It makes perfect sense that spot oil prices are relatively high at the moment. Event though Iran’s military capabilities have been almost entirely destroyed, they do still have some capacity to threaten commercial vessels in the Strait of Hormuz.

From the standpoint of the vessels’ owners, insurers and crew, even a small risk may not be worth taking. So oil remains trapped in the Persian Gulf, driving up spot prices.

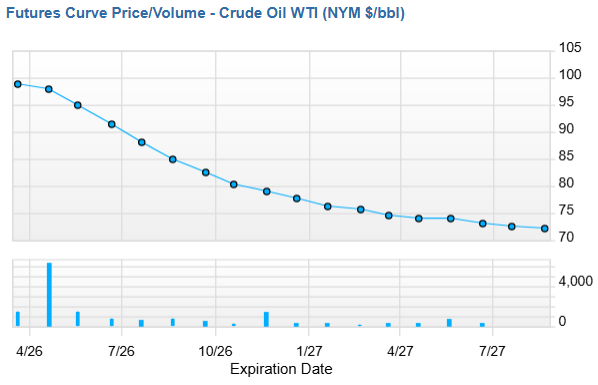

What oil futures are clearly telling us, however, is that the situation will eventually get sorted out.

The U.S. has completely dominated Iran from a military perspective, virtually eliminating its air force, navy and senior leadership. It is just a matter of time before the regime will no longer be able to credibly threaten the flow of goods through the Strait of Hormuz (or the regime falls or surrenders).

While the world waits for traffic to flow through the Strait again, alternative methods of supplying oil to the world are being activated.

The Saudi East-West Pipeline (Petroline) is among the most significant. The Petroline is expected to move from 2 million to 7 million barrels per day, which makes a big dent in the 20 million barrel deficit created by the effective closure of the Strait.

Long-term implications

Oil will not stay trapped in the Persian Gulf forever, but the current situation does complicate the short-term inflation picture. Right or wrong, the Fed as it is currently constituted would prefer to wait and see if this leads to incremental inflation pressure.

But for long-term investors, what really matters is where oil settles once the dust is cleared. And as so often happens across commodities, short-term spikes produce a supply response that increases long-term capacity.

We entered this conflict with oil prices quite low, with WTI Crude having fallen through $60 per barrel late last year and into January of this year (before U.S. naval assets started getting positioned in the Middle East).

Forecasts of future oil prices vary as always, but many leading firms still expect oil surplus conditions to return by the end of this year.

In addition to the Strait of Hormuz fully reopening, which we see as just a matter of time, there is also the possibility of a new regime (or a much more compliant version of the old regime) eventually ramping up Iran’s future contributions to world oil markets.

A similar dynamic may already be underway in Venezuela, which has the opportunity to reinvest in its oil output with American support. This may be what President Trump was alluding to when he offered his own long-term price forecast for oil yesterday.