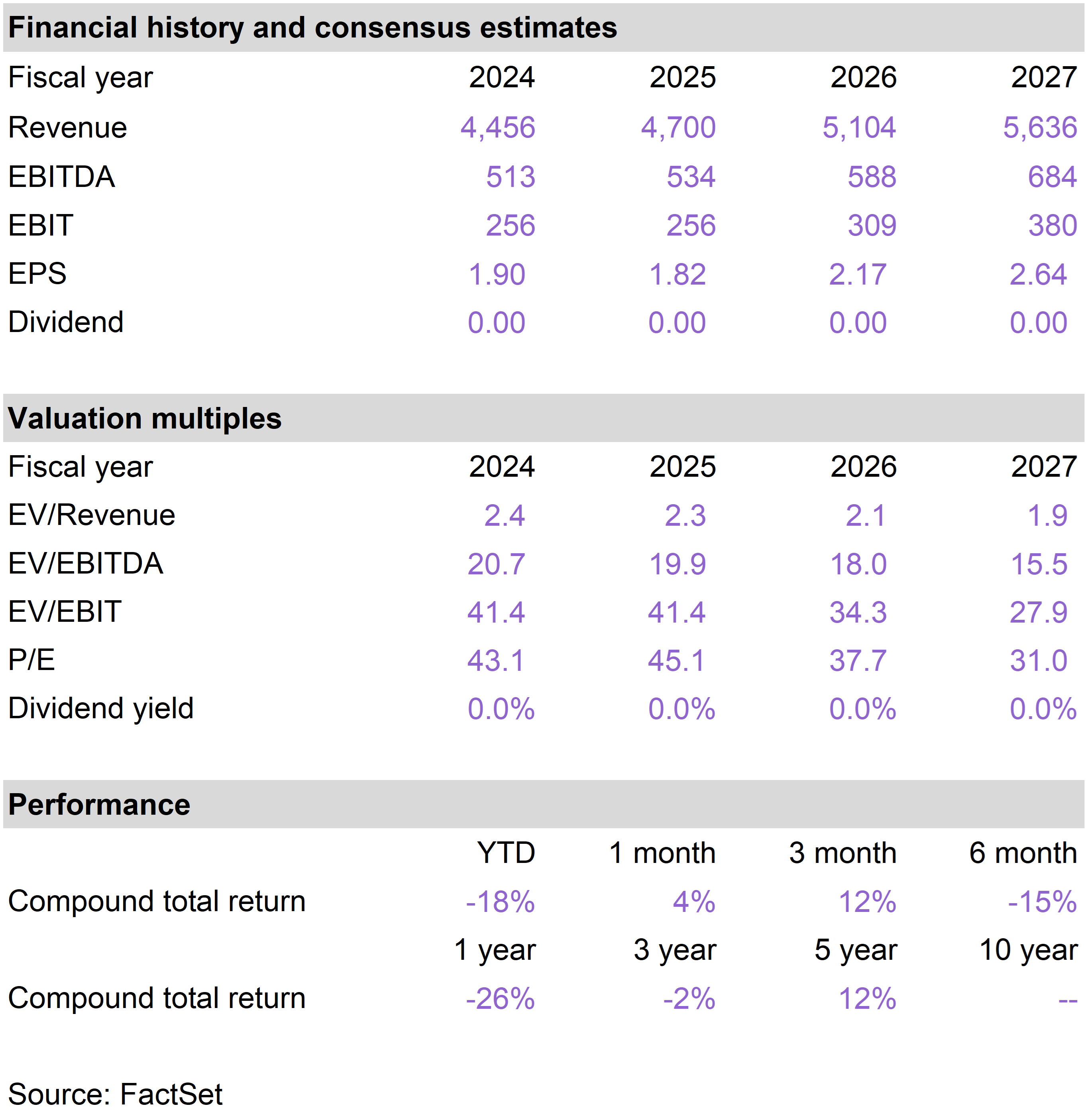

| | Floor & Decor Holdings (FND) |

|

|

|

| | |

|

| | |

|

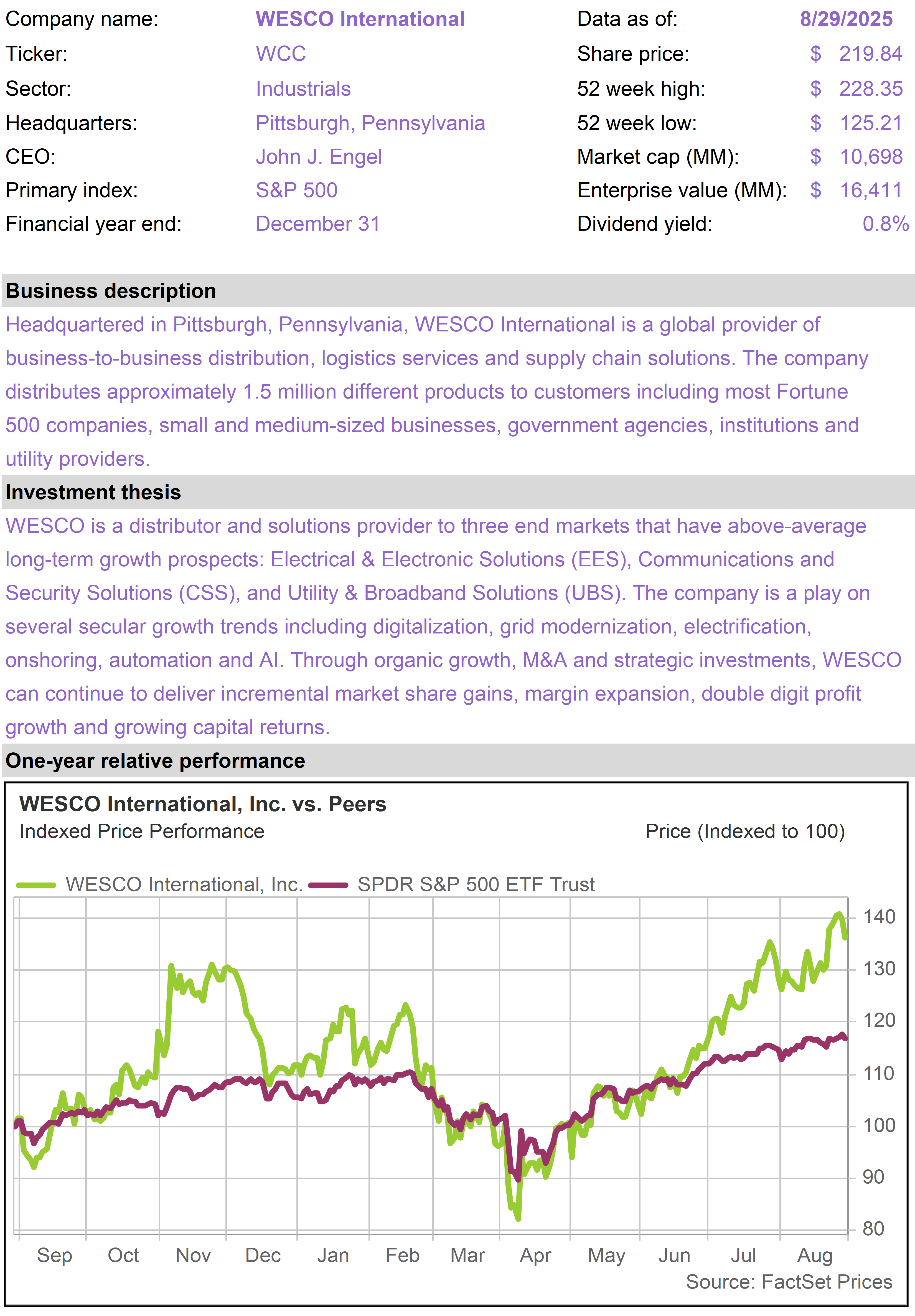

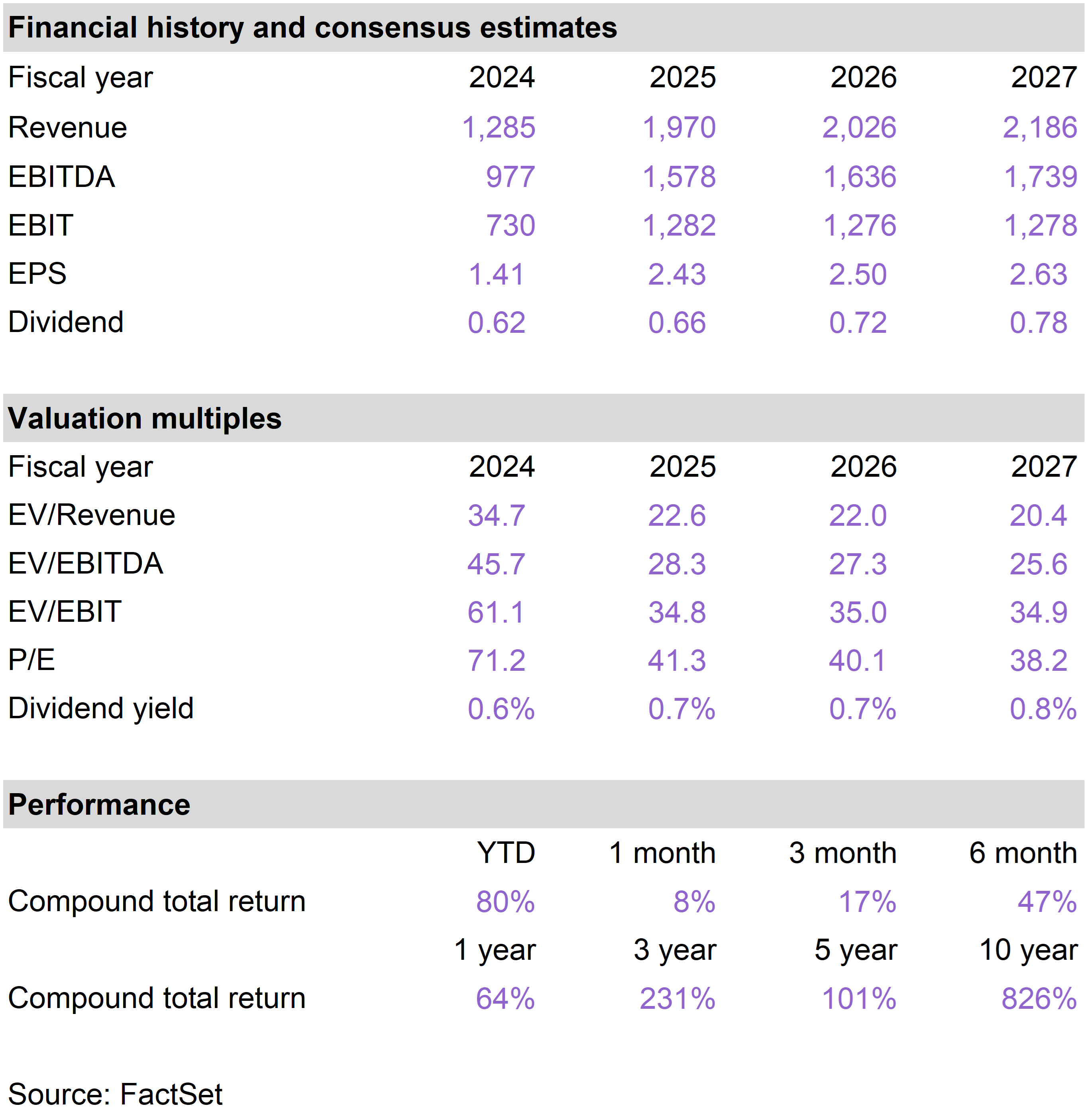

| | WESCO International (WCC) |

|

|

|

| | Wheaton Precious Metals (WPM) |

|

|

|

| | The 76research Inflation Protection Model Portfolio emphasizes business models that benefit from inflationary pressure. Holdings are typically selected from industries based on supply constrained real assets, including commodity and energy businesses, or companies that otherwise demonstrate superior pricing power. Drawing from an investable universe of expected inflation beneficiaries, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

| |

|