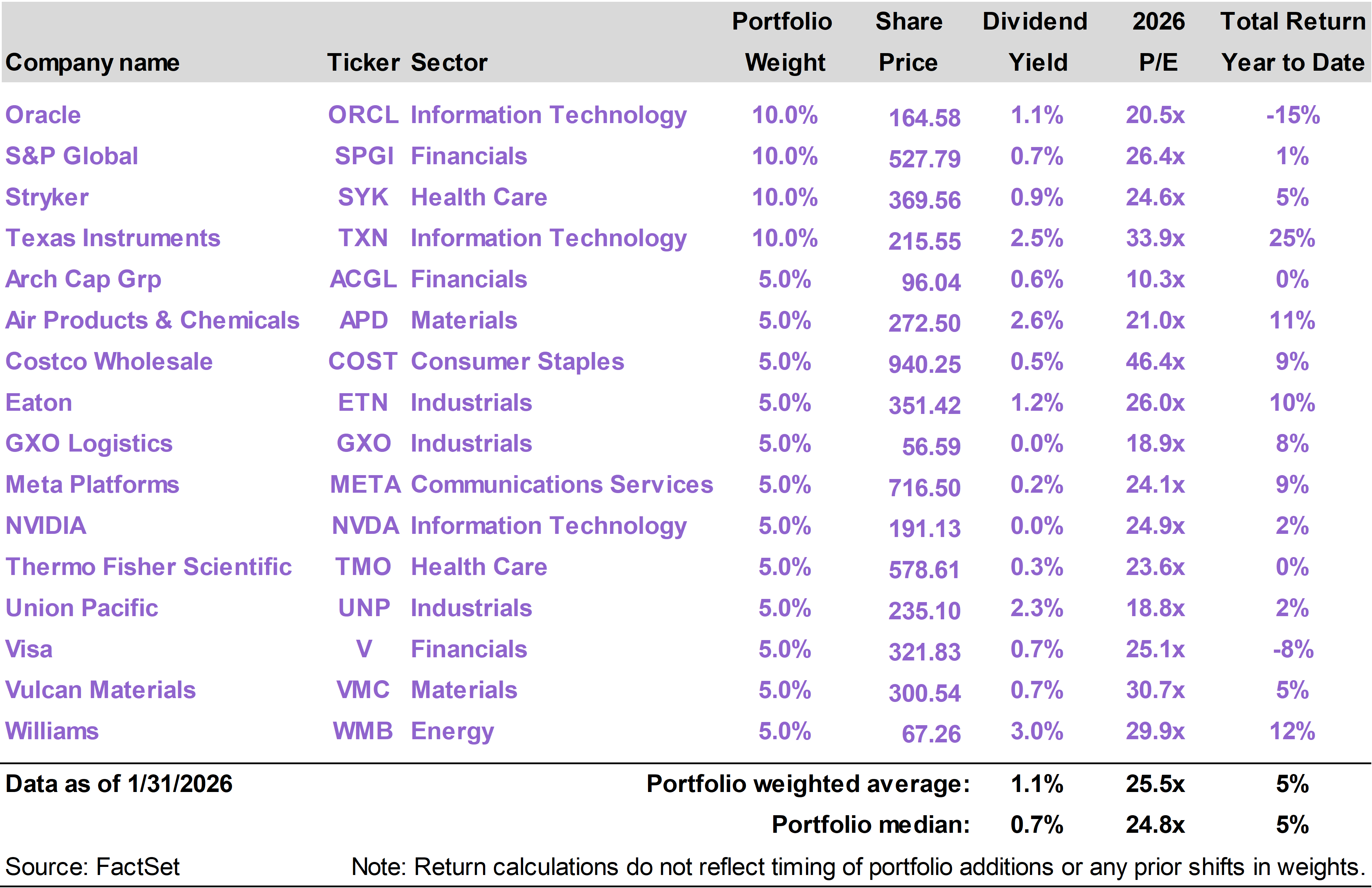

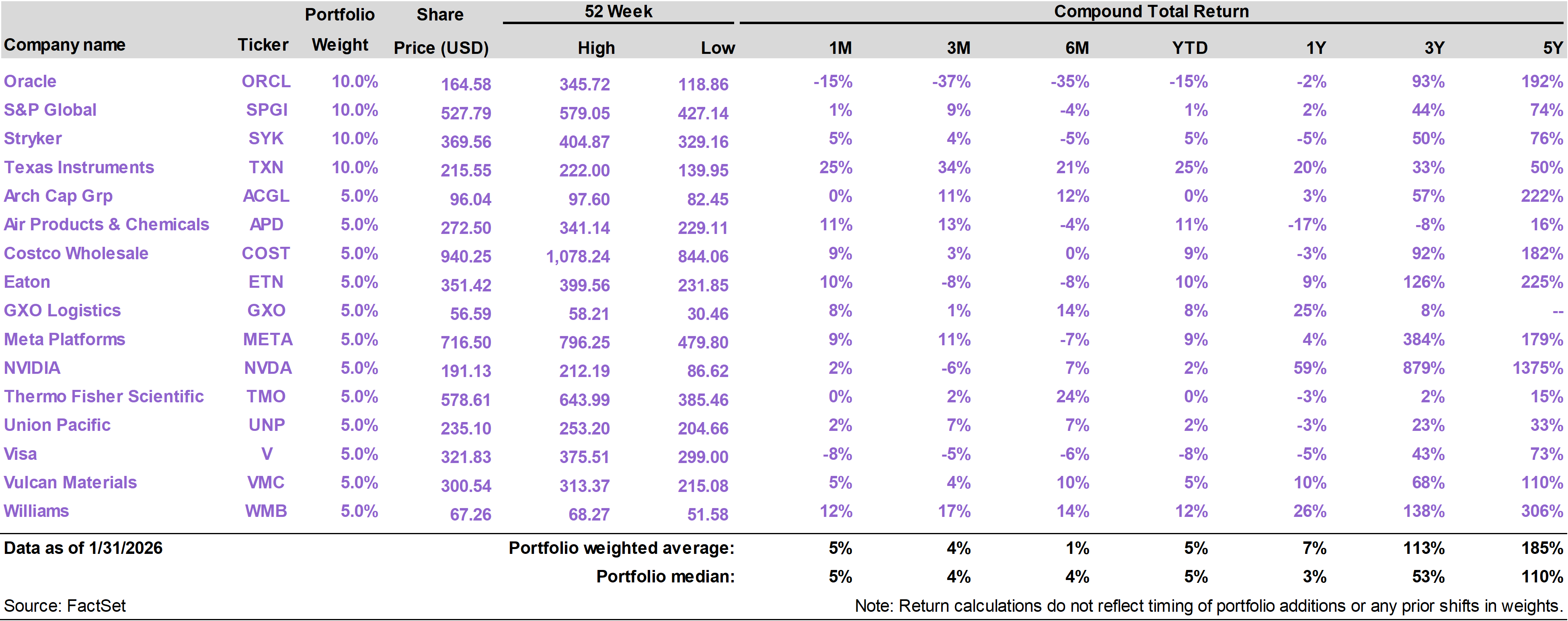

TXN shares performed quite well this month on the heels of a strong fourth quarter earnings report.

Results and guidance point to revenue growth running ahead of normal seasonality, supported by improving order trends, better bookings visibility, and rising activity across core analog and embedded chip markets. Management also struck a confident tone on margins, with improved factory utilization and mix driving upside.

Data center exposure is now emerging as a meaningful incremental growth driver, while the industrial and automotive segments still have room to recover toward (and potentially above) prior peaks.

Capital intensity is beginning to roll over, setting up the long-awaited inflection in free cash flow. Historically, the combination of above-trend growth and accelerating free cash flow has been a powerful catalyst for TXN shares.

We have been bullish on TXN because of falling capital expenditure (as multi-year capacity expansions wind down) and long-term structural exposure to AI-driven demand via data centers, robotics, automation, and autonomous vehicles.

TXN has been held back in recent quarters by cyclical pressures in the industrial segment, but the latest earnings report suggests this is diminishing as a headwind.

WMB performed well in January as investors continue to appreciate how its growth story is evolving beyond traditional gas pipelines.

The market is increasingly focused on WMB’s expanding role in supplying natural gas-powered electricity to data centers and other large power users, an area seeing rapid and durable demand growth. These projects are typically long-term and contract-based, giving WMB visible cash flows rather than exposure to volatile commodity prices.

At the same time, the core pipeline network, especially along the East Coast, is benefiting from rising gas demand tied to electricity generation, LNG exports, and regional capacity constraints. Management has recently signaled confidence in sustaining faster cash flow growth over the coming years, which will likely be discussed at its annual Investor Day next week.

WMB announced a 5% increase in its dividend on January 27. The company has paid a dividend every quarter since 1974.

APD gained momentum in January as investors focused on improving near-term fundamentals alongside the company’s longer-term reset.

A key driver was a favorable backdrop for U.S. refiners, where cheaper heavy crude from Venezuela has encouraged higher refinery utilization. Refineries are major customers for its hydrogen business, supporting higher volumes and better operating leverage in the Americas.

With a sharper focus on cost control, productivity gains, and disciplined capital allocation following recent project scrutiny, APD looks like a business with downside increasingly contained and multiple paths to improving cash flow.

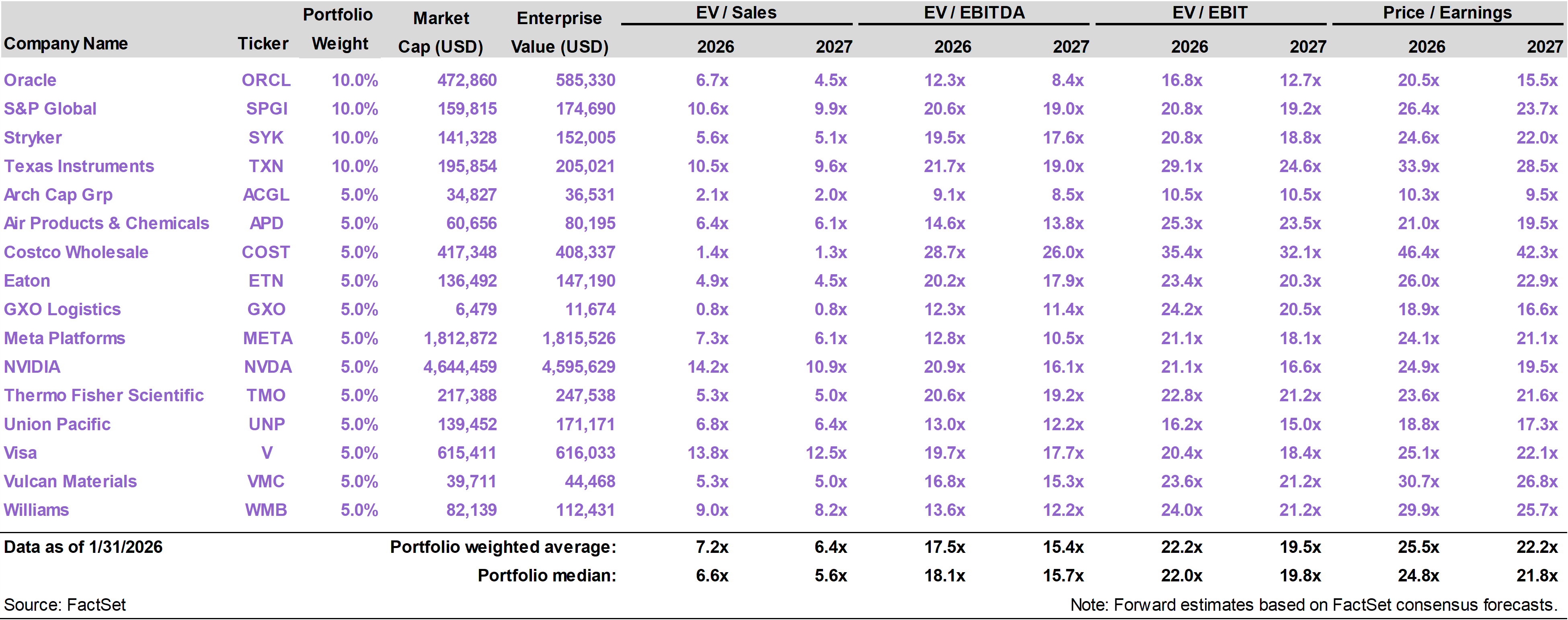

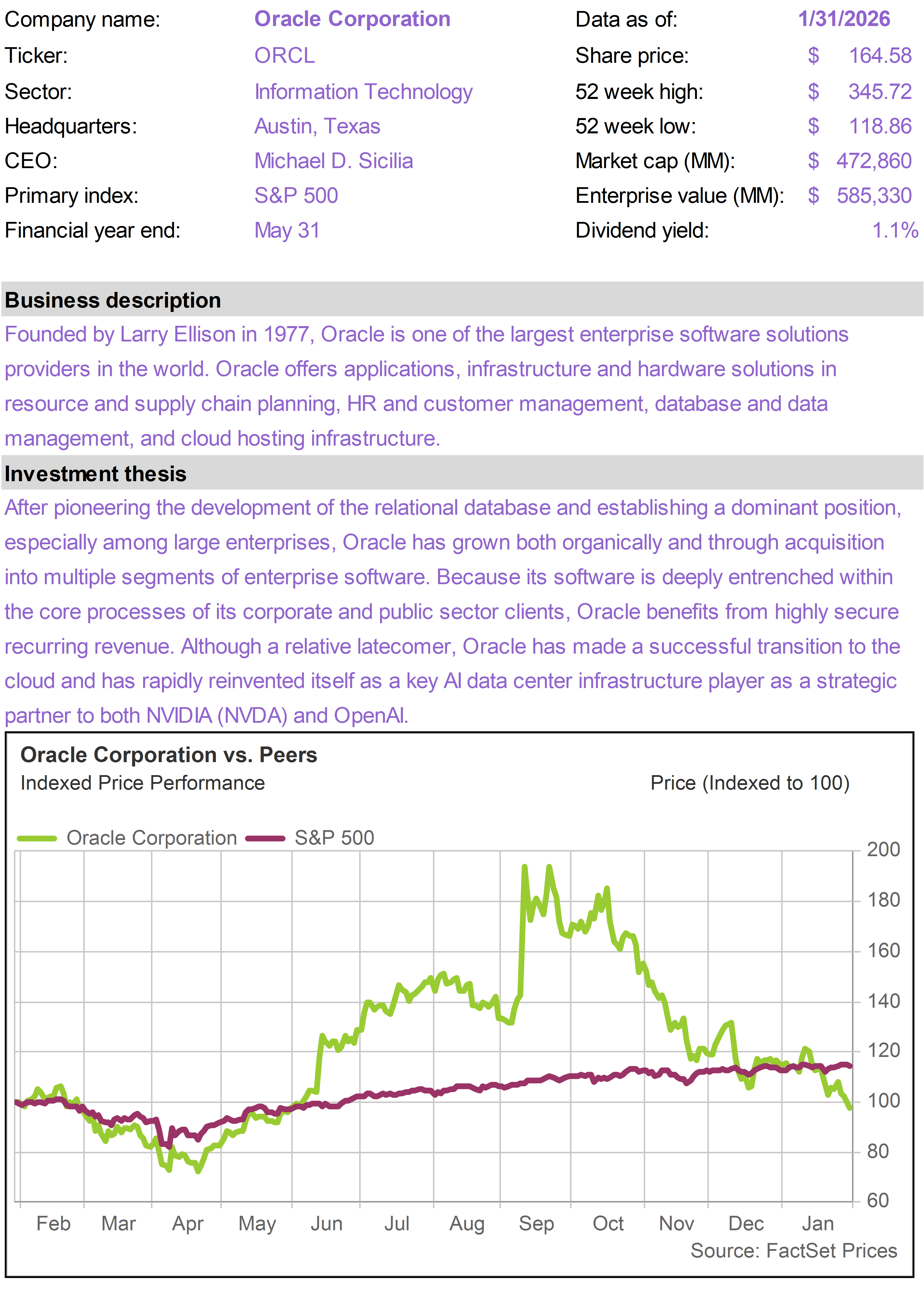

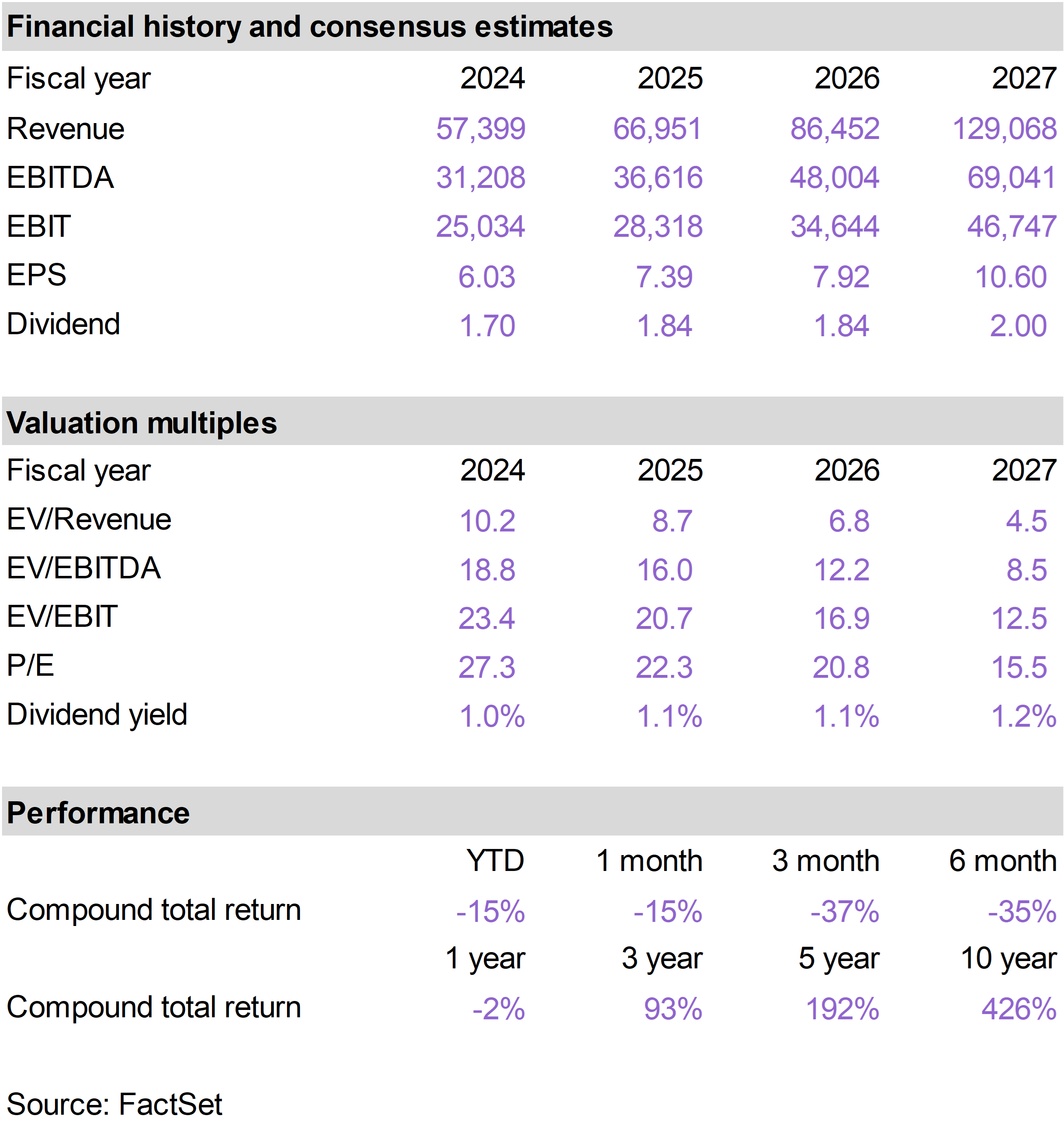

ORCL shares declined as investors have become increasingly skeptical of its capital intensive AI infrastructure strategy. Valuation here has once again become compelling, with the company now trading at less than 11x the fiscal 2028 consensus earnings forecast.

The market is arguably mispricing both of ORCL’s major businesses.

When broken apart, the company’s core applications and database segment warrants a much higher valuation given its durable, low-growth but very high-margin profile. Separately, the cloud infrastructure business is growing rapidly and is being valued at a steep discount to comparable cloud and AI-infrastructure peers, despite strong revenue growth and improving scale economics.

Much of the current expense and debt burden is tied to building out cloud capacity, which temporarily obscures underlying profitability. As cloud growth accelerates and utilization rises, margins and earnings power should improve meaningfully.

Viewed through either lens, the combined valuation does not reflect the long-term earnings and cash-flow potential embedded in the business.

Shares of V were negatively affected by Trump’s proposed plan to cap credit card interest, which could have a marginally negative impact on transaction volumes if implemented.

V also reported earnings at the end of the month. Consumer spending has proven resilient, cross-border volumes continue to grow, and higher value services such as value-added services and commercial payments are expanding rapidly.

Management reaffirmed its full year outlook. With strong volume growth, powerful network effects, and multiple secular growth drivers layered on top of a high-margin base business, V’s long-term earnings power and cash flow profile remain very attractive, even after a choppy start to the year.

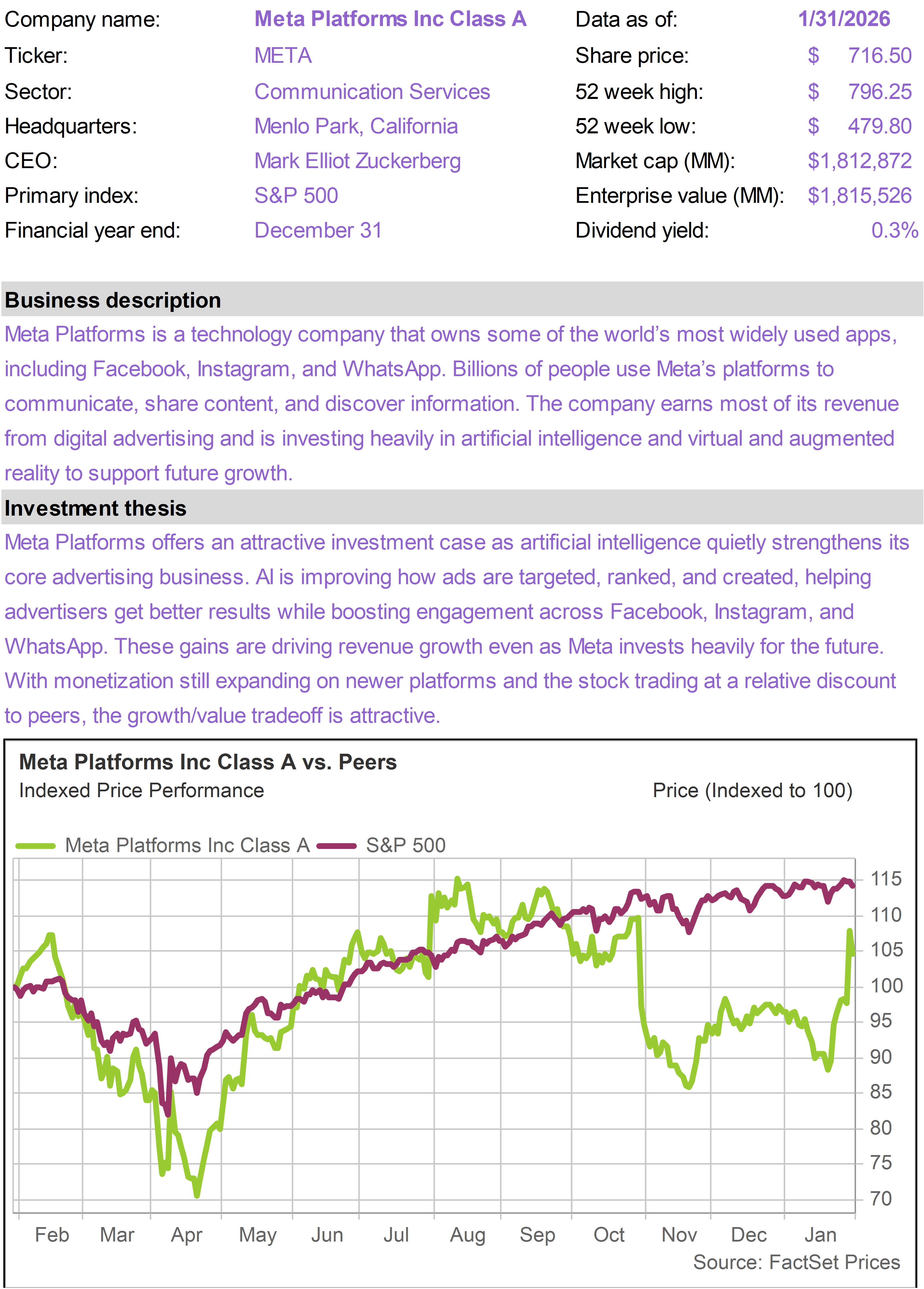

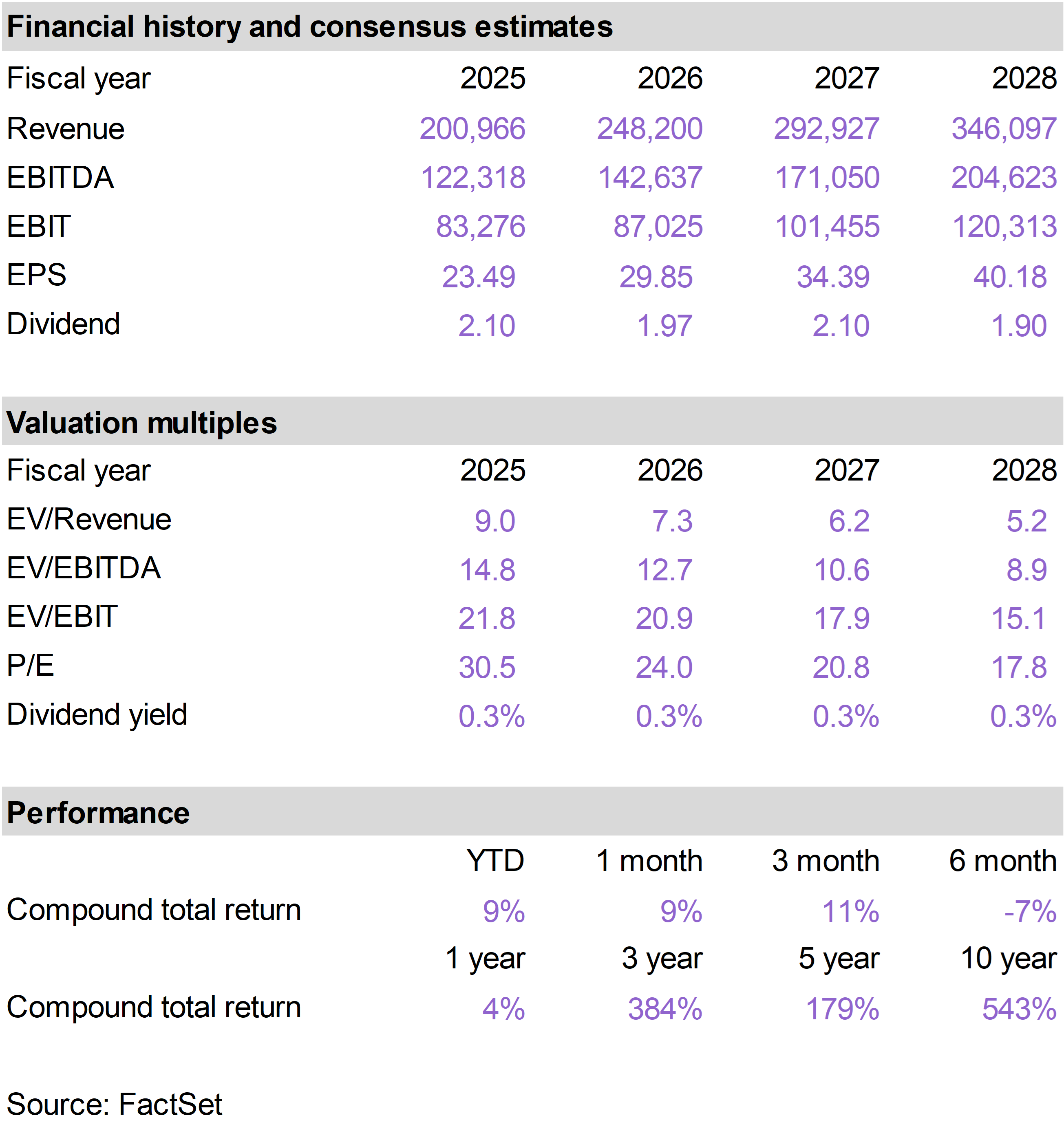

As noted in our portfolio update on January 15, Meta Platforms (META) replaced Roper Technologies (ROP) as a 5% position. Shares of META advanced approximately 15% since then through the end of the month. The upside in META followed impressive fourth quarter results in the final week of January, as discussed in the latest installment of The MAG7 MONITOR.