|

| Inflation Protection Model Portfolio |

|

| Monthly Portfolio Review: December 2025Publication date: January 5, 2026 |

|

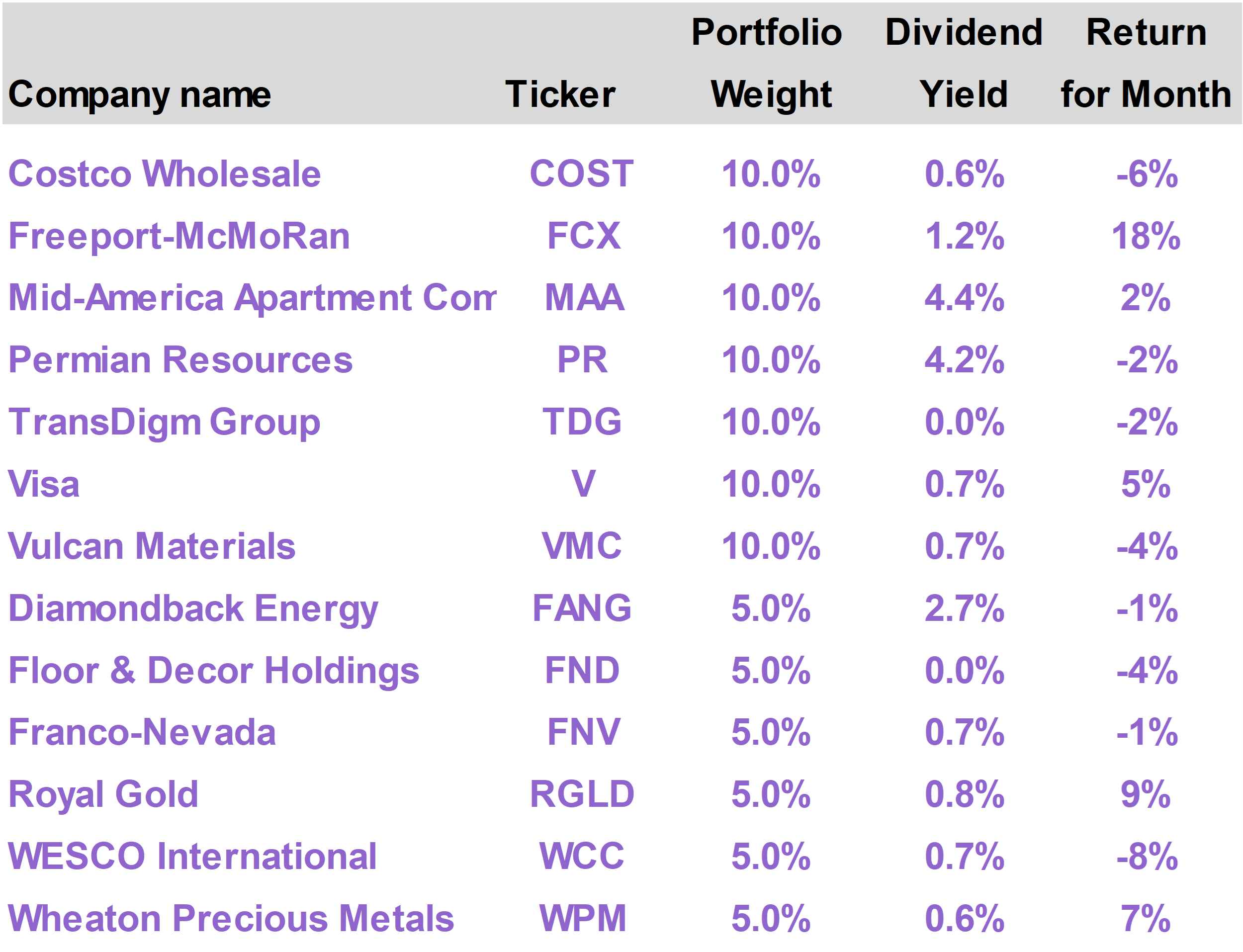

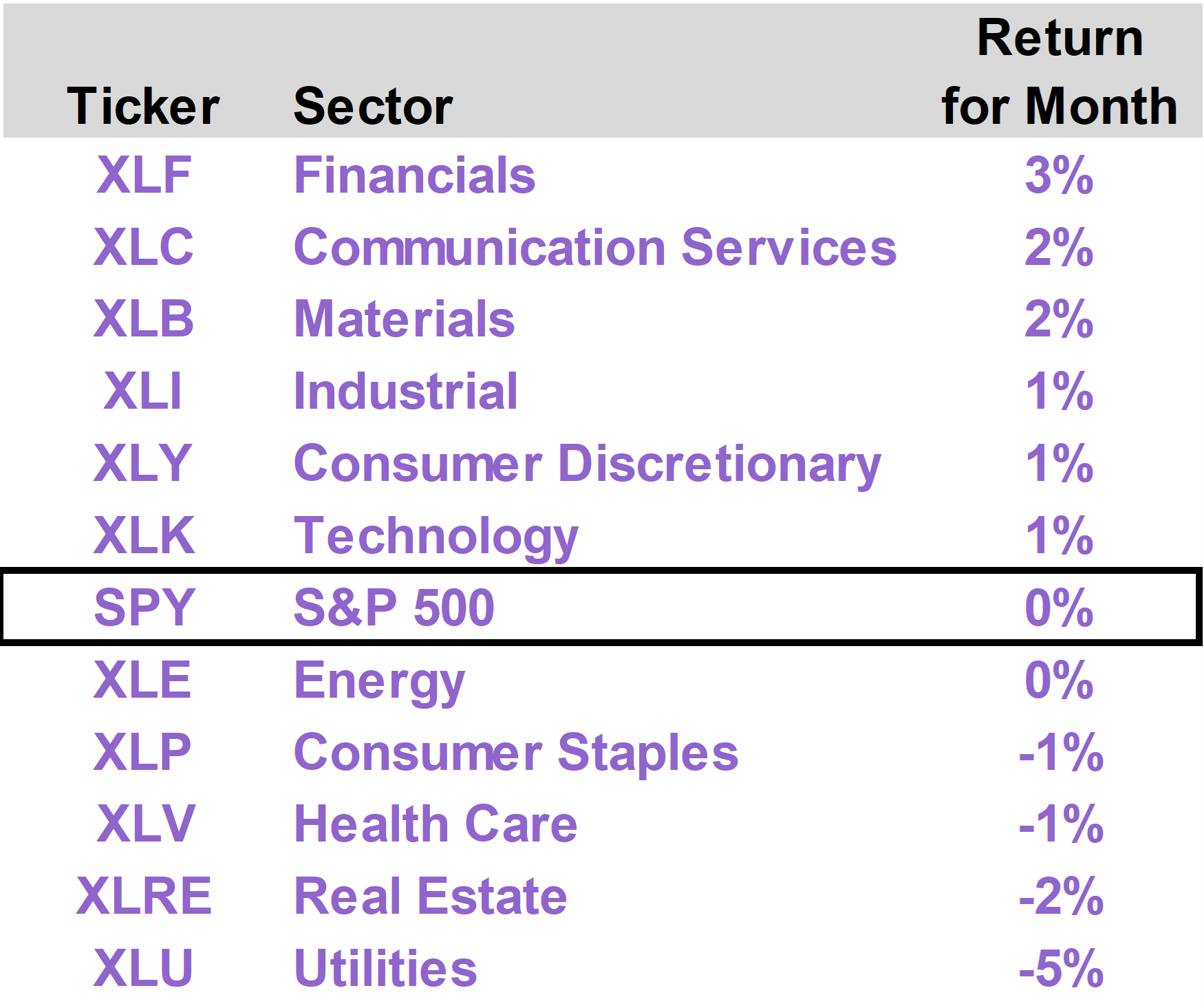

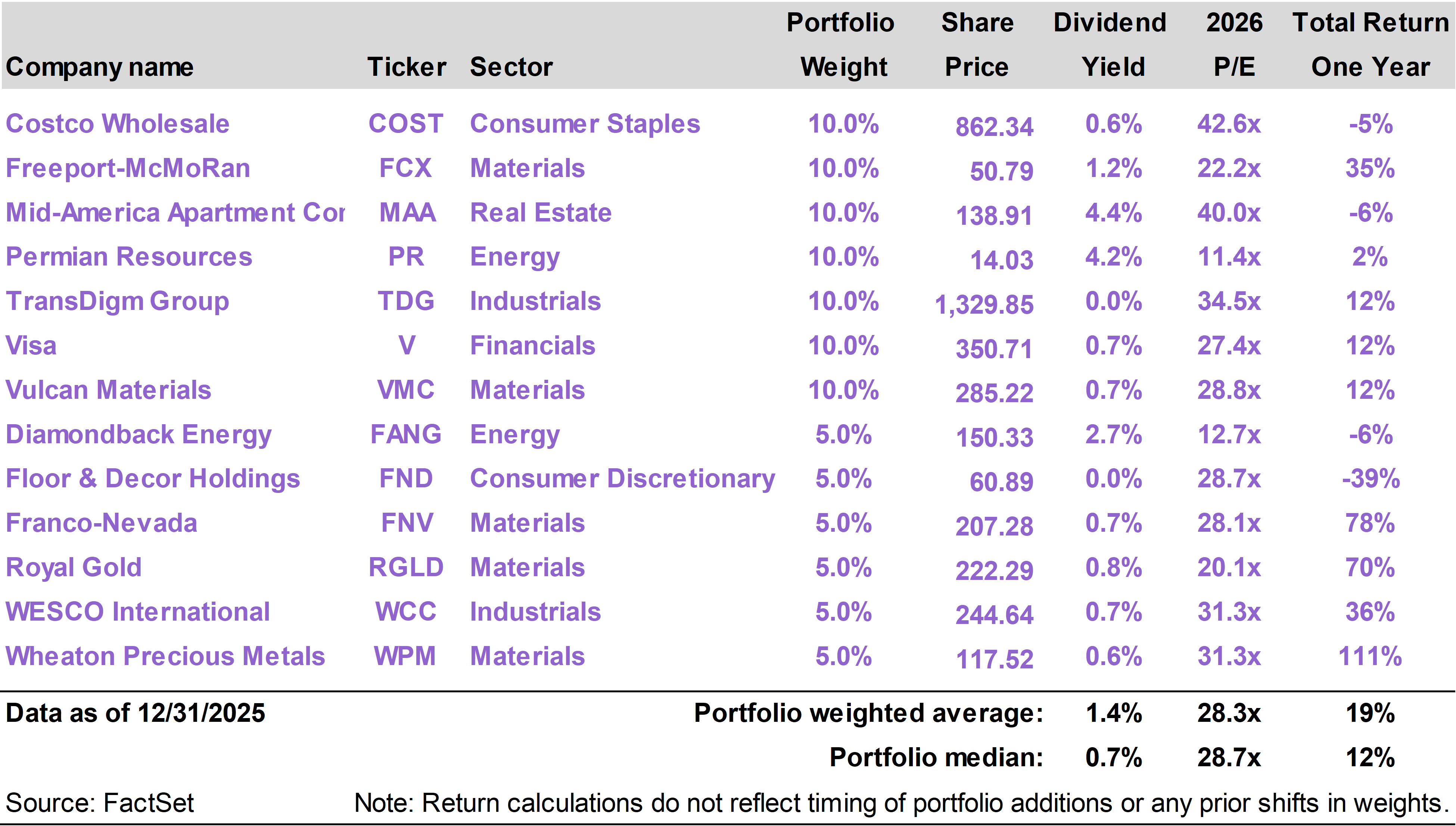

| | | Current portfolio holdings |

|

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

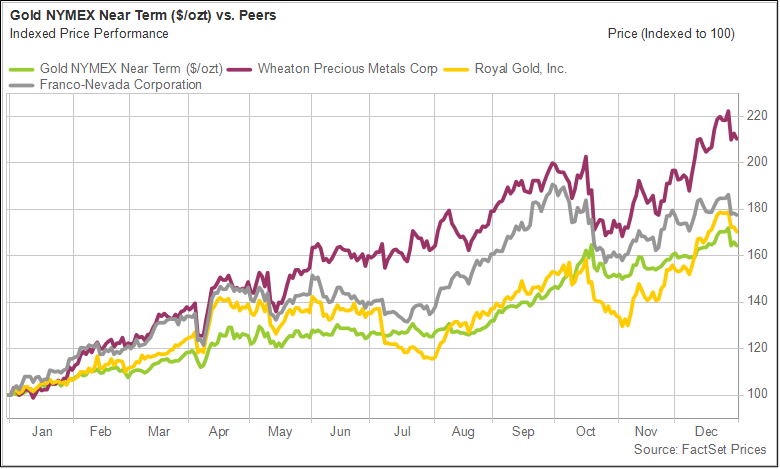

| | | December was generally an uneventful month for stocks. The S&P 500 was flat and the Nasdaq Composite was down slightly. The Inflation Protection portfolio advanced 1%, as shares of Freeport-McMoRan (FCX) advanced 18% on surging copper prices. Tech was soft in December but led the stock market in 2025, with a few mega-cap AI leaders having a disproportionate impact. Falling interest rates provided another important tailwind to stocks last year, especially in the fourth quarter. Gold rose 8% in December, capping off its best year since 1979 (up 65%). The portfolio’s gold streaming stocks generated returns last year ranging from 70% to 110%. Gold, copper and other scarce commodities have the potential to perform well, along with stocks, as monetary policy continues to ease in 2026. Trump is likely to appoint a successor to Fed Chair Jerome Powell within the next few weeks or months with a strong preference for easier monetary policy.

|

|

| | | The Inflation Protection portfolio returned 1.2% in December, versus a total return of 0.1% for the S&P 500 Index. On a one-year basis through the end of the month, the portfolio generated a total return of 14.8%, versus a 17.9% return for the S&P 500.

The portfolio’s top performing stocks this month were Freeport-McMoRan (FCX), which returned 18%; Royal Gold (RGLD), which returned 9%; and Wheaton Precious Metals (WPM), which returned 7%.

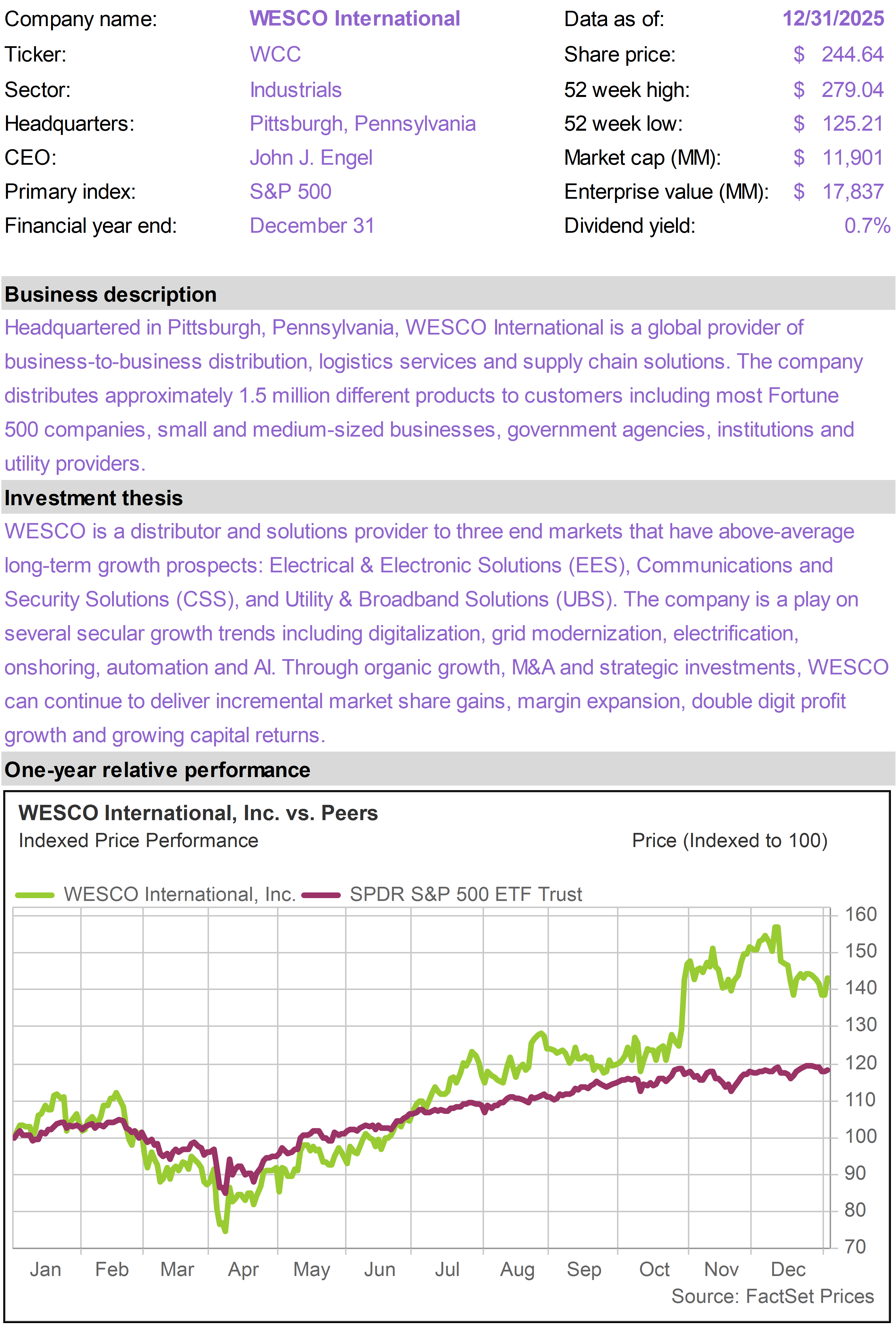

The portfolio’s worst performers were WESCO International (WCC), which returned -8%, and Costco (COST), which returned -6%. |

|

|

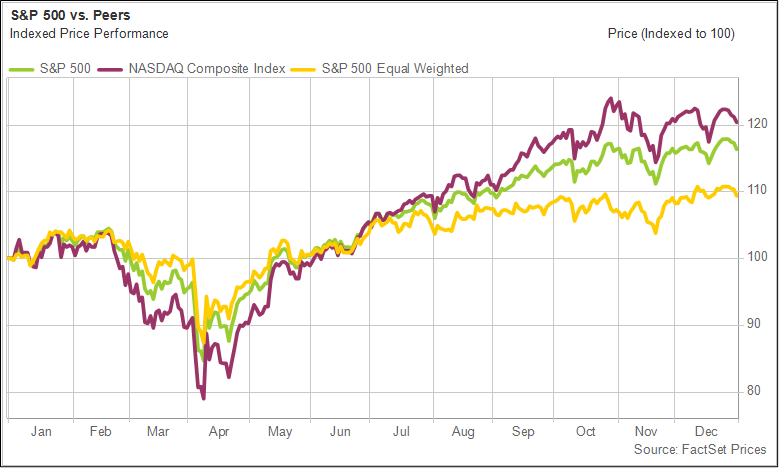

Calm end to a strong year

While December was basically a flat month for stocks, the bigger picture is that stocks generally delivered quite strong returns over the course of the year. The S&P 500 closed the year just about 1% below its all-time highest levels.

Technology stocks mildly underperformed in December but ultimately led the way in 2025. The indexes with the most tech exposure did the best.

The NASDAQ Composite returned 21% in 2025, versus 18% for the S&P 500 and 11% for the S&P 500 Equal Weighted Index (which captures the average stock in the index and has much lower exposure to mega-cap tech stocks).

|

|

|

|

S&P 500, NASDAQ, S&P 500 Equal WeightTotal Return (12/31/24 - 12/31/25) |

|

|

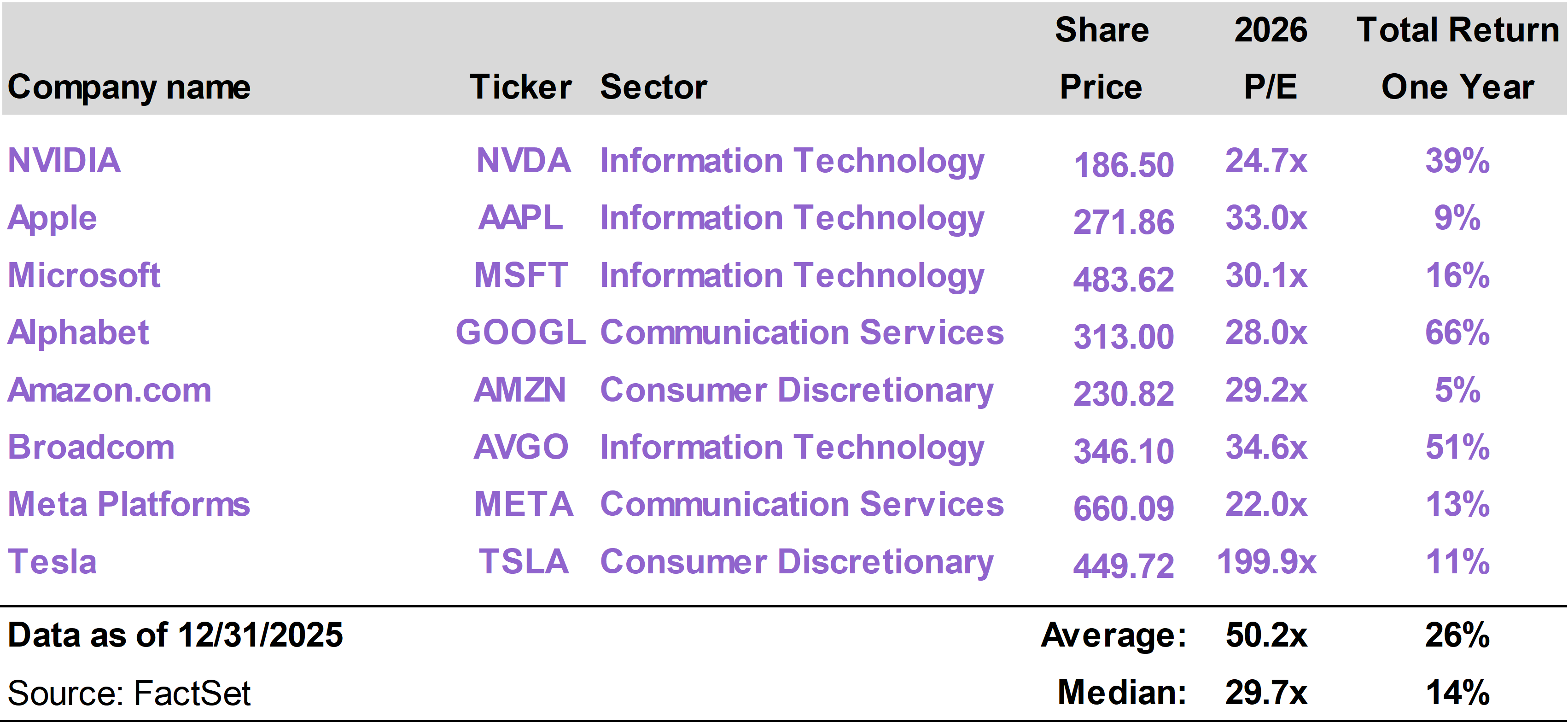

Mag 7 continue to lead

Given their extreme importance to the market now, we have begun tracking the Magnificent Seven mega-caps, including Broadcom (AVGO), directly via our regularly recurring Mag 7 Monitor.

These stocks played a critical role in driving the upside in the broader market last year, delivering an average total return of approximately 26%, which exceeded the Nasdaq. |

|

|

|

Mag 7 - Total Return(12/31/24 - 12/31/25) |

|

|

The success of the Mag 7 in 2025 was clearly AI-driven. Interestingly, only three of the stocks—AVGO, Alphabet (GOOGL), and NVIDIA (NVDA)—actually outperformed the S&P 500. But the performance of these three stocks was extremely strong and made up for the relatively subdued performance of the rest of them.

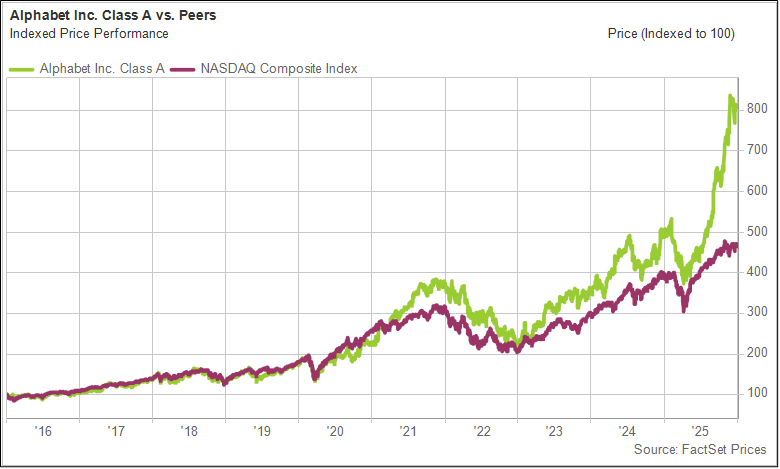

GOOGL’s success this year (up 66%) was particularly notable, after about a decade of basically in-line performance with the Nasdaq.

GOOGL shares broke out in the final months of 2025 as investors recognized the success of its Gemini AI offering as a top AI model. The market also now has greater confidence in GOOGL’s ability to use AI to reinvent its leading internet search business without cannibalizing it. |

|

|

|

GOOGL vs. Nasdaq- Total Return(Last 10 Years) |

|

|

NVDA and AVGO succeeded in 2025 as the two leading hardware players in AI.

Despite some volatility along the way, especially in April with the tariff panic, NVDA shares delivered another impressive result on the back of continued earnings growth and a healthy outlook.

In 2025, AVGO asserted itself as a critically important AI hardware player through Application-Specific Integrated Circuits (ASICS). The company designs and manufactures these custom AI chips, often in close partnership with its customers, including GOOGL.

While there is concern among tech investors that AVGO’s ASICS represent a competitive threat to NVDA’s Graphics Processing Units (GPUs), both companies thrived in 2025 on broad demand for the key equipment that makes AI possible.

Heading into the new year, AI remains the growth engine of the stock market. Companies across the economy are benefiting from the AI build-out and increasingly from AI adoption, which allows for faster growth and lower costs.

Real progress on inflation

AI growth may be driving the economy and stock market forward, but inflation is the main factor holding them back. Inflation remains somewhat elevated, keeping the Federal Reserve in a still “restrictive” policy stance.

The good news is that inflation appears to be easing—a main reason stocks touched all-time highs in the final quarter of the year. That easing trend showed up across several measures as the year progressed.

Goods inflation continued to cool as supply chains normalized, while housing-related inflation—one of the stickier components—began to decelerate with a lag.

Wage growth also moderated without a sharp rise in unemployment, reinforcing confidence that inflation could come down without a recession.

Against the backdrop of moderating inflation, at its most recent meeting in December, the Fed dropped short-term rates by another quarter-point. This was the third rate cut since Jerome Powell’s late-August 2025 pivot in Jackson Hole.

An improving inflation outlook led to a substantial decline in One-year Treasury yields over the course of the year, especially in the final months. |

|

|

|

One-Year Treasury Yields(Last 12 months) |

|

|

Rates influence sector performance

The Financial sector led performance in December. This can be explained to a large degree by shifts in the yield curve.

With the December interest rate cut, short-term interest rates fell notably. The One-year Treasury yield fell from 3.59% at the end of November to 3.47% at the end of December.

Meanwhile, partly as a result of an improved growth outlook, long-term Treasury yields rose. The Ten-year Treasury yield increased from 4.01% at the end of November to 4.17% at the end of December.

These shifts in the yield curve—in this case, a “steepening,” with short rates coming down and long rates going up—were not extreme but can be impactful in an otherwise relatively quiet market.

Financial stocks, especially banks, benefit from a steeper yield curve. Banks have to pay depositors less in an environment of lower short-term interest rates. If long-term rates simultaneously rise, they can earn more by placing those funds into higher yielding long-term instruments. |

|

|

| |

Given the rise in long-term yields in December, it is unsurprising that Utilities were the worst performing sector, followed by other defensive sectors that are also sensitive to movements in long-term rates (Real Estate, Health Care, Consumer Staples).

Utilities are stocks but trade with a high-correlation to long-term bonds because their value is similarly based on stable long-term cash flows. The weakness in Utilities in December reflects the mild increase in long-term rates.

Could inflation undershoot?

After several years of high inflation, an increasingly important question for markets is whether inflation could fall faster and further than expected. Several factors seem to be pointing in that direction.

First, goods inflation has already cooled meaningfully as one-time tariff impacts (which were probably milder than many people expected anyway) have already become embedded in price levels.

Second, housing inflation, which moves with long lags, is beginning to roll over as lower new-lease growth rates slowly feed into official data. The shelter component represents as much as one-third of the Consumer Price Index (CPI).

Third, moderately rising unemployment alleviates wage pressures. Businesses are no longer scrambling to fill open positions as they were just a few years ago, when aggressive post-pandemic hiring led to notable labor shortages in certain areas.

When inflation peaked in 2022, the unemployment rate was as low as 3.5%, versus 4.6% today. To avoid inflation, the economy requires some labor market slack.

All of these positive cyclical trends are playing out just as AI-driven productivity growth, a more structural factor, is only now starting to take hold.

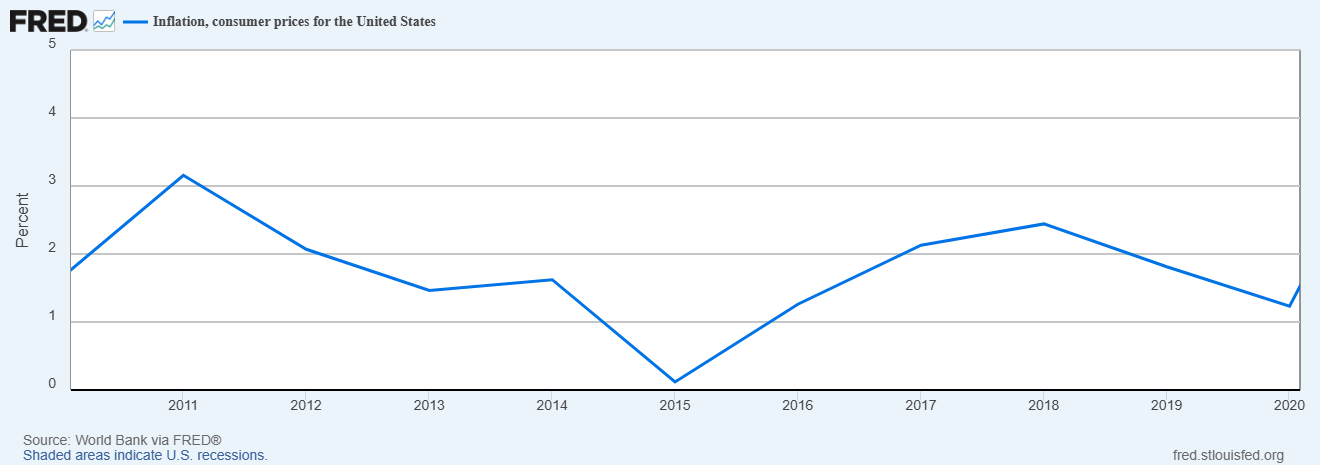

Inflation in recent months has been running just below 3%, meaningfully above the Fed’s 2% target. This is basically the only reason that Fed has not been more aggressively cutting short-term rates, which are still elevated, as unemployment rates creep up.

But it is worth remembering that for the ten-year period that preceded the pandemic, inflation rates were consistently below the Fed’s semi-official 2% target. |

|

|

|

Increase in Consumer Price Index (CPI)(2010-2020) |

|

| The pandemic created an inflationary shock to the system that took many years to work through—a combination of supply chain disruptions and excessive monetary and fiscal stimulus.

Now, we potentially find ourselves returning to conditions that prevailed before the pandemic hit—a nimble, productive, high-tech economy that bypasses inflationary pressures.

As we look forward to 2026, we are mindful of the possibility of positive surprises on the inflation front. This would give the Fed, especially under the leadership of whoever President Trump decides to appoint as the next Chair, significant leeway to cut rates.

A return to the “old normal” of persistently low inflation is not currently priced into markets with long-term inflation expectations still north of 2%. This optimistic scenario represents a potentially significant source of upside for stocks, and risk assets in general, in the year ahead. |

|

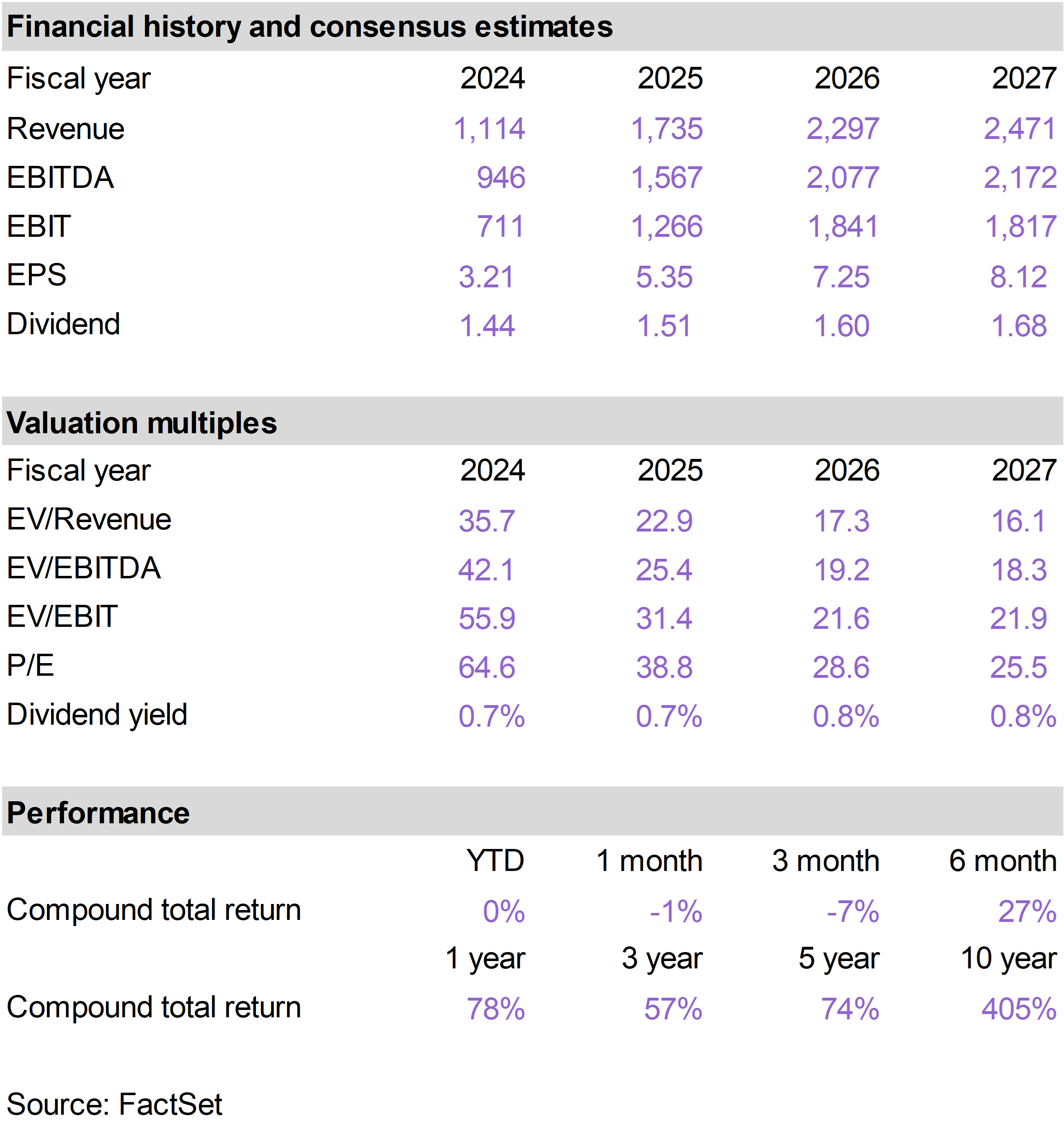

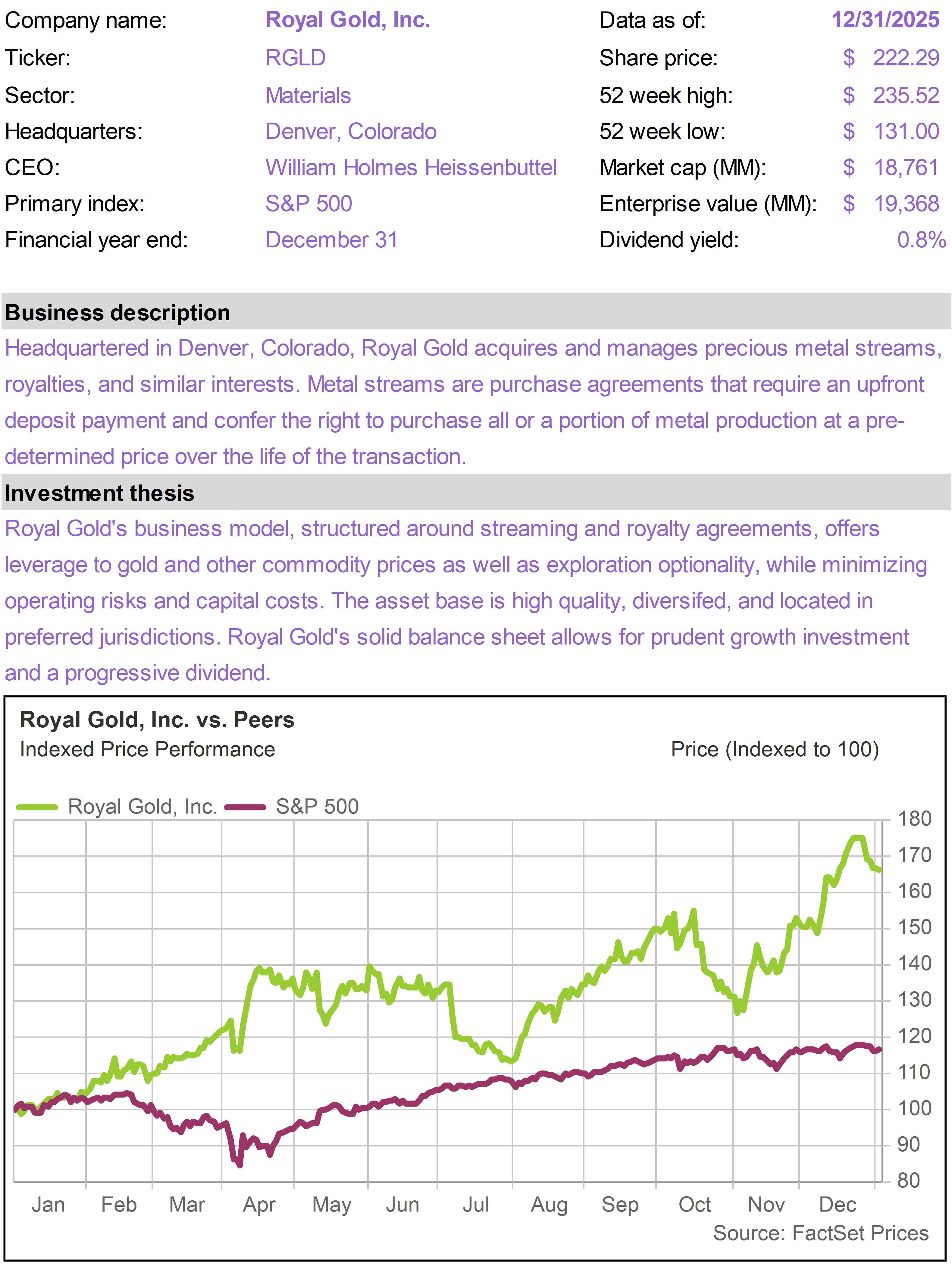

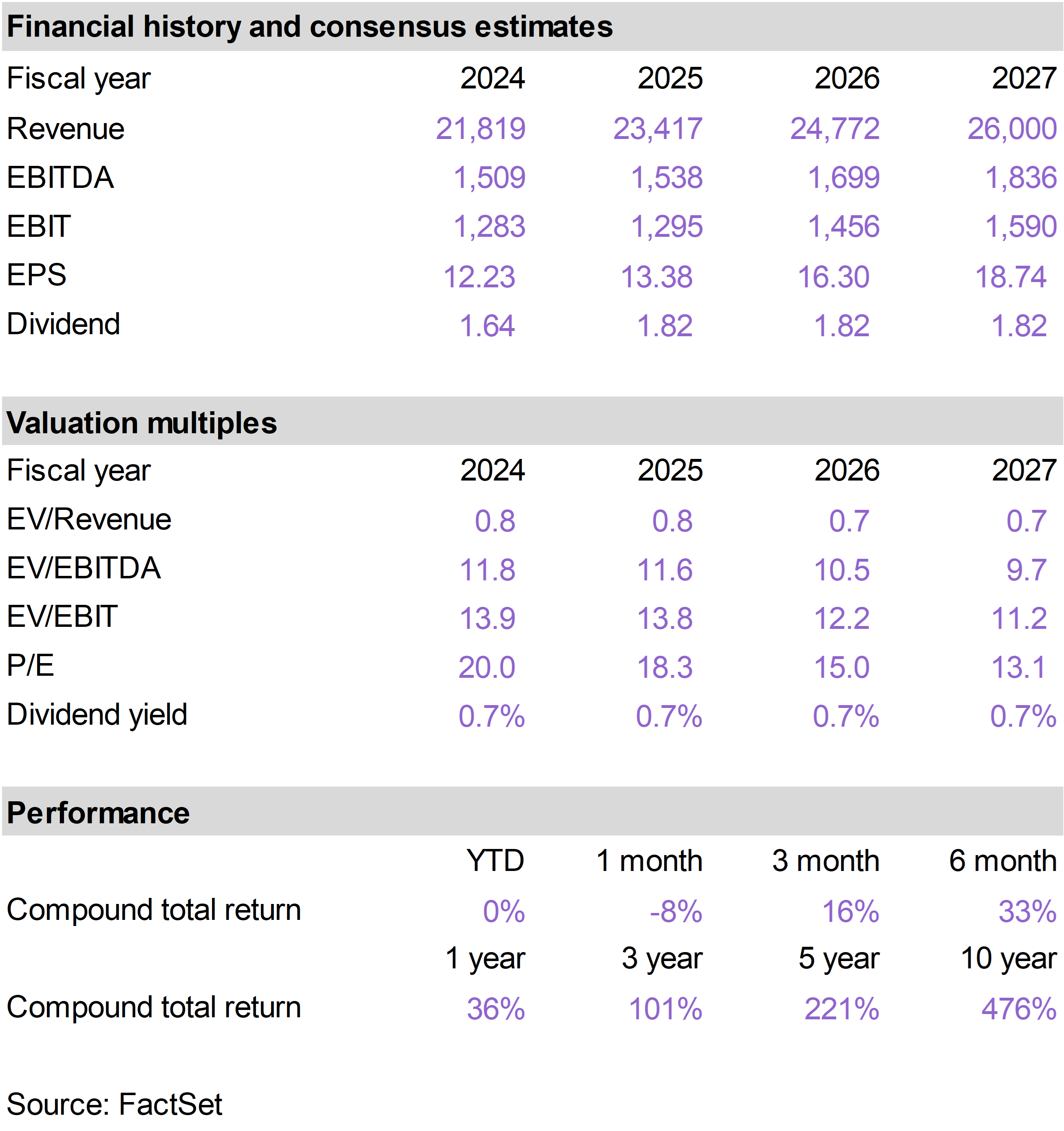

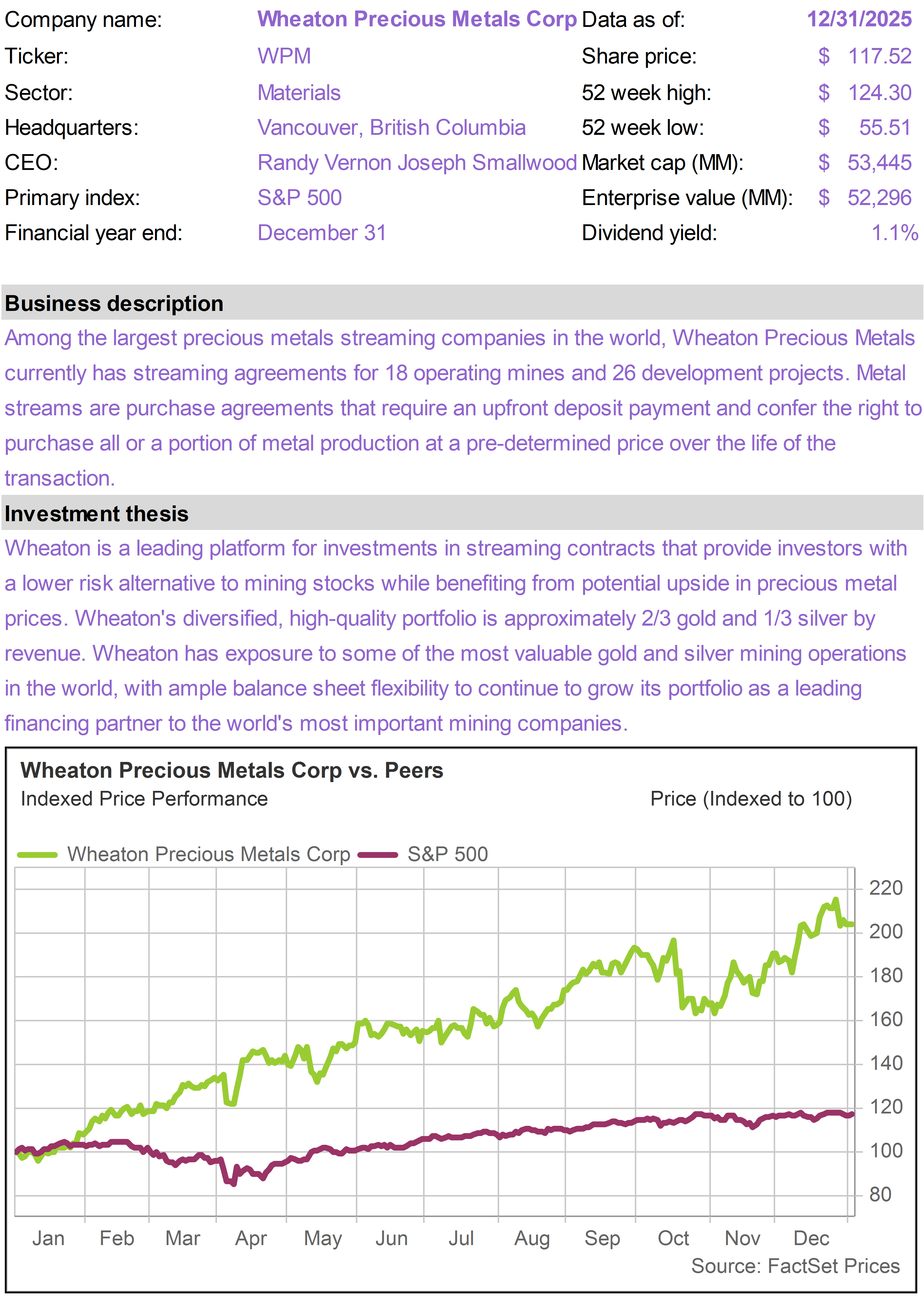

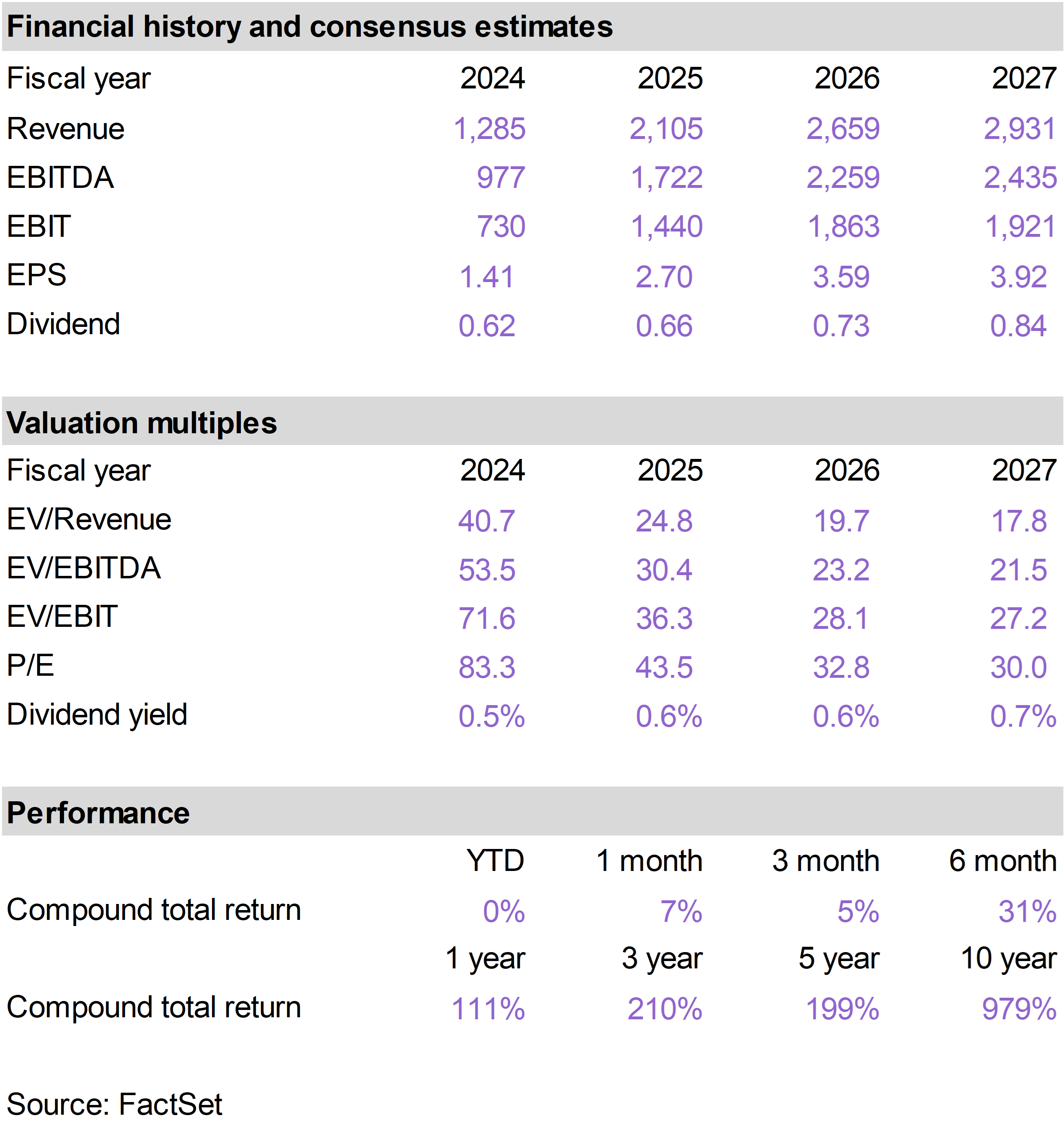

| | | The top performing stocks in the Inflation Protection portfolio this month were Freeport-McMoRan (FCX), which returned 18%; Royal Gold (RGLD), which returned 9%; and Wheaton Precious Metals (WPM), which returned 7%.

Notable detractors in the portfolio this month were WESCO International (WCC), which returned -8%, and Costco (COST), which returned -6%. |

|

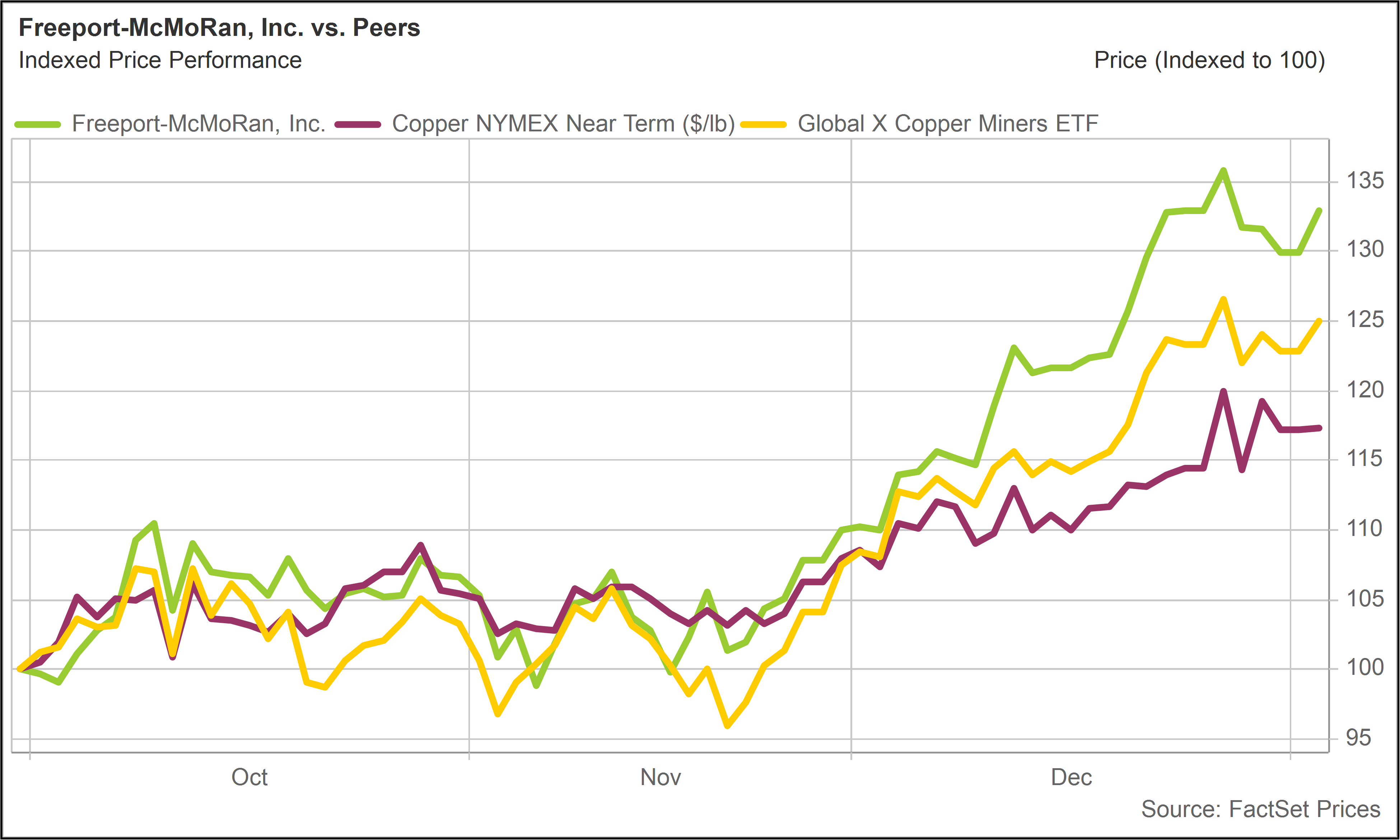

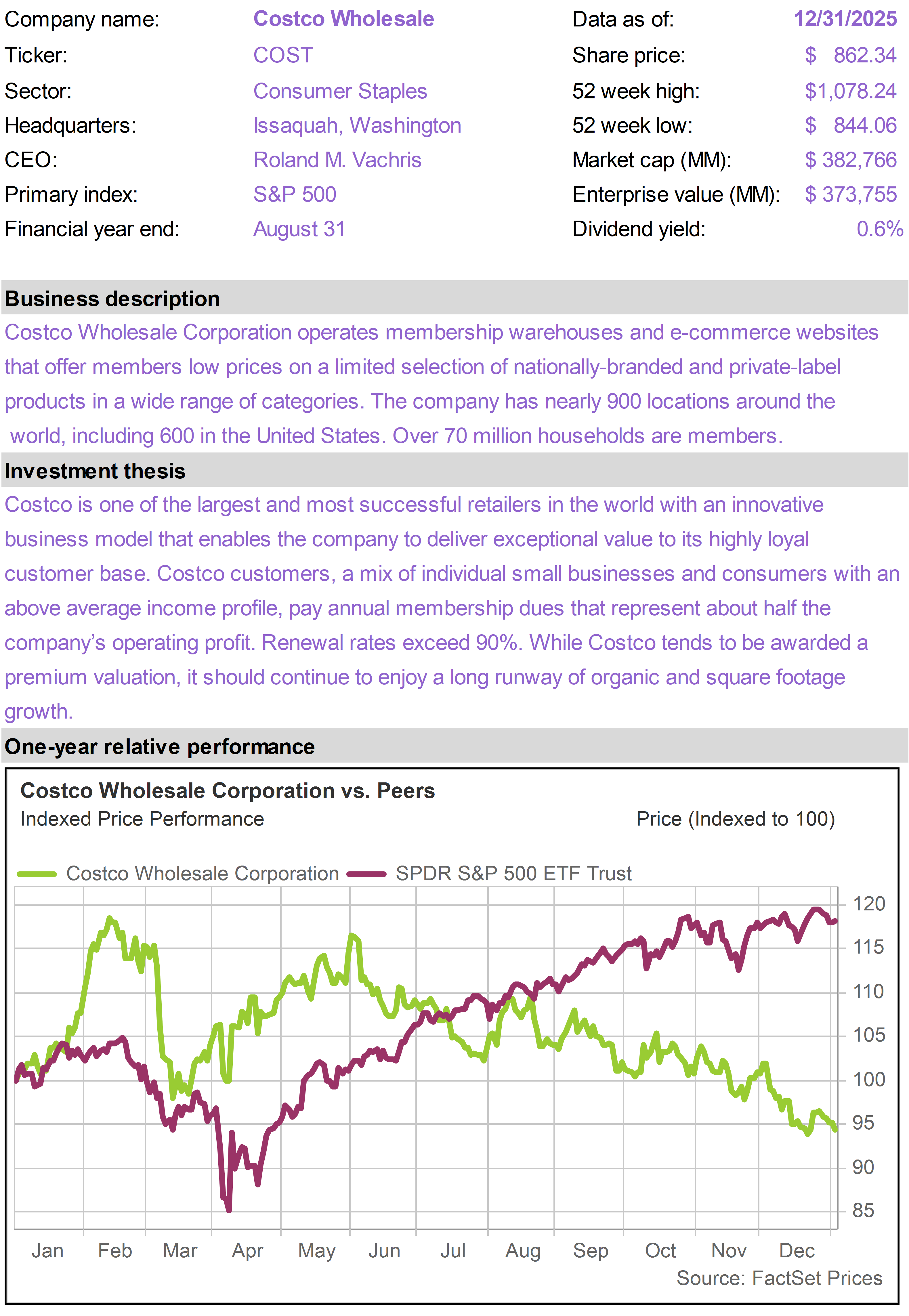

| Shares of FCX advanced sharply in December as copper prices surged to all-time highs—a trend that has continued into the new year.

As previously discussed, we have a long-term bullish view of copper because of the indispensable role it plays within the electrification theme. Put simply, the world is becoming more wired, a trend that will only accelerate with AI. Copper is a necessary input for electrical wiring, with no practical alternatives.

At the same time, copper supplies are highly constrained by geology (copper is abundant but only in certain locations) and the enormous lead times associated with copper mine development (ten years plus).

FCX suffered a setback in September 2025 after an accident that impacted output from its key mining operation in Indonesia. FCX shares declined, justifiably, but as we noted at the time, we felt the market was overreacting.

Over the past three months, as copper prices have advanced, FCX shares have outperformed both copper itself and the broader copper mining group. |

|

|

|

FCX vs. Copper, Copper ETF(Last 3 Months) |

|

| |

|

Gold vs. WPM, FNV, RGLD(Total Return - 2025) |

|

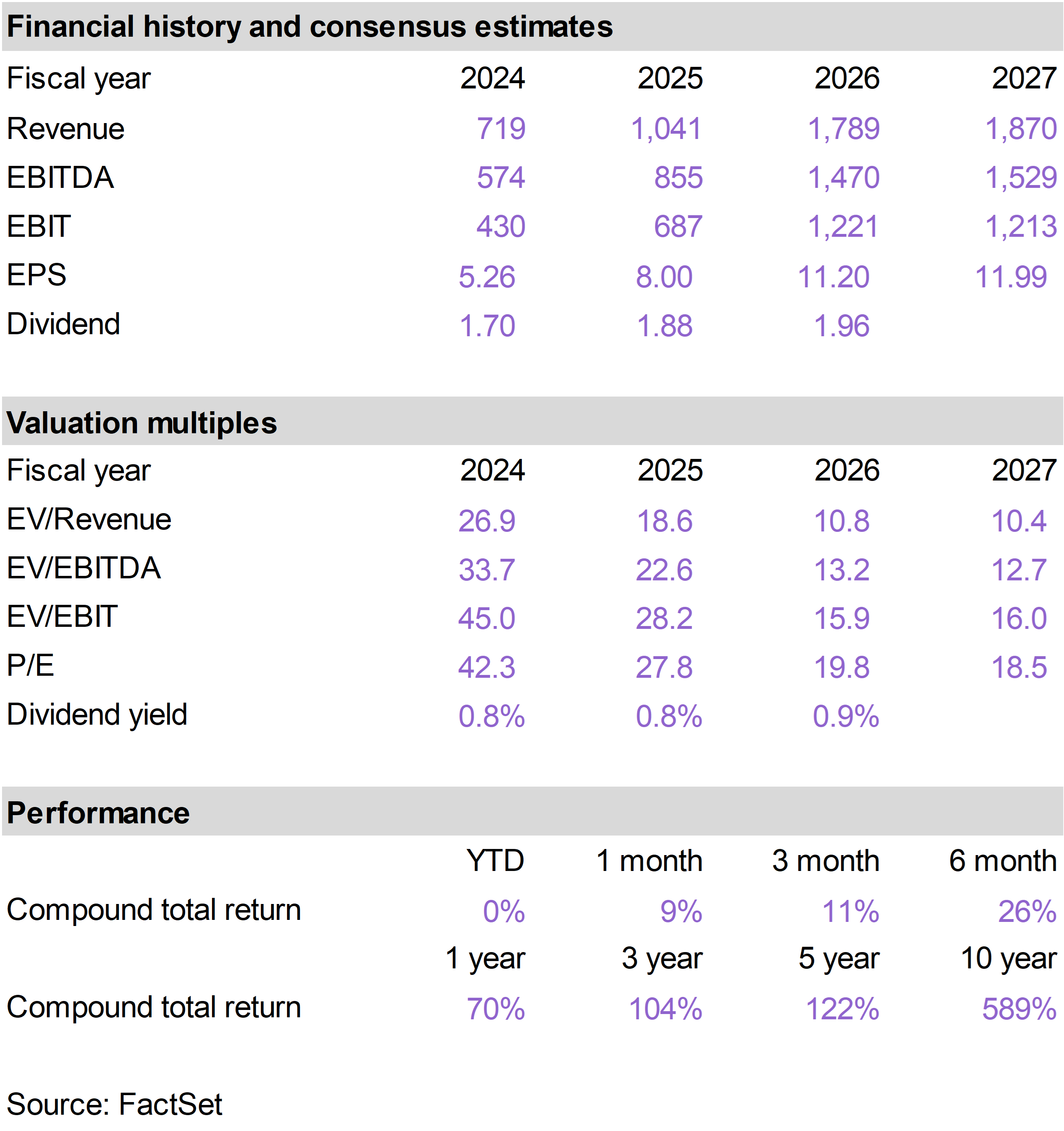

| WCC is a leading distributor of industrial supplies with high exposure to data centers and electrical power infrastructure. Shares retreated somewhat in December after strong performance in October and November.

Despite the December setback, WCC generated a total return of 36% in 2025. We continue to view WCC as well-positioned to benefit from long-term structural forces within the economy.

COST shares retreated along with other consumer staples names in December and in reaction to some concerns about intensified competition. |

|

| | |

| | |

| | |

| | | |

|

| | |

|

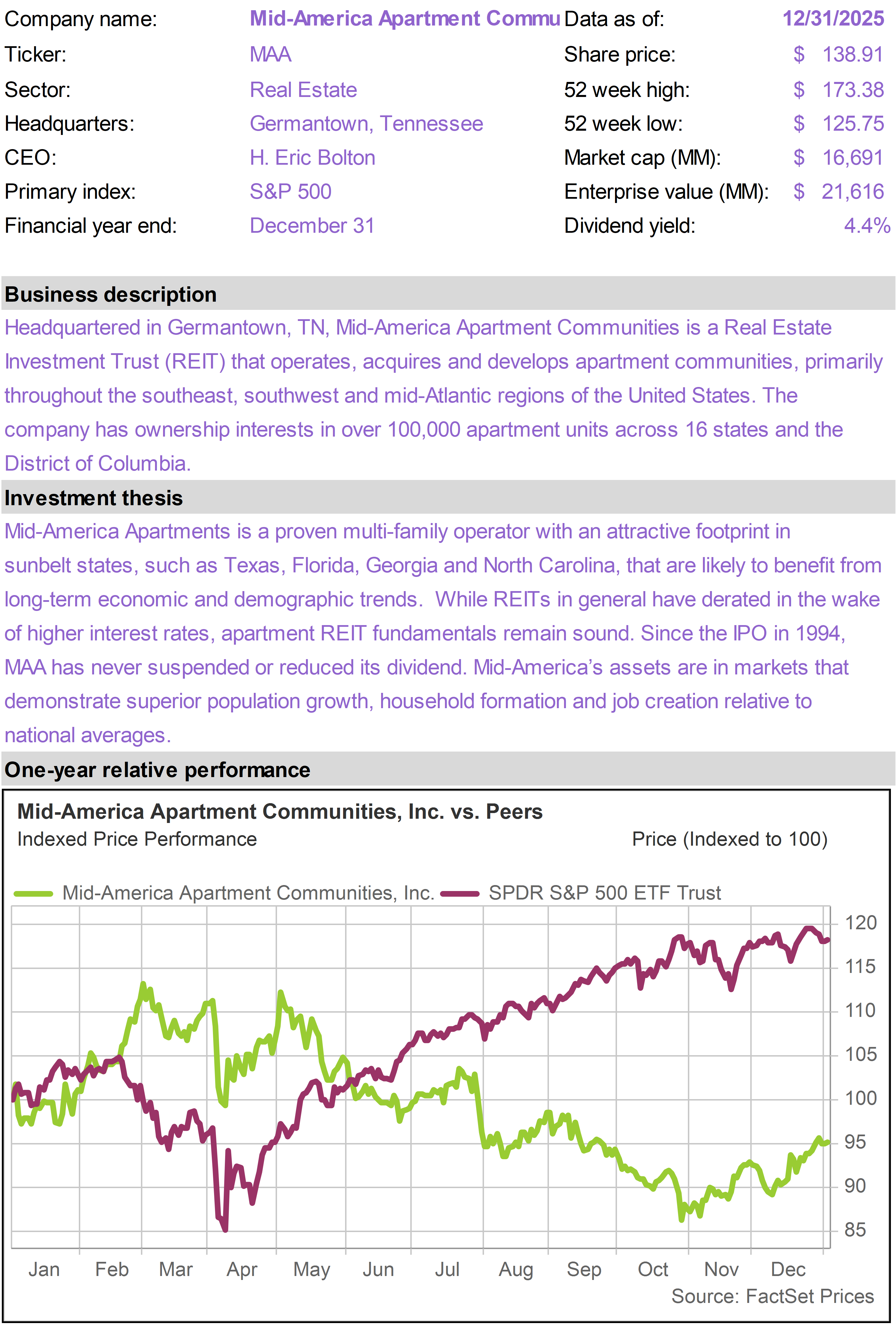

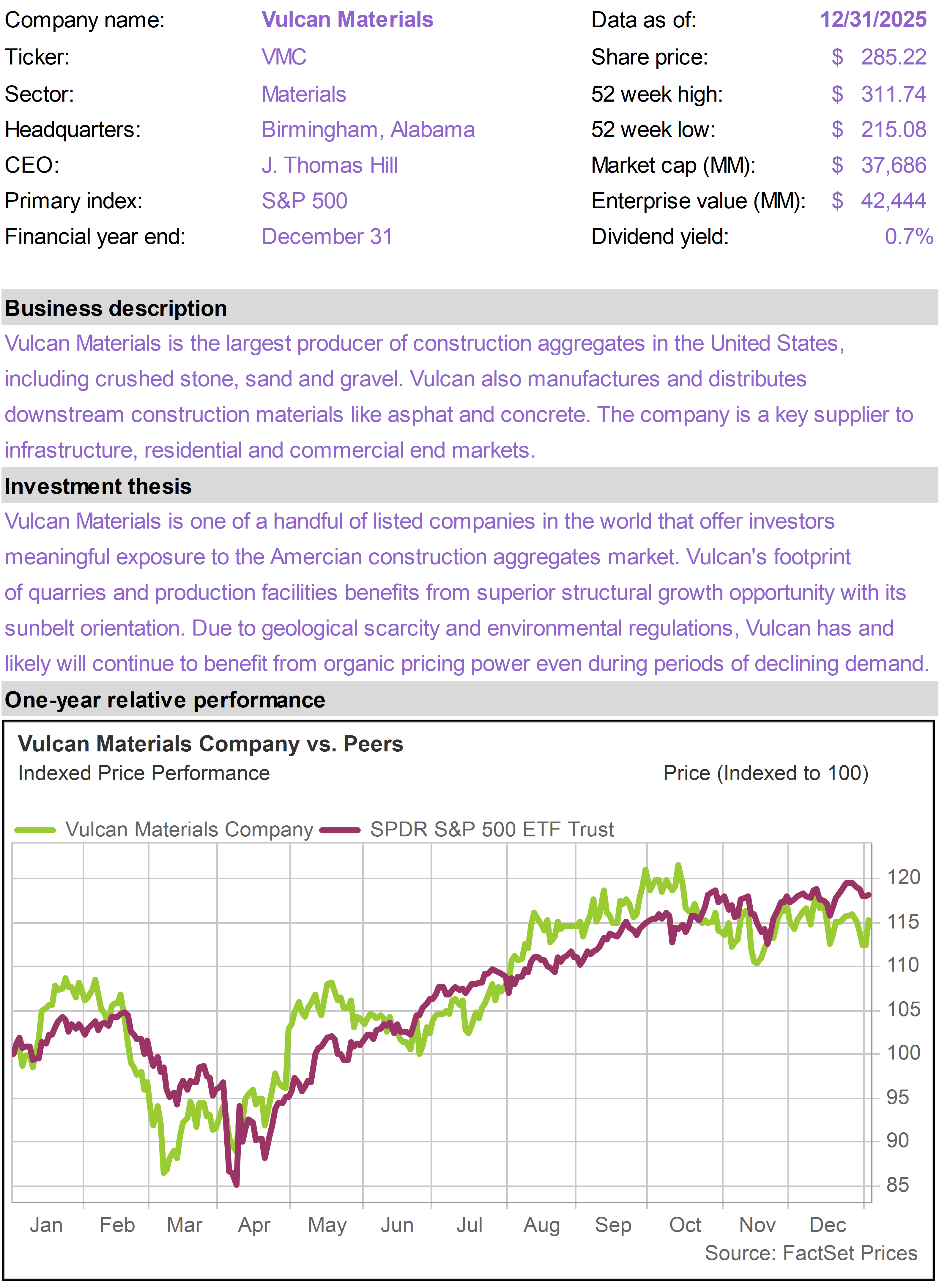

| | Mid-America Apartment (MAA) |

|

|

|

| |

|

| | |

|

| | |

|

| | |

|

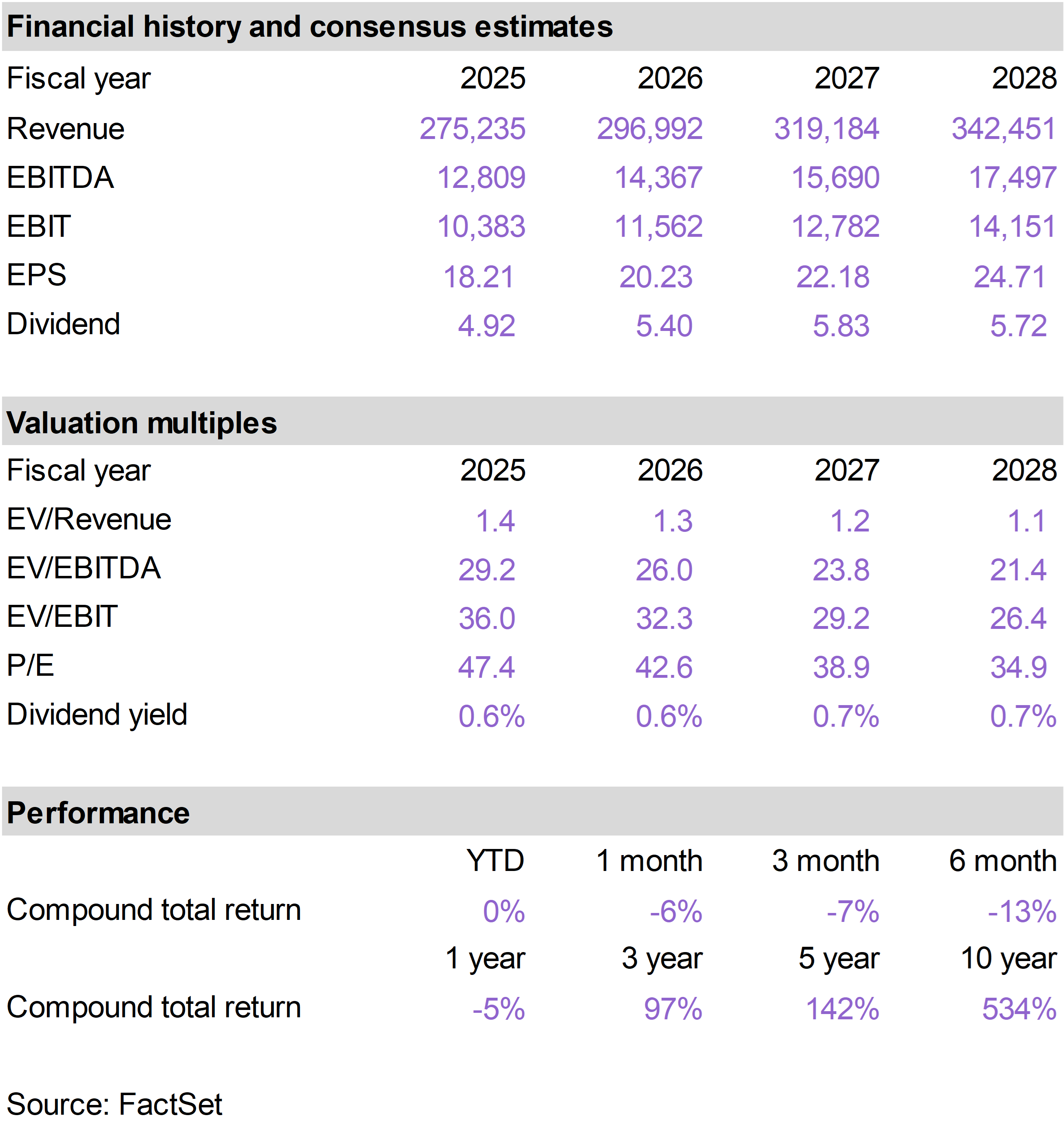

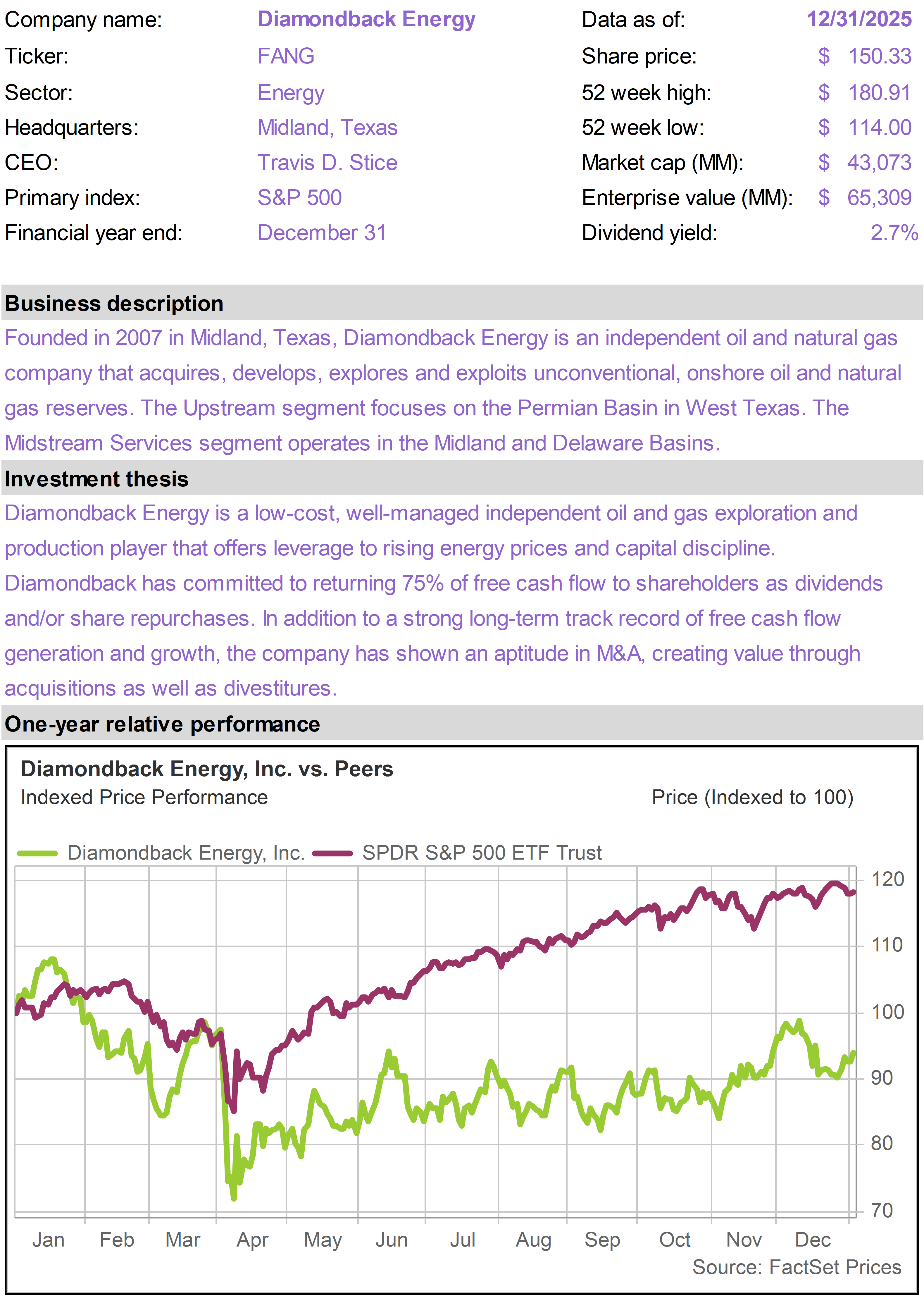

| | Diamondback Energy (FANG) |

|

|

|

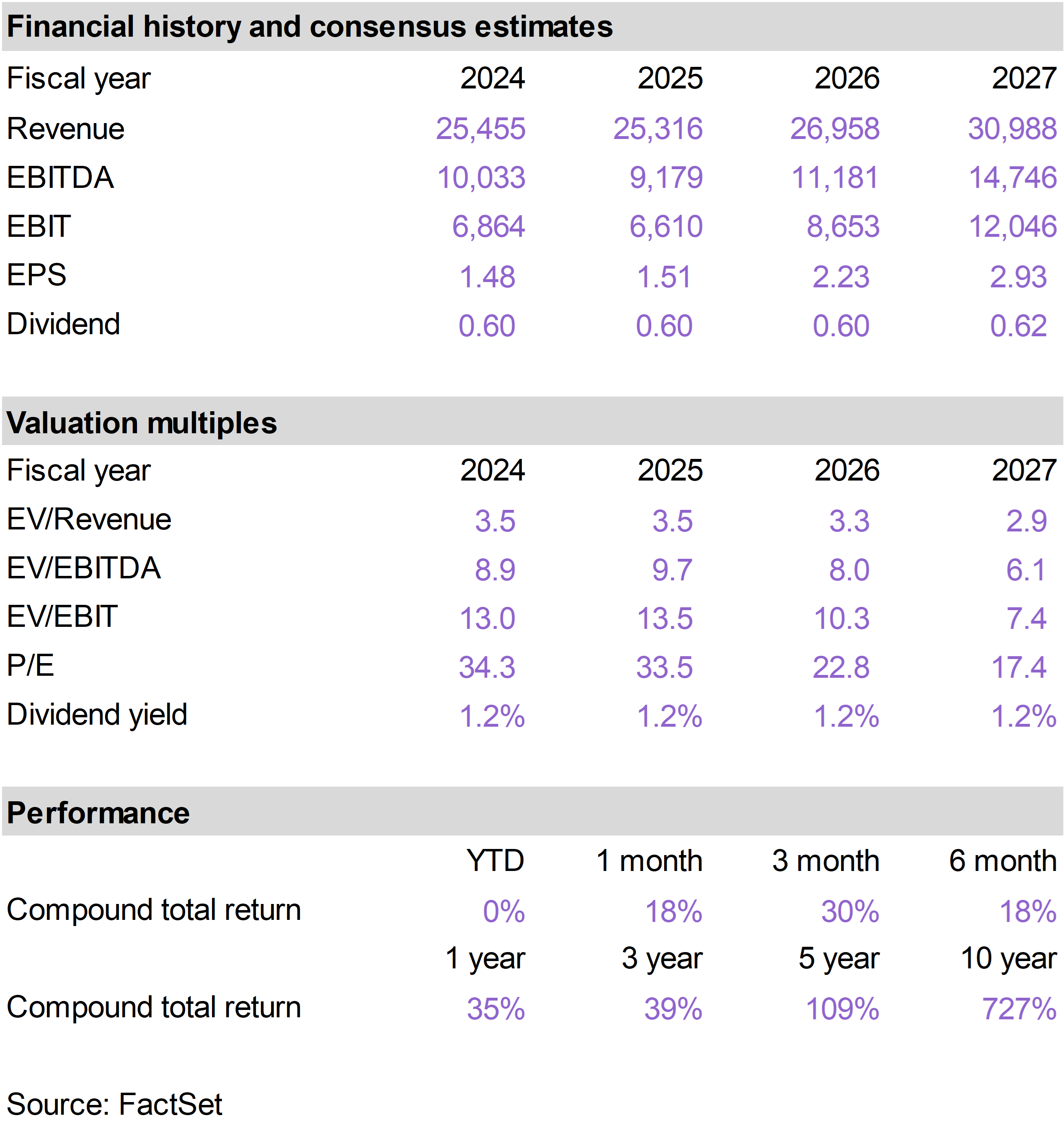

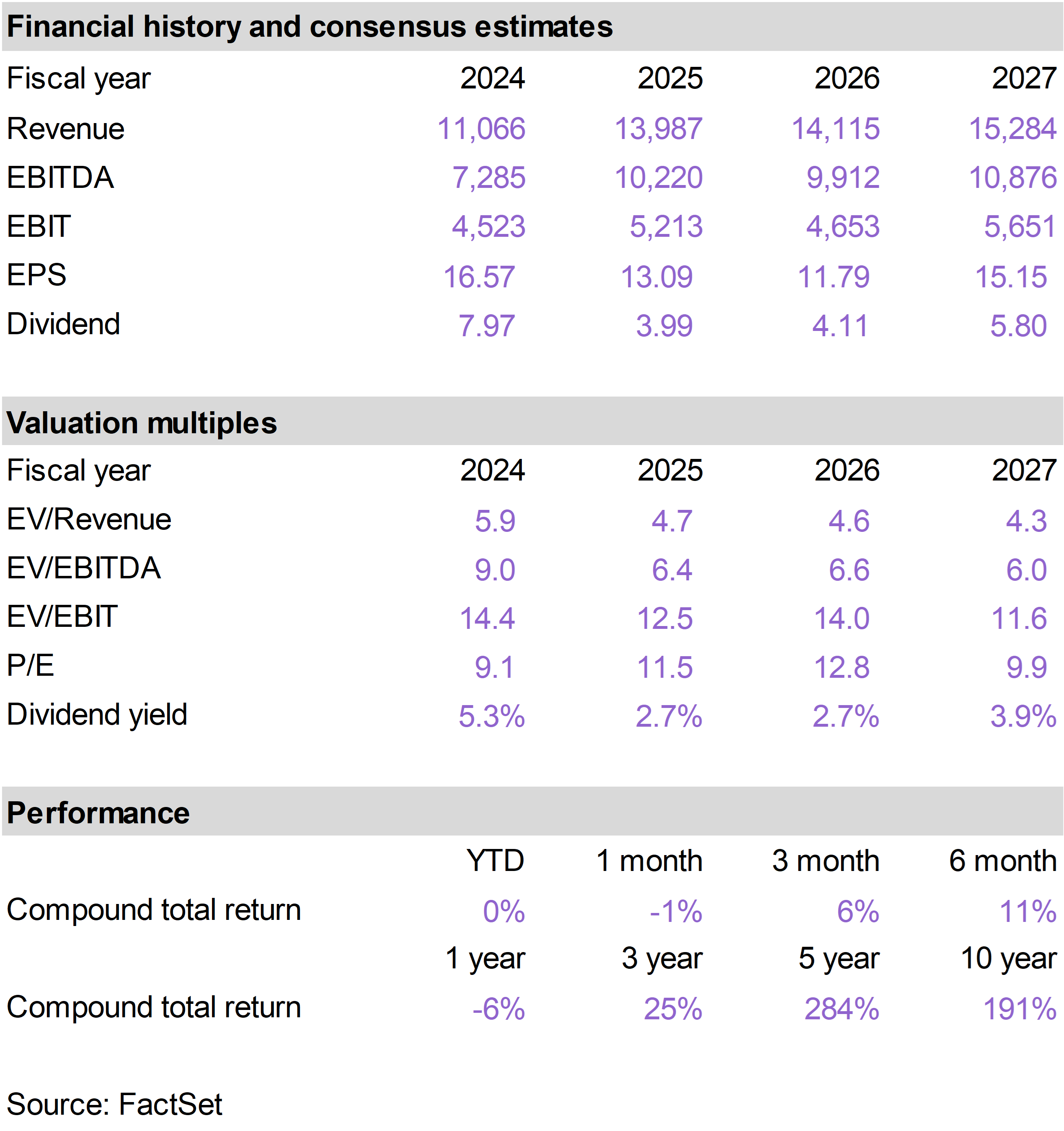

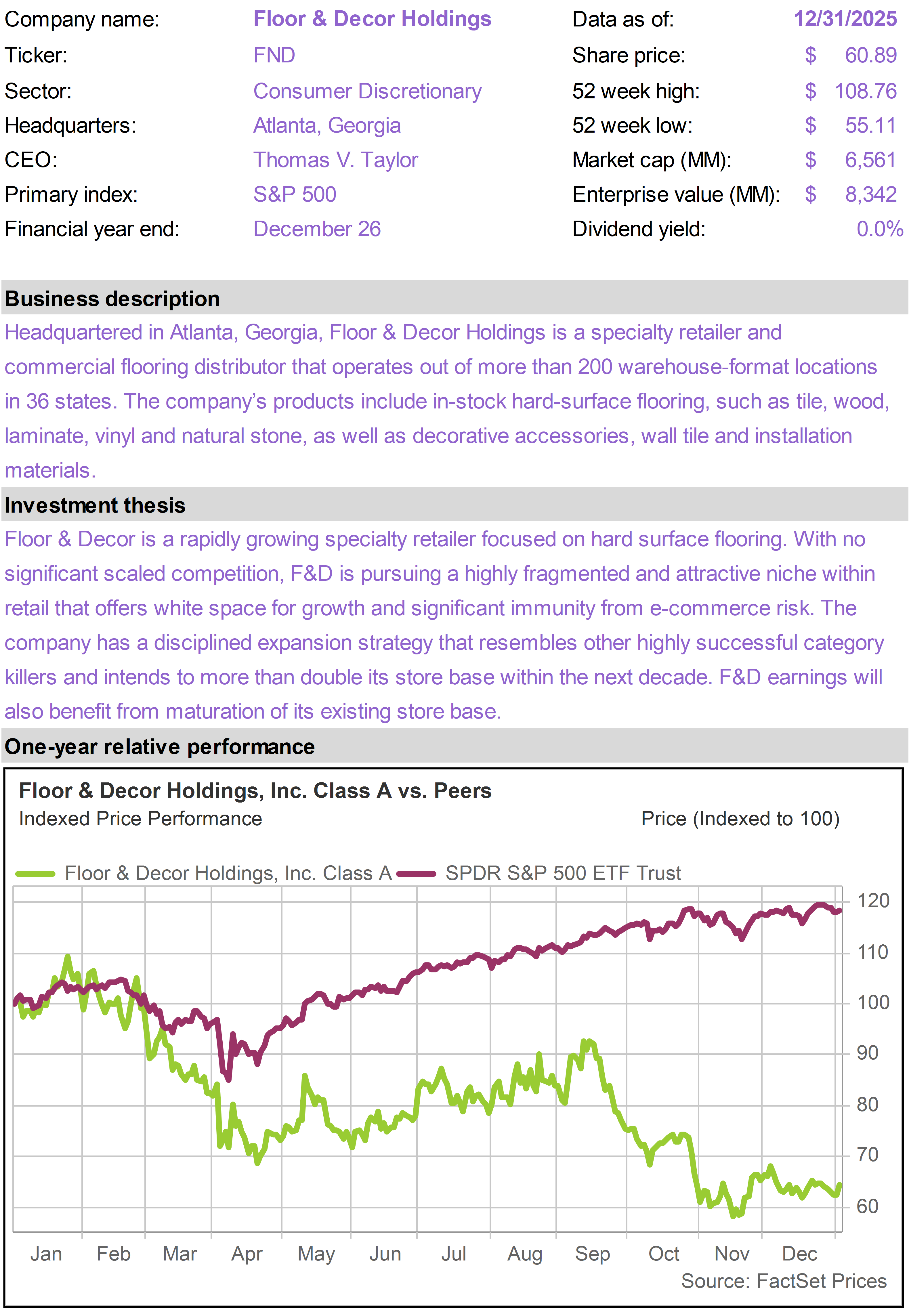

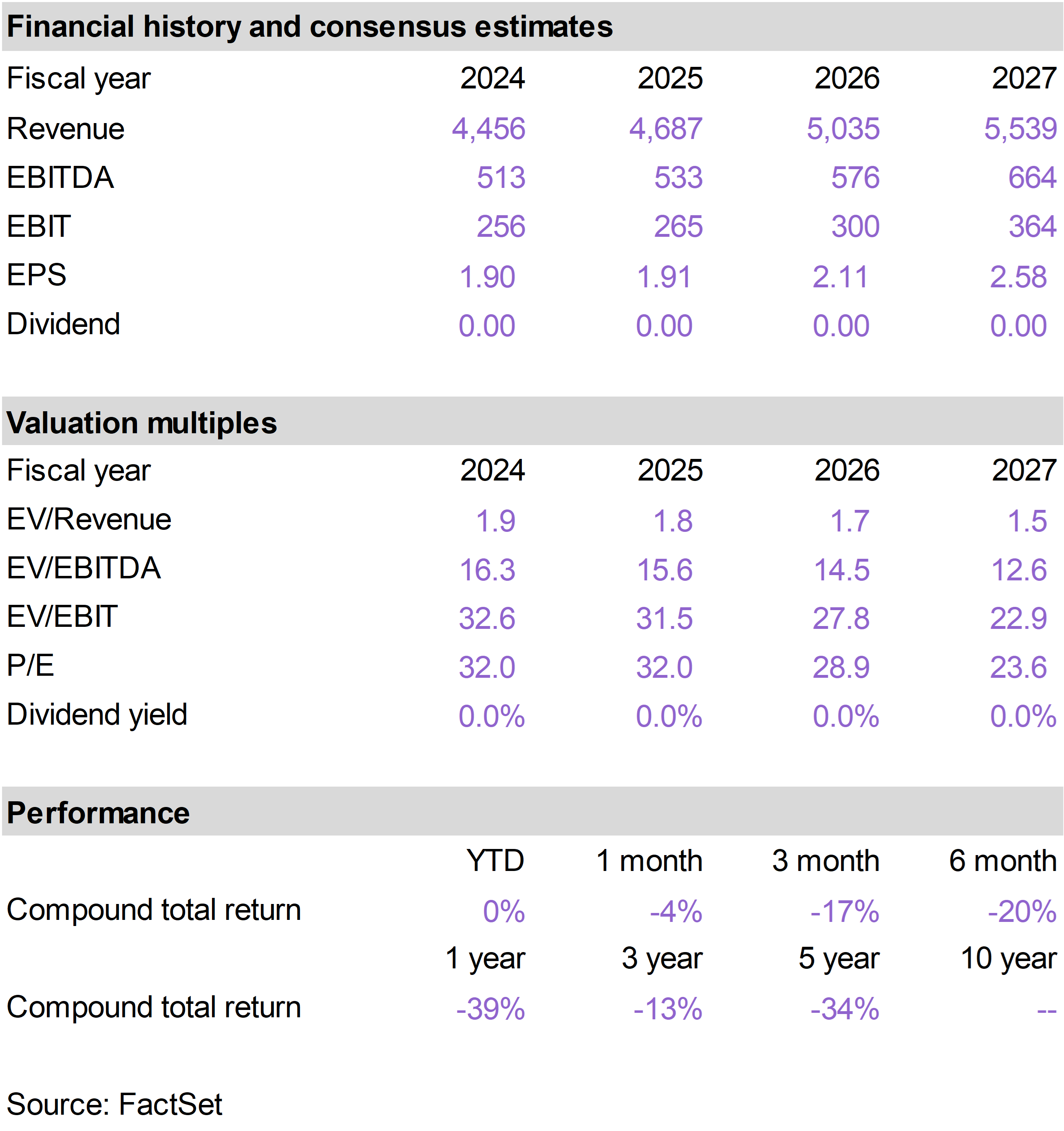

| | Floor & Decor Holdings (FND) |

|

|

|

| | |

|

| | |

|

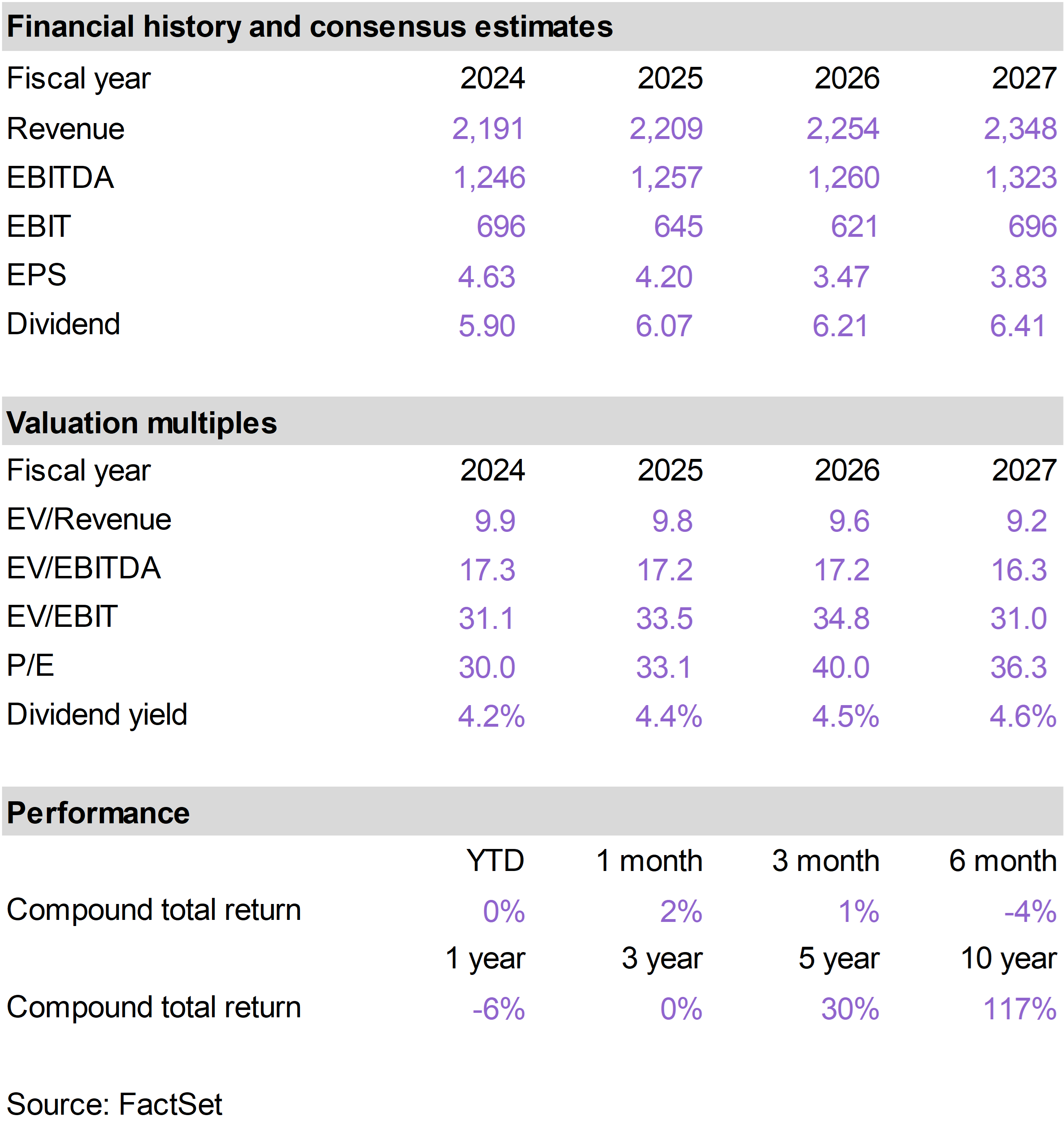

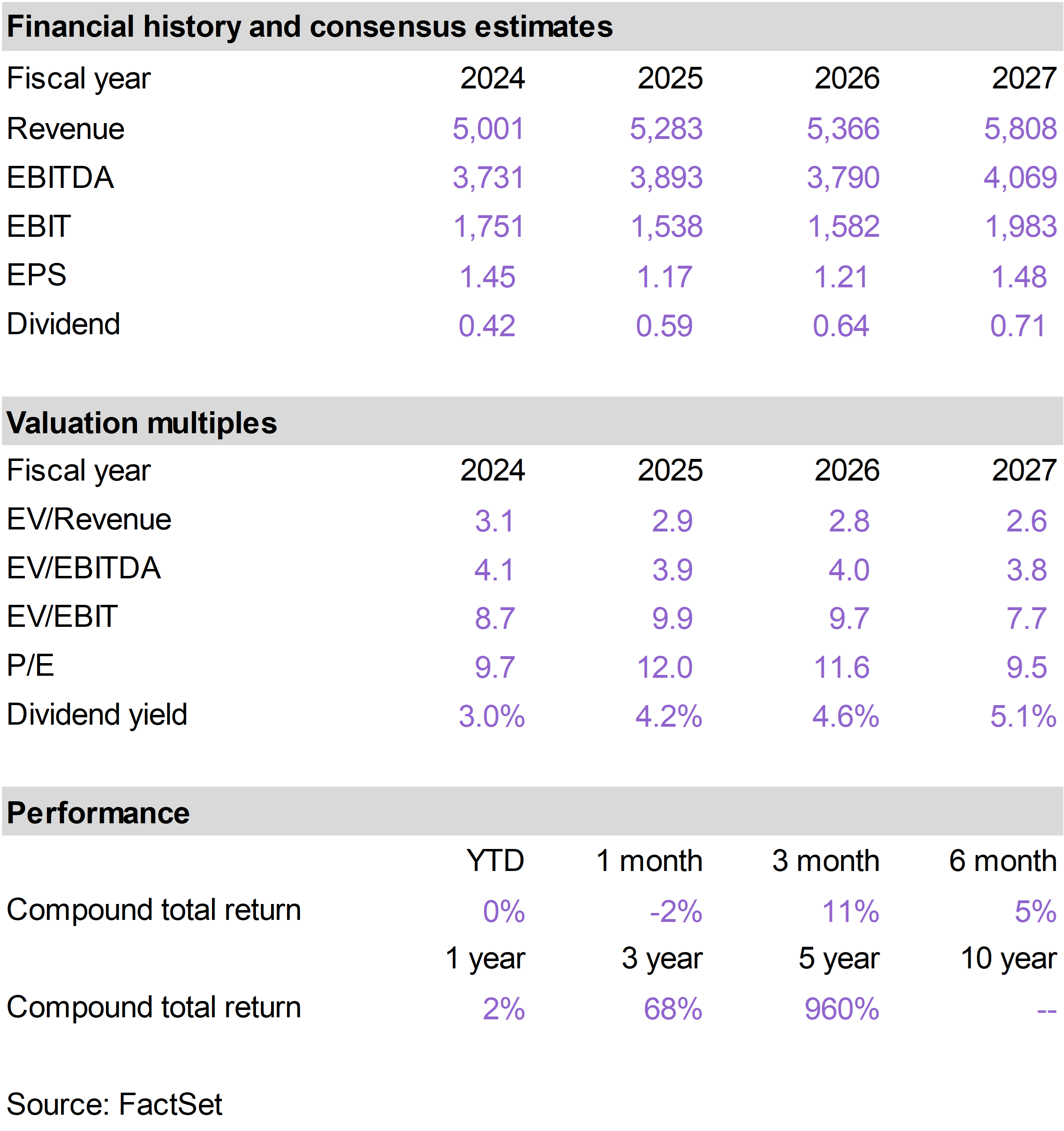

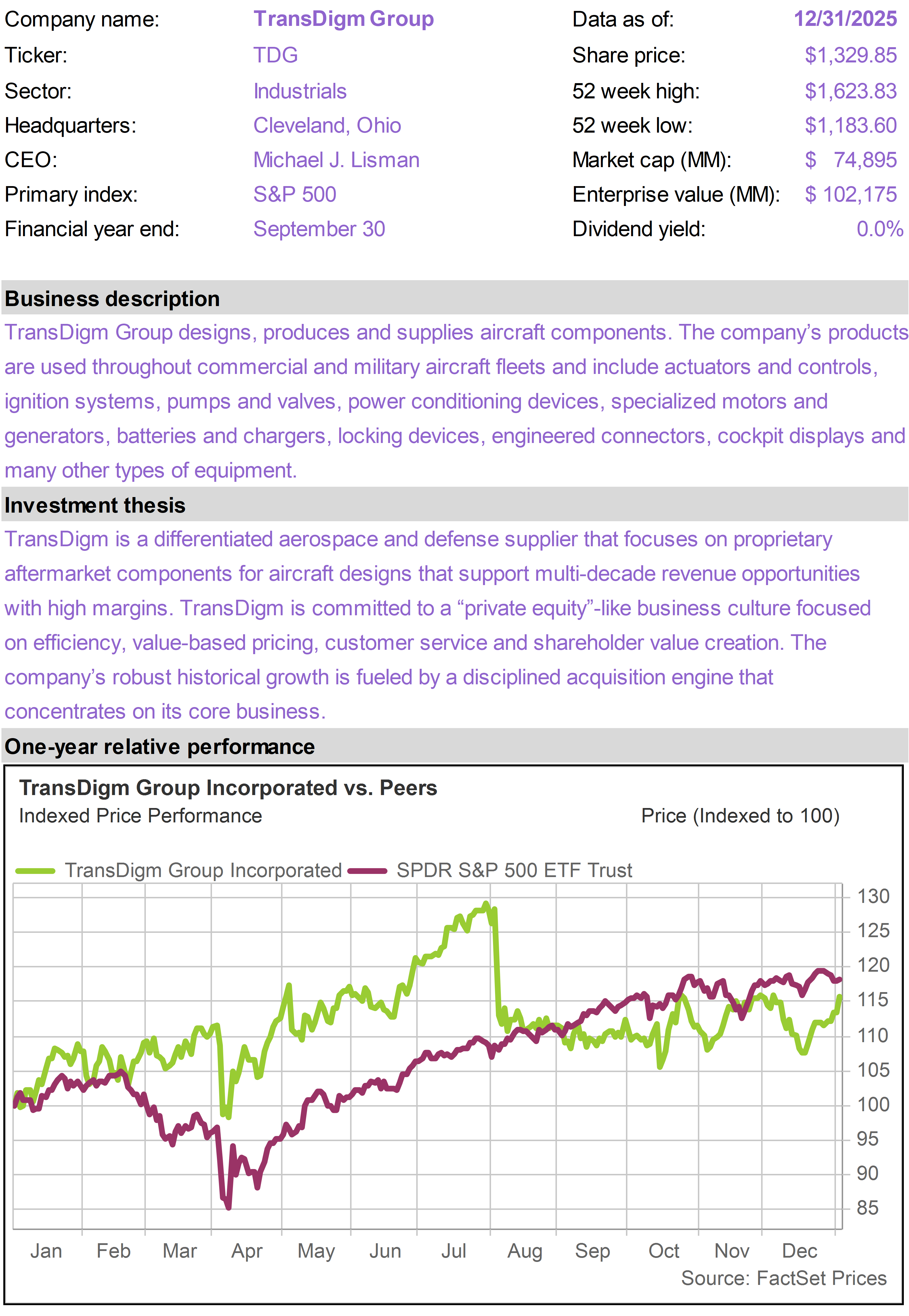

| | WESCO International (WCC) |

|

|

|

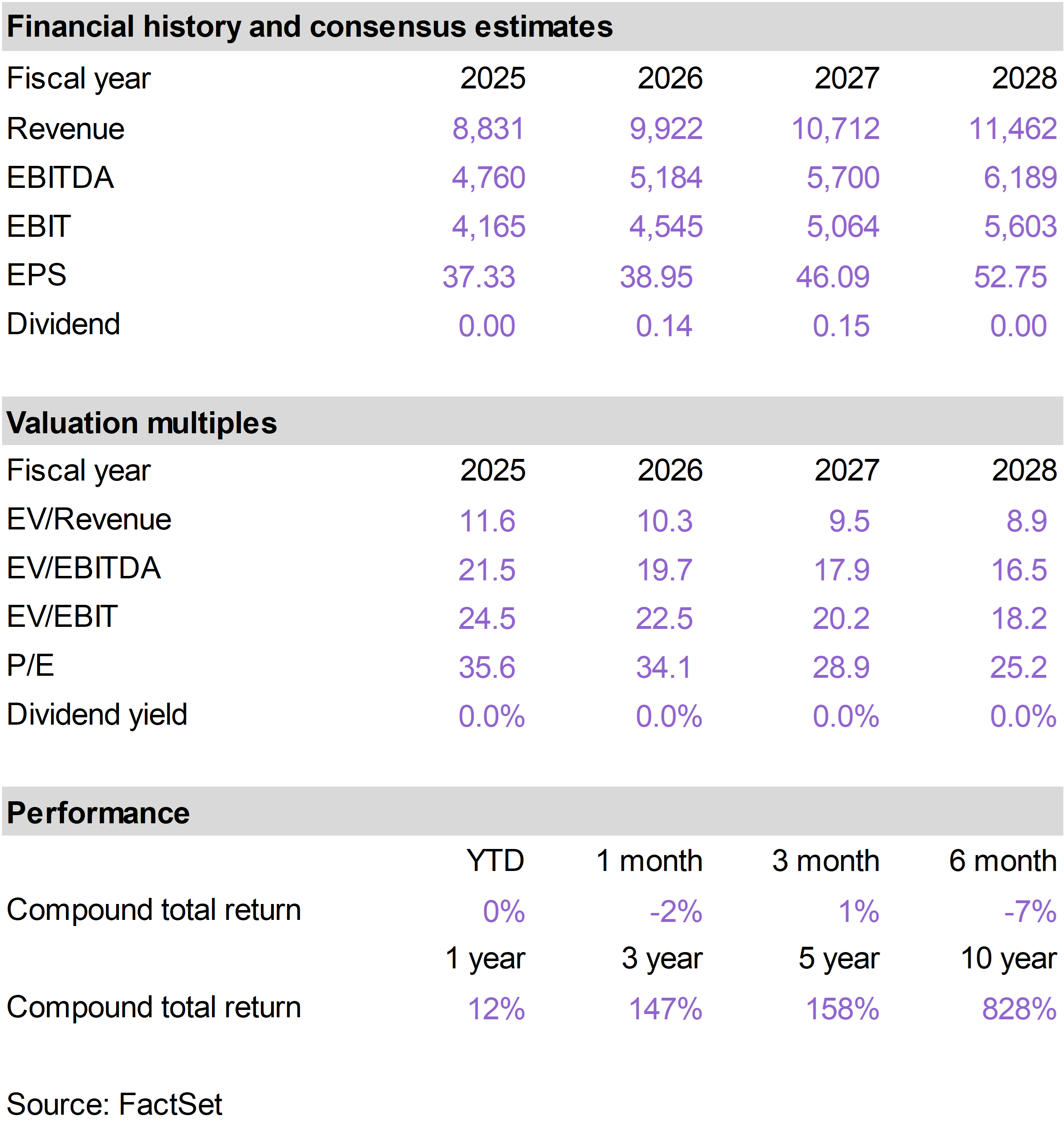

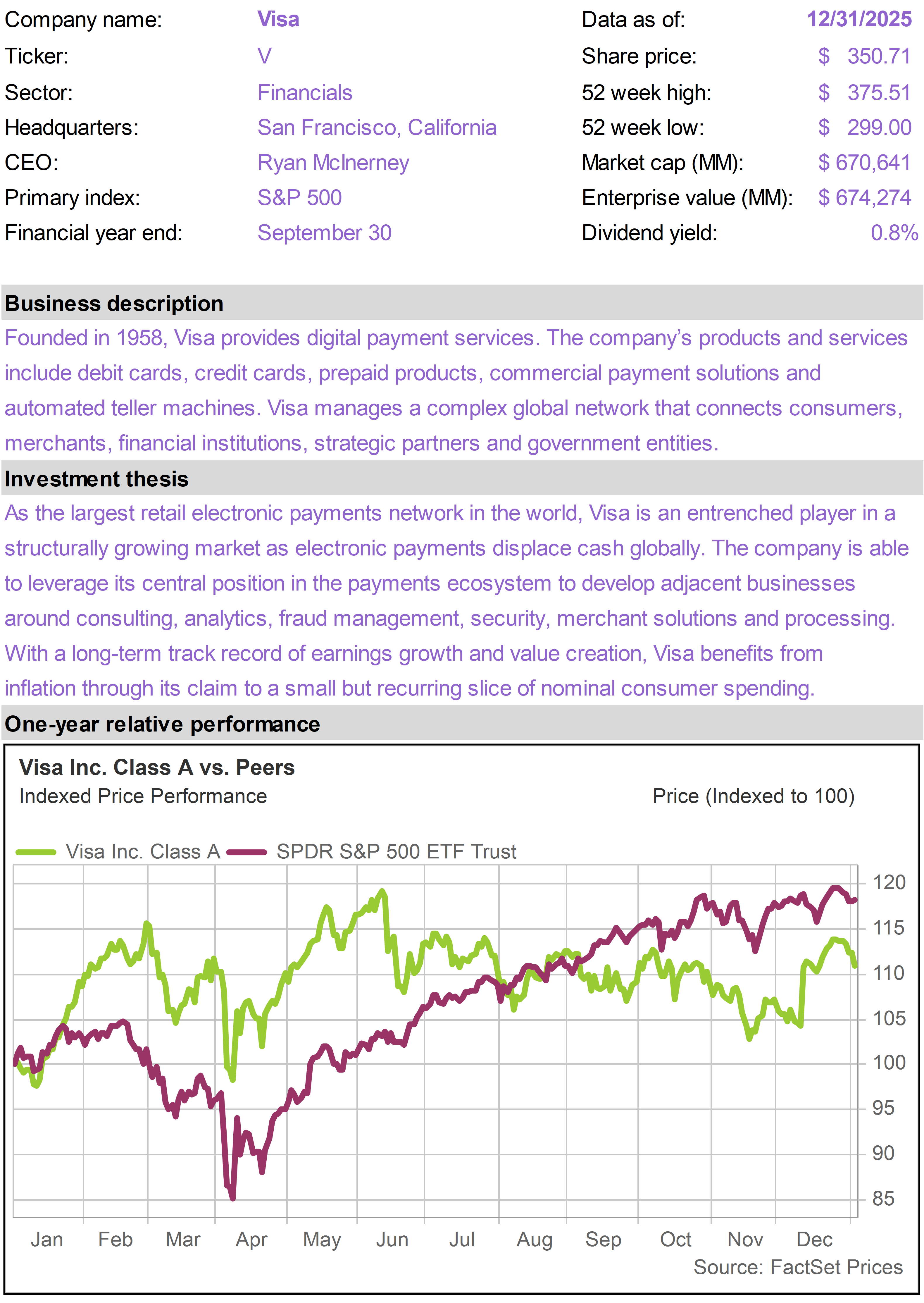

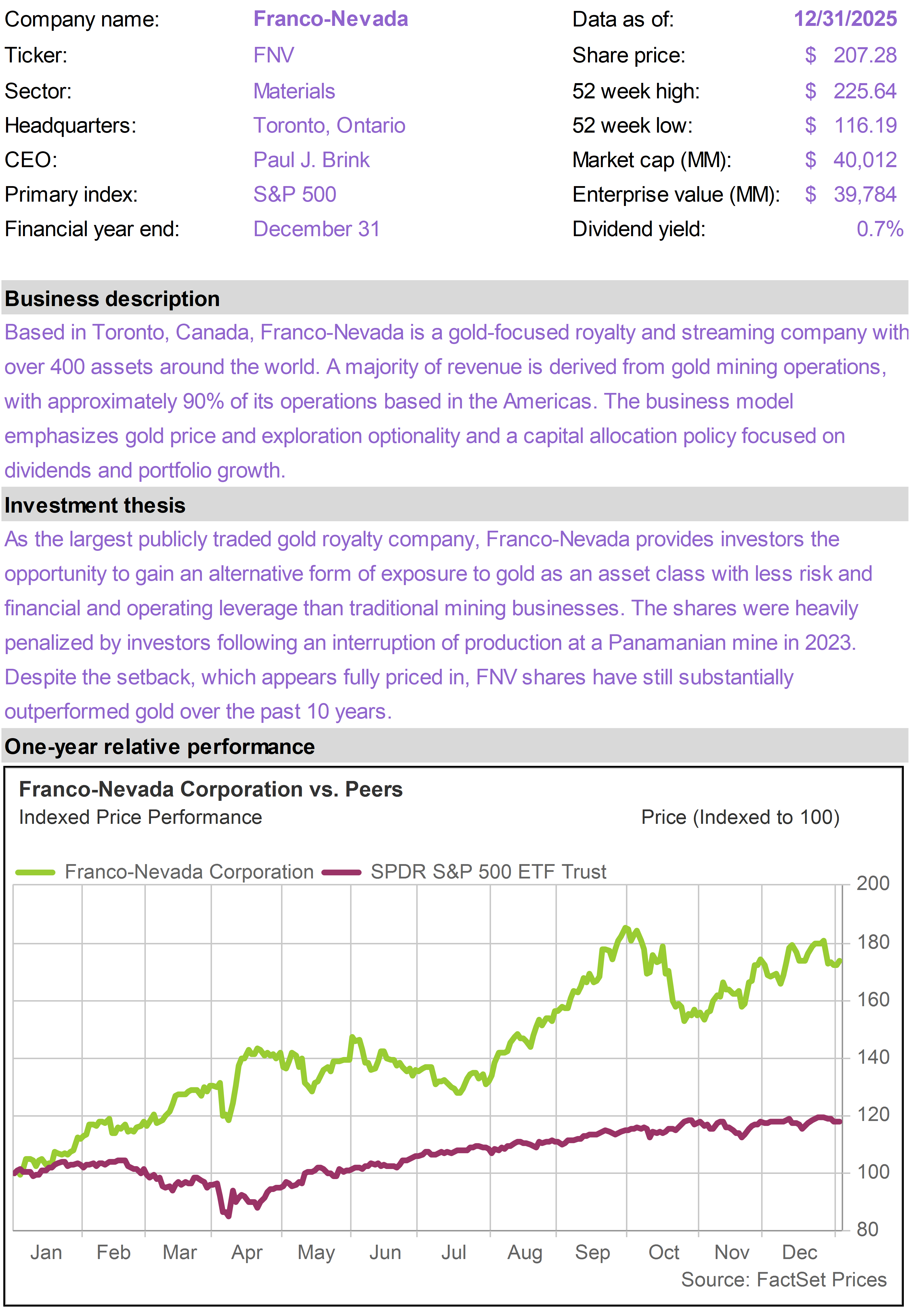

| | Wheaton Precious Metals (WPM) |

|

|

|

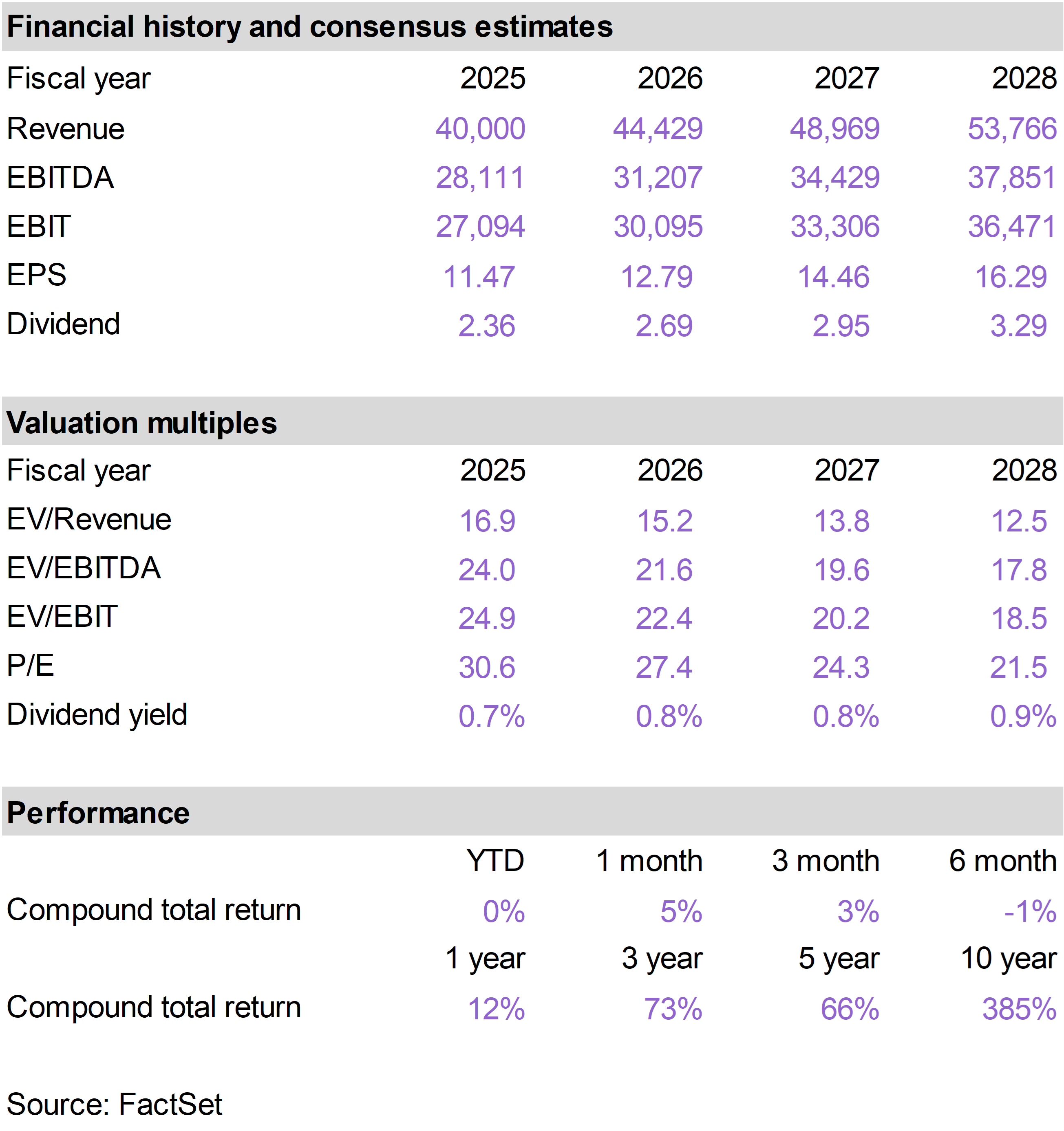

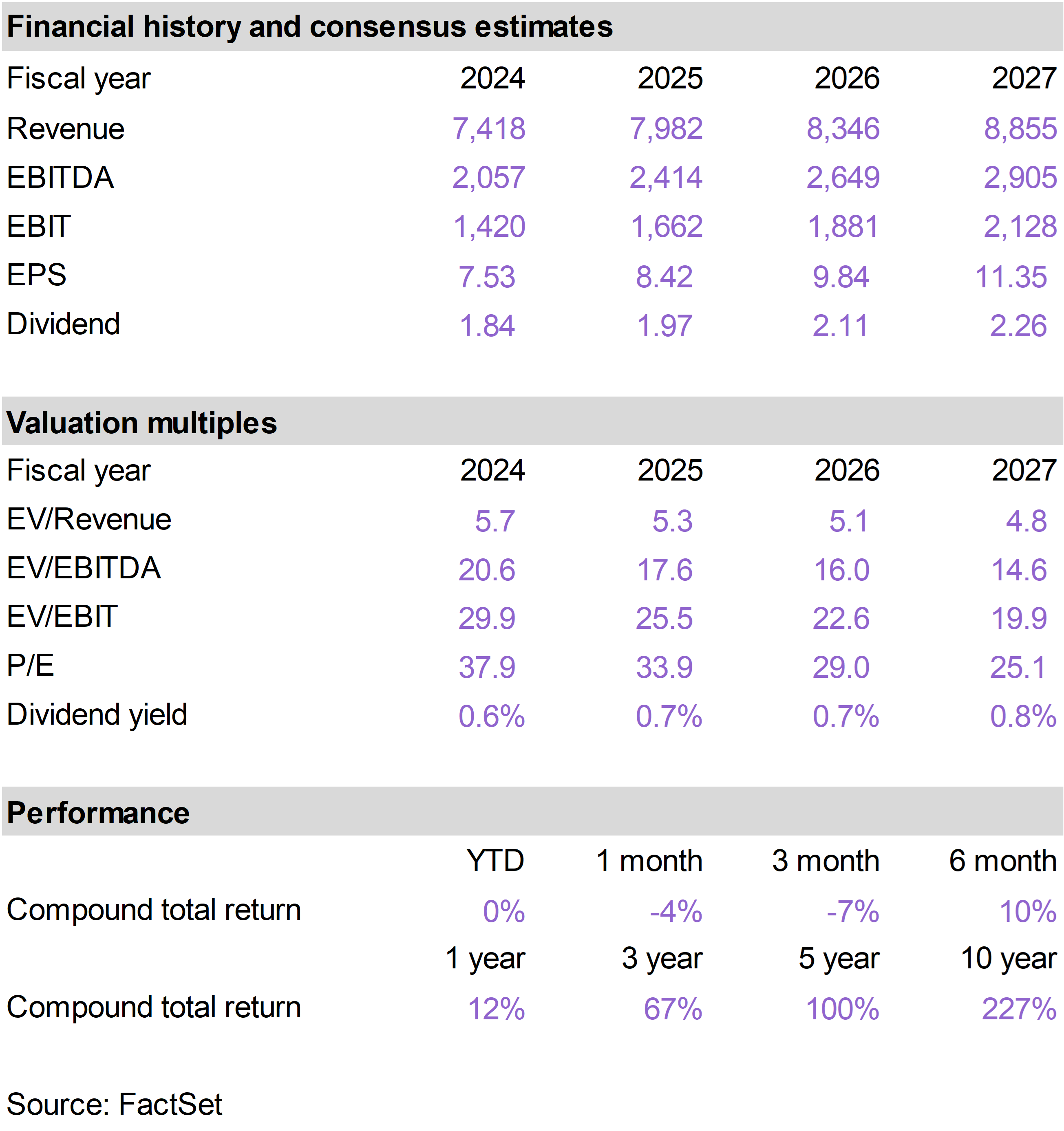

| | The 76research Inflation Protection Model Portfolio emphasizes business models that benefit from inflationary pressure. Holdings are typically selected from industries based on supply constrained real assets, including commodity and energy businesses, or companies that otherwise demonstrate superior pricing power. Drawing from an investable universe of expected inflation beneficiaries, specific holdings are chosen based on valuation and general business quality, growth and risk considerations. |

|

| | FOR SUBSCRIBER USE ONLY. DO NOT FORWARD OR SHARE. |

|

| | | |

|

|

|

|

| |

|